Access the latest CBSE Class 11 Accountancy Introduction to Accounting Worksheet Set 07. We have provided free printable Class 11 Accountancy worksheets in PDF format, specifically designed for Chapter 1 Introduction to Accounting. These practice sets are prepared by expert teachers following the 2025-26 syllabus and exam patterns issued by CBSE, NCERT, and KVS.

Chapter 1 Introduction to Accounting Accountancy Practice Worksheet for Class 11

Students should use these Class 11 Accountancy chapter-wise worksheets for daily practice to improve their conceptual understanding. This detailed test papers include important questions and solutions for Chapter 1 Introduction to Accounting, to help you prepare for school tests and final examination. Regular practice of these Class 11 Accountancy questions will help improve your problem-solving speed and exam accuracy for the 2026 session.

Download Class 11 Accountancy Chapter 1 Introduction to Accounting Worksheet PDF

Department of Commerce and Humanities

Introduction to

Accounting (NOTES)

♦ Definition of Accounting

According to the American Institute of Certified Public Accountant “ Accounting is the art of recording, Classifying and summarizing in a significant manner and in terms of money; transactions and events, which are in part at least of a financial character and interpreting the results there of.” AICPA

Attributes / Characteristics / Features of Accounting

1. Identifying Financial Transactions and Events:

• It is the process of determining which transactions are to be recorded.

• Accounting records only those transactions which are of financial nature.

• For eg: Purchase of raw materials or sale of goods.

2. Measuring the Identified Transactions:

• Accounting measures the transactions and events in terms of a common measurement units i.e. the currency of the country.

• For eg. Purchase of goods for Cash Rs. 2,00,000.

3. Recording:

• Recording is the process of recording business transactions of financial character in the books of original entry i.e. Journal.

• Journal is further sub-divided into subsidiary books such as Cash Book, Purchase Book, Sales Book etc.

4. Classifying:

• Classifying is a process of collecting similar transactions at one place by opening accounts in the Ledger Book.

• This book contains individual account heads under which all financial transactions of similar nature are collected

• For eg. Rahul’s account, Purchase account etc.

5. Summarizing:

• It involves presenting the classified data in a manner which is understandable and useful to internal as well as external users of accounting statements.

• This process leads to preparation of following statements:

a. Trial Balance

b. Income Statement (Trading and Profit and loss Account)

c. Position Statement ( Balance sheet)

• They are collectively known as Final Accounts or Financial Statements.

6. Analysing and Interpretation:

• Financial data is analyzed and interpreted so that the users of financial data can make a meaningful assessment of the financial performance (profit) and financial position of the business.

7. Communicating:

• Finally accounting involves communicating the financial statements to its users (Internal and External).

♦ Branches of Accounting

1. Financial accounting

2. Cost Accounting

3. Management Accounting

4. Forensic Accounting

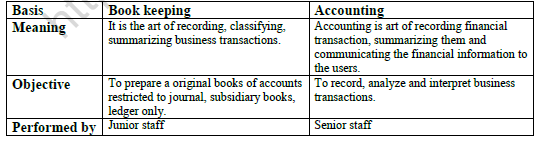

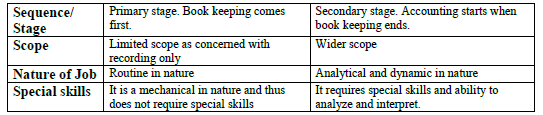

♦ Book Keeping

Book Keeping is a part of accounting and is concerned with the recording of financial data in the books of accounts.

→ Difference between Book Keeping and Accounting

♦ Objectives of accounting

1) Record of financial Transactions and events:

• The objective of accounting is to record financial transactions and events of the organization in the books of account in a systematic manner following the principles of accountancy.

2) Determining Profit or Loss:

• Another objective of accounting is to determine the financial performance i.e profit earned or loss incurred for the accounting period.

• A statement called Profit and loss account is prepared.

3) Determining Financial Position:

• Another objective of accounting is to determine financial position.

• A statement called position statement or the balance sheet is prepared.

4) Accounting assists the management by providing financial information to it:

• The management requires financial information for decision making, exercising control, budgeting and forecasting.

5) Communicating :

• Another objective of accounting is to provide accounting information to users who analyze them as per their individual requirements.

6) Protecting Business assets:

• Another objective is to have records of assets owned by the business.

• It helps the management to protect them and exercise control.

♦ Role / Functions of accounting

1) Maintaining a systematic Accounting Records:

• To Maintain systematic accounting records of financial transactions and events.

• It means accounting should be maintained following the accounting rules, principles and concepts.

2) Preparation of financial statements:

• Financial statement means final accounts prepared at the end of the accounting period.

• It includes Income statement and Position statement

• It is a important function as it shows the financial performance (profit earned or loss incurred) and position of the accounting year.

3) Meeting Legal requirements:

• Accounting records are accepted as evidence by the court of law if they are maintained systematically following the accounting rules, principles and concepts.

• Thus it is the function of accounting to meet legal requirements.

4) Communicating the financial information:

• Another function of accounting is to communicate the financial information to the users which may be internal as well as external users.

• Such as Banks, Employees, Government etc.

5) Assistance to management:

• Management often requires financial information which is given by the accounting records which in turn helps the management in decision making.

• It will also help the management in protecting the assets and exercising control.

♦ Advantages

1) Financial information about business:

• Financial performance during the accounting period i.e. profit earned or loss incurred and also the financial position at the end of the accounting period is known through accounting.

2) Assistance to management:

• The management makes the business plans, takes decisions and exercises control over the affairs on the basis of accounting information.

3) Replaces memory:

• A systematic and timely recording of transactions obviates the necessity to remember transactions.

• The accounting provides the necessary information.

4) Facilitates comparative study:

• A systematic record enables a businessman to compare one year’s results with those of others years and locate significant factors heading to change.

5) Facilitates settlement of tax liabilities:

• A systematic accounting record immensely helps in settlement of income tax, sales tax,VAT and excise duty liabilities, since it is good evidence of the correctness of transactions.

6) Facilitates loans:

• Loans are granted by the banks and financial institutions on the basis of growth potential which is supported by the performance.

• Accounting makes available the information with respect to performance.

♦ Limitations

1) Accounting is not fully exact:

• Although most of the transactions are recorded on the basis of evidence such as sale or receipt of cash yet some estimates are also made for ascertaining profit or loss.

• Examples are providing for depreciation etc.

2) Accounting does not indicate the realizable value:

• The Balance sheet does not show the amount of cash which the firm may realize by the sale of all the assets.

• This is because many assets are not meant to be sold but for use.

3) Accounting ignores the Qualitative elements:

• Since accounting is confined to monetary matters only, qualitative elements like quality of staff, industrial relations and public relations are ignored.

4) Accounting ignores the effect of price level changes:

• Accounting statements are prepared at historical cost.

• Money as a measurement unit, changes in value. It does not remain stable.

• Unless price level changes are considered while preparing financial statements, accounting information will jot show true financial results.

5) Accounting may lead to window dressing:

• The term window dressing means manipulation of accounts so as to conceal vital facts and present the financial statements in such a way as to show better position than what it actually is.

•In this situation the profit and loss account fails to provide a true and fair view of the result of operations and balance sheet fails to provide a true and fair view of the financial position.

Please click on below link to download CBSE Class 11 Accountancy Introduction to Accounting Worksheet Set B

Free study material for Accountancy

Chapter 1 Introduction to Accounting CBSE Class 11 Accountancy Worksheet

Students can use the Chapter 1 Introduction to Accounting practice sheet provided above to prepare for their upcoming school tests. This solved questions and answers follow the latest CBSE syllabus for Class 11 Accountancy. You can easily download the PDF format and solve these questions every day to improve your marks. Our expert teachers have made these from the most important topics that are always asked in your exams to help you get more marks in exams.

NCERT Based Questions and Solutions for Chapter 1 Introduction to Accounting

Our expert team has used the official NCERT book for Class 11 Accountancy to create this practice material for students. After solving the questions our teachers have also suggested to study the NCERT solutions which will help you to understand the best way to solve problems in Accountancy. You can get all this study material for free on studiestoday.com.

Extra Practice for Accountancy

To get the best results in Class 11, students should try the Accountancy MCQ Test for this chapter. We have also provided printable assignments for Class 11 Accountancy on our website. Regular practice will help you feel more confident and get higher marks in CBSE examinations.

FAQs

You can download the teacher-verified PDF for CBSE Class 11 Accountancy Introduction to Accounting Worksheet Set 07 from StudiesToday.com. These practice sheets for Class 11 Accountancy are designed as per the latest CBSE academic session.

Yes, our CBSE Class 11 Accountancy Introduction to Accounting Worksheet Set 07 includes a variety of questions like Case-based studies, Assertion-Reasoning, and MCQs as per the 50% competency-based weightage in the latest curriculum for Class 11.

Yes, we have provided detailed solutions for CBSE Class 11 Accountancy Introduction to Accounting Worksheet Set 07 to help Class 11 and follow the official CBSE marking scheme.

Daily practice with these Accountancy worksheets helps in identifying understanding gaps. It also improves question solving speed and ensures that Class 11 students get more marks in CBSE exams.

All our Class 11 Accountancy practice test papers and worksheets are available for free download in mobile-friendly PDF format. You can access CBSE Class 11 Accountancy Introduction to Accounting Worksheet Set 07 without any registration.