Get the most accurate NCERT Solutions for Class 11 Accountancy Chapter 3 Recording of Transactions 1 here. Updated for the 2026-27 academic session, these solutions are based on the latest NCERT textbooks for Class 11 Accountancy. Our expert-created answers for Class 11 Accountancy are available for free download in PDF format.

Detailed Chapter 3 Recording of Transactions 1 NCERT Solutions for Class 11 Accountancy

For Class 11 students, solving NCERT textbook questions is the most effective way to build a strong conceptual foundation. Our Class 11 Accountancy solutions follow a detailed, step-by-step approach to ensure you understand the logic behind every answer. Practicing these Chapter 3 Recording of Transactions 1 solutions will improve your exam performance.

Class 11 Accountancy Chapter 3 Recording of Transactions 1 NCERT Solutions PDF

HOTs Questions

Question. Define a journal voucher.

Answer : Preparation of accounting voucher for multiple debit and credit transaction is known as a journal voucher

Question. Give three elements of accounting voucher.

Answer : The three elements of accounting voucher are.

• Name of the company should be printed on the top

• The voucher number should be mentioned in the serial order

• Debit and credit amount should be written in figures against the amount

Question. What are the two rule to follow when changing record in assets/expenses (Losses)?.

Answer : The two rules to follow while recording differences in Assets/Expenses (Losses) are.

• A rise in an asset is debited, and the drop in the asset is credited.

• A Rise in expenses/losses is debited, and the drop in expenses/ losses is credited.

Question. State journal entries that are subdivided into a number of books of original entry

Answer : swer: The journal is subdivided into a number of books of original entry are.

• Journal Proper

• Cashbook

• Other day books:

• Purchases (journal) book

• Sales (journal) book

• Purchase Returns (journal) book

• Sale Returns (journal) book

• Bills Receivable (journal) book

• Bills Payable (journal) book

Question. Give two differences between journal and ledger.

Answer : The two differences between journal and ledger are.

• For a transaction, a journal is the initial book of entry. And the ledger is the second book of entry. • The recording process in the journal is known as journalising. The recording process in the ledger is known as posting.

Question. Which of the following is correct?

1.Liabilities = Assets + Capital 2. Assets = Liabilities – Capital 3. Capital = Assets – Liabilities 4.Capital = Assets + Liabilities.Cash/Credit sales

Answer : Capital = Assets – Liabilities

Question. Recording of a transaction in the Journal is called:

1. Casting

2. Posting

3. Journalising

4. Recording

Answer : Journalising

Chapter 3 Recording of Transactions 1

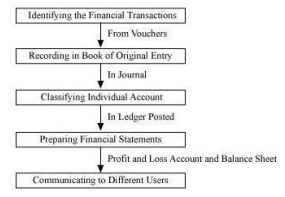

Question. State the three fundamental steps in the accounting process.

Answer : The fundamental steps in the accounting process are diagrammatically presented below.

Question. Why is the evidence provided by source documents important to accounting?

Answer : The evidence provided by the source document is important in the following manners:

1. It provides evidence that a transaction has actually occurred.

2. It provides important and relevant information about date, amount, parties involved and other details of a particular transaction.

3. It acts as a proof in the court of law.

4. It helps in verifying transactions during the auditing process.

Question. Should a transaction be first recorded in a journal or ledger? Why?

Answer : A transaction should be recorded first in a journal because journal provides complete details of a transaction in one entry. Further, a journal forms the basis for posting the transactions into their respective accounts into ledger. Transactions are recorded in journal in chronological order, i.e. in the order of occurrence with the help of source documents. Journal is also known as ‘book of original entry’, because with the help of source document, transactions are originally recorded in books. The process of recording the transactions in journal and then in ledger.

Question. Are debits or credits listed first in journal entries? Are debits or credits indented?

Answer : As per the rule of double entry system, there are two columns of ‘Amount’ in the journal format namely ‘Debit Amount’ and ‘Credit Amount’. The way of recording in a journal is quite different from normal recording. Journal entry is recorded in journal format in which the ‘Debit Amount’ column is listed before the ‘Credit Amount’ column.

Credits are indented. Indentation is leaving a space before writing any word. Journal entry has its own jargon. While journalising, in the ‘Particulars’ column of journal format, debited account is written first and credited account is in the next line leaving some space, which is indentation.

Question. Why are some accounting systems called double accounting systems?

Answer : Some accounting systems are called double accounting systems because under this system there are two aspects of every transaction, i.e., every transaction has dual effect. Every transaction affects two accounts simultaneously, that is represented by debiting one account and crediting the other account. It is based on the fact that if there is receiver, there should be a giver.

Question. Why are the rules of debit and credit same for both liability and capital?

Answer : Every business acquires funds from internal as well as from external sources. According to the business entity concept, the amount borrowed from the external sources together with the internal sources like, capital invested by the proprietor, is termed as liability to the business. Business entity concept treats business and business owner separately. Capital of the owner is treated as liability to the business because the business has to repay the amount of capital to the owner, in case of closure of the business. As liability incurred is credited, in the same way, fresh capital introduced and net profit increases the owner’s capital, and so, capital is credited. On the other hand, if liability is paid, it reduces liability, and so, it is debited. Similarly, drawings from capital and net loss reduce the capital, and so, capital is debited. Thus the rules of debit and credit are same for both liability and capital.

Question. What is the purpose of posting J.F numbers that are entered in the journal at the time entries are posted to the accounts?

Answer : J.F. number is the number that is entered in the ledger at the time of posting entries into their respective accounts. It helps in determining whether all transactions are properly posted in their accounts. It is recorded at the time of posting and not at the time of recording the transactions.

The purpose of entering J.F. number in the ledger is because of the below given benefits.

1. J.F. number helps in locating the entries of accounts in the journal book. In other words, J.F number helps to locate the position of the related journal entry and subsidiary book in the journal book.

2. J.F. number in accounts ensures that recording in the books of original entry has been posted or not.

Question. What entry (debit or credit) would you make to: (a) increase revenue (b) decrease in expense,(c) record drawings (d) record the fresh capital introduced by the owner.

Answer :

1. Increase in revenue

Increase in revenue is credited as it increases the capital. Capital has credit balance and if capital increases, then it is credited.

2. Decrease in expense

Decrease in expense is credited as all expenses have debit balance. If expense decreases, then it is credited.

3. Record drawings

Capital has credit balance; if the capital increases, then it is credited. If capital decreases, then it is debited. Drawings are debited as they decrease the capital.

4. Record of fresh capital introduced by the owner- credit

Capital has credit balance, if capital increases, then it is credited. The introduction of fresh capital increases the balance of capital, and so, it is credited.

Question. If a transaction has the effect of decreasing an asset, is the decrease recorded as a debit or as a credit? If the transaction has the effect of decreasing a liability, is the decrease recorded as a debit or as a credit?

Answer : If a transaction has a decreasing effect on an asset, then this decrease is recorded as credit.

This is because, as all assets have debit balance and if assets decrease, then it is credited. For example, sale of furniture results in decrease in furniture (asset); so, the sale of furniture will be credited.

If a transaction has a decreasing effect on a liability, then this decrease is recorded as debit. This is because all liabilities have credit balance. If the liability increases, then it is credited and if the liability decreases, then it is debited. For example, payment to the creditors results in a decrease in the creditors (liability); so, the creditors account will be debited.

Free study material for Accountancy

NCERT Solutions Class 11 Accountancy Chapter 3 Recording of Transactions 1

Students can now access the NCERT Solutions for Chapter 3 Recording of Transactions 1 prepared by teachers on our website. These solutions cover all questions in exercise in your Class 11 Accountancy textbook. Each answer is updated based on the current academic session as per the latest NCERT syllabus.

Detailed Explanations for Chapter 3 Recording of Transactions 1

Our expert teachers have provided step-by-step explanations for all the difficult questions in the Class 11 Accountancy chapter. Along with the final answers, we have also explained the concept behind it to help you build stronger understanding of each topic. This will be really helpful for Class 11 students who want to understand both theoretical and practical questions. By studying these NCERT Questions and Answers your basic concepts will improve a lot.

Benefits of using Accountancy Class 11 Solved Papers

Using our Accountancy solutions regularly students will be able to improve their logical thinking and problem-solving speed. These Class 11 solutions are a guide for self-study and homework assistance. Along with the chapter-wise solutions, you should also refer to our Revision Notes and Sample Papers for Chapter 3 Recording of Transactions 1 to get a complete preparation experience.

FAQs

The complete and updated is available for free on StudiesToday.com. These solutions for Class 11 Accountancy are as per latest NCERT curriculum.

Yes, our experts have revised the as per 2026 exam pattern. All textbook exercises have been solved and have added explanation about how the Accountancy concepts are applied in case-study and assertion-reasoning questions.

Toppers recommend using NCERT language because NCERT marking schemes are strictly based on textbook definitions. Our will help students to get full marks in the theory paper.

Yes, we provide bilingual support for Class 11 Accountancy. You can access in both English and Hindi medium.

Yes, you can download the entire in printable PDF format for offline study on any device.