Read TS Grewal Accountancy Class 11 Solution Chapter 15 Provisions and Reserves 2023 2024. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers of Grade 11. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in standard 11 Accounts class tests and examinations.

Class 11 Accounts Chapter 15 Provisions and Reserves TS Grewal Solutions

TS Grewal Solutions for Chapter 15 Provisions and Reserves Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2023 2024 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11. Class 11 Grewal solutions should be revised regularly as more practice will help you get a better rank and easily solve more questions.

Chapter 15 Provisions and Reserves TS Grewal Class 11 Solutions

Question.1. Explain the terms ‘Reserve’ and ‘Provision’ with examples.

Answer .1

Reserves: Reserves are the amounts set aside out of profits. It is an appropriation of profits or accumulated profits to strengthen the financial position of the business. Reserves are not set aside to meet liability depreciation in the value of assets but it is set aside to meet known or unknown contingency that may arise in future. Examples are General Reserve. Dividend Equalization Reserve. Reserve for Expansion, etc. the amount of reserve when invested in outside securities, the reserve is termed 'Reserve Fund'. But when no specific investment is made it is not called Reserve Fund but Reserve. General Reserve. Workmen Compensation Reserve and Investment Fluctuation Reserve being appropriation of profit are not shown in the Profit and Loss Account.

Provision: Provision is an amount set aside, by charging it to the Profit and Loss Account or Statement of Profit and Loss in case Of companies, to provide for a known liability the amount of which cannot be determined with accuracy. It is charged in the Profit and Loss Account on an estimate basis. In other words, a provision is a charge against profit for the purpose of providing for any liability or loss. Provision for Depreciation, Provision for Doubtful Debts, Provision for Repairs and Provision for Tax are few examples of provisions. Provision differs from liability to the extent that provision is an estimated amount while liability is determined amount. For example: providing for rent of 1,00,000 payable for the month of December is a liability, Hence, Provision is an estimated amount set aside to meet an uncertain loss or expense in future.

Question.2. Define the Provision. What is the importance of creating a provision? (Any three points of importance)

Answer.2

According to Penguin Dictionary of Commerce, "A Provision is the amount written off or retained by way of providing depreciation, renewals or diminution in the value of assets or retained by way of providing for any known liability of which the amount cannot be determined with substantial accuracy."

The following are the importance of creating provisions:

1. Provision is an amount set aside out of the current earnings considered necessary to provide for all losses that are expected to arise out of transactions entered into, during the accounting period.

2. Provision is made following the Prudence Concept of accounting which holds "provide for all anticipated expenses and losses but do not provide for anticipated incomes." By making a provision, a part of the profits and corresponding assets are retained. which otherwise could have been distributed as profits.

3. Any loss or depletion in the value of an asset or any liability as may not have been provided against income or profit would effectively erode the capital of a business. Creation of Provisions is an attempt to main the capital of business intact.

Question.2. Give any four points of distinction between Reserve and Provision. (Old Question)

Answer .2

Question.3. Explain the types of Reserves.

Answer.3

To have a better understanding of the nature and purpose of Reserves, let us classify them into different types. Reserves are generally classified into Revenue Reserves and Capital Reserves. The detailed discussion of which is given below:

1. Revenue Reserves: are set aside out of revenue profits which are available for distribution as dividend. Revenue Reserves can be classified into General Reserve and Specific Reserve.

i. General Reserve: is the amount set aside out of profits not for any specific purpose. It is available for any future contingency or expansion of business. Such reserve strengthens the financial position of the business. Example is General Reserve.

ii. Specific Reserve: is that reserve which is set aside for a specific purpose and can be utilized only for that purpose, For example, Workmen Compensation Reserve is a specific reserve because it is maintained to pay compensation to workmen. Debenture Redemption Reserve, Capital Redemption Reserve, Investment Fluctuation Reserve. etc., are other examples of Specific Reserve. It should be kept in mind that both General Reserve and Specific Reserve are set aside as appropriation.

2. Capital Reserves: are set aside out of capital profits and are normally not available for distribution as dividend. In other words, reserve created out of capital profits and which is not readily available for distribution as dividend among the shareholders is called Capital Reserve. Examples of capital reserves are:

(i) Profit prior to incorporation.

(ii) Premium on issue of shares or debentures.

(iii) Profit on redemption of debentures.

(iv) Profit on forfeiture of shares,

(v) Profit on sale of fixed assets,

(vi) Capital redemption reserve, and

(vii) Profit on revaluation of fixed assets and liabilities.

Question.4 Explain the Capital Reserve and give any two examples.

Answer.4

Capital Reserves are set aside out of capital profits and are normally not available for distribution as dividend. In other words, reserve created out of capital profits and which is not readily available for distribution as dividend among the shareholders is called Capital Reserve. Two examples of capital reserves are:

(i) Profit prior to incorporation

(ii) Premium on issue of shares or debentures

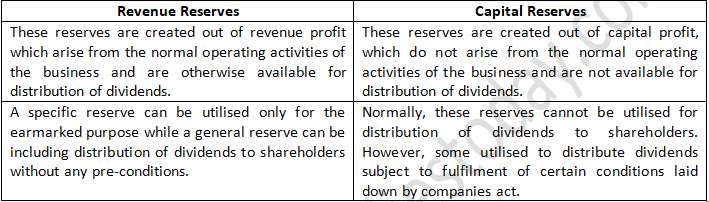

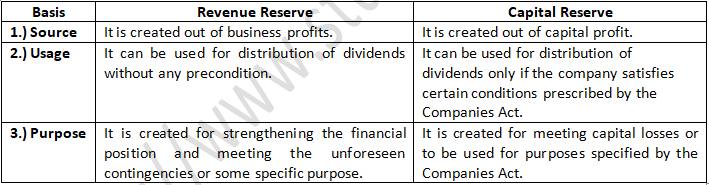

Question.5 Distinguish between ‘Revenue Reserve’ and a ‘Capital Reserve’.

Answer.5

Class 11 Accounts Chapter 15 Practical Problems Solutions

Question.6. What is a Capital Reserve? How is it different from a Revenue Reserve?

Or

Distinguish between ‘Revenue Reserve’ and a ‘Capital Reserve’ on the basis of:

(i) Source of creation

(ii) Purpose

(iii) Usage.

Answer .6

Capital Reserves are set aside out of capital profits and are normally not available for distribution as dividend. In other words, reserve created out of capital profits and which is not readily available for distribution as dividend among the shareholders is called Capital Reserve.

It is different from the revenue reserve on the following grounds:

Question.7. Is Reserve a charge against profit or an appropriation of profit? Discuss.

Answer .7 Reserves: Reserves are the amounts set aside out of profits. It is an appropriation of profits or accumulated profits to strengthen the financial position of the business. Reserves are not set aside to meet liability depreciation in the value of assets but it is set aside to meet known or unknown contingency that may arise in future. Examples are General Reserve. Dividend Equalization Reserve, Reserve for Expansion, etc. the amount of reserve when invested in outside securities, the reserve is termed 'Reserve Fund'. But when no specific investment is made it is not called Reserve Fund but Reserve. General Reserve. Workmen Compensation Reserve and Investment Fluctuation Reserve being appropriation of profit are not shown in the Profit and Loss Account.

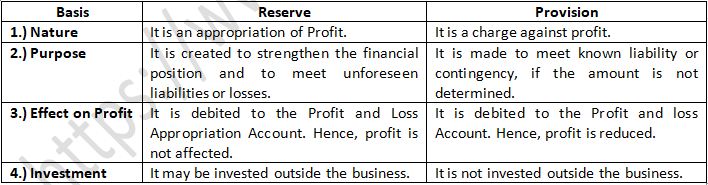

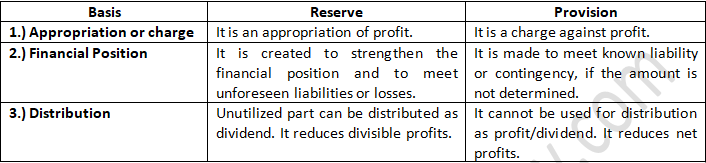

Question.8. Distinguish between Reserve and Provision on the basis of:

(i) Appropriation or charge

(ii) Financial Position

(iii) Distribution.

Answer.8

Distinguish between Reserve and Provision on the basis of:

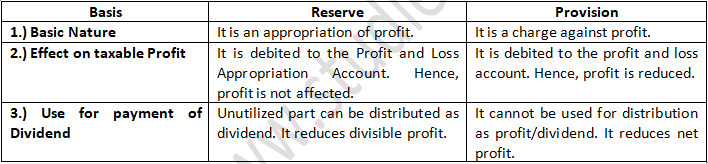

Question.9 Distinguish between Reserve and Provision on the basis of:

(i) Basic Nature

(ii) Effect on taxable Profits

(iii) Use for payment of Dividend.

Answer.9

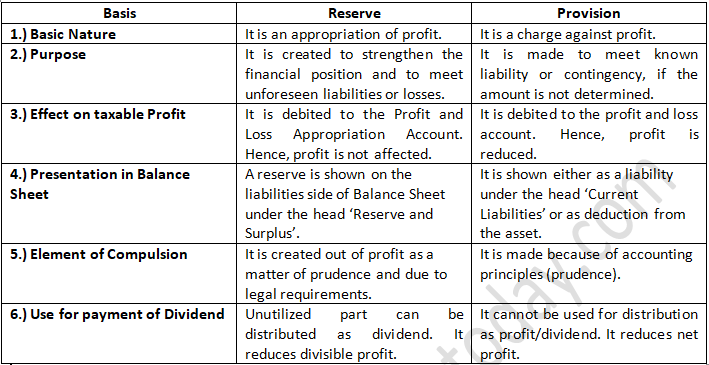

Question.10. Distinguish between Provision and Reserve on the following basis:

(i) Basic Nature

(ii) Purpose

(iii) Effect on Taxable Profit

(iv) Presentation in Balance Sheet

(v) Element of Compulsion

(vi) Use of Payment of Dividend.

Answer.10