Read DK Goel Class 11 Accountancy Solutions for Chapter 14 Trial Balance and Errors below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 14 Trial Balance and Errors should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 14 Trial Balance and Errors DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 14 Trial Balance and Errors in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 14 Trial Balance and Errors Class 11 Accountancy

Short Answer Question

Question 1. What is a Trail Balance? State any four functions of a Trail Balance.

Solution 1: According to J.R. Batliboi, "A Trial Balance is a statement, prepared with the debit and credit balances of the Ledger Accounts to test the arithmetical accuracy of the books."

Four Functions of a Trial Balance are:

(i) Ascertain the Arithmetical Accuracy of Ledger Accounts: The Trial Balance enables one to establish whether posting and other accounting processes have been carried out without committing arithmetical errors.

(ii) To Help Prepare the Final Accounts: Financial Statements are prepared from the Trial Balance. Preparation of Financial Statements, therefore, is the second objective of preparing a Trial Balance.

(iii) Summary of Each Account: The Trial Balance offers a summary of the Ledger. The Ledger may have to be referred to only when more details is required in respect of an account.

(iv) To Help in Locating Errors: The Trial Balances helps in locating errors in Book keeping work. It should, however, be borne in mind that it does not disclose all the errors in Book Keeping but only the arithmetical inaccuracies.

Question 2. Trail Balance is a link between ledger and final accounts.

Solution 2: A trial balance may be prepared at any time, at the end of every month, quarter, half-year or year. Generally it is prepared at the end of the accounting period so as to verify the arithmetical accuracy of the ledger accounts before the preparation of final accounts. It may be noted it is always prepared on a particular date and not for a particular period.

Question 3. “Is trail Balance merely a proof of Arithmetical accuracy”? Explain the errors which are not disclosed by a Trial Balance.

Solution 3:

- Errors of Principle:- When the accounting principle is violated while recording a transaction is called error of principle. For example, purchase of machinery is debited to Purchase Account, instead of Machinery Account.

- Errors of Omission:- If a transaction forgotten to record there will be no effect on the trail balance. When a transaction goes unrecorded in both aspects and a transaction after being recorded in the books of primary entry is not at all posted in the ledger. For example, Purchases of Rs. 20,000 omitted to be posted in purchases day book.

- Error of Amounts in Original Book:- If an invoice for Rs 632 is entered in Sales Book as Rs 623, the Trial Balance will come out correctly, since the debit and credit have been recorded as Rs 623. The arithmetical accuracy is there, but in fact there is an error.

- Compensating Errors:- If one account in the ledger is debited with Rs 500 less and another account in the ledger is credited Rs 500 less, these errors cancel themselves. That is, one error is neutralized by similar error on the opposite side.

Question 4. Give two examples of compensating errors.

Solution 4:

1.) Goods sold to Mr. Kumar amounted Rs. 500/- was recorded to the debit side of Mr. Kumar’s account by Rs. 50/-

2.) Mr. X paid Rs. 30,000 to Mr. Y however Mr. Y’s a/c was debited with Rs. 3,000 only.

Question 5. What is meant by error of omission? Give any one example.

Solution 5: If a transaction remains unrecorded in journal or subsidiary books is called error of omission. Example:- Purchases of Rs. 20,000 omitted to be posted in purchases day book.

Question 6. What is error of principle? Give two examples.

Solution 6: When the accounting principle is violated while recording a transaction is called error of principle. Example:

1. Purchase of Machinery is debited to purchase account instead of Machinery Account.

2. Sales of old furniture is credited to sales account instead of furniture account.

Question 7. Name four errors which cannot be disclosed by preparing a Trail Balance.

Solution 7: Below are the errors cannot be disclosed by preparing a Trail Balance:-

- Errors of Omission

- Errors of Principle

- Error of Duplication

- Compensatory errors

Question 8. What is a suspense account? When is it opened?

Solution 8: An account in which the difference in the trail balance is put till such time that errors are located and rectified. It facilitates the preparation of financial statement even when the trail balance does not tally.

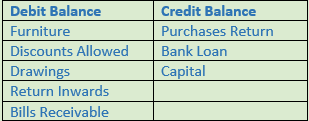

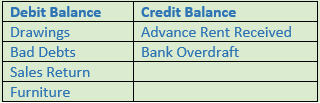

Question 9. On which side of the Trail Balance, the following Ledger balances will appear:-

Solution 9:

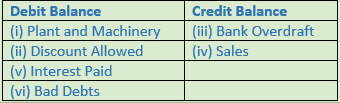

Question 10. State whether the balance of the following accounts should be placed in the debit (or) the credit columns of the Trail Balance:

Solution 10:

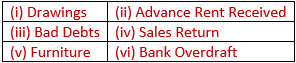

Question 11. State whether the following accounts will indicate a debit or credit balance:

Solution 11:

Question 12.

Classify the under-mentioned error into:-

(a) Error of Omission, (b) Error of Commission, (c) Compensating Error, and (d) Error of Principle:-

(i) Purchased goods from Bhardwaj on credit for Rs. 600, but were recorded in the purchases book as Rs. 6,000.

(ii) Amount paid for the proprietor’s life insurance premium was debited to ‘General Expenses Account’.

(iii) Goods amounting to Rs. 2,000 have been returned to Chakravati, but no entry has been made in the books.

(iv) An excess debit of Rs. 4,500 has been made in the account of X, whereas Y’s account has been credited by Rs. 5,000 instead of Rs. 500.

(v) Goods sold to suresh for Rs. 650 were recorded as Rs. 560 in the Sales Book.

(vi) Typewriter purchased for office use has been debited to purchases Account.

(vii) Wages paid for the construction of Building Rs. 15,000 were recorded in ‘Wages Account’.

(viii) Goods for Rs. 500 have been taken by the proprietor for his personal use, for which no entry has been passed in the books.

Solution 12:

Errors of Omission:-

(iii) Goods amounting to Rs. 2,000 have been returned to Chakravati, but no entry has been made in the books.

(viii) Goods for Rs. 500 have been taken by the proprietor for his personal use, for which no entry has been passed in the books.

Error of Commission:-

(i) Purchased goods from Bhardwaj on credit for Rs. 600, but were recorded in the purchases book as Rs. 6,000.

(v) Goods sold to suresh for Rs. 650 were recorded as Rs. 560 in the Sales Book.

Compensating Error:-

(iv) An excess debit of Rs. 4,500 has been made in the account of X, whereas Y’s account has been credited by Rs. 5,000 instead of Rs. 500.

Error of Principle:-

(ii) Amount paid for the proprietor’s life insurance premium was debited to ‘General Expenses Account’.

(vi) Typewriter purchased for office use has been debited to purchases Account.

(vii) Wages paid for the construction of Building Rs. 15,000 were recorded in ‘Wages Account’.

Question 13.

Which of the following errors will affect the trial balance?

(i) The total of the Sales Book has not been posted to the Sales Account.

(ii) Rs. 1,000 paid as installation charges of a new machine has been debited to Repairs Account.

(iii) Goods costing Rs. 4,000 taken by the proprietor for personal use have been debited to Debtors Account.

(iv) Rs. 1,000 paid for repairs to building have been debited to Building Account.

Solution 13:

In the above transactions only 1st transaction will affect the trail balance it is error of posting in one account. Transaction 2nd, 3rd and 4th will not affect the trail balance because these are error of principle.

Question 14. What is trail Balance? Does the balancing of this ensure accuracy of books of accounts.

Solution 14:

It is statement prepared with the help of ledger balances at the end of financial year to test the arithmetical accuracy of books of accounts. Balancing of trial balance does not ensure the accuracy of books of accounts. Errors which remain undetected even if trail balance agrees:

Errors of Omission:- If a transaction forgotten to record there will be no effect on the trail balance.

Errors of Commission:- When wrong amount is entered either in journal or subsidiary books.

Compensating Errors:- If the effect of one error is neutralised by the effect of some other error.

Errors of Principle:- When fundamental principle of accountancy is violated while recording a transaction.

Class 11 Accounts Chapter 14 Practical Problems Solutions

Numerical Question

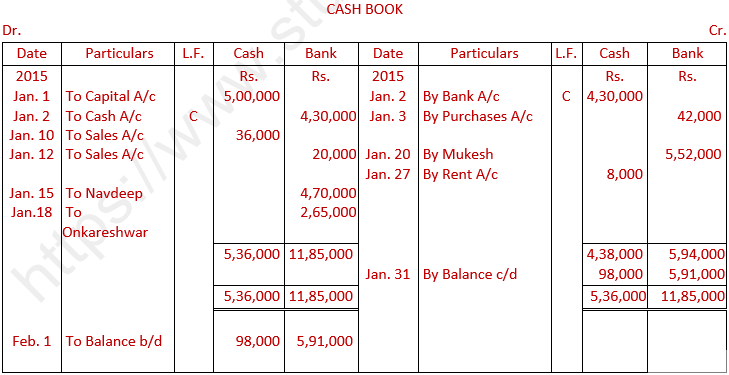

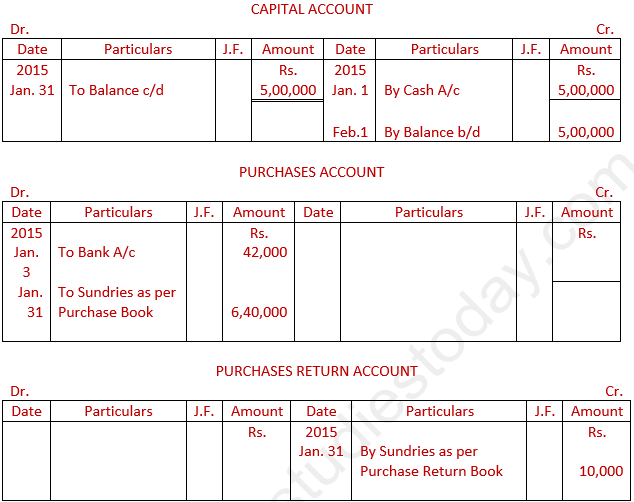

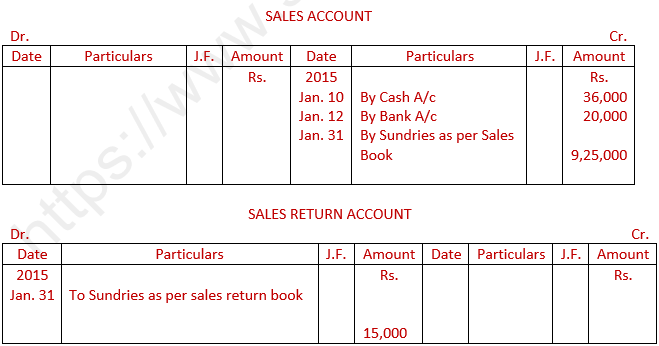

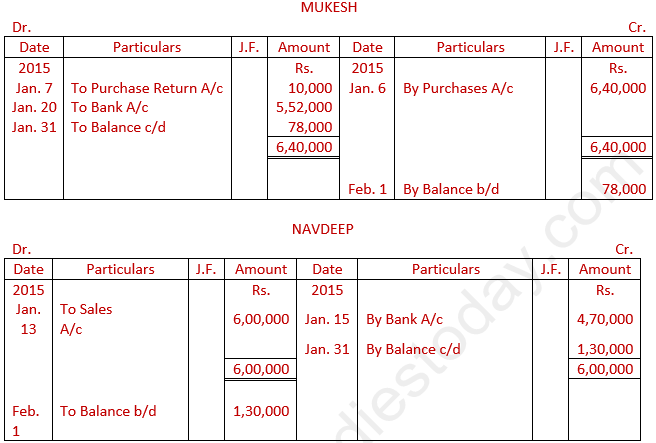

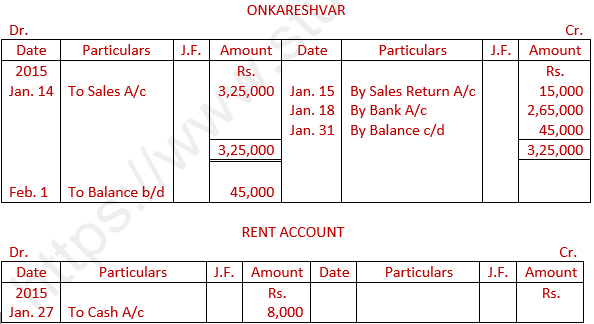

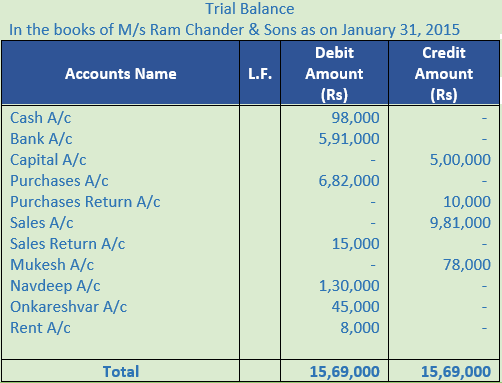

Question 1. Given below is a Cash Book and Ledger extracts relating to the books of M/s Ram Chander & Sons as at 31st January 2015. You are required to prepare a Trial Balance.

Solution 1:

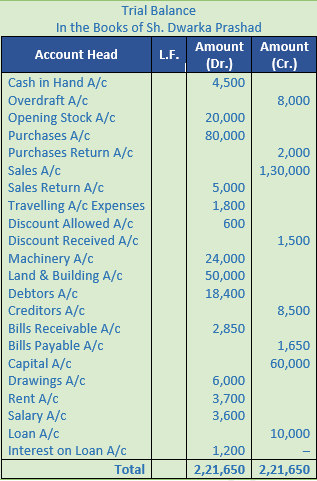

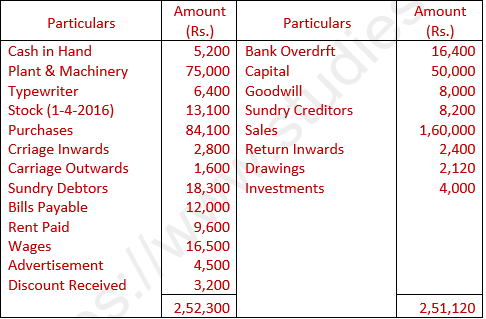

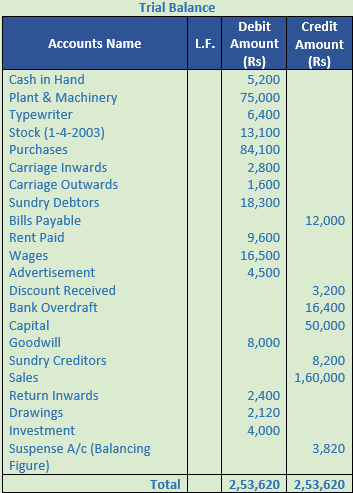

Question 2. From the following balances, taken from the books of M/s Dwarka Parshad & Sons as at 31st March 2017, prepare a Trial Balance in proper form :−

Solution 2:

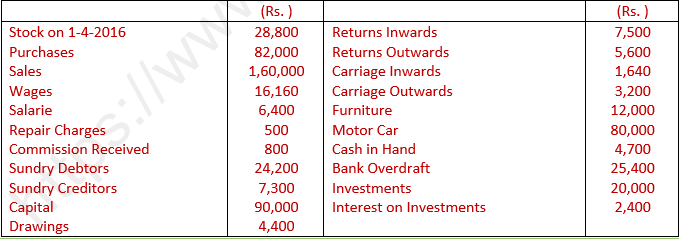

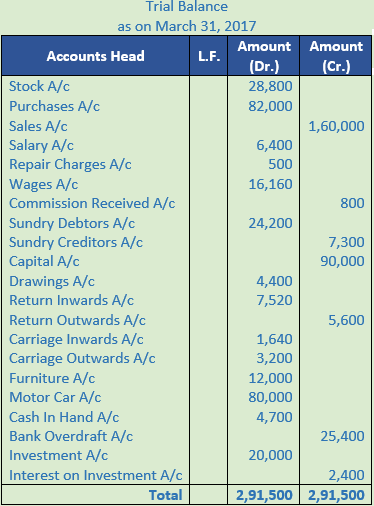

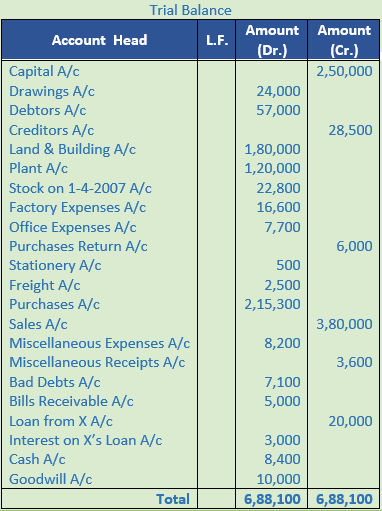

Question 3. (A) Prepare a Trial Balance from the following balances as at 31st March 2017 :−

Solution 3:

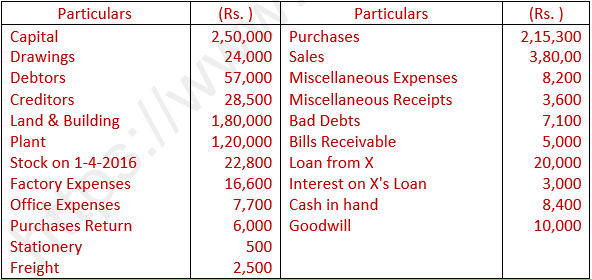

Question 3. (B) Prepare a Trial Balance from the following balances taken as at 31st March 2017 :−

Solution 3: (B)

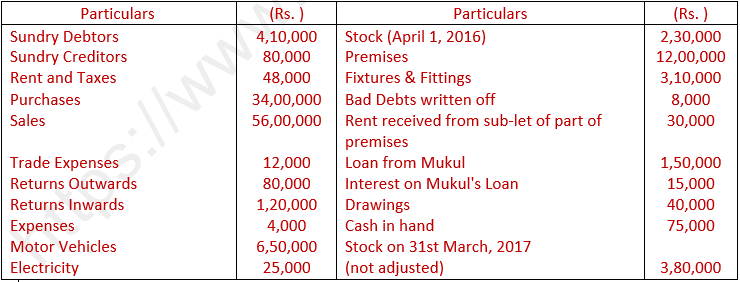

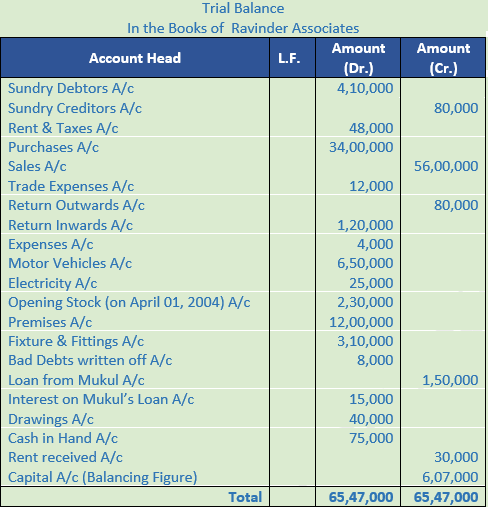

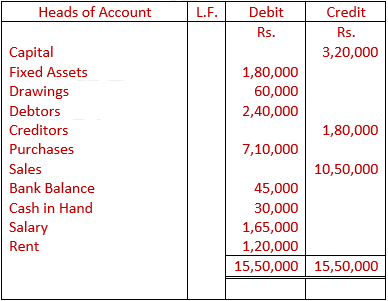

Question 4. Following balances were extracted from the books of Ravinder Associates as at 31st March, 2017 :

You are required to prepare the trial balance treating the difference as his capital.

Solution 4:

Point of Knowledge:-

Closing Stock not recorded individual as it has not been accounted yet.

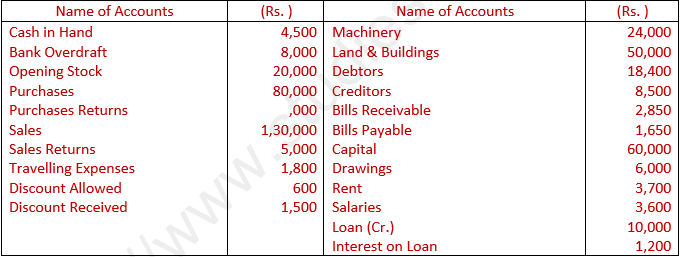

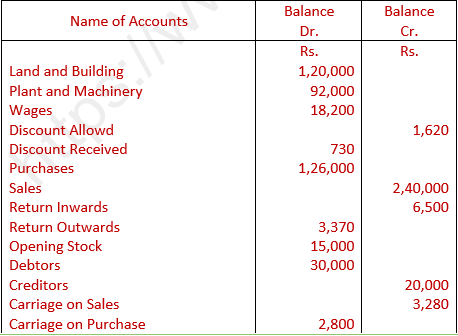

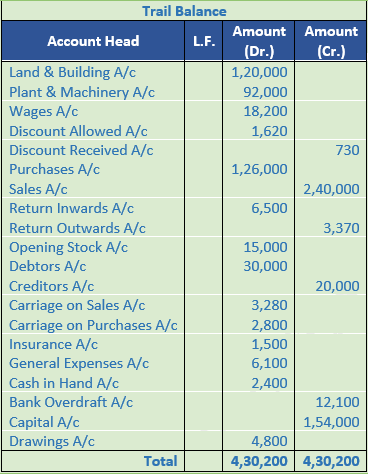

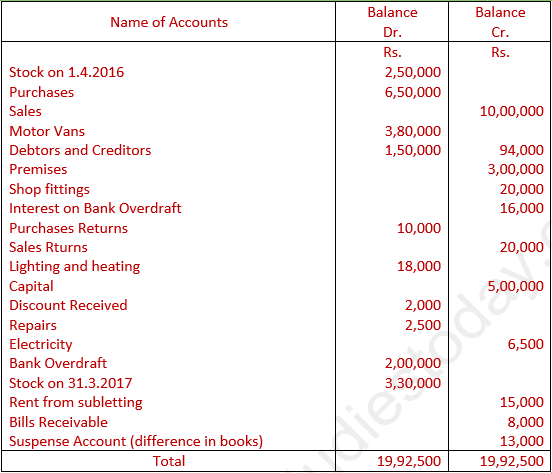

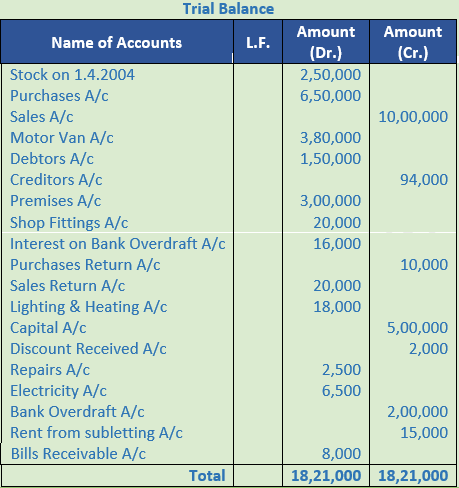

Question 5. The following trial balance has been prepared by an inexperienced accountant. Redraft it in a correct form :−

Solution 5:

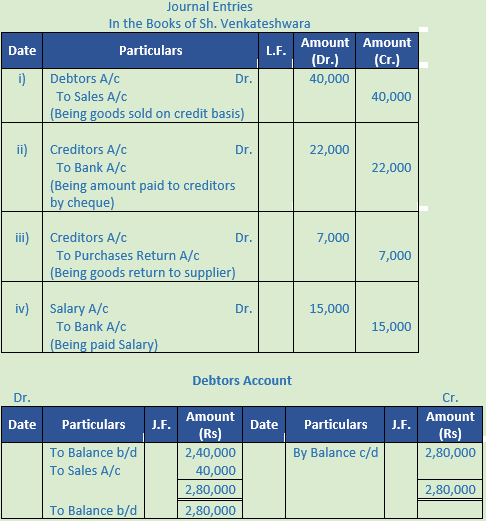

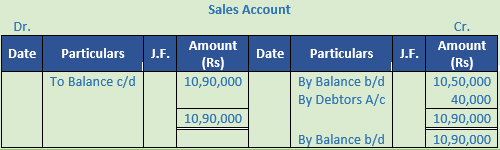

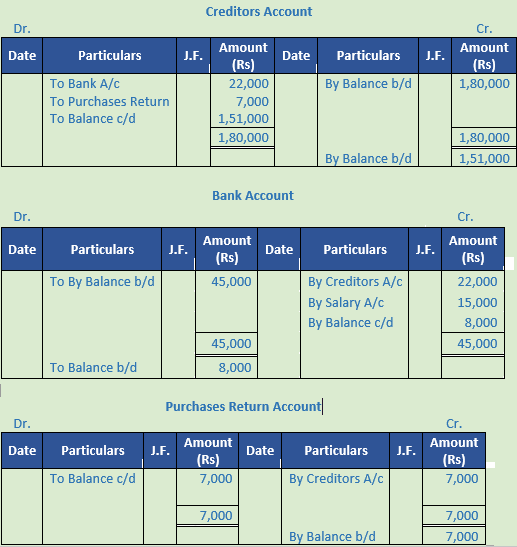

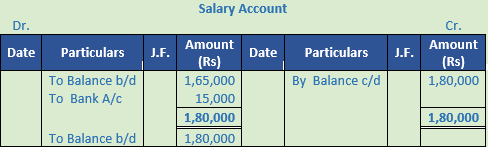

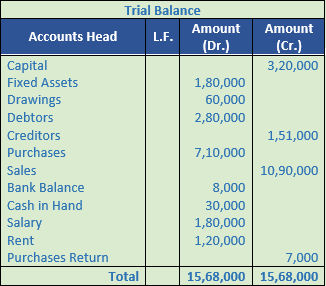

Question 6. Following is the Trial Balance as at 31st March, 2015 :

Having prepared the Trial Balance, it was discovered that following transactions remained unrecorded :

(i) Goods were sold on credit amounting to Rs. 40,000.

(ii) Paid to creditors Rs. 22,000 by cheque.

(iii) Goods worth Rs. 7,000 were returned to a supplier.

(iv) Paid salary Rs. 15,000 by cheque.

Required:

(i) Pass Journal entries for the above mentioned transactions and post them into Ledger.

(ii) Redraft the Trial Balance.

Solution 6:

Question 7. The following is the Trial Balance prepared by an inexperienced accountant. Redraft it in a correct form and give necessary notes : −

Solution 7:

Point of knowledge:-

Here Trail Balance is not matched hence we have to make a Suspense Account by balancing figure.

Question 8. A book-keeper extracted the following Trial Balance as at 31st March, 2017 :

You are required to redraft the trial balance correctly.

Solution 8:

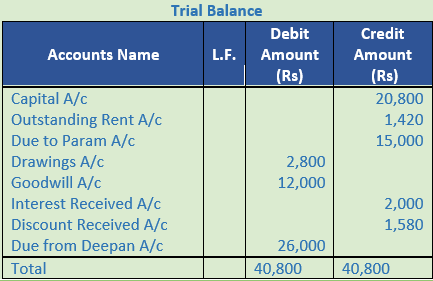

Question 9. From the following ledger balances prepare trial balance :

Capital Rs. 20,800, Rent outstanding Rs. 1,420, Amount due to Param, Rs. 15,000, Drawing Rs. 2,800, Goodwill Rs. 12,000, Interest received Rs. 2,000, Discount received Rs. 1,580, Amount due from Deepan Rs. 26,000.

Solution 9: