Short Answer Type Questions:

Question 1. Amit of Delhi sells goods of Rs. 10,000 to Dev of Gurugram, Haryana. Rates of CGST and SGST are 6% each and IGST is 12%.

Answer 1:

Question 2. Anil of Faridabad, Haryana sold goods of Rs. 20,000 to Pawan of Hisar, Haryana. Rates of CGST and SGST are 6% each while that of IGST is 12%.

Answer 2:

Question 3. Hari of Chandigarh returned goods of Rs. 30,000 purchased from Raman of Ludhiana, Punjab. Rates of CGST and SGST are 6% each while that of IGST is 12%.

Pass the Journal entry in the books of Hari.

Answer 3:

Question 4. Kashish of Chennai, Tamil Nadu returned goods of Rs. 50,000 purchased from Nagrath of Hyderabad, Telengana. Rates of CGST and SGST are 6% each while that of IGST is 12%. Pass the Journal entry in the books of Nagrath.

Answer 4:

Question 5. Goods of Rs. 10,000 purchased intra-state were destroyed in rain. If rates of CGST and SGST are 6% each and that of IGST is 12%. Pass the Journal entry for the goods destroyed.

Answer 5:

Question 6. Goods of Rs. 5,000 purchased for donation. CGST and SGST were charged @ 6% each. Pass the Journal entry for the purchase.

Answer 6:

Question 7. R & Co. paid professional fee to Rajat, an advocate. If applicable rate of CGST and SGST is 6% each, pass the Journal entry for payment of CGST and SGST.

Answer 7:

Question 8. Deo of Delhi is to receive commission of Rs. 10,000 from Vinod of Delhi. If rate of CGST and SGST is 6% each and that of IGST is 12%, what will be the Journal entry passed?

Answer 8:

Question 9. Input IGST is Rs. 20,000, Output IGST is Rs. 15,000, Input CGST is Rs. 15,000, Output CGST is Rs. 12,000 and Input SGST is Rs. 15,000, Output SGST is Rs. 12,000.

Answer 9:

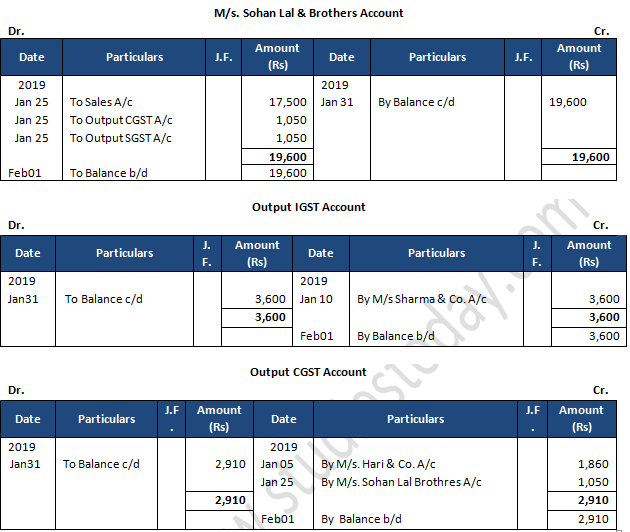

Question 10. Input IGST is Rs. 10,000, Output IGST is Rs. 15,000, Input CGST is Rs. 15,000, Output CGST is Rs. 10,000. Pass the Journal entry for setting off Input CGST.

Answer 10:

Practical Problems :->

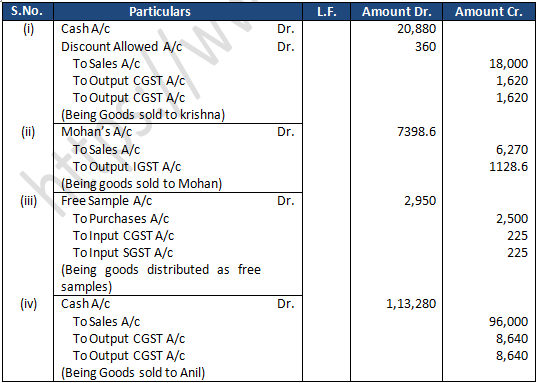

Question 1. Journalise the following transactions in the books of Rajan of Delhi:

(i) Sold goods to Krishna of Delhi at the list price Rs. 20,000 less trade discount 10% add CGST and SGST @ 9% each, and allowed cash discount 5%. He paid the amount immediately.

(ii) Supplied goods costing Rs. 6,000 to Mohan of Kalkata issued invoice at 10% above cost less 5% trade discount plus IGST @ 18%.

(iii) Goods valued at Rs. 2,500 distributed from stock as samples, as part of an advertising campaign. These goods were purchased paying CGST and SGST @ 9% each.

(iv) Sold goods costing Rs. 1,00,000 to Anil of Delhi at a profit of 20% on sales less 20% Trade discount plus CGST and SGST @ 9%.

Answer 1:

Working Note:-

1.) Cost of Goods = Rs. 6,000

Add: Profit 10% = Rs. 600

Sale = Rs. 6,000 + Rs. 600 = Rs. 6,600

Trade Discount = Rs. 6,600 × 5% = Rs. 330

Net Sales Value = Rs. 6,600 – Rs. 330

Net Sales Value = Rs. 6,270

2.) Value of Goods = Rs. 1,00,000

Profit = 20%

Sale Value = Rs. 1,00,000 + Rs. 20,000

Sale Value = Rs. 1,20,000

Sale Value after Trade Discount = Rs. 1,20,000 – 20%

Sale Value after Trade Discount = Rs. 96,000

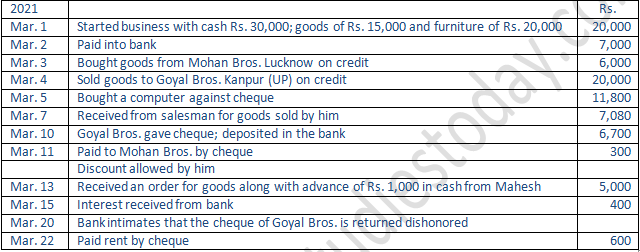

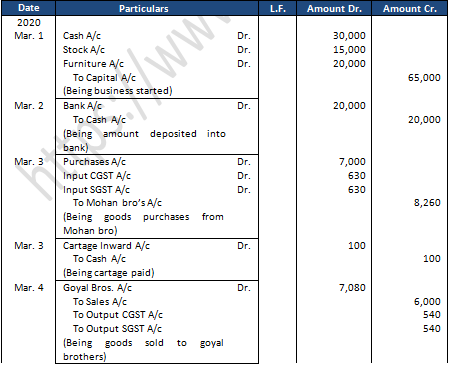

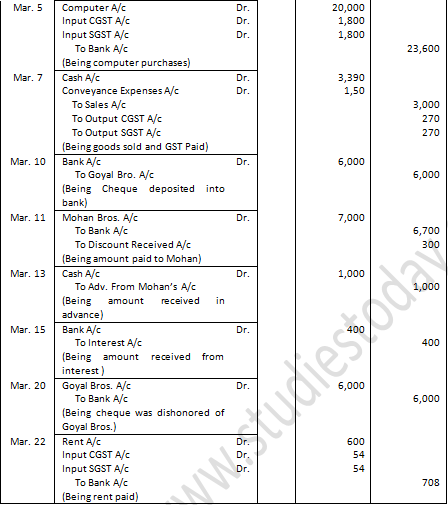

Question 2. Journalise the following transactions in the books of Gupta Bros. Lucknow (UP).

Answer 2:

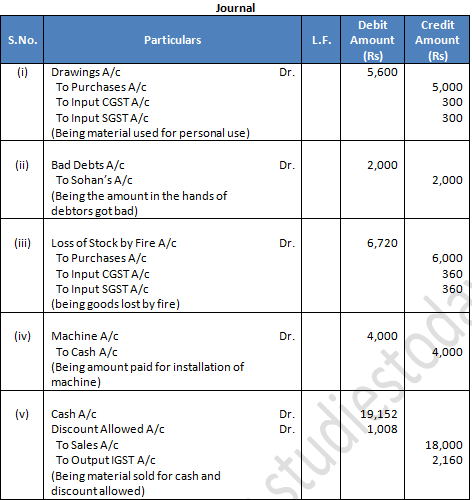

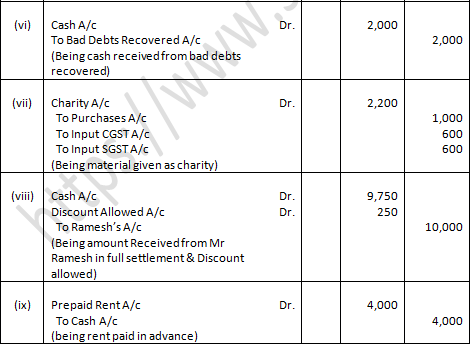

Question 3. Journalise the following in the books of Amit Saini, Gurugram (Haryana):

(i) Goods of Rs 5,000 were used by him for domestic purpose.

(ii) Rs 2,000 due from Sohan became bad debts.

(iii) Goods of Rs 6,000 were destroyed by fire and were not insured.

(iv) Paid Rs 4,000 in cash as wages on installation of machine. GST is not to be levied.

(v) Sold goods to Arjun of Delhi of list price Rs 20,000. Trade discount @ 10% and cash discount of 5% was allowed. He paid the amount on the same day and availed the cash discount.

(vi) Received cash for a bad debt written off last year Rs 2,000.

(vii) Goods of Rs 1,000 given as charity.

(viii) Received Rs 9,750 from Ramesh in full settlement of his account of Rs 10,000.

(ix) Paid rent in advance Rs 4,000.

CGST and SGST are to be levied on intra-state sale @ 6% each and IGST @ 12% on inter-state sale.

Answer 3:

Statement showing Journal Entries of Amit Saini

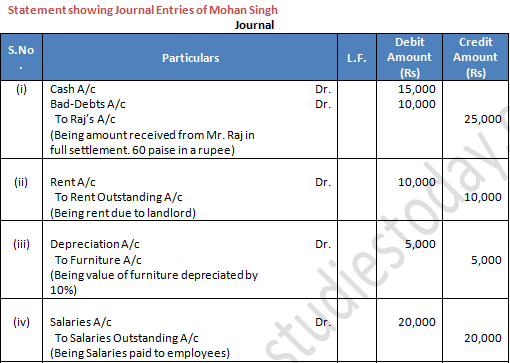

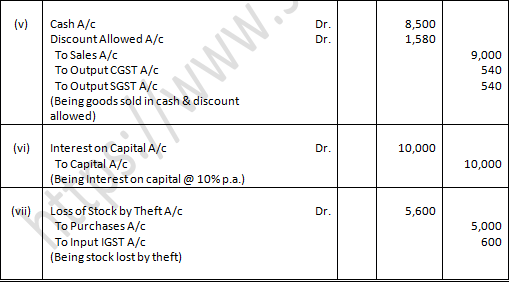

Question 4. Journalise the following transactions in the books of Mohan Singh, Delhi:

(i) Raj of Alwar, Rajasthan who owed Mohan Singh Rs 25,000 became insolvent and received 60 paise in a rupee as full and final settlement.

(ii) Mohan Singh owes to his landlord Rs 10,000 as rent.

(iii) Charge depreciation of 10% on furniture costing Rs 50,000.

(iv) Salaries due to employees Rs 20,000.

(v) Sold to Sunil goods in cash of Rs 10,000 less 10% trade discount plus CGST and SGST @ 6% each and received a net of Rs 8,500.

(vi) Provided interest on capital of Rs 1,00,000 @ 10% per annum.

(vii) Goods lost in theft−-Rs 5,000, which were purchased paying IGST @ 12% from Alwar, Rajasthan.

Answer 4:

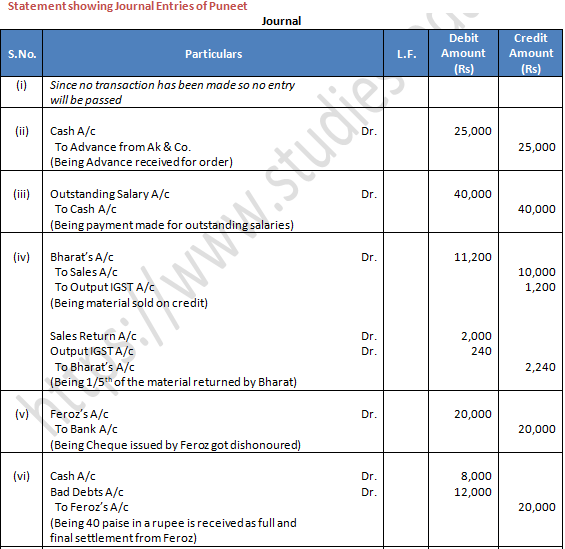

Question 5: Pass Journal entries in the books of Puneet, Delhi for the following:

(i) Received an order from Karan & Co. for supply of goods of Rs 50,000.

(ii) Received an order from AK & Co. for goods of Rs 1,00,000 along with a cheque for Rs 25,000 as advance.

(iii) Paid to staff Rs 40,000 against outstanding salary of Rs 60,000.

(iv) Sold goods to Bharat, Kaithal (Haryana) of Rs 10,000 plus IGST @ 12% out of which 1/5th were returned being defective.

(v) Cheque of Rs 20,000 issued by Feroz was dishonoured.

(vi) Received 40 paise in a rupee from Feroz against the above dues.

(vii) Received a cheque of Rs 25,000 from Mohan after banking hours.

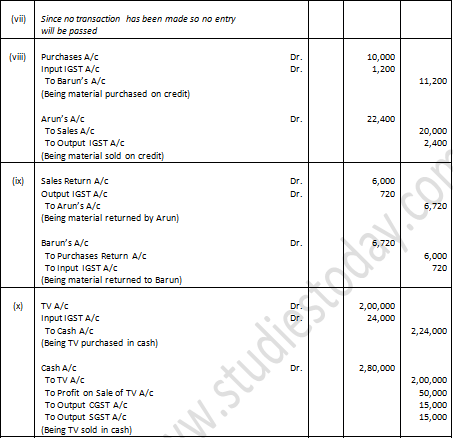

(viii) Purchased goods from Barun of Chandigarh of Rs 10,000 plus IGST @ 12% and sold them to Arun of Shimla (HP) at Rs 22,400, including IGST @ 12%.

(ix) Arun returned goods of Rs 6,720, including IGST which were returned to Barun.

(x) ABC & Co. purchased 10 TV sets @ 20,000 per set and paid IGST @ 12%. It sold all the sets @ 25,000 per set plus CGST and SGST @ 6% each.

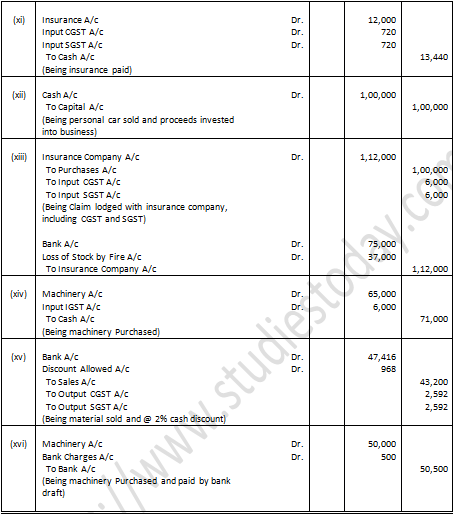

(xi) Paid insurance of Rs 12,000 plus CGST and SGST @ 6% each for a period of one year.

(xii) Sold personal car for Rs 1,00,000 and invested the amount in the firm.

(xiii) Goods costing Rs 1,00,000 were destroyed in fire. Insurance company admitted the claim gor Rs 75,000. These goods were purchased within Delhi.

(xiv) Purchased machinery for Rs 56,000 including IGST of Rs 6,000 and paid cartage thereon Rs 5,000 and installation charges Rs10,000.

(xv) Goods costing Rs 40,000 sold to Mr. X at a profit of 20% on sales less 10% Trade Discount plus CGST and SGST @ 6% each and received a cheque under 2% cash discount.

(xvi) Purchased machinery from New Machinery House for Rs 50,000 and paid it by means of a bank draft purchased from bank. Paid charges Rs 500.

Answer 5:

Cash Book

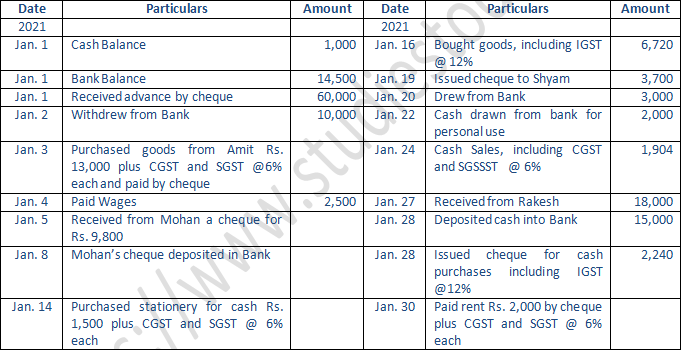

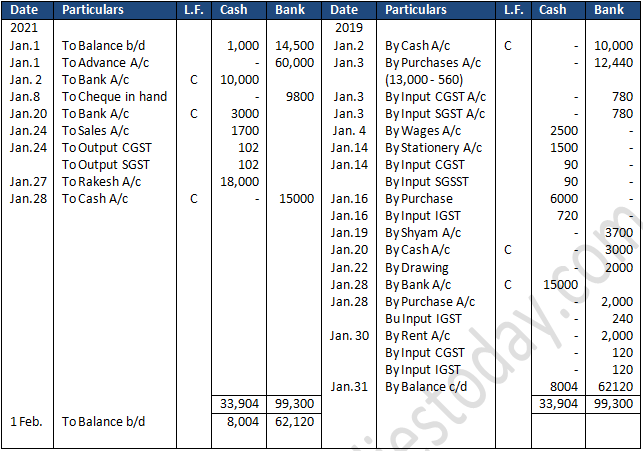

Question 6. Record the following transactions of Sumant, Kochi in a Two-column Cash Book and Balance the book on 31st January, 2021:

Answer 6:

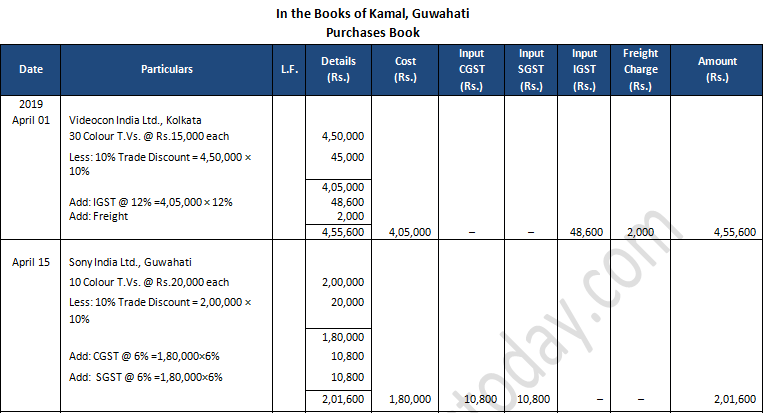

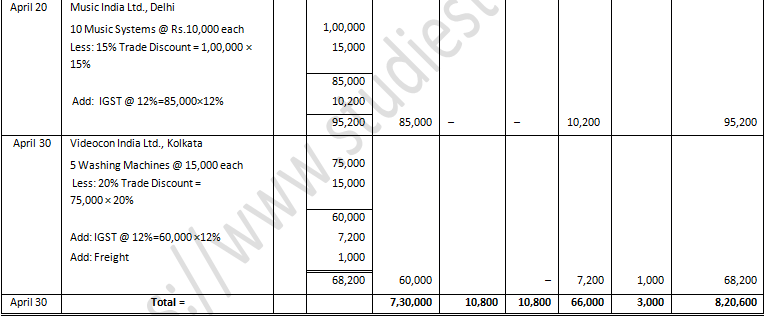

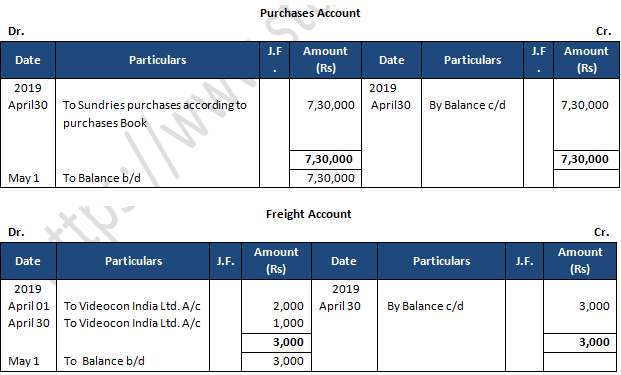

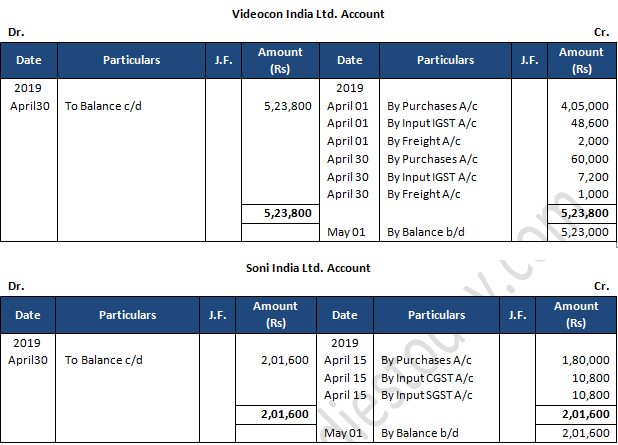

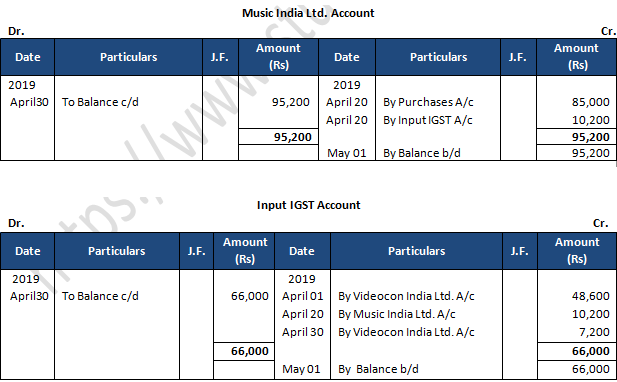

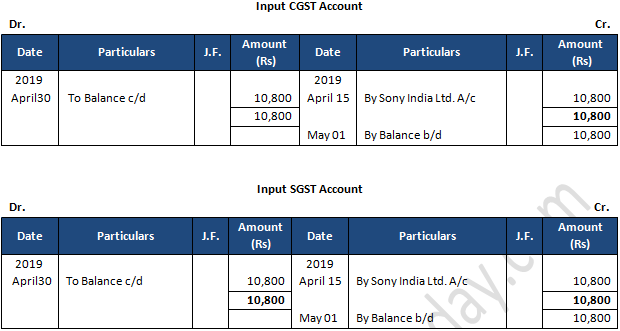

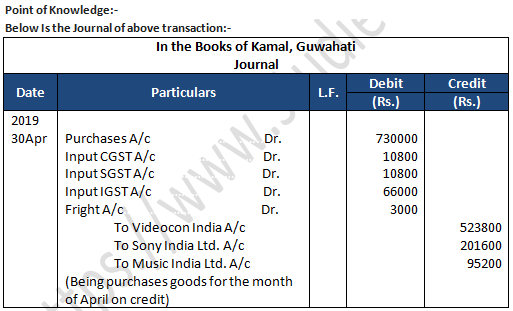

Purchases Book

Question 7. From the following information of Kamal, Guwahati, prepare a Purchases Book and post them into Ledger:

Answer 7:

Sales Book

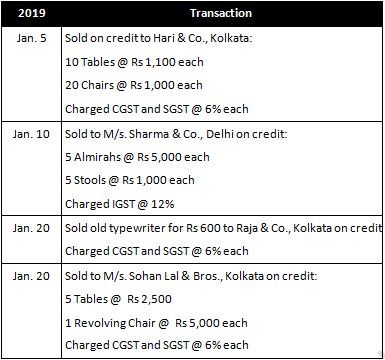

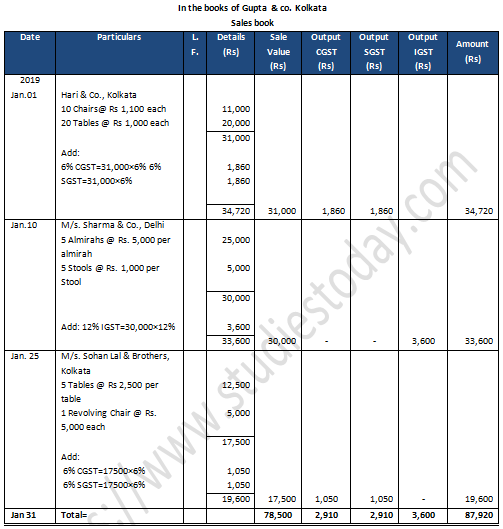

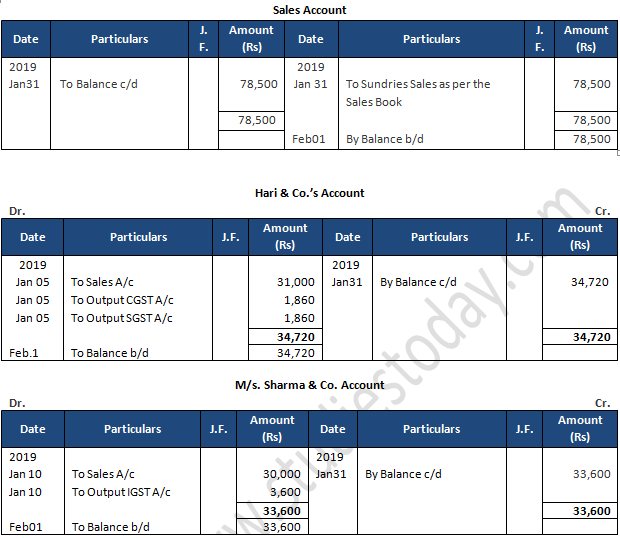

Question 8: From the following particulars, prepare Sales Book of Gupta & Co., Kolkata who deals in furniture:

Answer 8:

(ii) Since only credit sales of goods are recorded in sales book so sales of old typewriter was not shown in sales book.

Purchases Return Book

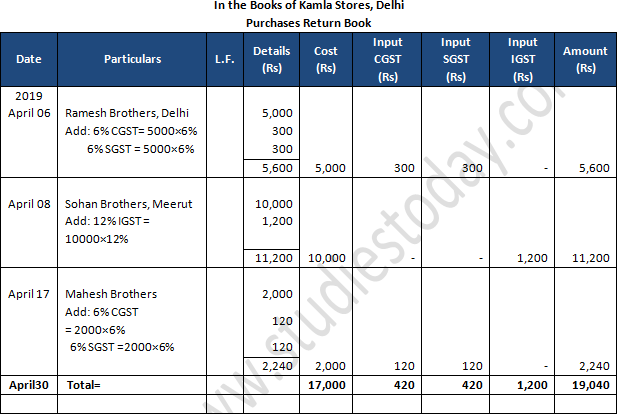

Question 9: Record following transactions in the Purchases Return Book of Kamla Stores for June 2017:

Answer 9:

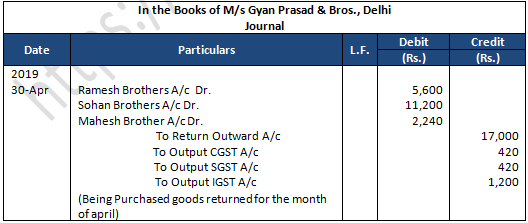

Point of Knowledge:-

Below Is the Journal of above transaction:-

Sales Return Book

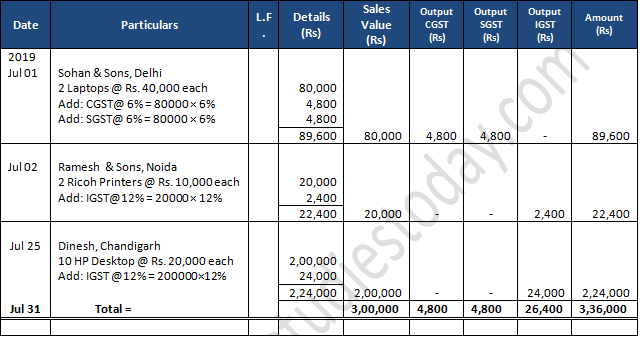

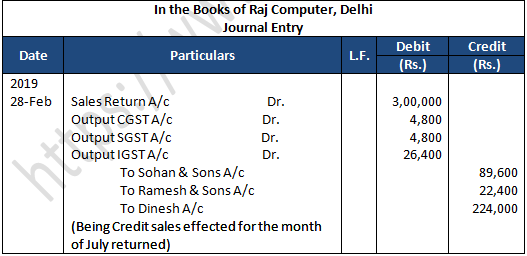

Question 10: Enter following transactions in the Sales Return Books of Raj Computers, Delhi:

Answer 10:

Point of Knowledge:-

Below Is the Journal of above transaction:-

(ii) Computer mouse are sold in cash mode then we are not considered sales return in sales return book.