Read DK Goel Class 11 Accountancy Solutions for Chapter 23 Accounts from Incomplete Records below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 23 Accounts from Incomplete Records should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 23 Accounts from Incomplete Records DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 23 Accounts from Incomplete Records in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 23 Accounts from Incomplete Records Class 11 Accountancy

Short Answer Questions

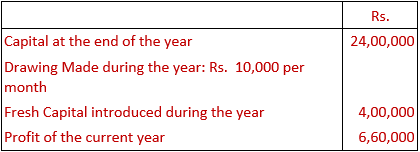

Question 1. Write any three characteristics of Single Entry System.

Solution 1: Below are the characteristics of Single Entry System:-

1.) Maintenance of Personal Accounts only:- Usually under this system, only personal accounts are prepared in the books and the real and nominal accounts are ignored.

2.) Maintenance of Cash Book:- A Cash Book is maintained under this system, which usually mixes up business as well as private transactions of the proprietor.

3.) Dependence on Original Vouchers:- In order to collect the required information one has to depend on original vouchers.

Question 2. Give any three reasons for keeping records under Single Entry System.

Solution 2: Below are the reasons for keeping records under single entry system:-

1.) Simple Method:- It is an easy and simple method of recording business transactions because it does not require any special knowledge of the principles of double entry system.

2.) Less Expensive:- Only the cash book and some of the ledger accounts are maintained under this system. As such the staff required for maintaining the accounts is also less in comparison to double entry system.

3.) Suitable for small concerns:- This method is most suitable to small business concerns which have mostly cash transactions and very few assets and liabilities.

Question 3. Write any three defects of Incomplete Records.

Solution 3: Below are the defects of Incomplete records:-

1.) Preparation of Trail Balance not Possible:- The method does not record both the aspects of transaction. As such, a trail balance cannot be prepared to check the arithmetical accuracy of the books of accounts. This increases the possibility of frauds and misappropriations.

2.) Incomplete and Unscientific System:- The system is incomplete and unscientific due to the fact that both the aspects, debit and credit of a transaction are not recorded.

3.) True Profit or Loss cannot be ascertained:- Because nominal accounts are not maintained, a Trading and profit and loss account cannot be prepared and hence, the profit earned or loss suffered during a particular period cannot be ascertained with reasonable accuracy.

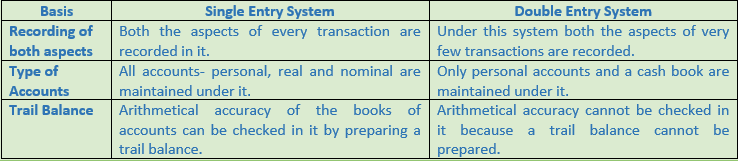

Question 4. State three points of difference between Single Entry and Double Entry System.

Solution 4:

Question 5. Why do big business houses not maintain their accounts under single entry system?

Solution 5:

Despite the records being incomplete, the businessman would like to know the trading results also the financial position of his business at the end of a particular period. This is done by adopting one of the two methods mentioned below:-

1.) Statement of affairs method or capital comparison method or Net worth method.

2.) Conversion into double entry method.

Question 6. What is meant by Statement of Affairs?

Solution 6: According to this method, the profits are ascertained by comparing the capital at the end and capital at the beginning of the accounting period. If the capital at the end of an accounting period is more than that at the beginning (with the necessary adjustments), the difference is treated as profit.

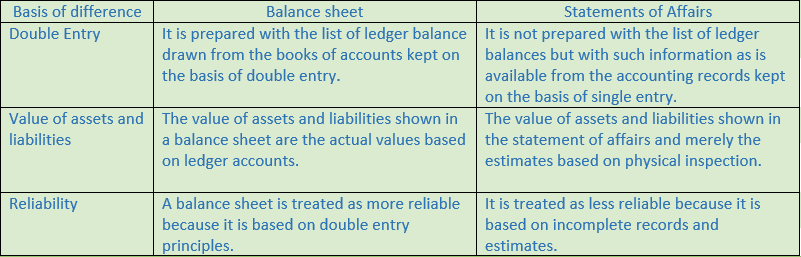

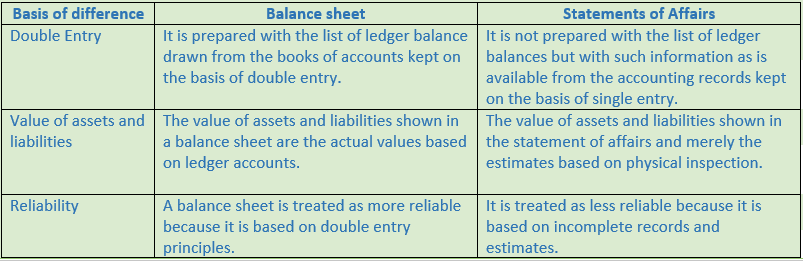

Question 7. State three points of difference between Statement of Affairs and Balance Sheet.

Solution 7:

Question 8. Why is Statement of Affairs not called a Balance Sheet?

Solution 8: Statement of Affairs not called a balance sheet because;-

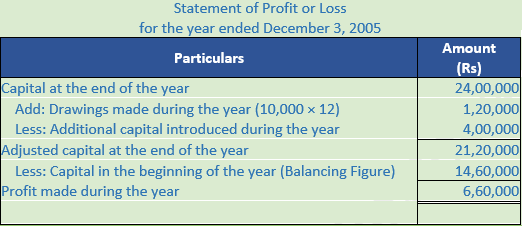

Question 9. Why are drawings added to Closing Capital in a statement of profit or loss?

Solution 9: Drawings are added to the closing capital on the logic that if the drawings had not been made, closing capital would have higher by this amount. Similarly additional capital is deducted from the closing capital on the logic that if the amount.

Question 10. Write a note on method of calculating profit under Single Entry System.

Solution 10: In order to ascertain profit according to this method, it is necessary to calculate the capital at the beginning of the year and also at the end of the year. Capital at the beginning is calculated by preparing an ‘opening statement of Affairs’ and similarly, capital at the end is calculated by preparing a ‘Closing Statement of Affairs’.

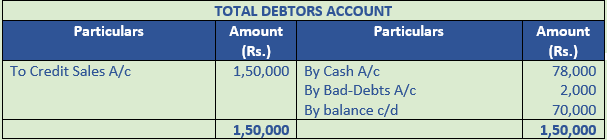

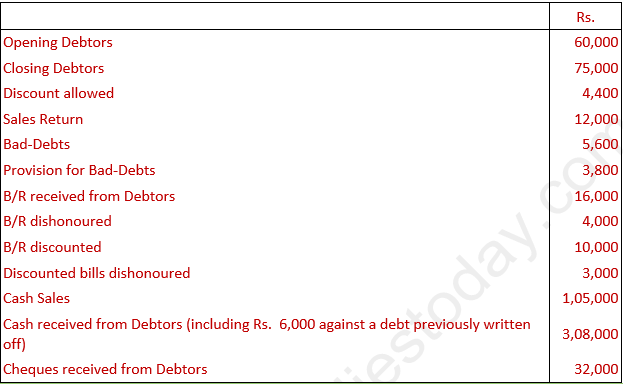

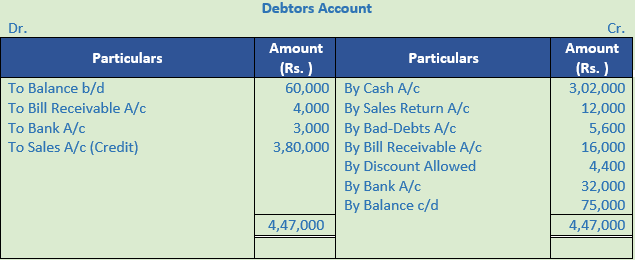

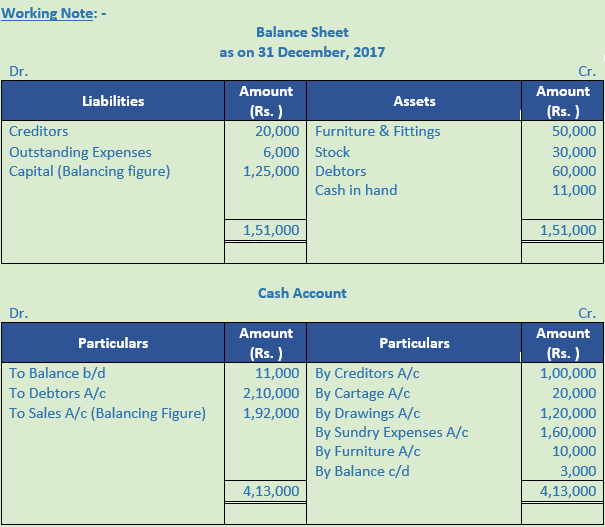

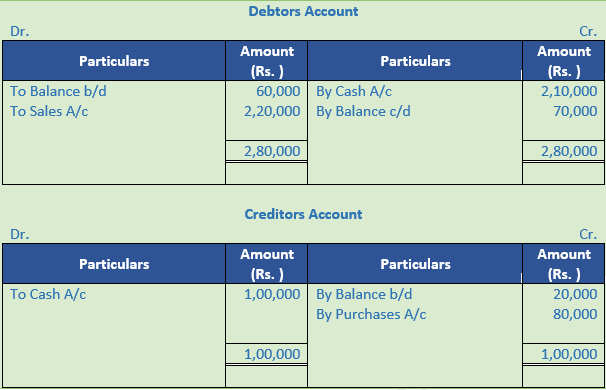

Question 11. Prepare a ‘Total Debtors Account’ with imaginary figures.

Solution 11:

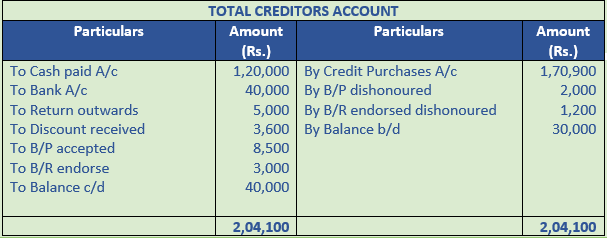

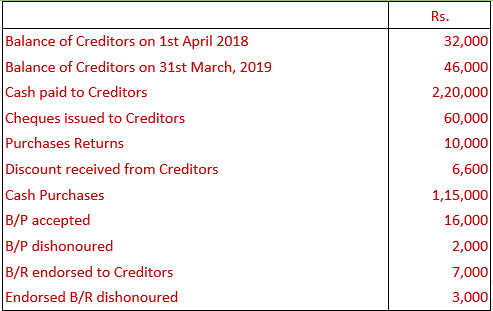

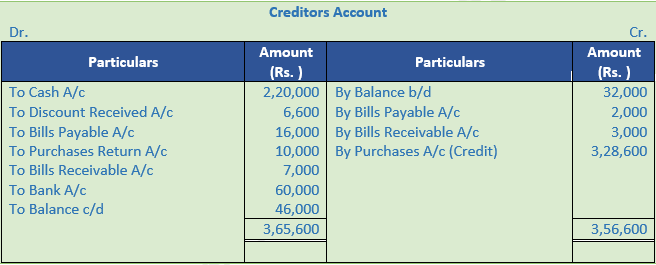

Question 12. Prepare a ‘Total Creditors Account’ with imaginary figures.

Solution 12:

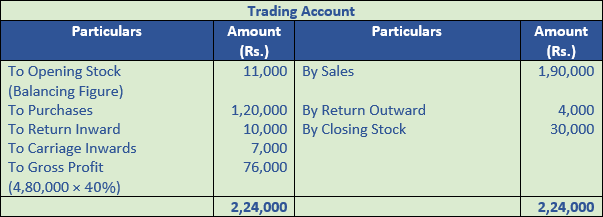

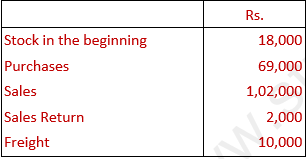

Question 13. Ascertain the value of Opening Stock from the following:

Solution 13:

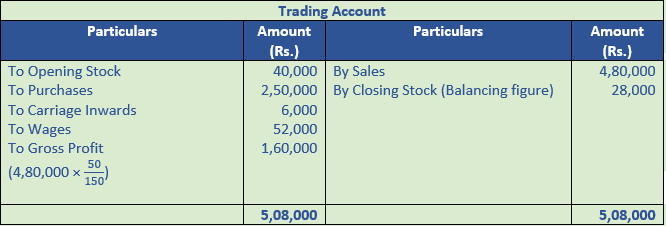

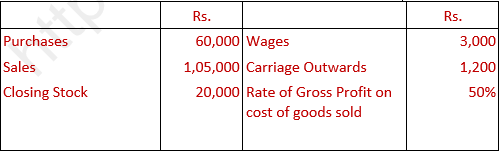

Question 14. Calculate the value of Closing Stock from the following:

Solution 14:

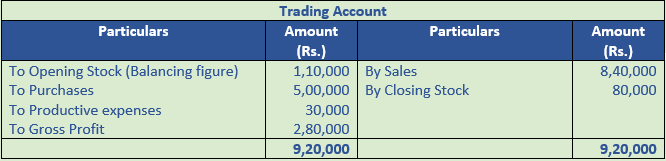

Question 15. From the following particulars, ascertain the value of Opening Stock:

Solution 15:

Question 16. From the following particulars, ascertain the value of Closing Stock:

Solution 16:

Practical Questions

Question 1. Atul does not keep proper records of his business. He gives you the following information:

Calculate profit or loss for the year

Solution 1:

Point of Knowledge:-

Profit = Closing Capital + Drawings – Additional Capital – Opening Capital

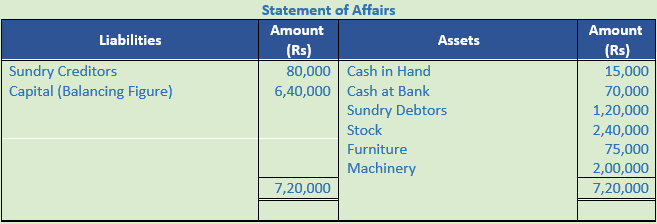

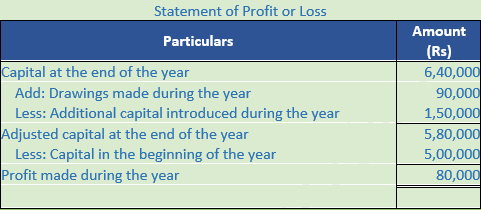

Question 2. Mr. Joshi started a business with a capital of Rs. 5,00,000. At the end of the year his position was:

Sundry creditors at this date totalled Rs. 80,000. During the year he introduced a further capital of Rs. 1,50,000 and withdrew for household expenses Rs. 90,000.

You are required to calculate profit or loss during the year.

Solution 2:

Question 3. Mr. Vasudev does not keep proper records of his business. He provided following information. You are required to prepare a statement showing the profit or loss for the year.

Solution 3:

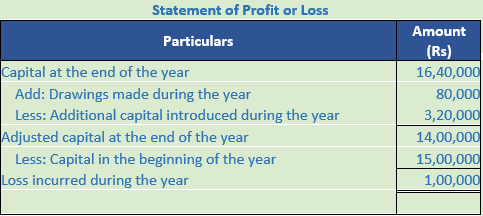

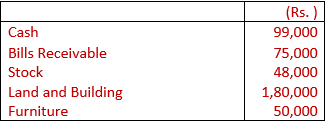

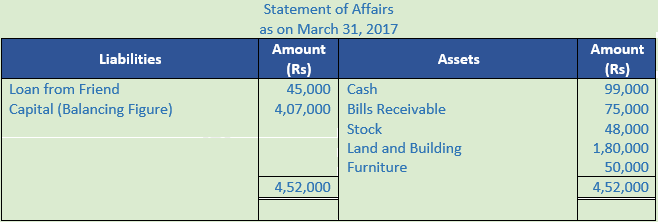

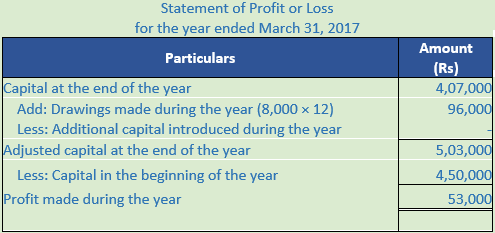

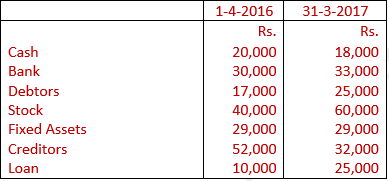

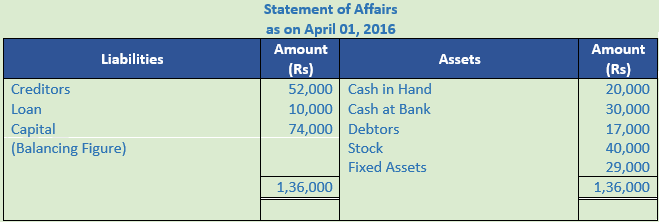

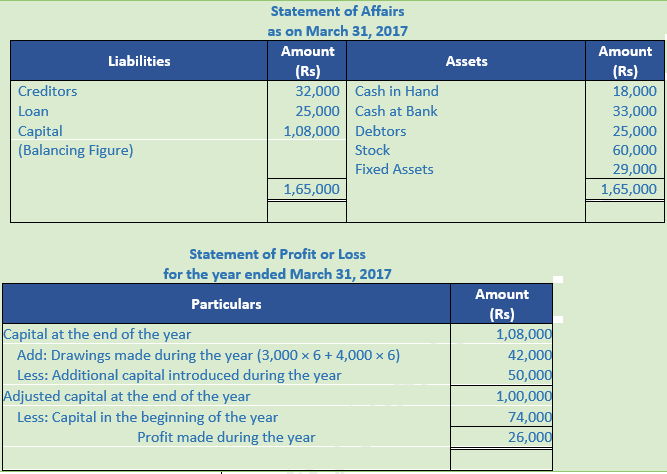

Question 4. Tulsi started business on 1st April, 2016 with a capital of Rs. 4,50,000. On 31st March, 2017 her position was as under:

She owed Rs. 45,000 to her friend Parvati on that date. She withdrew Rs. 8,000 per month for household purposes. Ascertain her profit or loss for the year ended 31st March, 2017.

Solution 4:

Question 5. (A) From the following information, calculate capital at the beginning :

Solution 5 (A):

Question 5. (B) Calculate Closing Capital:

Opening Capital Rs. 90,000; Profit for the year Rs. 25,000; Drawings Rs. 17,000. During the year proprietor sold ornaments of his wife for Rs. 40,000 and invested the same in business.

Solution 5 (B):

Profit = Closing Capital + Drawings – Additional Capital – Opening Capital

Closing Capital = Opening Capital + Additional Capital + Profits - Drawings

Closing Capital = 90,000 + 40,000 + 25,000 - 17,000

Closing Capital = Rs 1,38,000

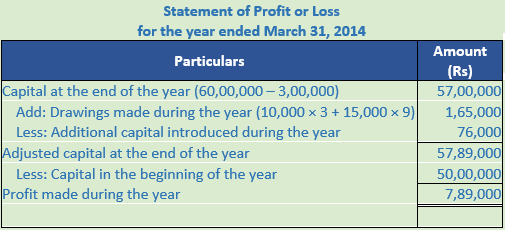

Question 6. Suchitra started a business on 1st April, 2013 with a Capital of Rs. 50,00,000. On 31st March, 2014 her total Assets were Rs. 60,00,000 and Creditors were 3,00,000. She withdrew during the year for her personal expenses Rs. 10,000 per month upto 30th June, 2013 and thereafter Rs. 15,000 per month upto 31st March, 2014. During the year she sold her personal investments of Rs. 80,000 at 5% loss and introduced that amount in the business.

You are required to prepare a Statement of Profit or Loss for the year ending 31st March, 2014.

Solution 6:

Working Note:-

Investment value = Rs. 80,000

Loss on investment = Rs. 80,000 × 5% = Rs. 4,000

Selling value of investment = Rs. 80,000 – Rs. 4,000 = Rs. 76,000

Question 7. Following incomplete information is available from records maintained by Mr. X:

During the year Mr. X introduced in the business the amount realised on sale of Rs. 10,000 investments at the premium of 5%. Personal expenses of Mr. X paid from business account amounted to Rs. 1,250 per month. Prepare a statement to calculate Profit (or Loss) during the year.

Solution 7:

Working Note:-

Investment value = Rs. 10,000

Profit on investment = Rs. 10,000 × 5% = Rs. 500

Selling value of investment = Rs. 10,000 + Rs. 500 = Rs. 10,500

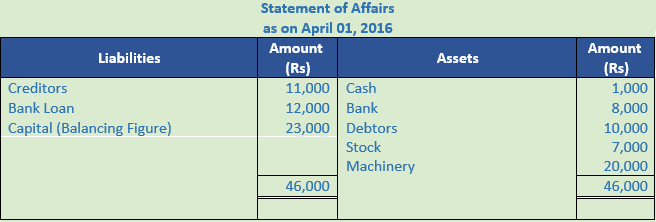

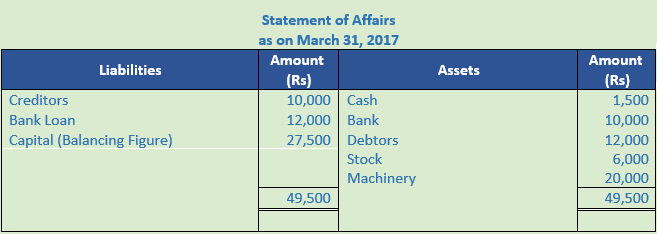

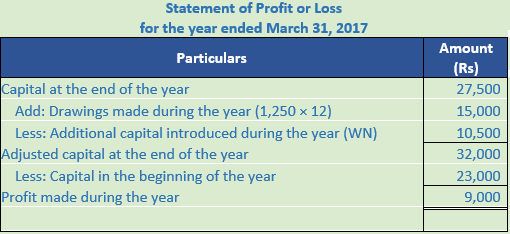

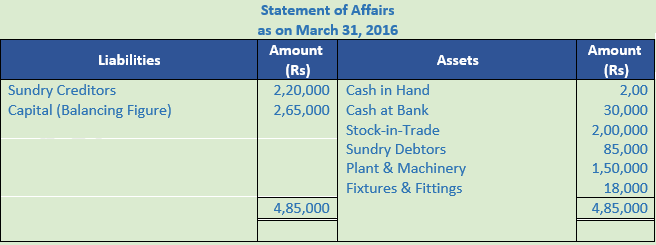

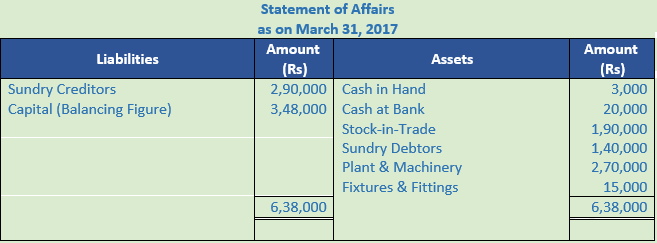

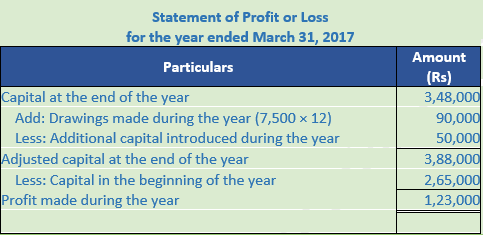

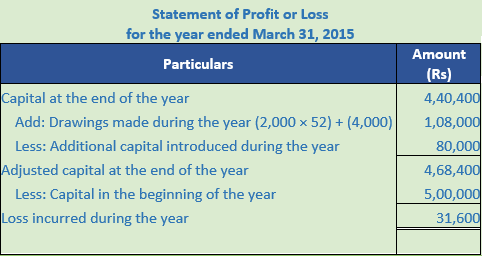

Question 8. Raghuveer keeps incomplete records. His position was as follows:

During the year, Raghuveer introduced Rs. 50,000 as further capital in the business and withdrew Rs. 7,500 per month. From the above information, show Profit or Loss for the year ended 31st March, 2017.

Solution 8:

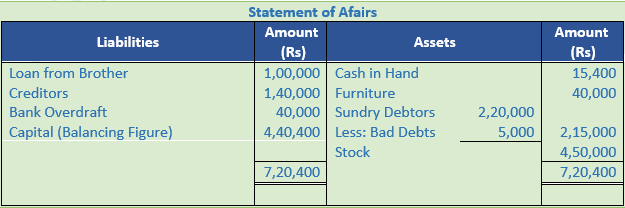

Question 9. On 1st April 2014, Mr, Ghosh started business with a capital of Rs. 5,00,000. He kept his books on single entry basis. Soon after he purchased furniture for Rs. 40,000 and purchased goods for Rs. 3,00,000. During the year he borrowed Rs. 1,00,000 from his brother and introduced further capital of his own amounting to Rs. 80,000.

On 31st March, 2015, there were sundry debtors amounting to Rs. 2,20,000 and creditors amounted to Rs. 1,40,000. Stock was valued at Rs. 4,50,000. Cash in hand Rs. 15,400 and Bank Overdraft Rs. 40,000

During the year Mr. Ghosh withdrew Rs. 2,000 per week for his family expenses. You are informed that included in sundry debtors is an irrecoverable amount of Rs. 5,000. He also took goods from the business for his personal use amounting to Rs. 4,000.

You are required to calculate his profit or loss during the year.

Solution 9:

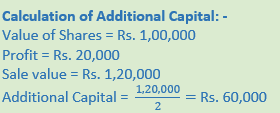

Question 10. The Capital of Sh. Madhusudan on 1st April, 2016 was Rs. 5,00,000 and on 31st March, 2017 was Rs. 4,80,000. He has informed you that he withdrew from the business Rs. 8,000 per month for his private use. He paid Rs. 20,000 for his income-tax and the instalment of the loan of his personal house at the rate of Rs. 15,000 per month from the business. He had also sold his shares of Reliance Company costing Rs. 1,00,000 at a profit of 20% and invested half of this amount in the business. Calculate the profit or loss of the business.

Solution 10:

Calculation of Drawings:-

Cash withdrawn = Rs. 8,000 × 12 = Rs. 96,000

Income tax paid = Rs. 20,000

Personal Loan instalment = Rs. 15,000 × 12 = Rs. 1,80,000

Total Drawings = Rs. 96,000 + Rs. 20,000 + Rs. 1,80,000 = Rs. 2,96,000

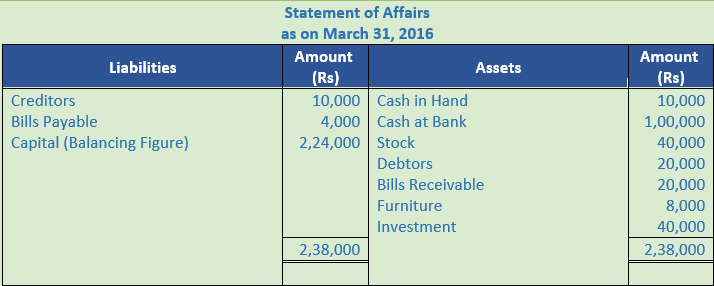

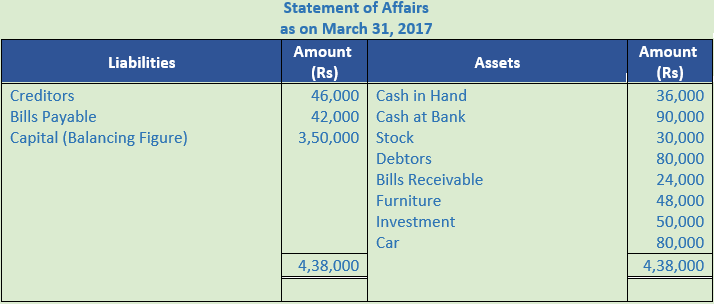

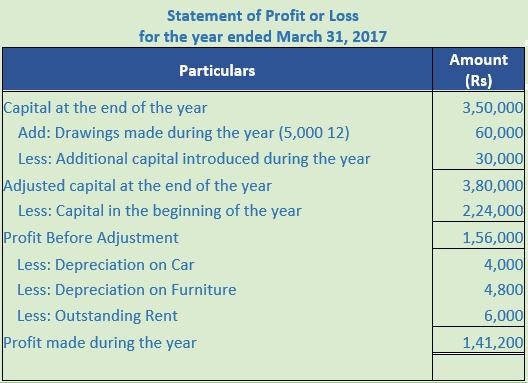

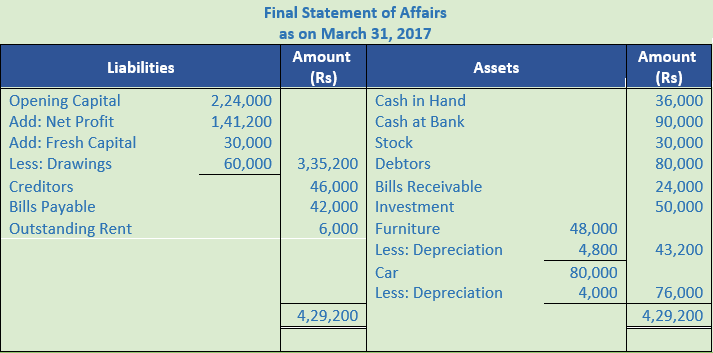

Question 11. Charu do not keep proper books of accounts. Prepare the statement of profit or loss for the year ending 31-3-2017 from the following information:

The following adjustments are to be made:

(a) Proprietor withdrew cash Rs. 5,000 per month for private use.

(b) Depreciation @ 5% on Car and @ 10% on furniture.

(c) Outstanding Rent Rs. 6,000.

(d) Fresh Capital introduced during the year Rs. 30,000.

Solution 11:

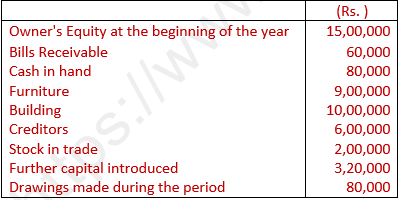

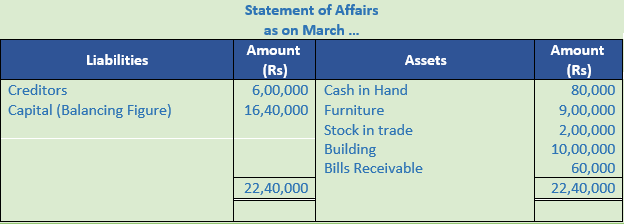

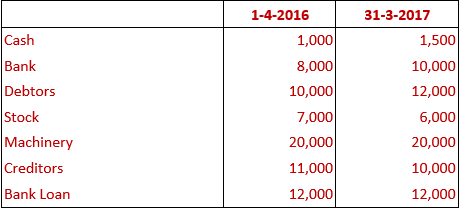

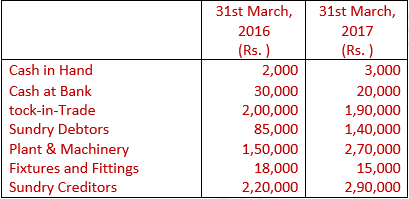

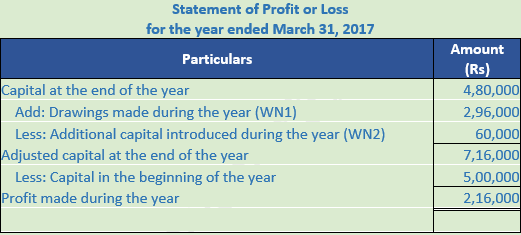

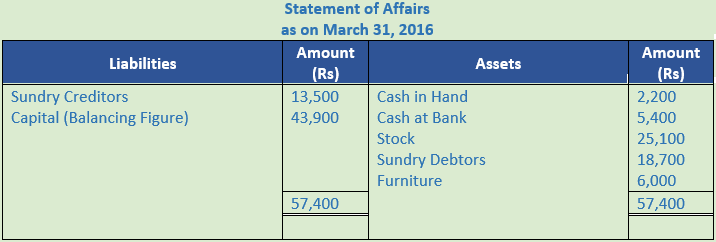

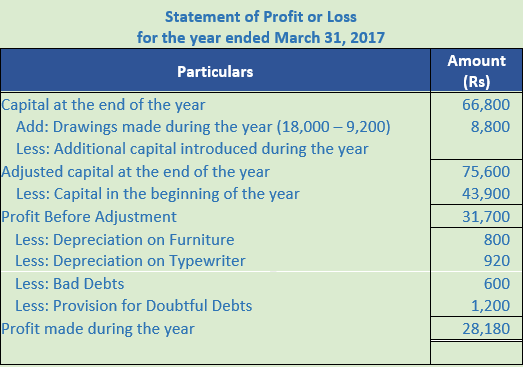

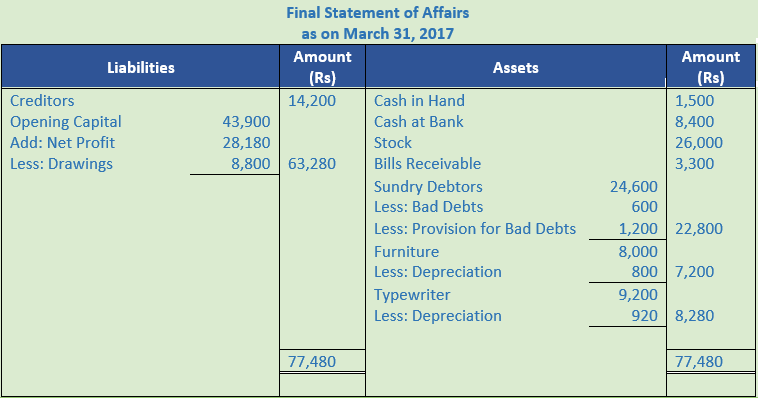

Question 12. Ashok keeps incomplete records. The position of his business on 1st April, 2016 was as follows:

Cash in Hand Rs. 2,200; Cash at Bank Rs. 5,400; Stock Rs. 25,100; Sundry Debtors Rs. 18,700; Furniture Rs. 6,000; Sundry Creditors Rs. 13,500.

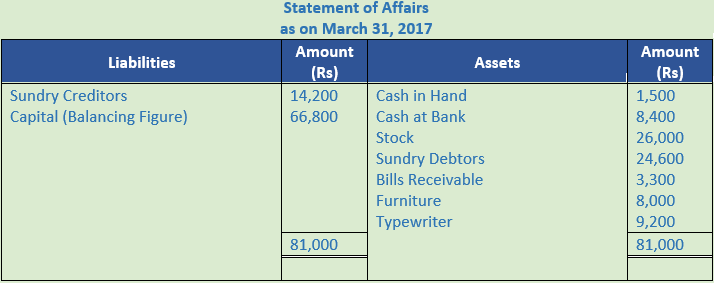

His position on 31st March, 2017 was as follows:

Cash in Hand Rs. 1,500; Cash at Bank Rs. 8,400; B/R Rs. 3,300; Stock Rs. 26,000; Sundry Debtors Rs. 24,600; Furniture Rs. 8,000; Sundry Creditors Rs. 14,200.

During the year he had withdrawn from the business Rs. 18,000, of which Rs. 9,200 were spent in purchasing a Typewriter for the business.

(a) Depreciate furniture and typewriter by 10%.

(b) Write off Rs. 600 as Bad-Debts.

(c) Make a provision of 5% on Debtors for doubtful debts.

Calculate the profit or loss of his business for the year ended 31st March, 2017 and prepare a final statement of affairs, after the above adjustments.

Solution 12:

Question 13. From the details given below find out the Credit Sales and Total Sales :

Solution 13:

Working Note:-

Calculation of Total Sales:-

Total Cash = Cash Sales + Credit Sales

Total Cash = Rs. 1,05,000 + Rs. 3,80,00

Total Cash = Rs. 4,85,000

Question 14. Find out the Credit Purchases from the details given below:

Solution 14:

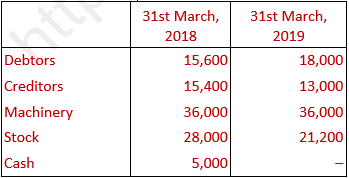

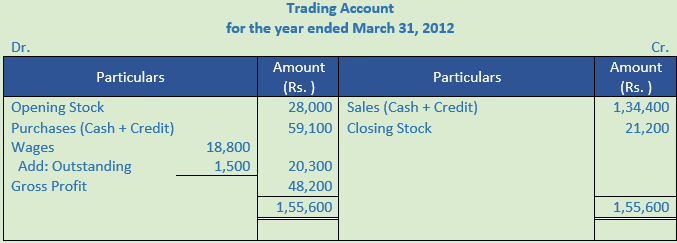

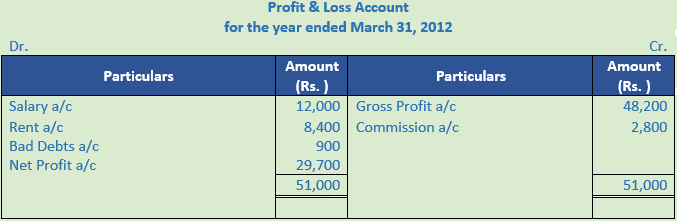

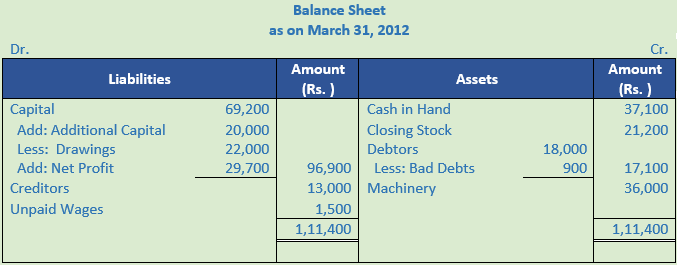

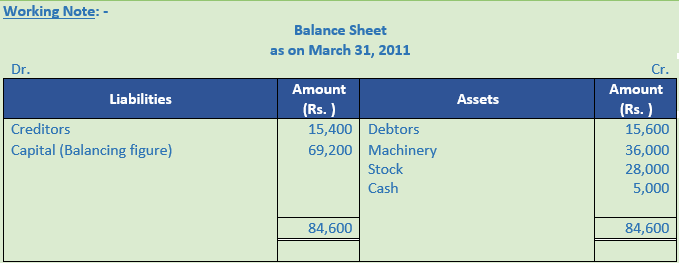

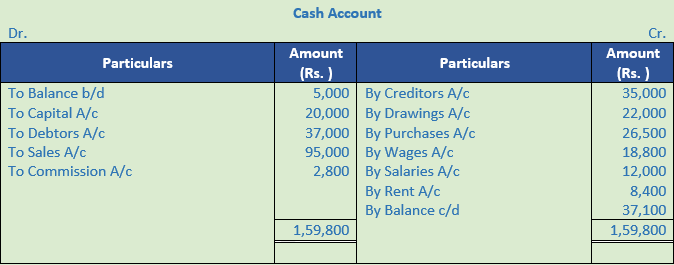

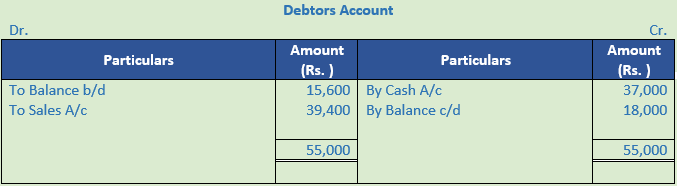

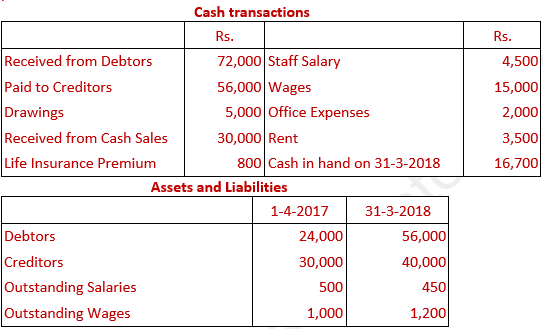

Question 15. Anand Mohan has kept incomplete books. From the following particulars, prepare his Final Accounts for the year ending 31st March, 2019:

Receipts:- Received from Debtors Rs. 37,000; Fresh Capital brought in cash Rs. 20,000; Commission Received Rs. 2,800; Cash Sales Rs. 95,000.

Payments:- Paid to Creditors Rs. 35,000; Cash Purchases Rs. 26,500; Ornaments for his wife Rs. 22,000; Wages Rs. 18,800; Rent Rs. 8,400; Salary Rs. 12,000.

His Other Assets and Liabilities:-

Adjustments:-

(1) Unpaid wages Rs. 1,500.

(2) Provide for Doubtful Debts at 5% on Debtors.

Solution 15:

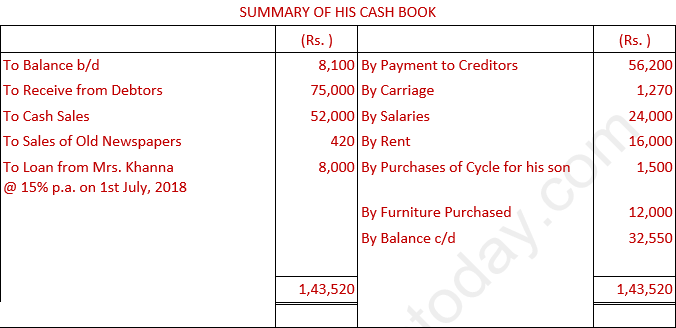

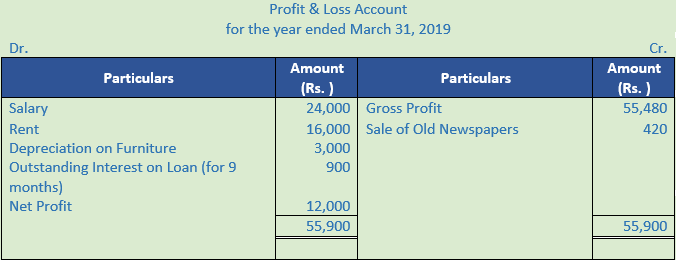

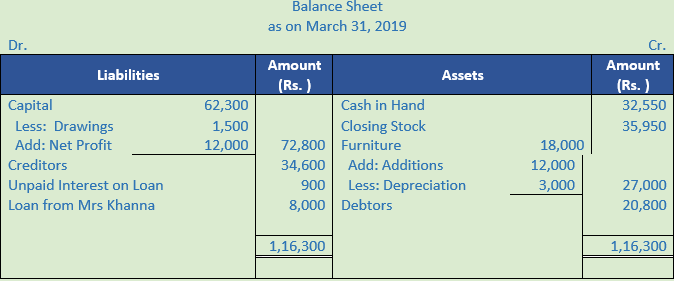

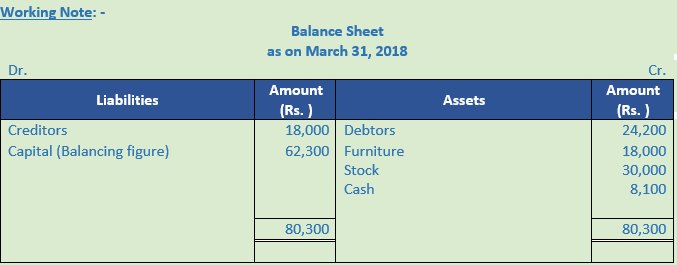

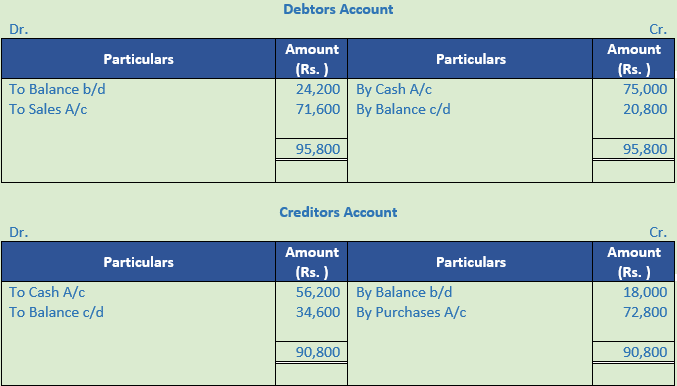

Question 16. Mukesh Khanna has not kept proper books. However, he gives you the following information relating to the year 2018-19:

The following balances existed on 1st April, 2018 - Debtors Rs. 24,200; Furniture Rs. 18,000; Stock Rs. 30,000; Creditors Rs. 18,000.

The following balances existed on 31st March, 2019 - Debtors Rs. 20,800; Furniture Rs. 30,000; Stock Rs. 35,950; Creditors Rs. 34,600.

Adjustments:-

(1) Depreciate Furniture by 10%.

(2) Provide upto-date interest on Mrs. Khanna's Loan.

Prepare Trading and Profit and Loss A/c for the year ending 31st March, 2019 and a Balance Sheet as at that date.

Solution 16:

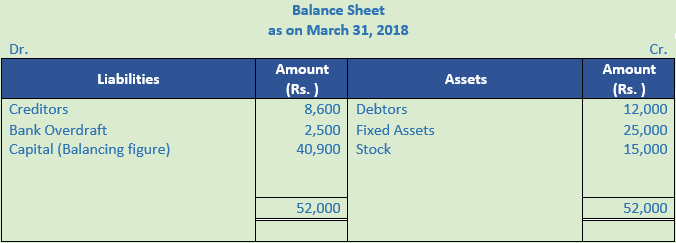

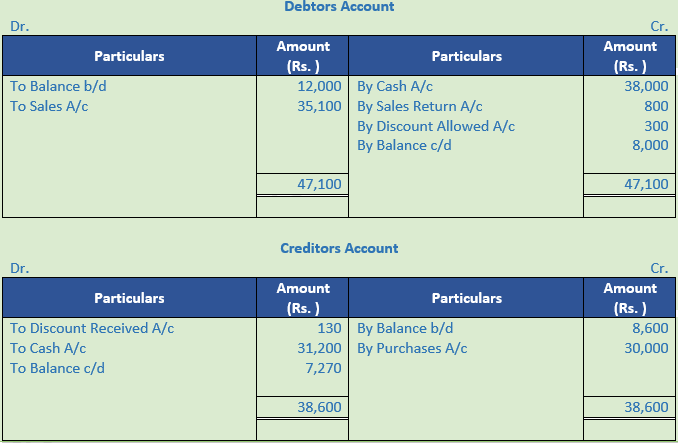

Question 17. Mr. Asif Ali, a retail trader, who keeps Incomplete Records gives you the following information for the year 2018-19:

Other Information’s:

(1) Credit Sales during the year were Rs. 35,100.

(2) Sales returns Rs. 800.

(3) Credit Purchases during the year were Rs. 30,000.

(4) Discount allowed to Debtors Rs. 300.

(5) Discount received from Creditors Rs. 130.

Adjustments:-

(1) Make a provision for doubtful debts @ 5% on Debtors.

(2) Also make a provision for discount @ 2% on Debtors.

Prepare his Trading, P & L A/c and a Balance Sheet as at 31st March, 2019.

Solution 17:

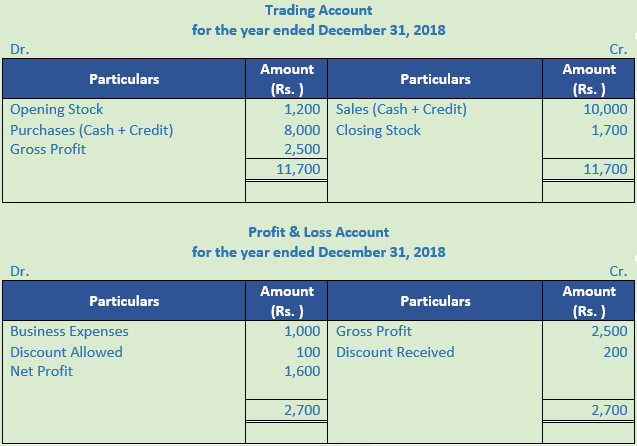

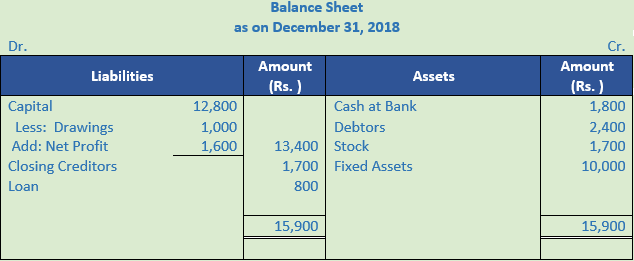

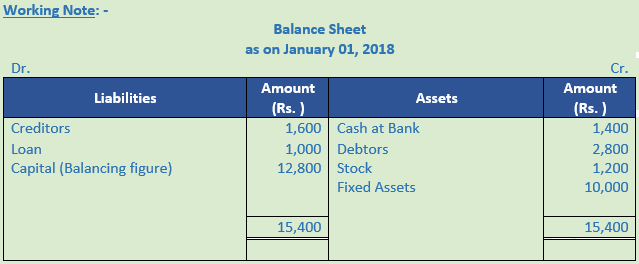

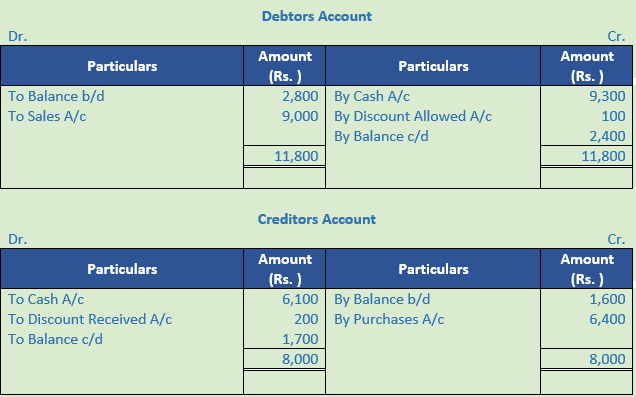

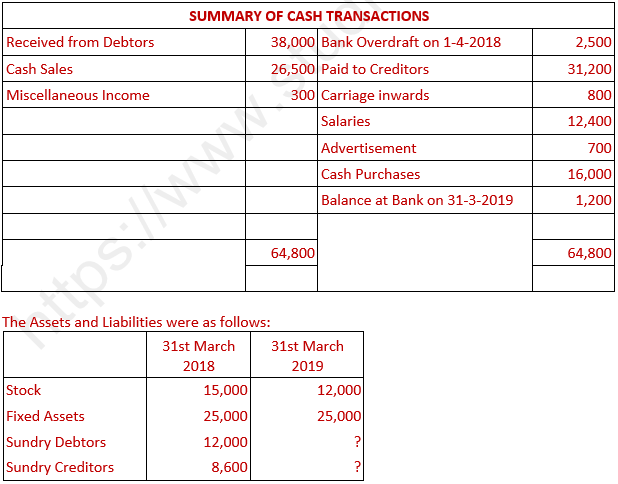

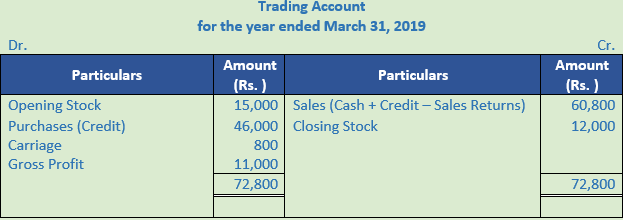

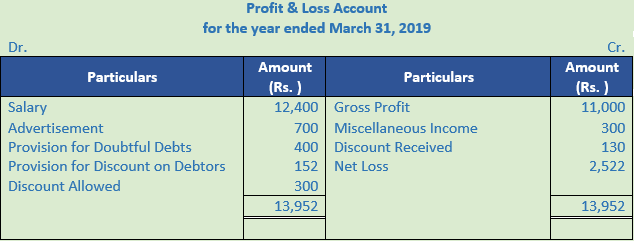

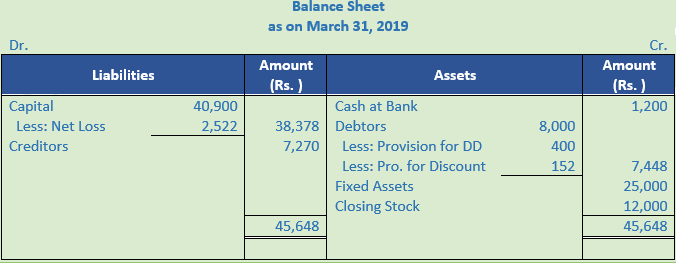

Question 18. Lalit Mohan keeps incomplete records. From the following information provided by him, prepare a Trading and Profit & Loss Account for the year ended 31st March, 2015 and a Balance Sheet as at that date:

Summary of cash transactions during the year:

You are informed that there were considerable amount of cash sales during the year. Credit purchases during the year amounted to Rs. 1,80,000. Provide 5% for doubtful debts on debtors.

Solution 18:

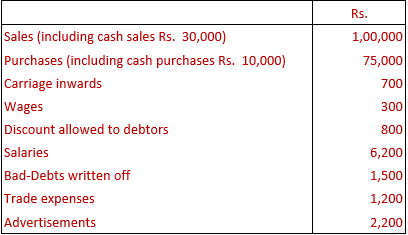

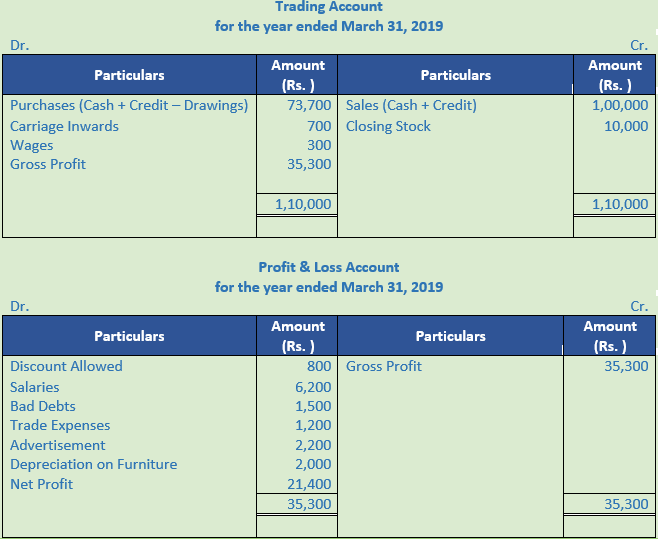

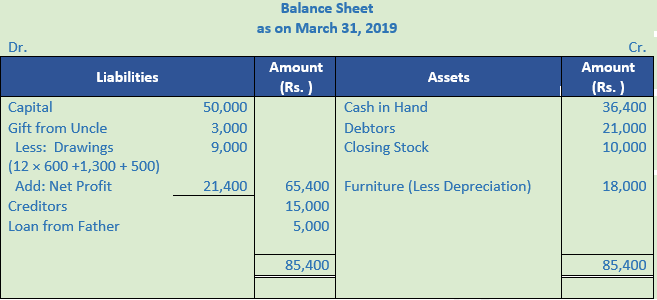

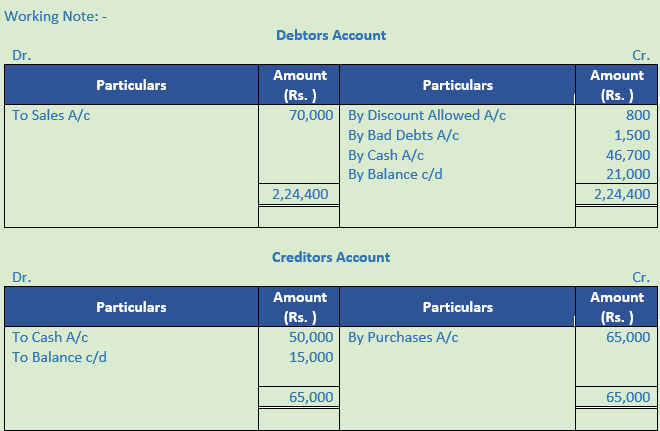

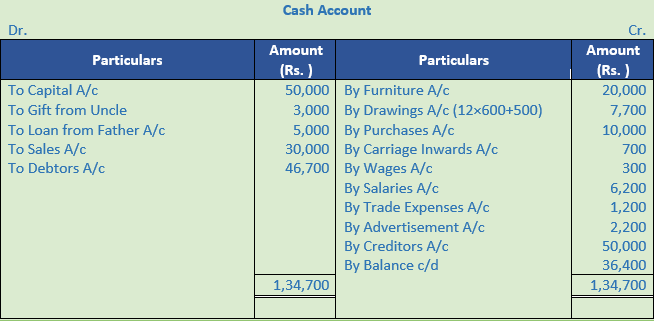

Question 19. Vardhman commenced business on 1st April, 2018, with a capital of Rs. 50,000. He immediately purchased furniture of Rs. 20,000. During the year he received from his uncle a gift of Rs. 3,000 and he borrowed from his father a sum of Rs. 5,000. He had withdrawn Rs. 600 per month for his household expenses. He had no Bank account and all dealings were in cash. He did not maintain any books but following information is given:

He used goods worth Rs. 1,300 for personal purposes and paid Rs. 500 to his son for examination and college fees.

On 31st March, 2019, his Debtors were worth Rs. 21,000 and Creditors Rs. 15,000. Stock in trade was valued at Rs. 10,000. Furniture to be depreciated by 10% p.a.

Prepare Trading and Profit and Loss Account for the year ended on 31st March, 2019, and Balance Sheet as at 31st March, 2019.

Solution 19:

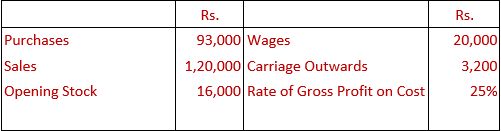

Question 20. Calculate the value of Closing Stock from the following particulars:

Solution 20:

Rate of Gross Profit (on cost) = 25%

Rate of Gross Profit (on sales) = 20%

Gross Profit = Rs. 1,20,000 × 20%

Gross Profit = Rs .24,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = Rs. 1,20,000 – Rs. 24,000

Cost of Goods Sold = Rs. 96,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Closing Stock = Opening Stock + Purchases + Direct Expenses – Cost of Goods Sold

Closing Stock = Rs. 16,000 + Rs. 93,000 + Rs. 20,000 – Rs. 96,000

Closing Stock = Rs. 33,000

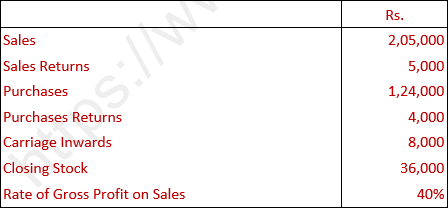

Question 21. Calculate the value of Opening Stock from the following:

Solution 21:

Rate of Gross Profit (on sales) = 40%

Gross Profit = 40% × (2,05,000 – 5,000)

Gross Profit = 80,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales –Gross Profit

Cost of Goods Sold = Rs. 2,00,000 – Rs. 80,000

Cost of Goods Sold = Rs. 1,20,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

1,20,000 = Opening Stock + (Rs. 1,24,000 – Rs. 4,000) + Rs. 8,000 – Rs. 36,000

Opening Stock = Rs. 1,20,000 – Rs. 1,20,000 – Rs. 8,000 + Rs. 36,000

Opening Stock = Rs. 28,000

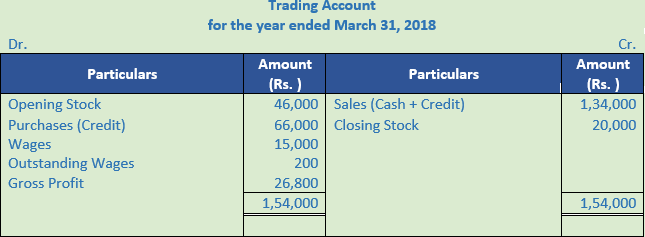

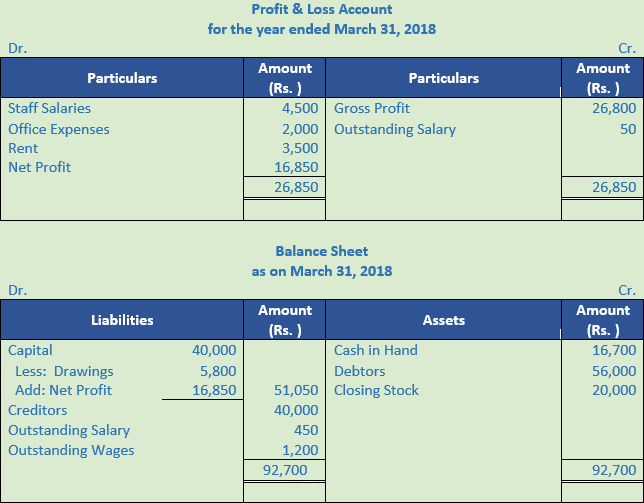

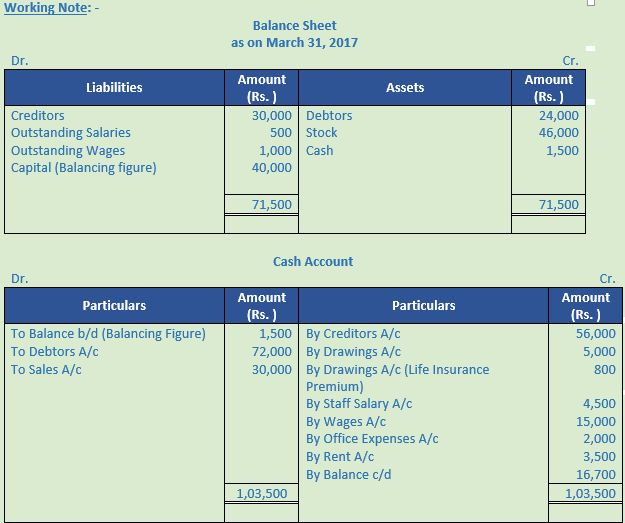

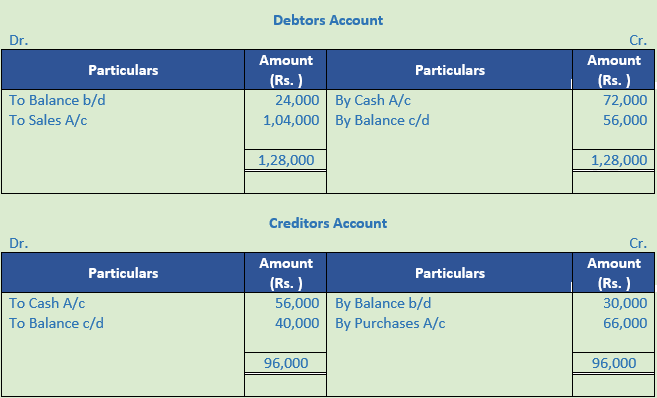

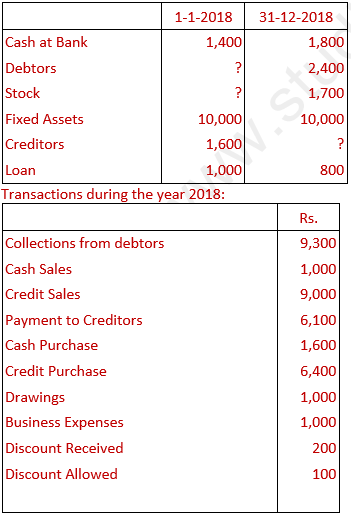

Question 22. Chakravarti does not maintain proper books of accounts. Following information is obtained from his books for the year ended 31st March, 2018:

The Stock on 31st March, 2018 was valued at Rs. 20,000 but Chakravarti has no record of the Stock on 1st April, 2017. However, he informs you that he sells his goods at cost plus 25%.

Prepare his Cash Book, Trading and P & L A/c for the year ended 31st March, 2018 and a Balance Sheet as at that date.

Solution 22:

Rate of Gross Profit (on cost) = 25%

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% of (30,000 + 1,04,000)

Gross Profit = 26,800

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 1,34,000 – 26,800

Cost of Goods Sold = Rs. 1,07,200

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

1,07,200 = Opening Stock + 66,000 + (15,000 + 200) – 20,000

Opening Stock = 1,07,200 – 66,000 – 15,200 + 20,000

Opening Stock = Rs. 46,000

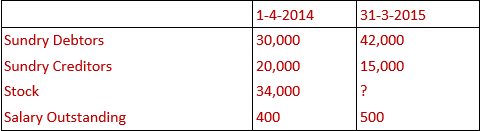

Question 23. Mr. Gopal Das has only a Bank Pass Book and does not keep any other books of accounts. From the following information prepare his Final Accounts for the year ended 31st March, 2015.

An analysis of the Pass Book shows:-

Total amount received from Debtors and deposited with the Bank Rs. 2,20,000; Payment to Creditors Rs. 1,82,000; Salaries Rs. 6,000; Rent paid Rs. 4,800; Advertisement Rs. 2,000; Printing Rs. 800; Personal Expenses Rs. 4,000; Payment for Furniture Rs. 12,000; Balance at Bank on 31st March, 2015, Rs. 21,000.

Other Assets and Liabilities were as follows:

Mr. Gopal Das takes 20% profit on sales.

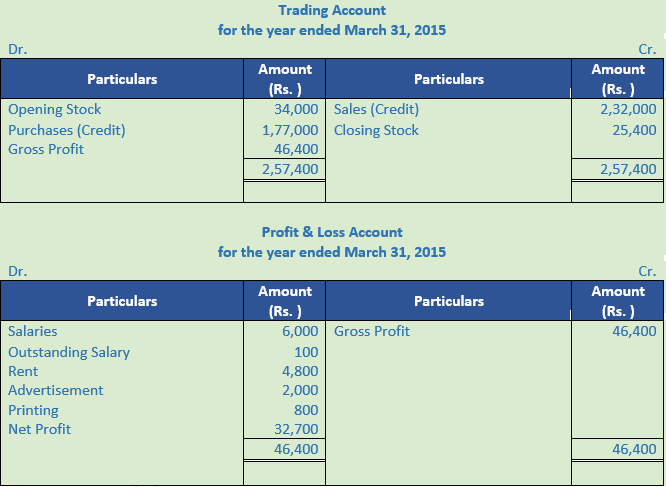

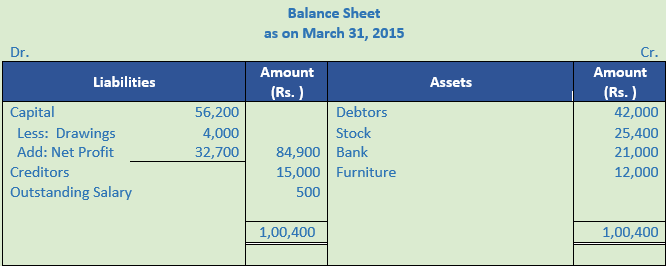

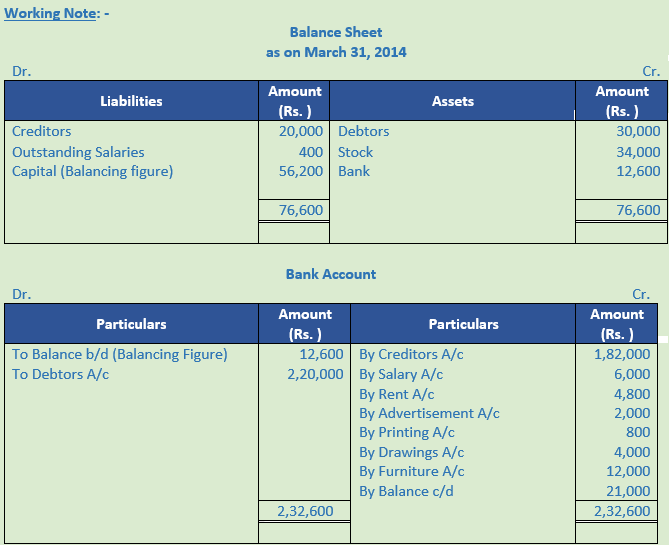

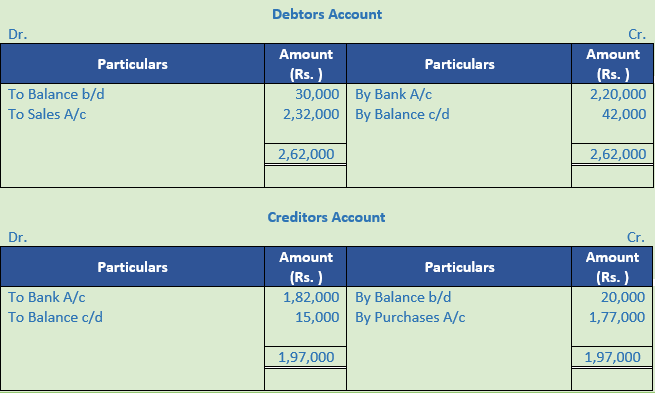

Solution 23:

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% × Rs. 2,32,000

Gross Profit = Rs. 46,400

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Gross Profit - Net Sales

Cost of Goods Sold = Rs. 2,32,000 – Rs. 46,400

Cost of Goods Sold = Rs. 1,85,600

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

1,85,600 = 34,000 + 1,77,000 – Closing Stock

Closing Stock = 34,000 + 1,77,000 – 1,85,600 = Rs. 25,400

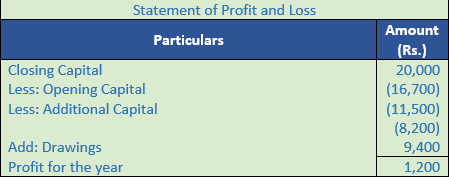

Question 24. Ravi, who keeps his books on Single Entry System, had his capital on 31st March, 2016 Rs. 20,000 and on 1st April, 2015 was Rs. 16,700. He further informs that during the year, he withdrew for his personal expenses Rs. 9,400. He also sold his personal investment of Rs. 10,000 at 15% premium and brought that money into the business.

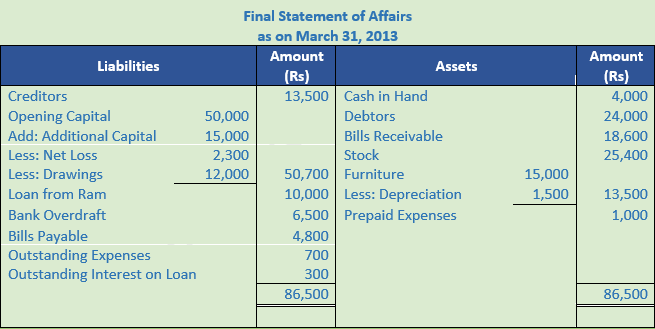

Prepare a statement of Profit or Loss.

Solution 24:

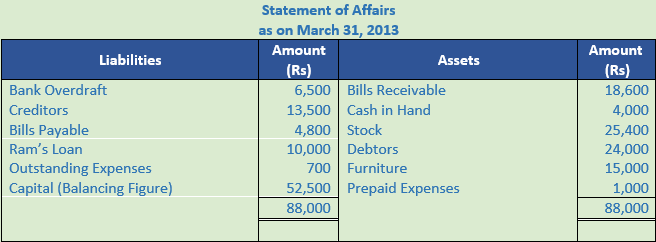

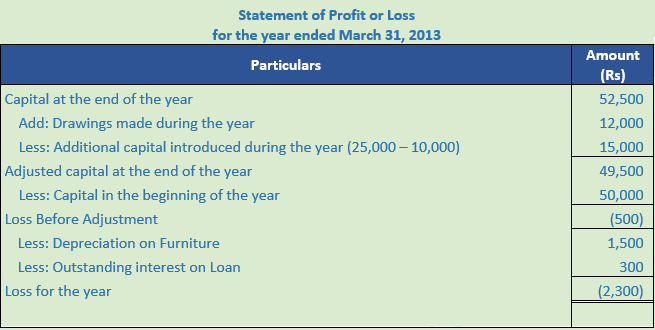

Question 25. Mohan commenced business on 1st April, 2012 with a capital of Rs. 50,000. On 1st January, 2013, he introduced Rs. 25,000 into business of which Rs. 10,000 was borrowed from Ram. His position on 31st March, 2013 was as under:

Assets: Cash in hand Rs. 4,000; Bank (Cr.) Rs. 6,500; Debtors Rs. 24,000; B/R Rs. 18,600.

Stock Rs. 25,400; Furniture Rs. 15,000; Prepaid expenses Rs. 1,000.

Liabilities: Creditors Rs. 13,500; B/P Rs. 4,800; Ram's Loan Rs. 10,000; Outstanding expenses Rs. 700.

Actual drawings were not known but his living expenses are Rs. 1,000 p.m. Depreciate furniture by 10%. Interest on loan is due @ 12% p.a.

Ascertain his profit or loss for the year 2012-13 & prepare final statement of affairs.

Solution 25:

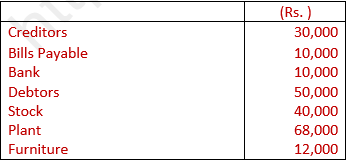

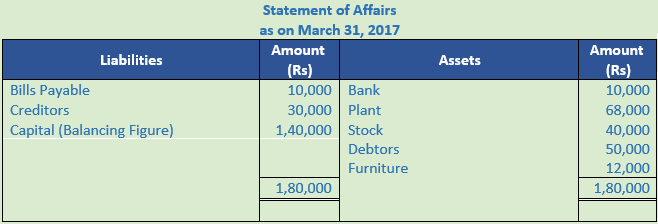

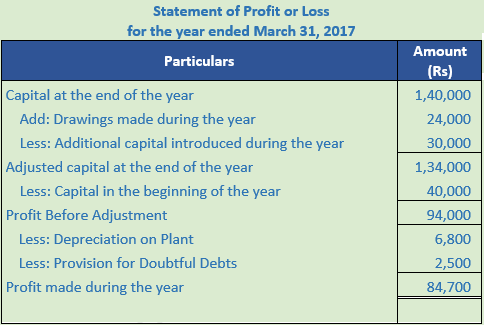

Question 26. On April 1st, 2016, X started a business with Rs. 40,000 as his capital. On March 31st, 2017, his position was as follows:

During the year 2016-17 X drew Rs. 24,000. On 1st October 2016, he introduced further capital amounting to Rs. 30,000. You are required to ascertain profit or loss made by him during the year 2016-17.

Adjustments:

(a) Plant is to be depreciated at 10%.

(b) A Provision of 5% is to be made against debtors.

Also prepare the Statement of Affairs as on March 31st 2017.

Solution 26:

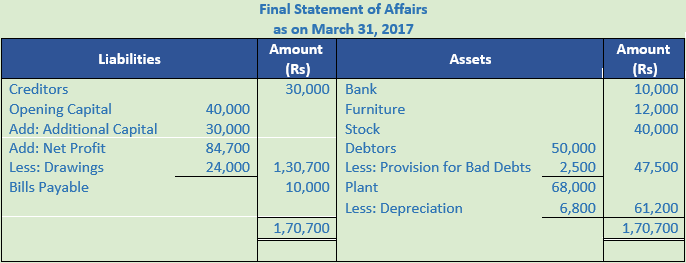

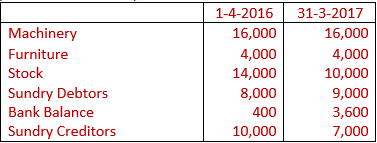

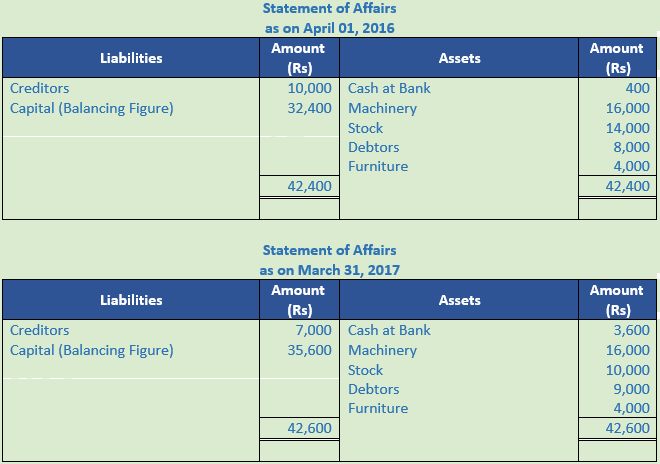

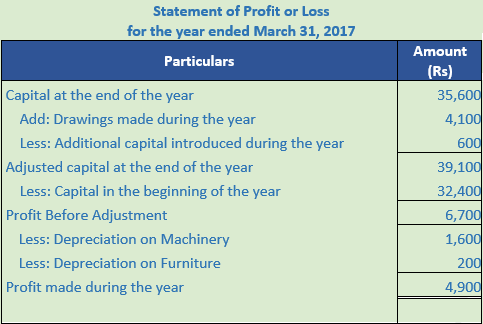

Question 27. From the following information relating to the business of Mr. X who keeps books by single entry ascertain the profit or loss for the year ended 31st March, 2017:

Mr. X withdrew Rs. 4,100 during the year to meet his household expenses. He introduced Rs. 600 as fresh capital. Machinery and furniture to be depreciated by 10% and 5% per annum respectively.

Solution 27:

Question 28. Mr. A does not keep proper records of his business. Following information is available from records kept by him:

Mr. A withdrew from the business Rs. 3,000 per month upto 30th September 2016 and thereafter Rs. 4,000 per month as drawings. Rs. 50,000 realised by the proprietor as maturity value of National Saving Certificates was invested in the business.

Prepare a statement showing net profit (or net loss) for the year.

Solution 28:

Question 29. Mr. White does not keep his books properly. Following information is available from his books.

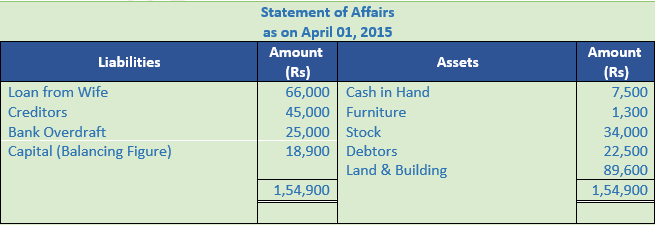

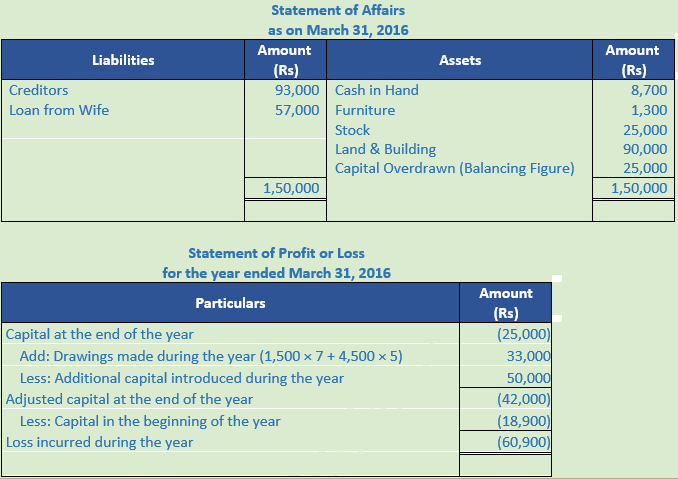

During the year Mr. White sold his private car for Rs. 50,000 and invested this amount into the business. He withdrew from the business Rs. 1,500 per month upto 31st October, 2015 and thereafter Rs. 4,500 per month as drawings. You are required to prepare a statement of profit or loss and a statement of affairs as at March 31, 2016.

Solution 29:

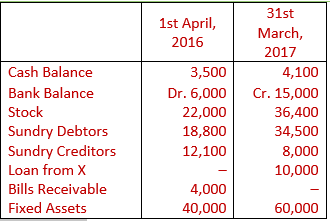

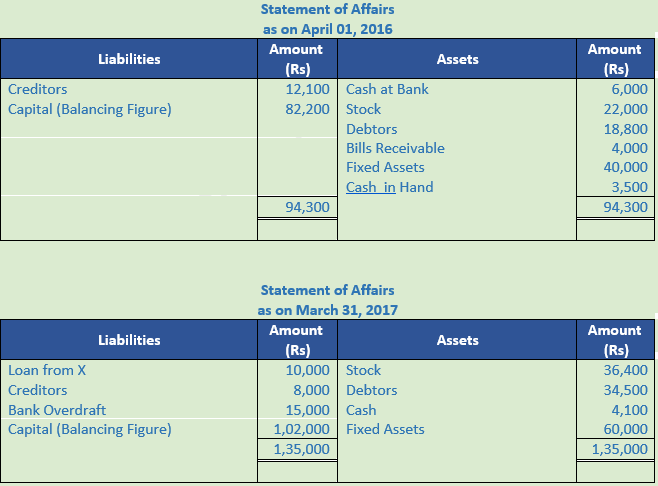

Question 30. X who keeps incomplete records, gives you the following information:

You are also given the following information:

(i) A provision of Rs. 1,450 is required for bad and doubtful debts.

(ii) Depreciation @ 5% is to be written off on Building and furniture.

(iii) Wages outstanding Rs. 3,000; salaries outstanding Rs. 1,200.

(iv) Insurance has been prepaid to the extent of Rs. 250.

(v) Legal Expenses outstanding Rs. 700.

(vi) Drawings of Mr. X during the year were Rs. 7,520.

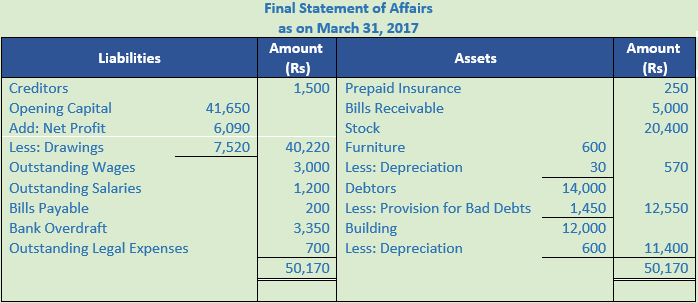

Prepare a statement of Profit as on 31st March, 2017, and a final statement of affairs as at that date.

Solution 30:

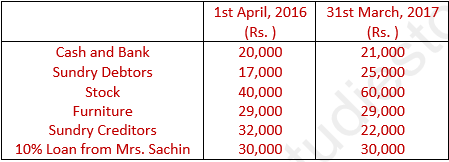

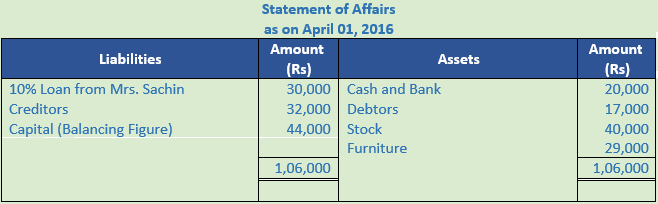

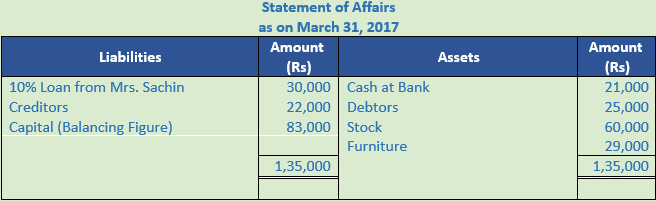

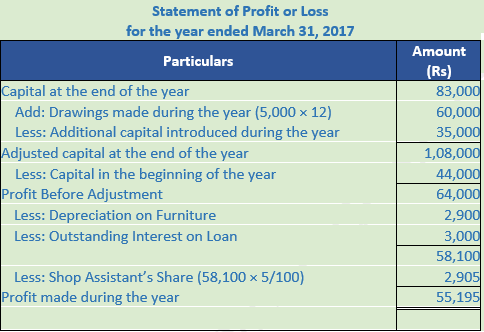

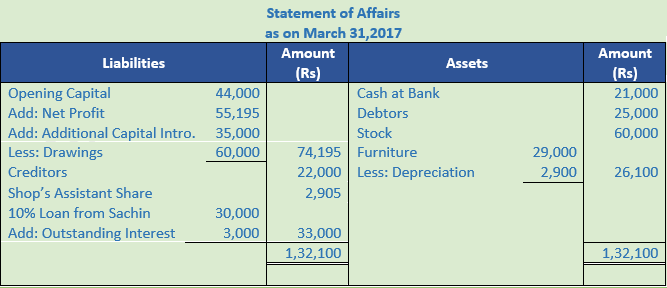

Question 31. The following information is available from Sachin, who maintains books of accounts on single entry system:

Sachin withdrew Rs. 5,000 from the business every month for meeting his household expenses. During the year, he sold investments held by him privately for Rs. 35,000 and invested the amount in his business.

At the end of the year 2016-17, it was found that full year's interest on loan from Mrs. Sachin had not been paid. Depreciation @ 10% per annum was to be provided on furniture for the full year. Shop assistant was to be given a share of 5% on the profits ascertained before charging such share.

Calculate profit earned during the year ended 31st March, 2017 by Sachin.

Solution 31:

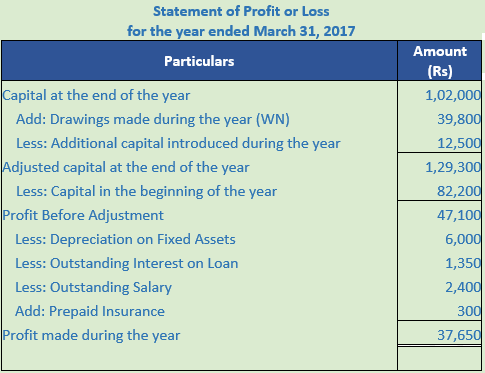

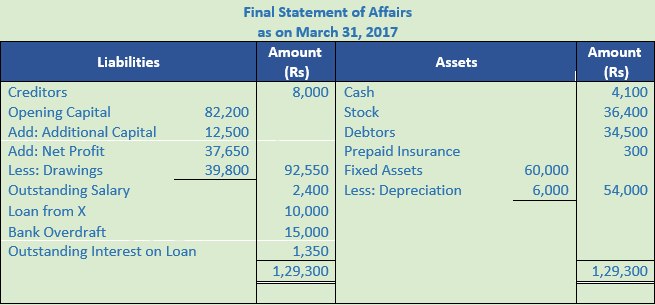

Question 32. A retail Trader has not kept proper books of accounts. Ascertain his profit or loss for the year ending 31st March, 2017, and prepare a final statement of affairs from the following information:

He withdrew from the business Rs. 1,500 per month for his personal use and Rs. 8,000 for giving a personal loan to his brother. He also used a house for his personal purposes, the rent of which at the rate of Rs. 900 per month and electricity charges at an average rate of Rs. 250 per month were paid from the business account.

He had received a lottery prize of Rs. 25,000, out of which he invested half the amount in business.

He has not paid two months' salary to his clerk @ Rs. 1,200 per month, but insurance premium @ Rs. 600 per annum was paid on 1st October, 2016 to run for one year.

Loan from X was taken on 1st July, 2016 on which interest was unpaid @ 18% p.a.

Fixed assets are to be depreciated @ 10% p.a.

Solution 32:

Working Note:-

Calculation of Amount of Drawings:-

Cash Withdrawn = Rs 18,000

Loan to Brother = Rs 8,000

Rent = Rs 10,800

Electricity Charges = Rs 3,000

Total Drawings = Rs 39,800

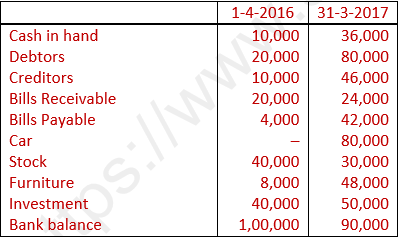

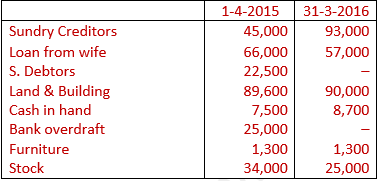

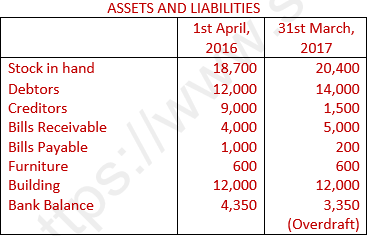

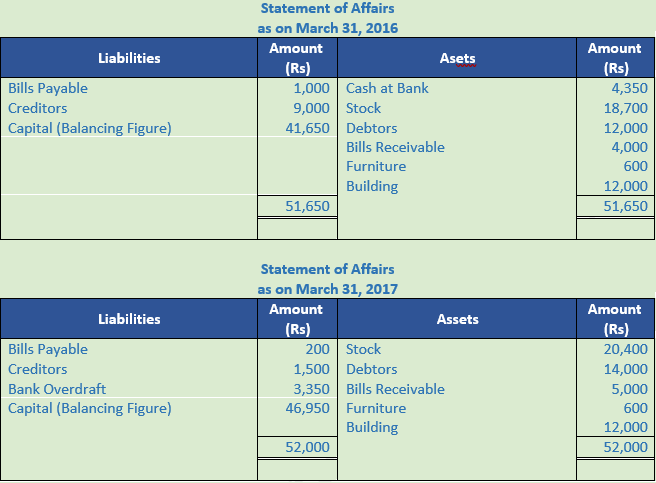

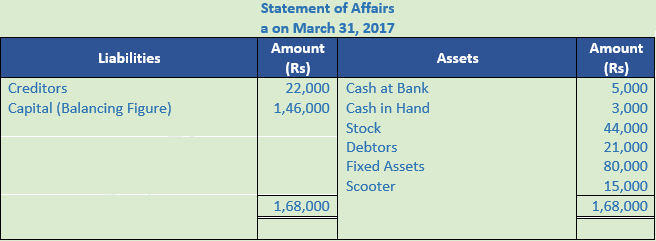

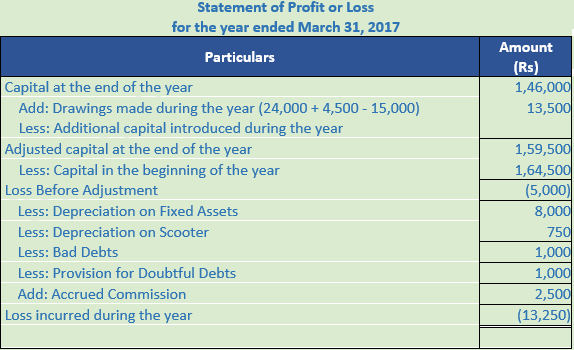

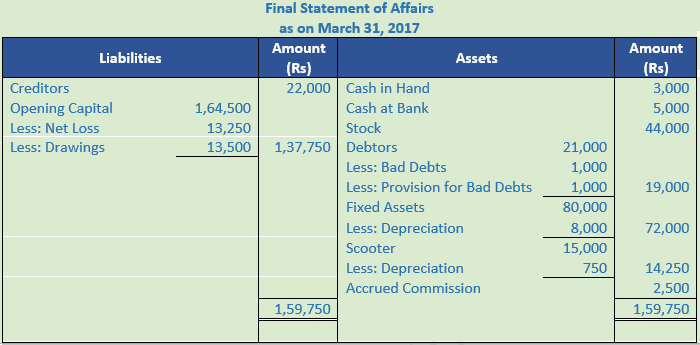

Question 33. Gopal keeps incomplete records. On 1st April, 2016, his position was as follows:

His position on 31st March, 2017 was as follows:

Cash in hand Rs. 3,000; Cash at Bank Rs. 5,000; Stock Rs. 44,000; Debtors Rs. 21,000; Fixed Assets Rs. 80,000; Creditors Rs. 22,000.

You are informed that Gopal has taken stocks worth Rs. 4,500 for his private use and that he has been regularly transferring Rs. 2,000 per month from his business banking account by way of drawings. Out of his drawings he spent Rs. 15,000 for purchasing a Scooter for the business on 1st October, 2016.

You are requested to find out his profit or loss and to prepare the Statement of Affairs after considering the following :

- Depreciate Fixed Assets and Scooter by 10% p.a.

- Write off Bad-Debts Rs. 1,000 and provide 5% for doubtful debts on Sundry Debtors.

- Commission earned but not received by him was Rs. 2,500.

Solution 33:

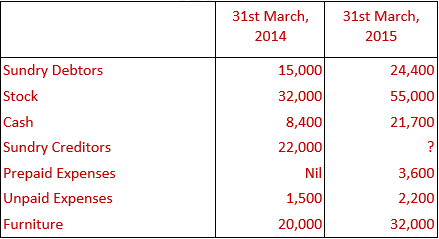

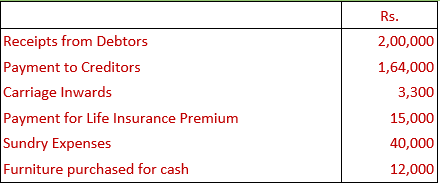

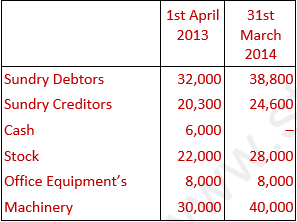

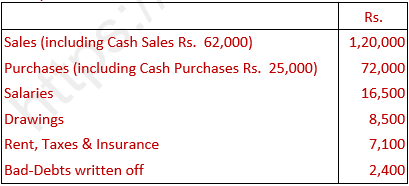

Question 34. A retail trader did not keep his books on the double entry system. Following balances were obtained from his books:

Following further details of the transactions for the year ended 31st March, 2014 are available from his incomplete records:

You are required to prepare his Trading, P & L A/c and Balance Sheet after considering the following:

- Rs. 1,500 are outstanding for salaries.

- Insurance was unexpired to the extent of Rs. 800.

- Goods worth Rs. 2,000 were used by the proprietor for personal use.

Solution 34:

Question 35. Mr. Manoj keeps incomplete records. During the year 2014-15 the analysis of his cash book was as under:-

Other Information’s:

(i) Credit sales during the year were Rs. 7,00,000

(ii) Sales Returns were Rs. 10,000

(iii) Discount allowed to debtors Rs. 8,400

(iv) Discount received from creditors Rs. 6,000

(v) Bad-debts written off during the year Rs. 11,400

Adjustments:

(i) Write off further bad-debts Rs. 2,000.

(ii) Provide 5% for doubtful debts and 2% for discount on debtors and creditors.

(iii) Charge 10% p.a. depreciation on furniture.

(iv) One month salaries and one month rent was outstanding.

Prepare Trading and Profit & Loss Account for the year ended 31st March, 2015 and a Balance Sheet as at that date.

Solution 35:

Working Note:-

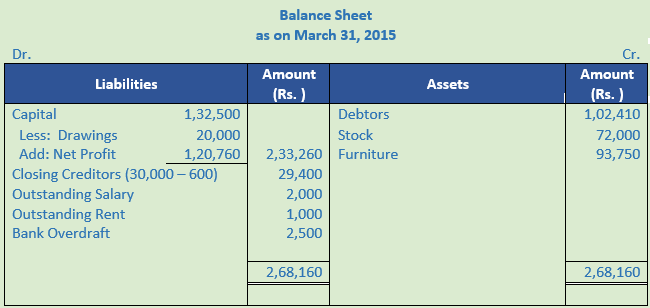

Calculation of Capital = 82,500 + 50,000 – 20,000 + 1,20,760 = 2,33,260

Calculation of Debtors = 1,12,000 – 2,000 –5,500 – 2,090 = 1,02,410

Calculation of Closing Creditors = 30,000 – 600 = 29,400

Calculation of Furniture = 25,000 + 75,000 – 6,250 = 93,750

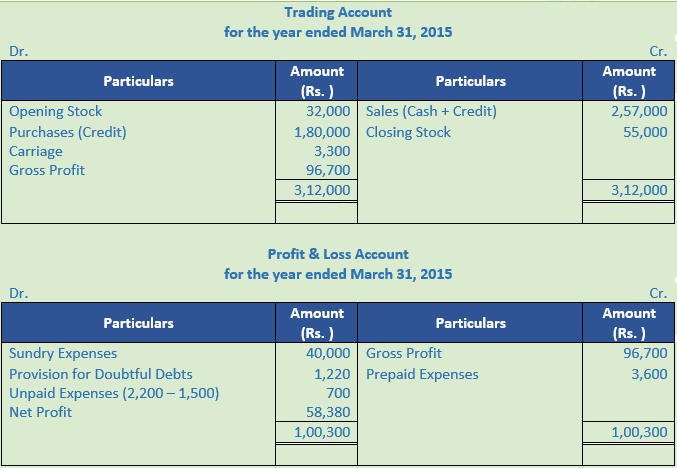

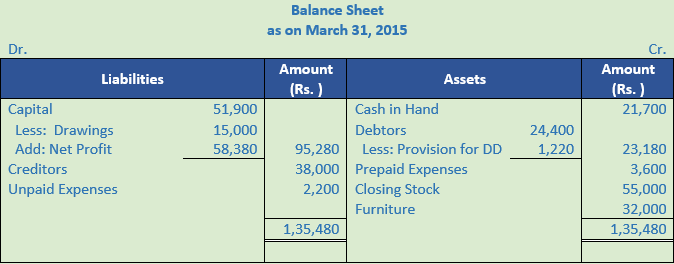

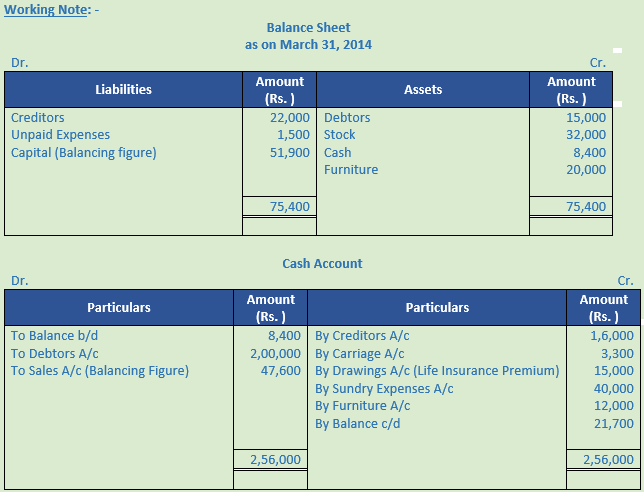

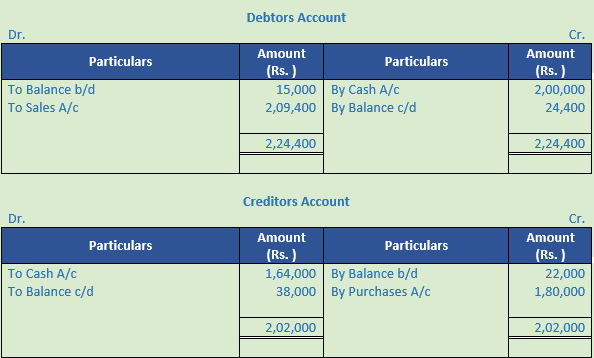

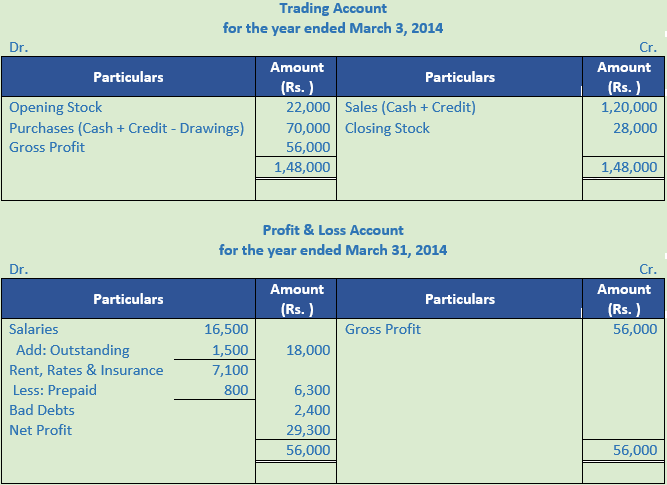

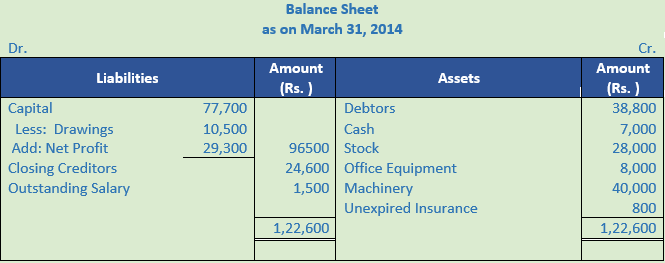

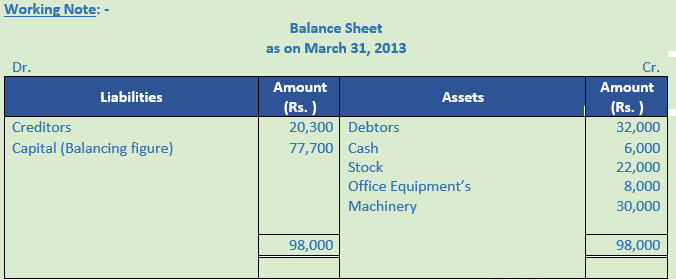

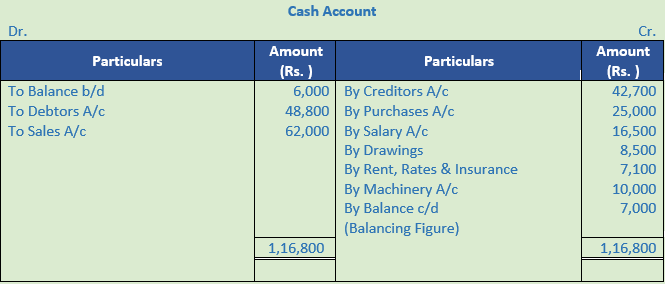

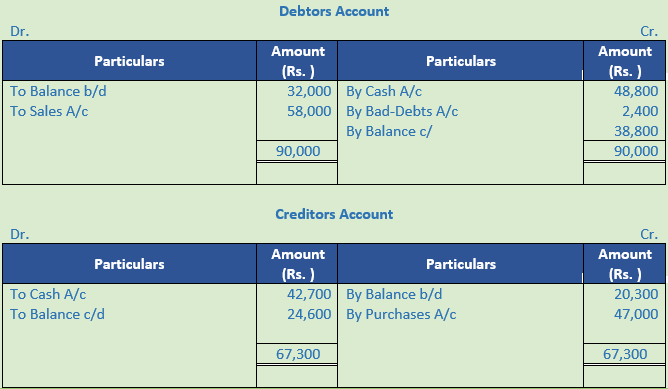

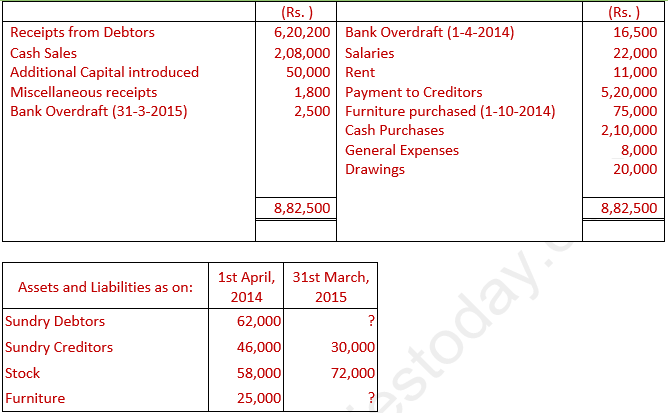

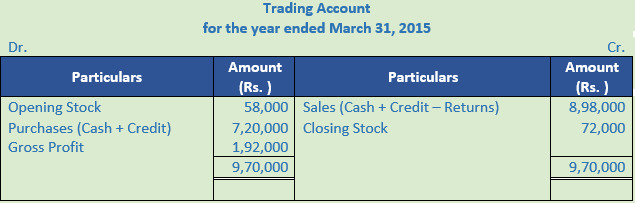

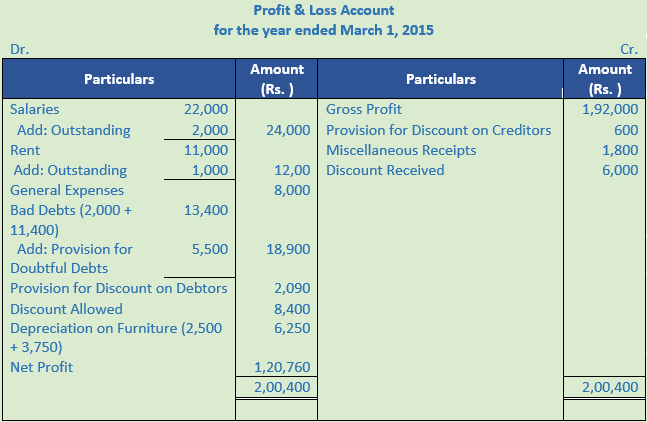

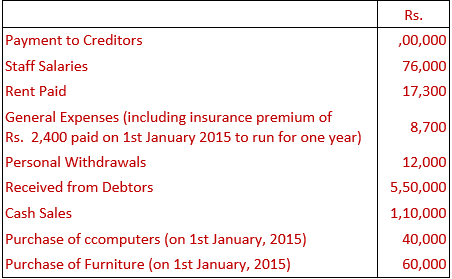

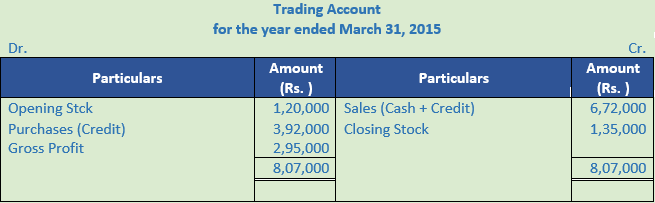

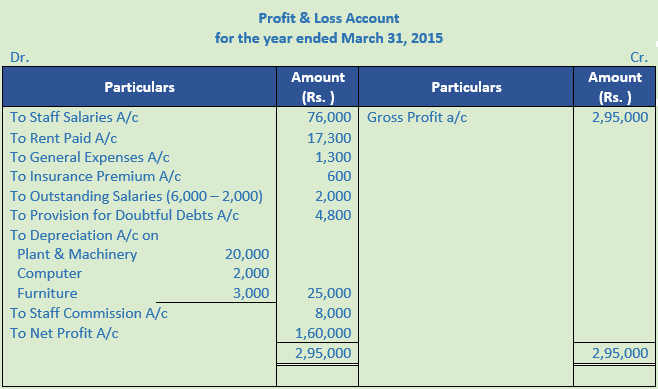

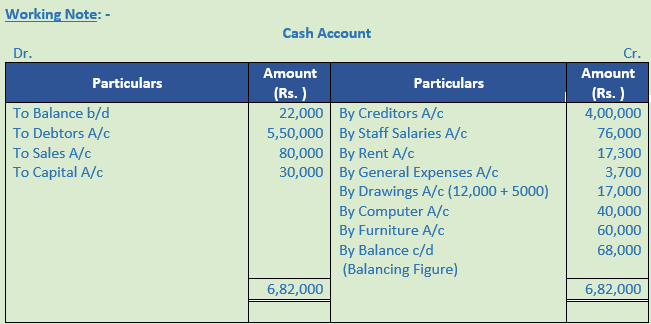

Question 36. Sh. Param Bhushan does not maintain proper books of accounts. From the following, prepare his trading and profit & loss account for the year ended 31st March, 2015, together with balance sheet as at that date:

Cash book analysis shows the following:

The following further information is available:

Closing Stock Rs. 1,35,000; Closing Debtors Rs. 1,92,000; Closing Creditors Rs. 72,000; Outstanding Salaries at the end Rs. 6,000; General Expenses include Rs. 5,000 for house rent of Sh. Param Bhushan and Cash Sale include Rs. 30,000 for sale of his personal jewellery.

Create a provision of 5/2 % for doubtful debts and depreciate plant and machinery by 10% p.a. and computers and furniture by 20% p.a. Also provide 5% for group incentive commission to staff on net profit after charging such commission.

Solution 36:

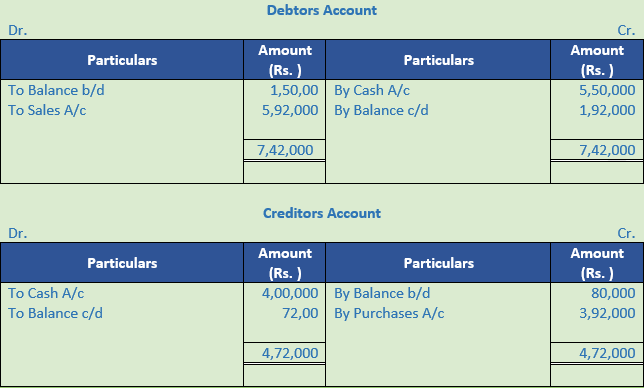

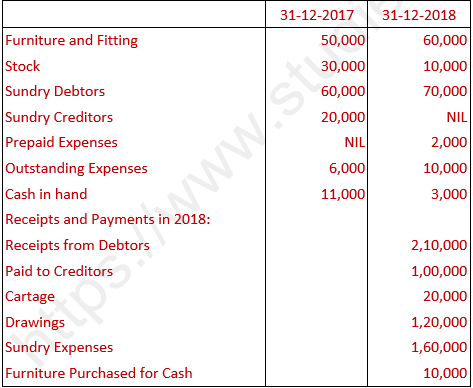

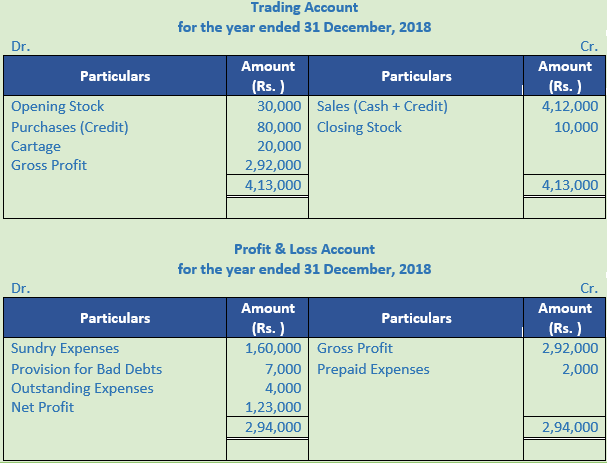

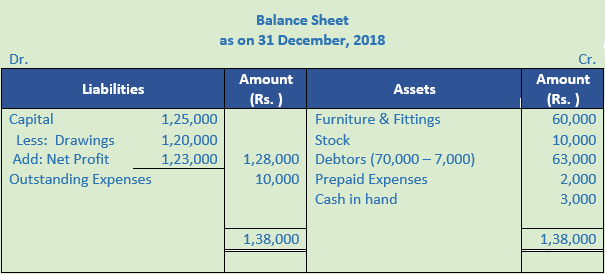

Question 37. Sonam keeps his books on single entry and provides you with the following information:

Prepare Trading and Profit & Loss Account for the year ended 31 December, 2018 after providing for bad debts at 10%. There was a considerable amount of Cash Sales.

Solution 37:

Question 38. Ascertain the value of Closing Stock from the following:

Rate of G.P. on cost is 25%.

Solution 38:

Rate of Gross Profit (on cost) = 25%

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% × 1,00,000 = 20,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales - Gross Profit

Cost of Goods Sold = 1,00,000 – 20,000

Cost of Goods Sold = Rs. 80,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

80,000 = 18,000 + 69,000 + 10,000 – Closing Stock

Closing Stock = 18,000 + 69,000 + 10,000 – 80,000 = Rs. 17,000

Question 39. From the following particulars, ascertain the value of Opening Stock:-

Solution 39:

Rate of Gross Profit (on cost) = 50%

Rate of Gross Profit (on sales) = 33.33%

Gross Profit = 33.33% × 1,05,000 = 35,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales - Gross Profit

Cost of Goods Sold = 1,05,000 – 35,000

Cost of Goods Sold = Rs. 70,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

70,000 = Opening Stock + 60,000 + 3,000 – 20,000

Opening Stock = 70,000 – 60,000 – 3,000 + 20,000 = Rs. 27,000

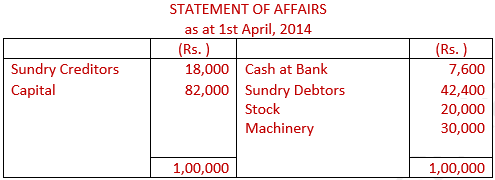

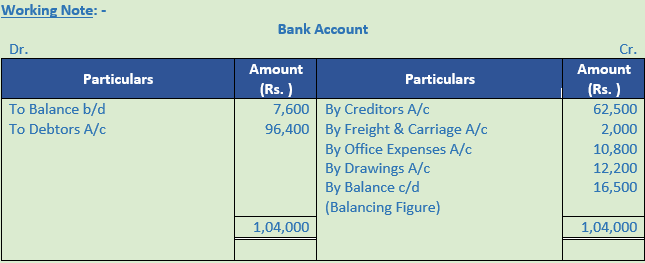

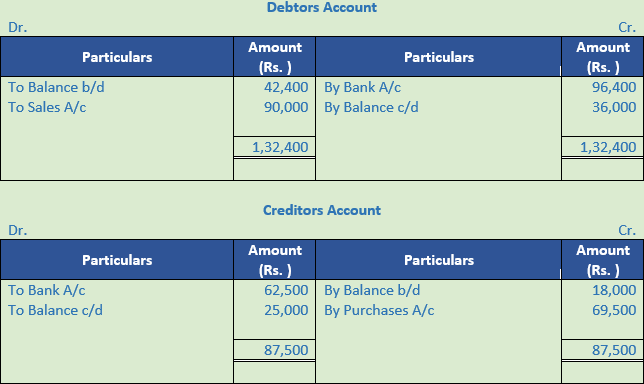

Question 40. Mr. Bhardwaj has kept incomplete records. He submits to you the following information:

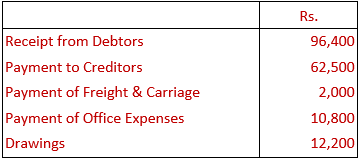

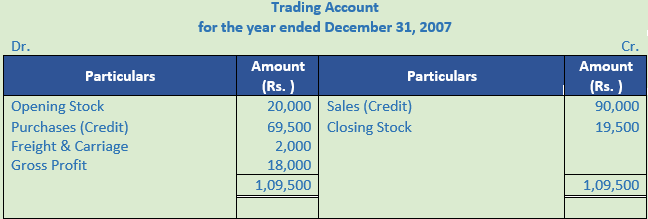

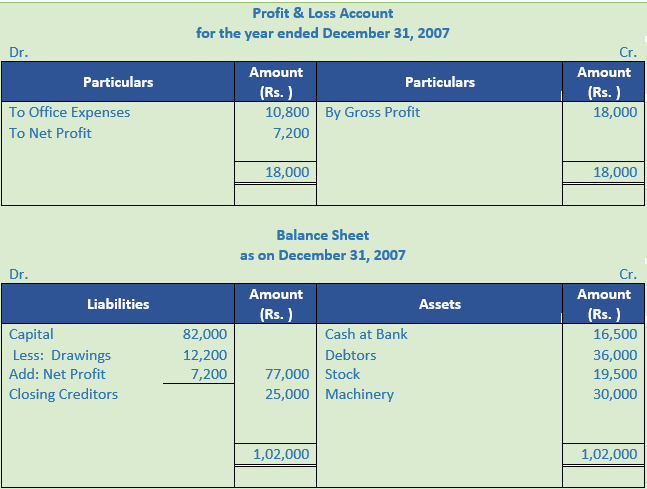

Bhardwaj banks all receipts and makes all payments only by means of cheques. Following is the analysis of his bank transactions:

Sundry Debtors on 31st March, 2015 were Rs. 36,000 and Sundry Creditors were Rs. 25,000. No information is available regarding stock-in-trade on 31st March, 2015, but it is ascertained that Mr. Bhardwaj takes 20% profit on Sales. Prepare Bhardwaj's Bank A/c, Trading and Profit & Loss A/c and a Balance Sheet as at 31st March, 2015.

Solution 40:

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% × 90,000

Gross Profit = 18,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 90,000 – 18,000

Cost of Goods Sold = Rs. 72,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

72,000 = 20,000 + 69,500 + 2,000 – Closing Stock

Closing Stock = 20,000 + 69,500 + 2,000 – 72,000 = Rs. 19,500

Question 41. From the following records kept on single entry basis, prepare final accounts assuming that ratio of gross profit to sales is 25%:

Solution 41: