Read DK Goel Class 11 Accountancy Solutions for Chapter 11 Books of Original Entry Cash Book below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 11 Books of Original Entry Cash Book should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 11 Books of Original Entry Cash Book DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 11 Books of Original Entry Cash Book in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 11 Books of Original Entry Cash Book Class 11 Accountancy

Short Answer Questions

Question 1. What is Sub-division of Journal?

Solution 1: It is convenient to maintain a separate book for each such class of transactions-one to record cash transactions, another to record credit purchase of goods and yet another to record credit sale of goods. All of these books are called the books of original entry or primary entry or subsidiary books - it is a special form of Journal, a sub-division of Journal.

Question 2. Name the various books of original entries.

Solution 2: Below are the books of original entries:-

- Cash Book

- Purchases Book

- Sales Book

- Purchases Return Book

- Sales Return Book

- Bills Receivable Book

- Bills Payable Book

- Journal Proper

Question 3. Elucidate the following statements:-

(a) ‘Only cash transactions are recorded in Cash Book’.

(b) ‘Cash Book is both Journal and Ledger’.

Solution 3: (a) Only Cash transactions are recorded in Cash Book because only cash or bank related transactions are recorded in this book. Also Cash Book always shows a debit balance. Cash Column in the Cash Book cannot show a credit balance because cash payments cannot exceed cash receipts. At best, it can show nil balance when total cash receipt are equal to total payment.

(b) Cash Book is both Journal and Ledger because cash Book is a book in which all transactions relating to cash receipts and cash payments are recorded. It starts with the cash or bank balances at the beginning of the period. Generally, it is made on monthly basis. This is a very popular book and is maintained by all organisations, big or small, profit or not-for-profit. It serves the purpose of both journals as well as ledger account.

Question 4. How does a Cash Book serve ‘Dual Purpose’?

Solution 4: Cash book plays both roles as an original books and a ledger. Cash Book serves the dual purpose or both books of original entry and the Ledger. When we are make cash book no need to make a separate cash account. A transaction is only to be recorded in cash book or cash account if there is either inflow or outflows of cash. Thus cash book serves dual purpose.

Question 5. What is Contra entry? How will you recognise it from among other entries in Cash Book?

Solution 5: Some transactions are recorded in a Two-Column Cash Book which relate to both cash and bank, i.e., balance of one will decrease and the other will increase due to such transactions. Such transactions are entered on both sides of the Cash Book. Such entries are knows as Contra Entries. Let us take an example to understand it better.

(a) Cash deposited into the Bank 10,000: In this transaction, Bank Account is to be debited and Cash Account is to be credited. Debit aspect is recorded on the debit side of the Bank Column and credit aspect is recorded on the credit side of Cash Column.

(b) Cash withdrawn from Bank for Office Use 1,000: In this transaction Cash Account is to be debited and Bank Account is credited. Debit aspect is recorded on the debit side of the Double Column Cash Book in the Cash Column and credit aspect is recorded on the credit side of the Double Column Cash Book in the Bank Column.

Against such entries, the letter 'C' is written in the L.F. column to indicate that these are contra transactions and are not posted into the Ledger Account.

Question 6. State three advantages of Sub-Division of Journal.

Solution 6: The three advantages of Sub-Division of Journal are:-

(i) Division of work according to ability.

(ii) Easiness in posting.

(iii) Time Saving

Question 7. Explain how the following transactions would be recorded in a Cash Book with Cash and Bank Columns?

(i) Deposit of Cash into Bank

(ii) Withdrawal of money from Bank for office use.

(iii) Deposit of cheque (received from other) into Bank.

(iv) Dishonour of cheque deposited into Bank.

Solution 7: (i) Deposit of Cash into Bank:-

Journal entry:

Bank a/c Dr.

To Cash A/c

In the above transaction both the account are affected a cash account and bank account. Hence it is contra entry because cash and bank both accounts is affected on same time. The cash account is credited this shows by recording the amount in the cash column of the cash book on the credit side to show a decrease in the asset of cash and the bank account is debited and this is shown by recording a debit in the bank column of the cash book.

(ii) Withdrawal of money from bank for office use:-

Journal entry:

Cash a/c Dr.

To Bank A/c

In the above transaction both the account are affected a cash account and bank account. Hence it is contra entry because cash and bank both accounts is affected on same time. The bank account is credited this shows by recording the amount in the bank column of the cash book on the credit side to show a decrease in the asset of cash and the cash account is debited and this is shown by recording a debit in the cash column of the cash book it show the increase in the cash.

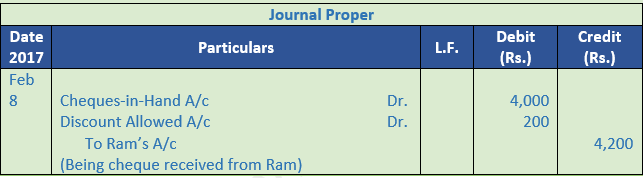

(iii) Deposit of cheque (received from other) into Bank:-

In this case we should pass a journal entry in Journal proper.

Cheque-in-hand A/c

To Debtors A/c

On the debit side "To Cheque-in-hand a/c" and on credit side “By Debtors a/c” with the same amount recorded.

(iv) Dishonour of cheque deposited into Bank:-

In this case we should pass a journal entry in Journal proper.

Debtor a/c Dr

To Bank a/c

On the credit side "By Debtor a/c" and amount will be credited into the bank account.

Question 8.

(i) Give the similarities of Cash Book with Journal.

(ii) Give the similarities of Cash Book with ledger.

Solution 8:

(i) Similarities of Cash Book with Journal:-

- Just like a journal, transactions in the cash book are recorded for the first time from source documents.

- Just like a journal, transactions in the cash book are recorded date-wise, i.e. in a chronological order, as and when they place.

- Just like a journal, transactions from cash book are also posted to the relevant accounts in the ledger.

- Just like a journal, a cash book also contains a ledger folio column.

(ii) Similarities of cash book with ledger:-

- Form of cash book closely resembles to a ledger account. It has two equally divided sides having identical columns. The left side (receipts side) is the debit side and the right side is the credit side and the right side (payment side) is the credit side.

- Cash book itself serves as a cash account also and as such when a cash book is maintained, Cash account is not opened is not opened in the ledger. The cash book, hence, is a part of ledger also.

- Just like a ledger account, the words ‘To’ and ‘By’ are used in a cash book also.

- It is balanced just like a ledger account.

Question 9. What are Contra Entries? Why these are not posted into the Ledger?

Solution 9: Contra entries means entries which are recorded on both sides of the cash book. These entries are made while depositing or withdrawing cash from the bank. Contra entries are affect the two accounts, Cash Account and Bank Account. These two accounts appear together in the Cash Book only so, the effect of Entries is completed in Cash Book and there is no need to post them in the ledger.

Question 10. Explain the Statement ‘Cash book is a journalised Ledger’.

Solution 10: Cash book is a journalised Ledger, it is a journal since cash and bank transactions are first recorded in it and a ledger since it serves the purpose of a cash account also. When a cash book is prepared, no separate Cash Account is opened in the ledger.

Question 11. Distinguish between Cash Book and Cash A/c.

Solution 11: Cash Book:- Cash Book is a book of prime entry in which cash and bank transactions are recorded in a chronological order, i.e., as they occur. Cash receipts are recorded on the debit side of the Cash Book and cash payments on the credit side. A balance is struck by deducting the total cash payments from the total cash receipts to know the cash in hand necessary and useful information.

Cash Account:- A cash account is a ledger account used for record day to day cash transactions of the business. On the debit side of the account cash receipts are recoded and or other side cash payments are recorded. Cash Account is an account which is traced cash transactions of the company. Cash book is a type of ledger.

Question 12. What is a Petty Cash Book?

Solution 12: Petty Cash Book is the book which is used for the purpose of recording expenses involving petty amounts. Besides petty expenses, receipts from main cash are recorded. Petty Cash Book is prepared by Petty Cashier and acts as the Petty Cash Account. It is maintained as in a business besides large payments, number of small payments, such as for conveyance, stationary, cartage, etc., have to be made.

Question 13. Prepare a proforma of Petty Cash Book with imaginary figures.

Solution 13:

Question 14. What is an imprest system of Petty Cash Book?

Solution 14: The imprest system of Petty Cash is explained below. Under this system, an estimate is made of amount required for petty expenses for a certain period (say for a week, a fortnight or a month). The amount so ascertained is given to the petty cashier in the beginning of a period and is reimbursed the amount paid by him during the period. Thus, he will again have the fixed amount in the beginning of the new period. This amount is called imprest money. This system of paying advance in the beginning and reimbursing the amount spent from time to time is called imprest system.

Practical Questions

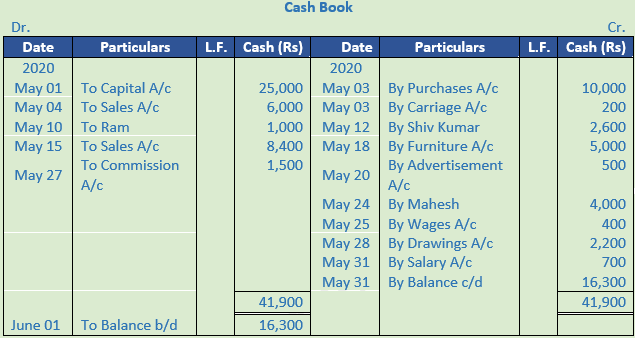

Question 1. Enter the following transactions in a Single Column Cash Book∶−

2020 (Rs.)

1 Commenced business with cash 25,000

3 Bought goods for Cash 10,000

3 Paid Carriage 200

4 Sold goods for Cash 6,000

10 Received from Ram 1,000

12 Paid to Shiv Kumar 2,600

15 ash Sales 8,400

18 Purchased furniture for cash for office 5,000

20 Paid for Advertisement 500

20 Purchased goods from Mahesh on credit 6,000

24 Paid to Mahesh 4,000

25 Paid Wages 400

27 Received for Commission 1,500

28 Withdrew for personal use 2,200

31 Paid salary 700

Solution 1:

Point of Knowledge:-

The Balancing of cash book done like any other account. Debit Column (Receipt column) is always greater than the Credit Column(payment column).

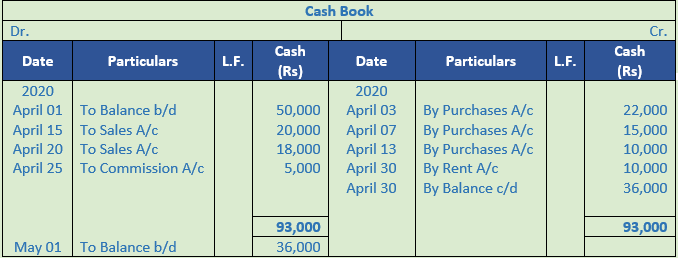

Question 2. Enter the following transactions in M/s Mukerjee & Bros. Single Column Cash Book:

2020 (Rs.)

1 Balance of Cash in hand 50,000

3 Purchased goods for cash 22,000

7 Purchased goods 15,000

10 Purchased goods from Gopi 30,000

13 Purchased goods from Gopi for cash 10,000

15 Sold goods 20,000

18 Sold goods to Vishwakarma 45,000

20 Sold goods to Raghunandan for cash 18,000

25 Received commission 5,000

30 Paid Rent

Solution 2:

Point of Knowledge:-

In the cash book only cash transaction are recorded. Credit transactions are not recorded.

The debit side is always greater than the credit as payments are never exceeds the cash available.

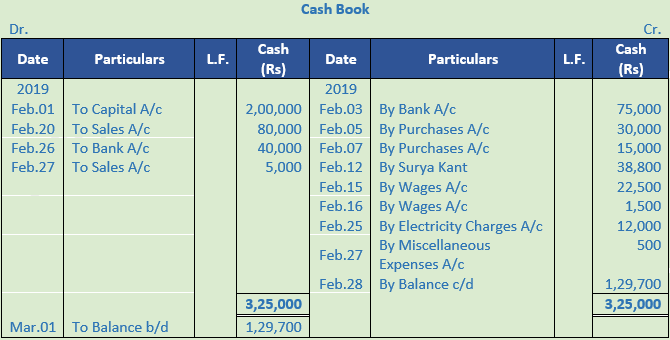

Question 3. Enter the following transactions in a Single Column Cash Book:-

2019

Feb. (Rs.)

1 Mr. Vipin commenced business with Cash 2,00,000

3 Opened a Bank Account and deposited 75,000

5 Purchased goods for Cash 30,000

7 Purchased goods 15,000

10 Purchased goods from Surya Kant 40,000

12 Paid to Surya Kant 38,800

Discount received 1,200

15 Paid Wages in Cash 22,500

16 Paid to casual labour 1,500

20 Sold goods to Dev Raj for Cash 80,000

25 Paid electricity bill in Cash 12,000

26 Withdrew Cash from Bank 40,000

27 Received for Cash sales 5,000

27 Paid for miscellaneous expenses 500

Solution 3:

Point of Knowledge:-

The Balancing of cash book done like any other account. Debit Column(Receipt column) is always greater than the Credit Column(payment column).

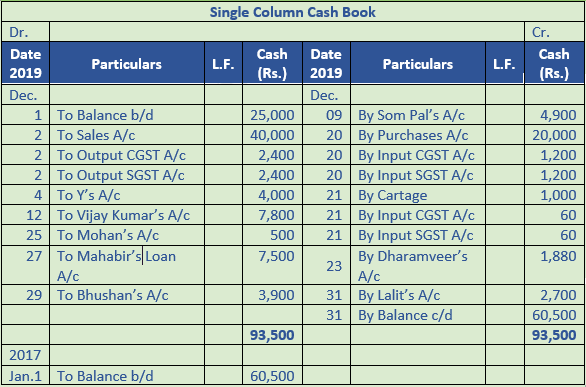

Question 4. Enter the following transactions in a Single Column Cash Book:-

2019 (Rs.)

Dec. 1 Cash-in-hand 25,000

2 Cash Sales (CGST 6%, SGST 6%) 40,000

4 Received from X on behalf of Y 4,000

9 Paid to Som Pal 4,900

Discount Received 100

12 Received from Vijay Kumar 7,800

and discount allowed 200

20 Bought goods for Cash (CGST 6%, SGST 6%) 20,000

21 Paid Cartage (CGST 6%, SGST 6%) 1,000

23 Remitted to Dharamvir 1,880

and discount allowed by him 120

25 Received M.O. from Mohan 500

27 Borrowed from Mahabir 7,500

29 Received from Bhushan 3,900

discount allowed 100

31 Paid to Lalit Rs. 2,700 in full settlement of his account of Rs. 3,000

Solution 4:

Point of Knowledge:-

Cash book is maintained to record only cash transaction so, the credit purchases are not recorded in the cash book.

Question 5. Enter the following transactions in a Single Column Cash Book of M/s Suchitra Sen & Co.

Solution 5:

Point of Knowledge:-

Cash Book is a book of prime entry in which cash and bank transactions are recorded in a chronological order, i.e., as they occur. Cash receipts are recorded on the debit side of the Cash Book and cash payments on the credit side. A balance is struck by deducting the total cash payments from the total cash receipts to know the cash in hand necessary and useful information.

Question 6. Write up Cash Book of Bhanu Partap with Cash and Bank Columns from the following transactions:−

Solution 6:

Point of Knowledge:-

Contra Entry is an entry which includes both Cash & Bank Account and it is recorded in both debit & credit side of the double column cash book. When a contra entry posted in cash book there is a reference column, the letter “C” is written this denotes that the entry is a contra entry. This entry will not be posted to any ledger account.

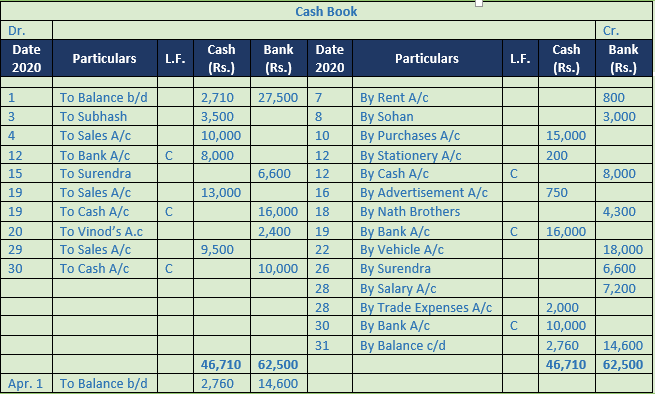

Question 7. Prepare Two Column Cash Book from the following transactions and balance the book on 31st Jan., 2020:-

Solution 7:

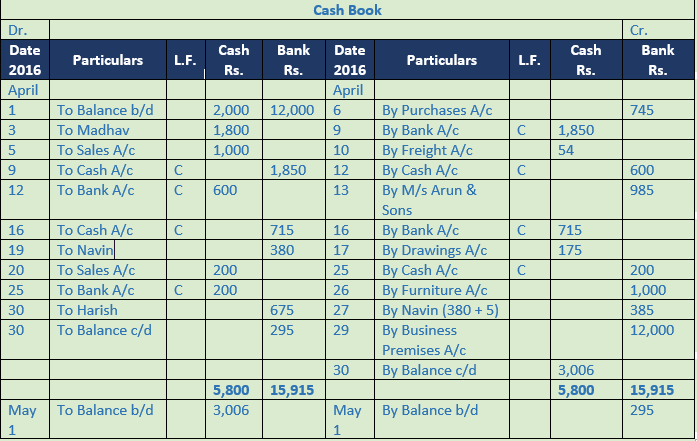

Question 8. (A) Enter the following particulars in the Cash Book with Cash and Bank columns:−

2016

April 1 Balance of cash in hand Rs. 2,000 and at Bank Rs. 12,000.

3 Received cash from Madhav Rs. 1,800.

5 Cash Sales Rs. 1,000

6 Purchases by cheque Rs. 745.

9 Paid into Bank Rs. 1,850.

10 Paid cash for freight Rs. 54.

12 Drew from Bank for office use Rs. 600.

13 Issued a cheque in favour of M/s Arun & Sons for Rs. 985.

16 Paid into Bank Rs. 715.

17 Drew Cash for his son’s birthday party Rs. 175.

19 Received a cheque from Navin for Rs. 380 and deposited it into bank on the same day.

20 Cash Sales Rs. 200.

25 Drew from Bank for office use Rs. 200.

26 Purchased furniture for Rs. 1,000 and payment made by cheque.

27 Navin’s cheque dishonoured, Bank charges Rs. 5.

29 Purchased business premises, payment made by cheque Rs. 12,000.

30 Received cheque for Rs. 675 from Harish.

Solution 8: (A)

Question 8. (B) Enter the following transactions in the Cash Book with Cash and Bank Columns:−

Solution 8:

Point of Knowledge:-

When a cheque is received and deposited into the bank on the same day the amount of the cheque is entered in the bank column on debit side.

When a cheque is received and does not represent on the same day, the amount of the cheque is entered in the cash column.

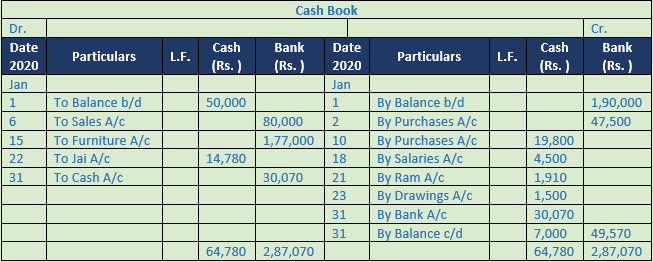

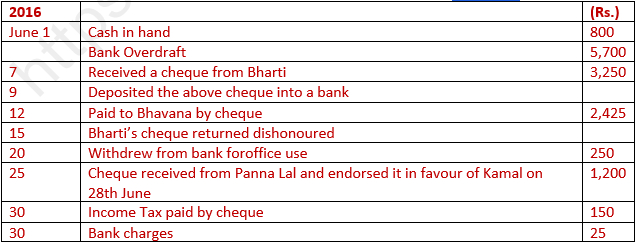

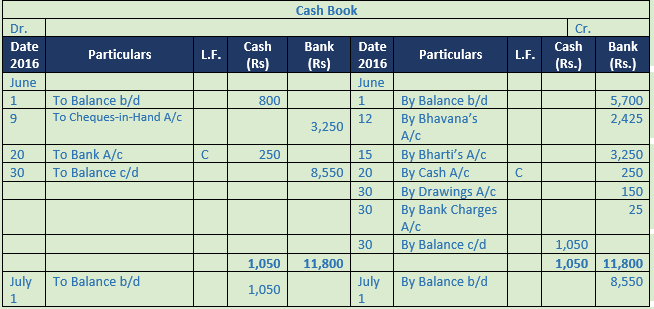

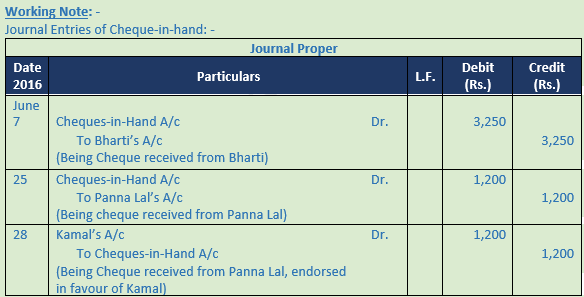

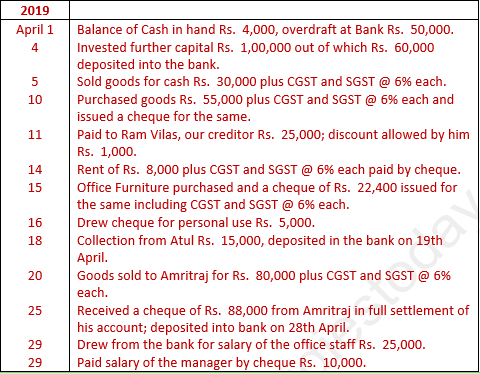

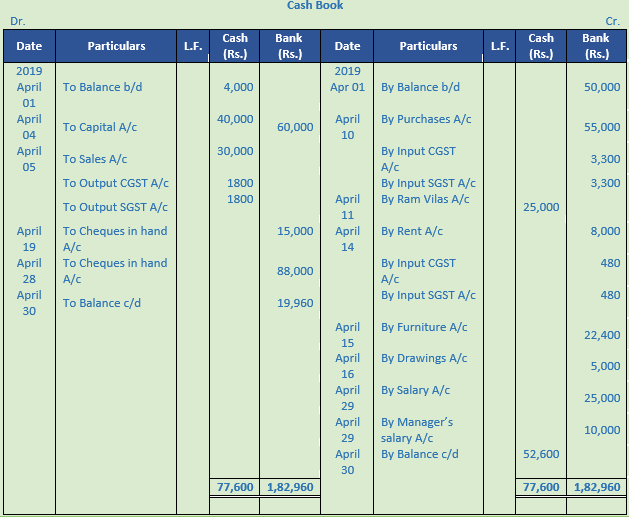

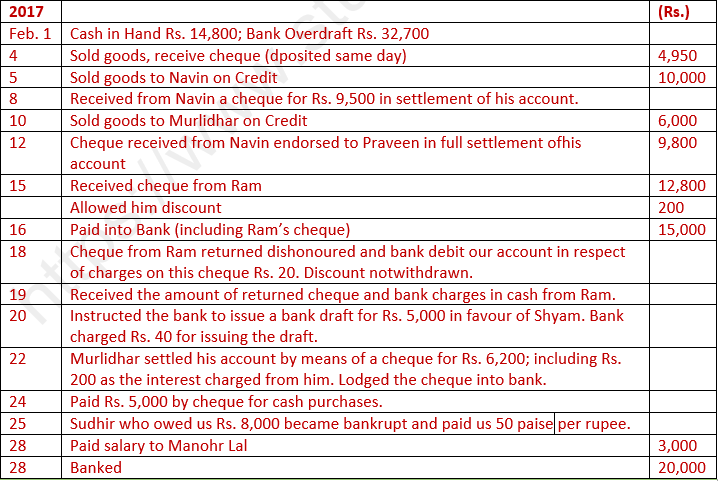

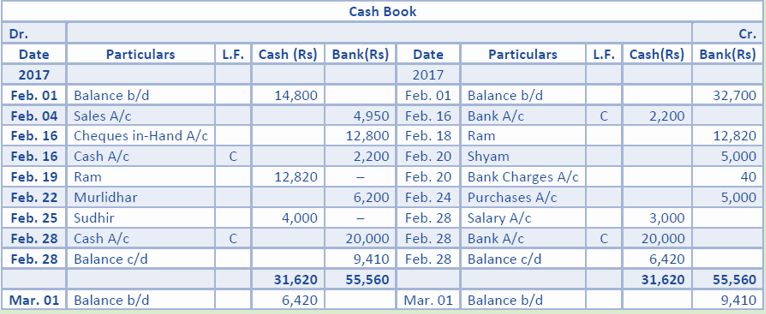

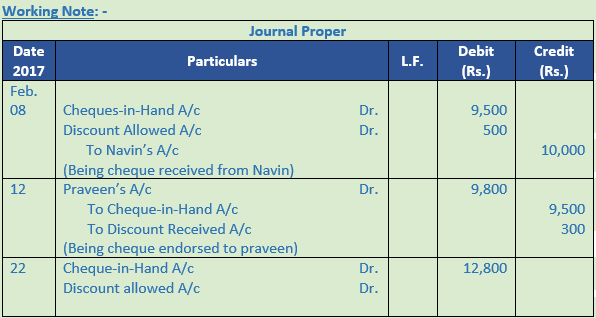

Question 9. Enter the following transactions in the Cash Book with Cash and Bank Columns ∶−

Solution 9:

Working Note:-

1. On 20th April, Entry for Credit sales of Rs. 80,000 plus CGST and SGST @ 6% each will he recorded in journal.

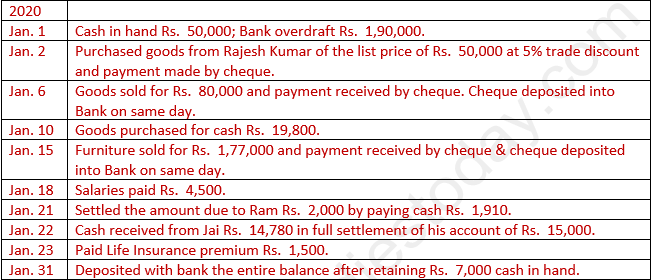

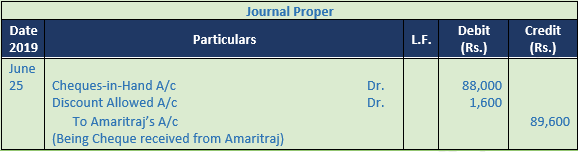

Question 10.

(A) Write the following transactions in a Two Column Cash Book and balance the Cash Book:−

Solution 10: (A)

Working Note:-

1. Cheque received from Prem Mohan on 9th and from Gopal on 20th will be recorded through Journal. These will be recorded in the Cash Book on the dates of their deposit into the Bank.

2. Since cheque from Prem Mohan has been dishonoured, the discount previously allowed to him would be withdrawn. Entry for discount will be recorded in Journal.

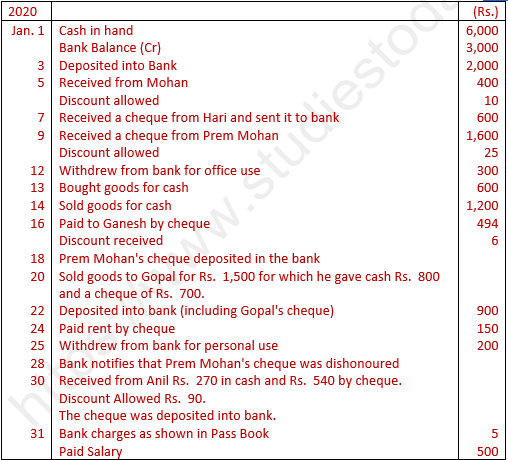

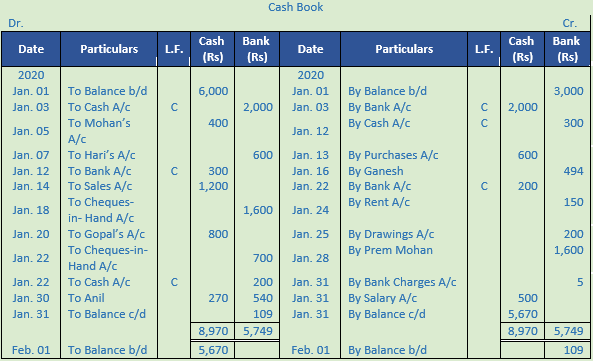

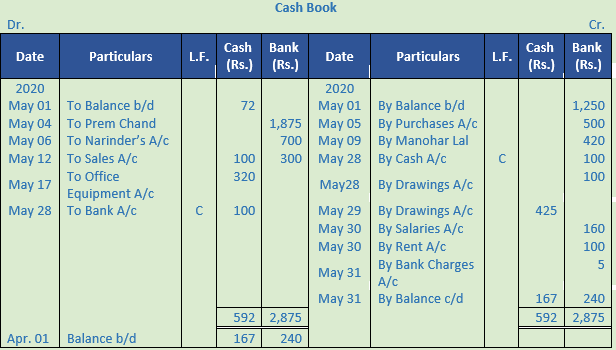

Question 10. (B) Prepare a Two Column Cash Book from the following transactions∶−

2020

May 1 Cash at office Rs. 72.

Bank overdraft Rs. 1,250.

4 Received from Prem Chand a cheque for Rs. 1,875 in full settlement of his account of Rs. 1,900. The cheque was banked on the same day.

5 Bought goods and paid by cheque Rs. 500.

6 Narinder settled his account of Rs. 700 by a cheque. This was banked on the same day.

9 Paid to Manohar Lal by a cheque for Rs. 420. Discount received Rs. 80.

12 Cash sales to date Rs. 400 of which Rs. 300 were banked.

17 Sold old typewriter for cash Rs. 320.

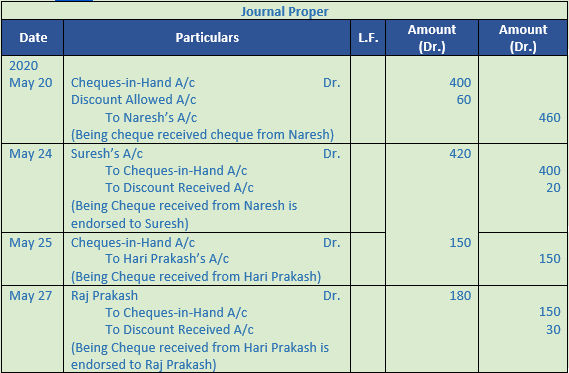

20 Received a cheque for Rs. 400 from Naresh in full settlement of his account of Rs. 460. The cheque is endorsed to Suresh on 24th May in full settlement of his account of Rs. 420.

25 Received a cheque from Hari Prakash for Rs. 150. The cheque is endorsed to Raj Prakash on 27th May; Discount received Rs. 30.

28 Withdrew from Bank for office use Rs. 100 and for personal use Rs. 100.

29 WIthdrew (from office) for payment of private bills Rs. 425.

30 Paid by cheque salaries Rs. 160 and rent Rs. 100.

31 Bank charges as per Pass Book Rs. 5.

Solution 10: (B)

Point of Knowledge:-

When a cheque is received and deposited into the bank on the same day the amount of the cheque is entered in the bank column on debit side.

When a cheque is received and does not represent on the same day, the amount of the cheque is entered in the cash column.

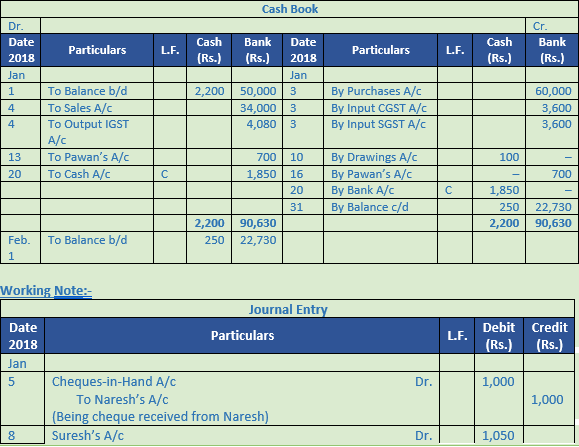

Question 11.

(A) Enter the following transactions in the Two Column Cash Book of Mr. Mohan:-

2018 (Rs.)

Jan. 1 Cash in Hand 2,200

Cash at Bank 50,000

3 Purchased goods for Rs. 75,000; Trade Discount 20%; CGST 6%, SGST 6%; Payment made by Cheque

4 Sold goods for Rs. 40,000; Trade Discount 15%; IGST 12%; Payment received by Cheque

5 Received a cheque from Naresh 1,000

8 Cheque received from Naresh endorsed to Suresh in full settlement of his account of Rs. 1,050

10 Paid Life Insurance premium of Mr. Mohan 100

13 Received a cheque from Pawan in full settlement of his account of Rs. 750. 700

16 Pawan’s cheque returned dishonoured by bank

20 Deposited into Bank, balance of Cash in excess of Rs. 250

Solution 11: (A)

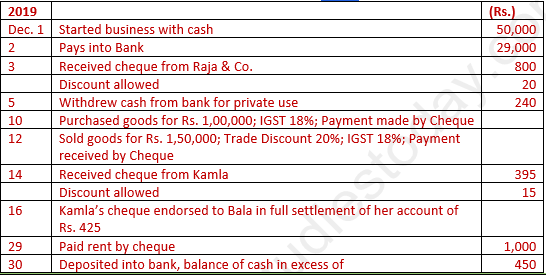

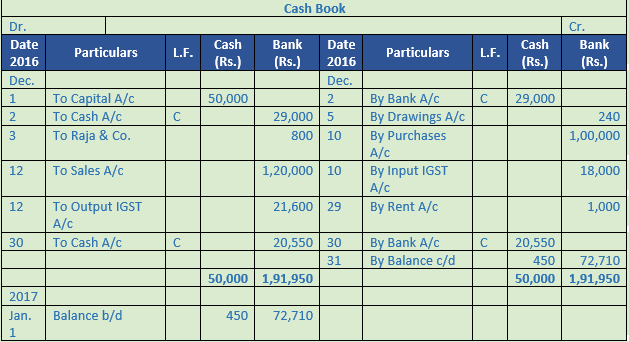

Question 11. (B) Enter the following transactions in a Two Column Cash Book:-

Solution 11: (B)

Calculation of Cash deposit into the Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 50,000 - 29,000 + 450

= 50,000 - 29,450

= 20,550

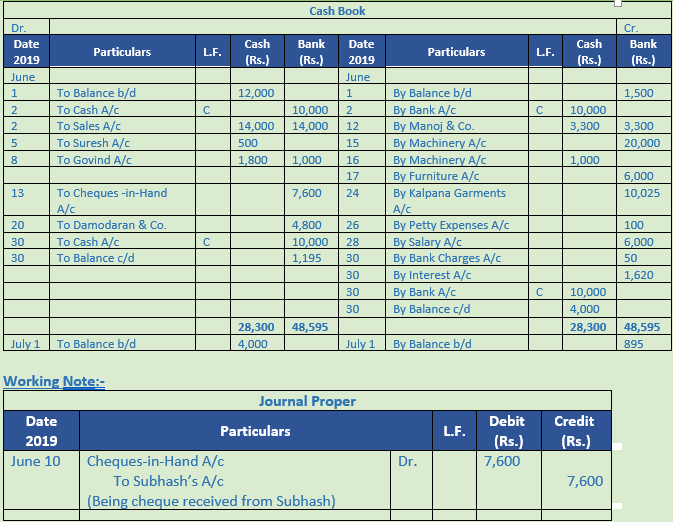

Question 12. Enter the following transactions in the Cash Book with Cash and Bank Columns∶−

2019

June 1 Balance of Cash in Hand Rs. 12,000; Overdraft at Bank Rs. 1,500.

2 Deposited into Bank Rs. 10,000.

Sold goods for Cash Rs. 28,000 and paid half the proceeds into Bank.

3 Purchased goods for Rs. 7,000 from Manoj & Co. on Credit.

5 Received a Money Order from Suresh Rs. 500.

8 Received Rs. 2,800 from Govind. Paid Rs. 1,000 into Bank.

10 Received a cheque for Rs. 7,600 from Subhash in full settlement of Rs. 8,000 dues from him.

12 Settled the account of Manoj & Co. by payment of Rs. 6,600

half Cash and half by cheque.

13 Cheque received from Subhash deposited into Bank.

15 Paid for purchase of Machinery by cheque Rs. 20,000.

16 Paid wages for the erection of above Machinery Rs. 1,000.

17 Cheque issued for Rs. 6,000 in favour of Sachdeva & Co. for purchase of furniture.

20 Purchased goods from Kalpana Garments for Rs. 10,500 on credit.

Received a Bank Draft for Rs. 4,800 from Damodaran & Co. in full settlement of Rs. 5,000 dues from them. Sent the draft to bank.

24 Bank issued a draft for Rs. 10,000 in favour of Kalpana Garments on our request. Bank charged Rs. 25 for issuing the draft. Account of Kalana Garments was fully settled.

26 Drew from bank for petty cash Rs. 100.

28 Paid salary by cheque Rs. 6,000.

30 Bank Charges Rs. 50 and Interest Rs. 1,620 charged by bank.

Deposited into bank the entire balance after retaining Rs. 4,000 at office

Solution 12:

Calculation of Cash Deposit into Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 28,300 - 14300 + 4,000

= 28,300 - 18,300

= 10,000

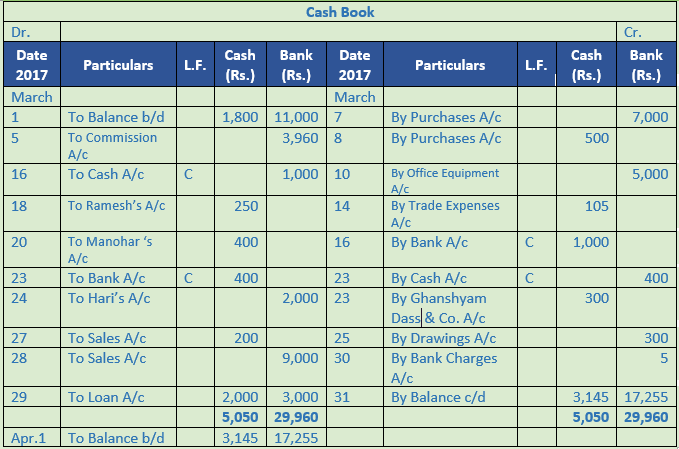

Question 13. (A) Prepare a Cash Book with Cash and Bank Columns from the following transactions:−

2017

March 1 Cash in hand Rs. 1,800 and at Bank Rs. 11,000.

5 Received a cheque for commission Rs. 3,960. Cheque was immediately deposited into bank.

7 Bought goods for cheque Rs. 7,000.

8 Bought goods for cash Rs. 500.

10 Purchased a Computer and payment made by cheque of Rs. 5,000.

14 Paid Trade Expenses Rs. 105.

16 Paid into Bank Rs. 1,000.

18 Ramesh who owed us Rs. 500 became bankrupt and paid us 50 paise in a Rs..

20 Received Rs. 400 from Manohar and allowed him discount Rs. 10.

23 Withdrew from Bank Rs. 400.

23 Paid Rs. 300 to Ghanshyam Dass & Co. They allowed us discount Rs. 10.

24 Received Rs. 2,000 from Hari Ram and deposited the same into Bank.

25 Withdrew from Bank for private expenses Rs. 300.

27 Sold goods for cash Rs. 200.

28 Received cheque for goods sold Rs. 9,000.

29 Received repayment of a loan of Rs. 5,000 and deposited Rs. 3,000 out of it into Bank.

30 Bank charges as per Book Rs. 5.

Solution 13: (A)

Working Note:-

Transaction of the 18th March: The amount of head debts will not be recorded in the Cash Book.

Transaction on 20th March: It will assume that the cheque has been deposited into the bank on the same day.

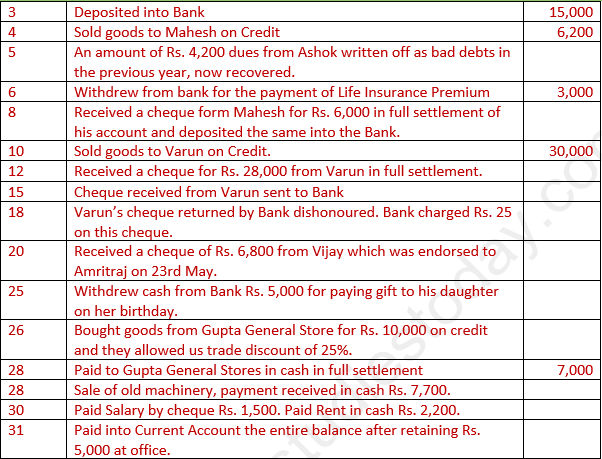

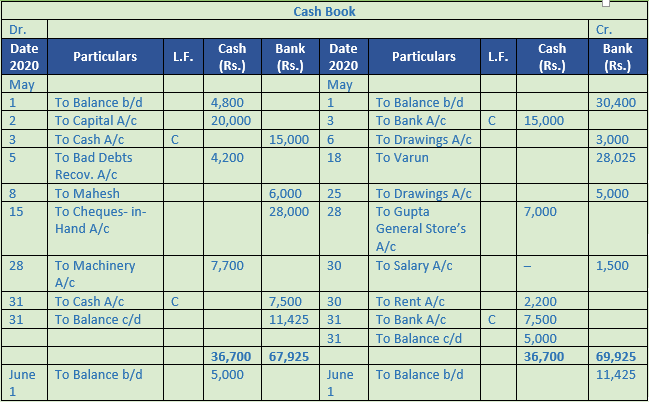

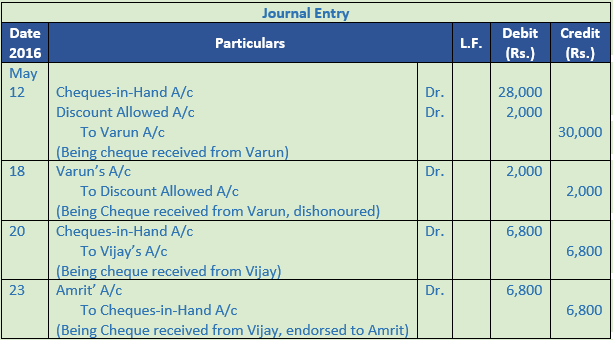

Question 13. (B) From the following transactions, prepare Cash Book with Cash and Bank Columns:−

Solution 13: (B)

Working Note:-

May 6th : Life Insurance Premium is treated as Drawings.

May 12th : Entry for receipt of cheque will be recorded in Journal Proper.

May 15th : To cheque in hand a/c Rs. 28,000 in bank column

May 18th : by Varun Rs. 28,025 in Bank Column, Entry for discount withdrawn Rs. 2,000 will be passed through Journal Proper.

Calculation of Cash Deposit into Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 36,700 - 24,200 + 5,000

= 36,700 - 29,200

= 7,500

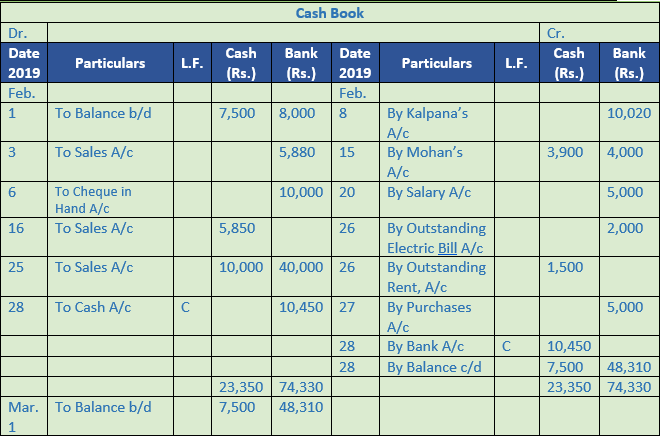

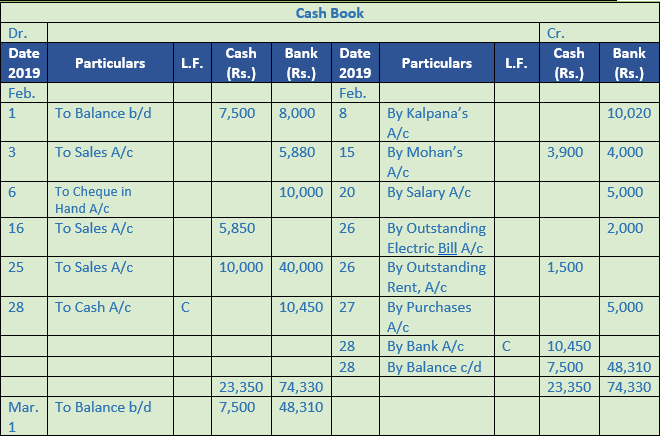

Question 14. Compile a Two Column Cash Book from the following transactions of Kavita Garments∶−

2019

Feb. 1 Cash in hand Rs. 7,500; Cash at bank Rs. 8,000.

3 Received a cheque of Rs. 5,880 for cash sales. Cheque was immediately deposited into bank.

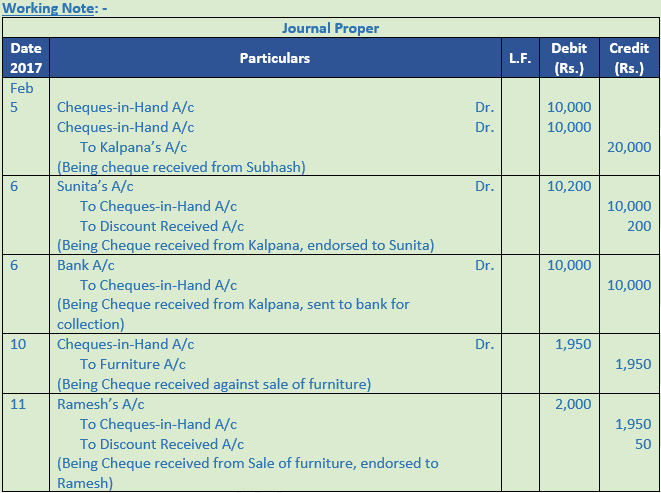

5 Received two cheques from Kalpna each of Rs. 10,000.

6 First cheque received from Kalpna is endorsed to Sunita in full settlement of Rs. 10,200.

Second cheque is sent to bank for collection.

8 Second cheque received from Kalpna is returned as dishonoured by the bank.

The bank has debited our account with Rs. 20 as bank charges on this cheque.

10 Received cheque from sale of old furniture Rs. 1,950. Next day, the cheque is endorsed to a creditor Ramesh in full settlement of Rs. 2,000 due to him.

12 Purchased goods from Mohan on Credit for Rs. 8,000.

15 Settled Mohan’s account by giving a cheque for Rs. 4,000 and Cash Rs. 3,900.

16 Goods sold to Pawan for Rs. 6,000. He paid the amount in cash immediately after deducting 5/2 % cash discount.

20 Paid salary by cheque Rs. 5,000.

25 Cash sale to date Rs. 50,000 of which Rs. 40,000 banked.

26 Paid electric bill of Rs. 2,000 for January by cheque. Paid Rent for January Rs. 1,500.

27 Cash purchases Rs. 5,000, issued a cheque.

28 Deposited into bank cash retaining Rs. 7,500.

Solution 14:

Calculation of Cash Deposit into Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 23,350 - 5,400 + 7,500

= 23,350 - 12,900

= 10,450

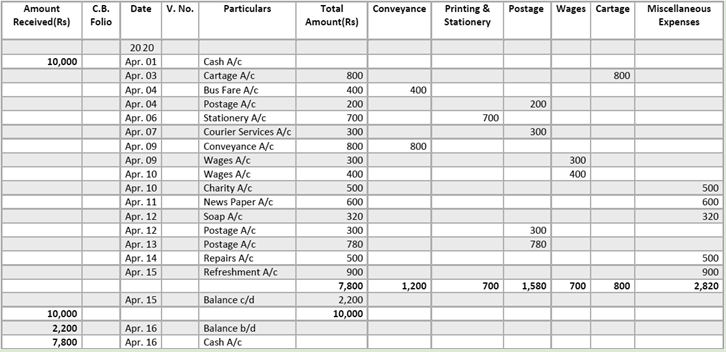

Question 15. Prepare a Petty Cash Book on the Imprest System from the following:

2020

April 1 Received Rs. 10,000 for Petty Cash.

3 Paid Cartage Rs. 800.

4 Paid Bus Fare Rs. 400; Speed Post Rs. 200.

6 Paid for Stationery Rs. 700.

7 Paid for Courier Services Rs. 300.

9 Paid for Taxi fare Rs. 800; Wages Rs. 300.

10 Paid for Wages Rs. 400; Charity Rs. 500

11 Paid for Newspaper bill Rs. 600.

12 Paid for soap Rs. 320; Speed post charges Rs. 300.

13 Paid for Postage Rs. 780.

14 Paid for Repairs of Chairs Rs. 500.

15 Paid for Refreshment to customers Rs. 900.

Solution 15:

Point of Knowledge:-

Petty Cash Book is the book which is used for the purpose of recording expenses involving petty amounts. Besides petty expenses, receipts from main cash are recorded. Petty Cash Book is prepared by Petty Cashier and acts as the Petty Cash Account. It is maintained as in a business besides large payments, number of small payments, such as for conveyance, stationary, cartage, etc., have to be made. If all these payments are recorded in the Cash Book, it will become unnecessarily large. Also, the main cashier will be overburdened with work.

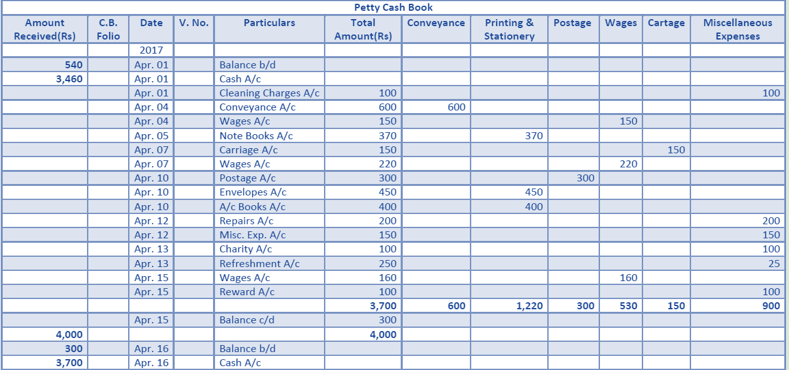

Question 16. Record the following transactions in a Petty Cash Book with suitable columns. The book is kept on imprest system, amount of imprest being Rs. 4,000.

2020

April 1 Petty cash in hand Rs. 540, Received cash to make-up the imprest.

Paid for office cleaning Rs. 100.

April 4 Paid railway fare Rs. 320, bus fare Rs. 280, wages Rs. 150.

April 5 Bought shorthand notebooks for office Rs. 370.

April 7 Paid carriage on parcels Rs. 150, paid for wages Rs. 220.

April 10 Bought stamps for Rs. 300, envelopes for Rs. 450 and an accounts register for Rs. 400.

April 12 Paid for repairs Rs. 200, gave tips to office peon Rs. 150.

April 13 Gave charity Rs. 100, served tea to customers Rs. 250.

April 15 Paid for wages Rs. 160, rewards to servant Rs. 100.

Solution 16:

Working Note:-

The imprest system of Petty Cash is explained below. Under this system, an estimate is made of amount required for petty expenses for a certain period (say for a week, a fortnight or a month). The amount so ascertained is given to the petty cashier in the beginning of a period and is reimbursed the amount paid by him during the period. Thus, he will again have the fixed amount in the beginning of the new period. This amount is called imprest money.

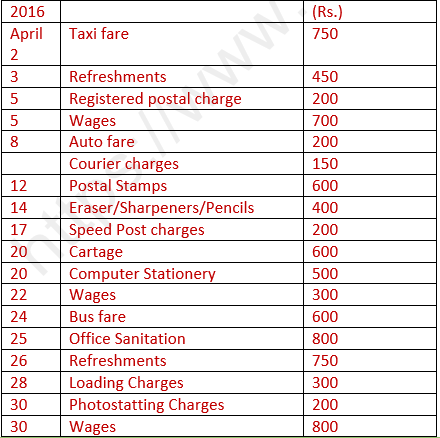

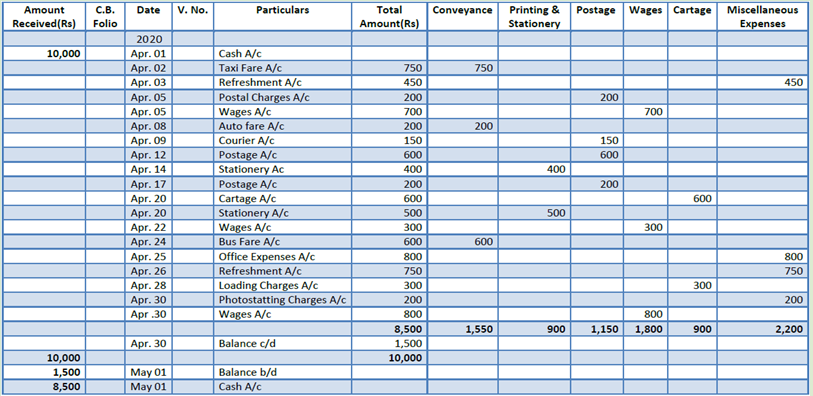

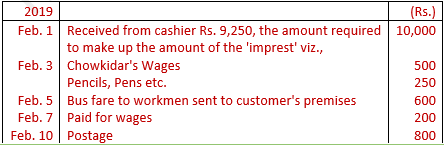

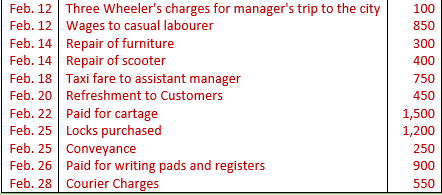

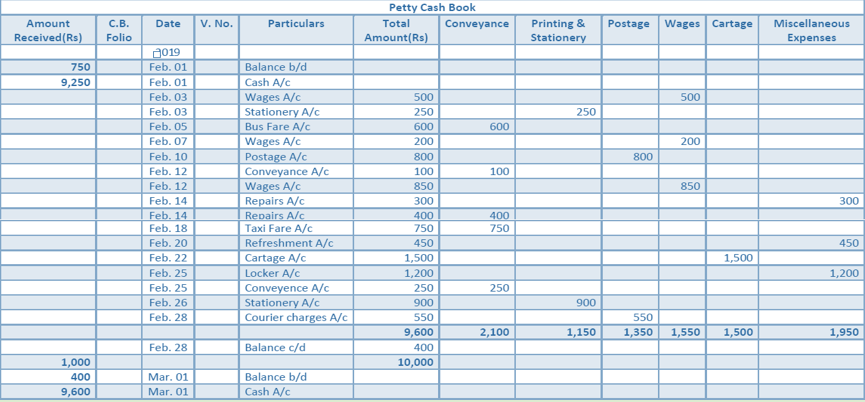

Question 17. Mr. Yadav, the petty cashier of M/s Triputi Traders received Rs.10,000 on April 1, 2016 from the Head Cashier. Following were the petty expenses :−

Solution 17:

Point of Knowledge:-

Petty Cash Book is the book which is used for the purpose of recording expenses involving petty amounts. Besides petty expenses, receipts from main cash are recorded. Petty Cash Book is prepared by Petty Cashier and acts as the Petty Cash Account. It is maintained as in a business besides large payments, number of small payments, such as for conveyance, stationary, cartage, etc., have to be made. If all these payments are recorded in the Cash Book, it will become unnecessarily large. Also, the main cashier will be overburdened with work.

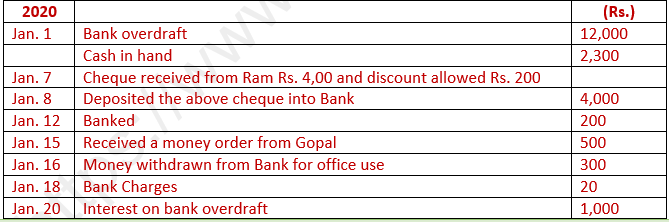

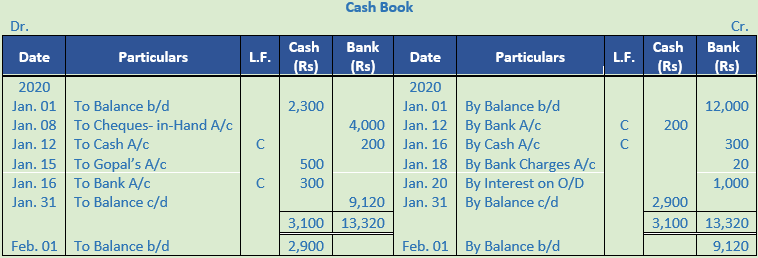

Question 18. Record the following transactions in a cash book with cash and bank columns:

Solution 18:

Working Note:-

1. For Jan.7 there is no entry in cash book for this transaction.

Question 19. Enter the following transactions in two Column cash book and find out the cash and bank balance∶

Solution 19:

Working Note:-

1. Cheque received on Jun.4 has been deposited in bank on Jan. 7. Hence it will not be recorded in cash book on Jan. 4.

2. On Jan. 7 : To Cheques in Hand A/c Rs. 200

On Jan. 7 : Contra entry will pass for Rs. 30

Question 20. Enter the following transactions in a Cash Book with Cash and Bank Columns:-

Solution 20:

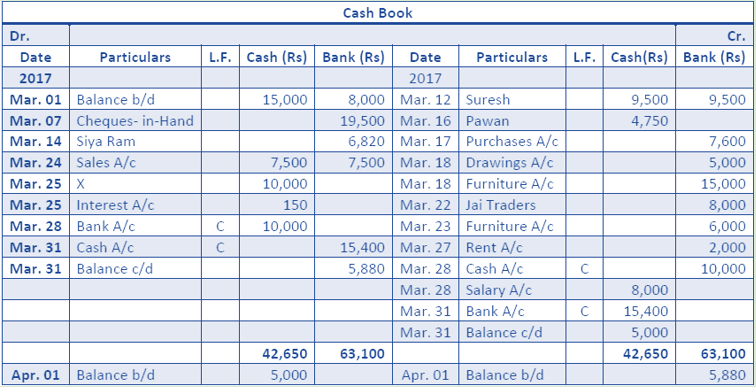

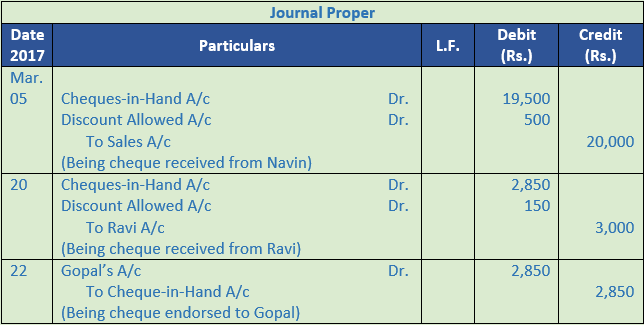

Question 21. Enter the following transactions in a Cash Book with Cash and Bank Columns∶-

2017

March 1 Cash in Hand Rs. 15,000; Bank Rs. 8,000

2 Sold goods to X on credit for Rs. 10,000.

5 Sold goods for Rs. 20,000; received cheque from them, discount allowed 212 %

Cheque was deposited into bank on 7th March.

10 Purchased goods from Suresh on the terms of 5% Cash discount if the payment is made within 3 days Rs. 20,000.

12 Payment made to Suresh; half in Cash and half by cheque.

14 Received a Bank Draft for Rs. 6,820 from Siya Ram in full settlement of Rs. 7,000 due from him. Sent the draft to th Bank.

16 Settled Pawan’s account of Rs. 5,000 at a discount of 5%.

17 Goods worth Rs. 8,000 were purchased from Sunil on 5th March. Its payment was made today by cheque after deducting 5% cash discount.

18 Withdrawn from Bank Rs. 20,000 and Furniture was purchased for Rs. 15,000; the balanc taken by the proprietor.

20 Received a cheque from Ravi for Rs. 2,850 in settlement after deducting 5%.

Endorsed the cheque to Gopal on 22nd March.

22 Placed an order with ‘Jai Traders’ for goods of the value of Rs. 10,000 and sent a cheque of Rs. 8,000 wih the order.

23 Purchased furniture by cheque of Rs. 6,000.

24 Cash sales Rs. 15,000; half of which deposited into bank.

25 X settled his account by payment of Rs. 10,150; Rs. 150 being the interest charged.

27 Paid rent to Landlord ‘Rakesh’ by cheque Rs. 2,000.

28 Cashed a cheque for Rs. 10,000 and paid salaries in cash Rs. 8,000.

31 Deposited into bank balance of cash in excess of Rs. 5,000.

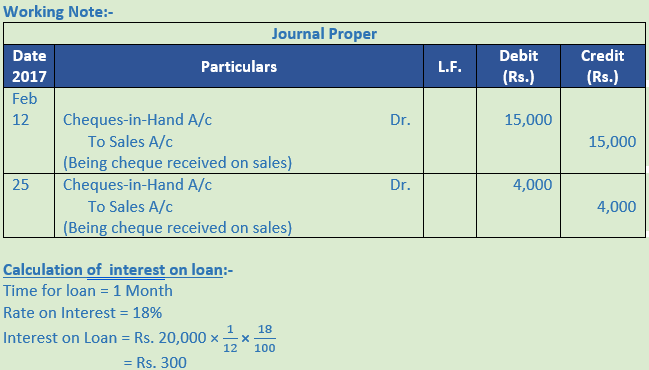

Solution 21:

Working Note:-

Calculation of Cash Deposit into Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 42,650 - 22,250 + 5,000

= 42,650 - 27,250

= 15,400

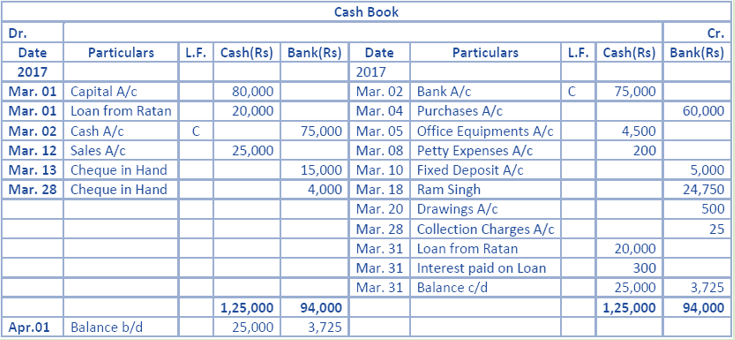

Question 22. Prepare a Cash Book with Cash and Bank Columns from the following particulars∶−

Solution 22:

Calculation of Cash Deposit into Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 42,650 - 22,250 + 5,000

= 42,650 - 27,250

= 15,400

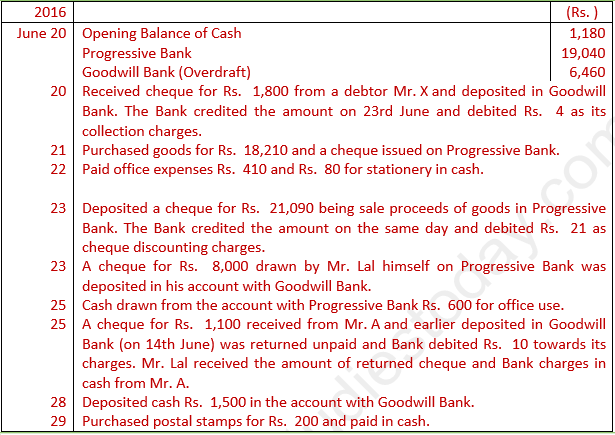

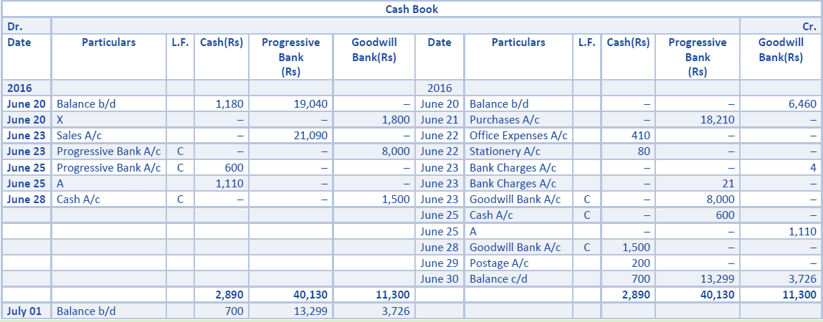

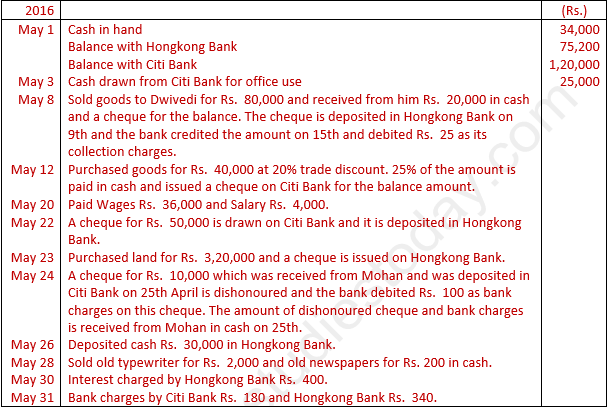

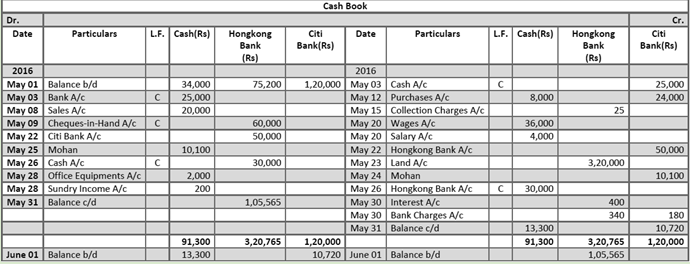

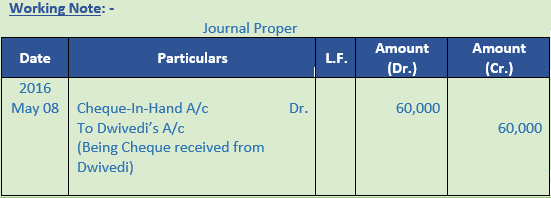

Question 23. Mr. Lal operates two bank accounts both of which are maintained in the columnar cash book itself. You are required to prepare a proforma of the cash book, record the following transactions therein and draw the closing balances as on 30th June, 2016:

Solution 23:

Point of Knowledge:-

When a cheque is received and deposited into the bank on the same day the amount of the cheque is entered in the bank column on debit side.

When a cheque is received and does not represent on the same day, the amount of the cheque is entered in the cash column.

Question 24. Mr. Chaturvedi maintains two bank accounts. Prepare his columnar cash book from the following particulars:

Solution 24:

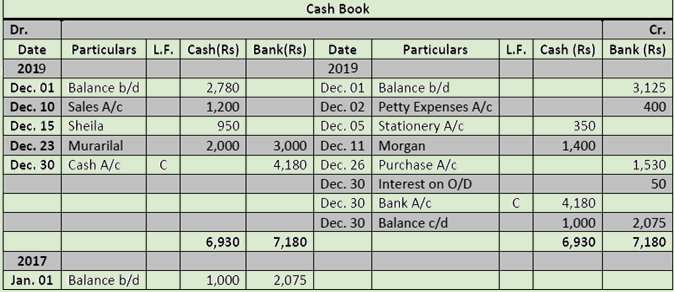

Question 25. Prepare a Cash Book with Cash and Bank columns from the following information for the month of December 2011 in the Books of O'Neil:

2019

Dec. 1 Cash in Hand Rs. 2,780; Bank Overdraft Rs. 3,125.

2 Cheque worth Rs. 400 issued to the petty cashier.

5 Rs. 350 was paid to Hari & Sons for the supply of stationery on this day.

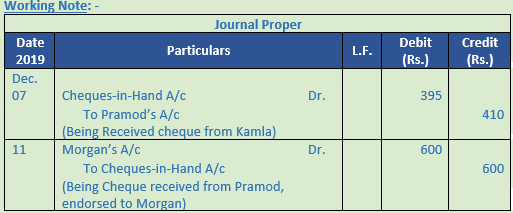

7 Received a cheque worth Rs. 600 from Pramod against sale of goods.

10 Received Rs. 1,200 for sale of goods.

11 The cheque which was received from Pramod on 7th December was endorsed as favour of Morgan together with Rs. 1,400 in cash.

15 Received Rs. 950 from Sheila.

23 Murarilal paid Rs. 2,000 in cash and Rs. 3,000 in cheque after receiving a discount of Rs. 200 for goods sold to him in November. The cheque was immediately deposited into the Bank.

26 Bought goods worth Rs. 1,700 from Rustom and paid by cheque after receiving a discount of Rs. 170.

30 Interest on overdraft Rs. 50 was charged by the Bank.

30 Cash in excess of Rs. 1,000 was deposited into the Bank.

Solution 25:

Calculation of Cash deposit into the Bank:-

Cash deposit into bank = Balance of cash column of Debit side - Total of Cash Column of Credit side + Cash Balance

= 50,000 - 29,000 + 450

= 50,000 - 29,450

= 20,550

Question 26. From the following particulars, prepare a Cash Book with Cash and Bank Columns:

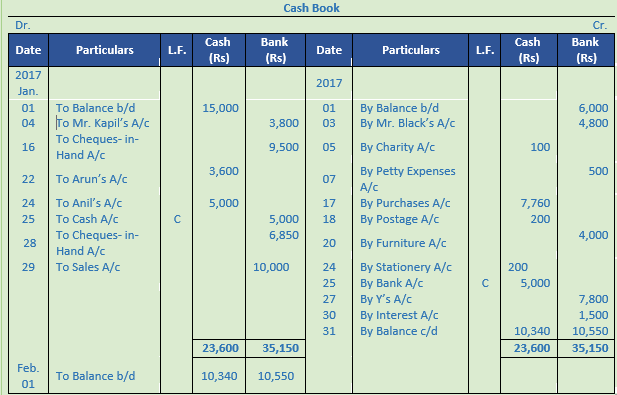

2017

Jan. 1 Balance of Cash in Hand Rs. 15,000 and Bank Overdraft Rs. 6,000

3 Issued a cheque of Rs. 4,800 to Mr. Black and earned a discount of Rs. 200.

4 Direct deposit by Mr. Kapil in our bank account Rs.3,800. Discount allowed Rs. 200.

5 Given as charity Rs. 100.

7 Issued a cheque of Rs. 500 to the petty cashier.

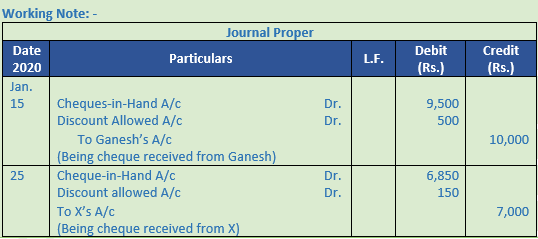

15 Goods worth Rs. 10,000 were sold to Ganesh on 10th January. Its payment was received today by cheque after deducting 5% cash discount.

16 Deposited the above cheque into Bank.

17 Goods purchased from Raghu for Rs. 8,000. Payment is made after deducting 3% cash discount.

18 Bought postage stamps Rs. 200.

20 Paid Rs. 4,000 by cheque for furniture purchased.

22 Arun who owed us Rs. 6,000 became bankrupt and paid 60 paise per Rs..

24 Collected from Anil Rs. 5,000 in cash and deposited into bank the next day.

24 Cash purchases of stationery Rs. 200.

25 X settled his account of Rs. 7,000 by cheque of Rs. 6,850.

Cheque was deposited into the bank on 28th January.

27 Settled Y's account of Rs. 8,000 by cheque after deducting therefrom 21212% cash discount.

29 Cash sales for Rs. 10,000, received cheque.

30 Interest charged by bank Rs. 1,500.

Solution 26:

Question 27. Record the following transactions in a Petty Cash Book drawn with suitable columns and then balance the same:

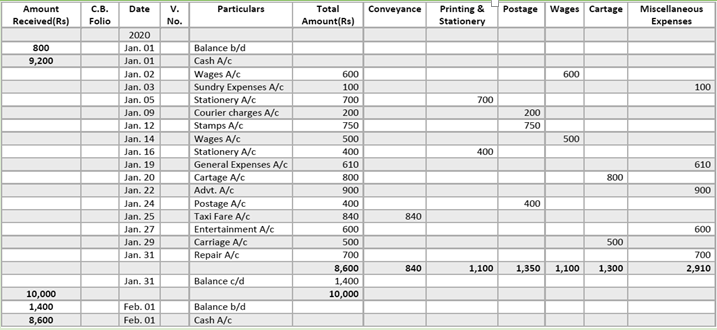

2017 (Rs.)

Jan. 1 Petty cashier is given a monthly imprest amount of Rs. 10,000. He spent last month Rs. 9,200 and got the balance from the head cashier today.

Jan. 2 Paid for Wages 600

Jan. 3 Paid for sundry expenses 100

Jan. 5 Paid for stationery 700

Jan. 9 Paid for courier charges 200

Jan. 12 Stamps purchased 750

Jan. 14 Paid wages to casual labour 500

Jan. 16 Stationery purchased 400

Jan. 19 Paid for general expenses 610

Jan. 20 Paid for cartage 800

Jan. 22 Paid for advertising 900

Jan. 24 Paid for postage 400

Jan. 25 Paid for Taxi Fare 840

Jan. 27 Paid for entertainment 600

Jan. 29 Paid for carriage 500

Jan. 31 Paid for petty repairs 700

Solution 27:

Working Note:-

The imprest system of Petty Cash is explained below. Under this system, an estimate is made of amount required for petty expenses for a certain period (say for a week, a fortnight or a month). The amount so ascertained is given to the petty cashier in the beginning of a period and is reimbursed the amount paid by him during the period. Thus, he will again have the fixed amount in the beginning of the new period. This amount is called imprest money. This system of paying advance in the beginning and reimbursing the amount spent from time to time is called imprest system.

Question 28. Enter the following transactions in the petty cash book with appropriate analysis columns:

Solution 28:

Working Note:-

The expiration of the method of posting a Petty Cash Book is explained below as: Petty cash given to the Petty Cashier for small payments is recorded on the credit side of the Cash Book as 'By Petty Cash Account' and is posted to the debit side of the Petty Cash Account in the Ledger. All payments are recorded in the particulars column as 'By Particular Petty Expenses Account' and the amount is posted in the total column along with individual Petty Expenses column.

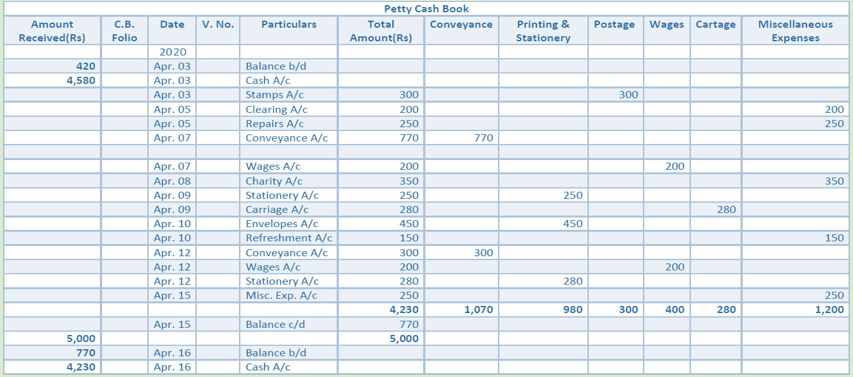

Question 29. Enter the following transactions in a petty cash book in analytical form. The book is kept on imprest system, amount of imprest being Rs. 5,000.

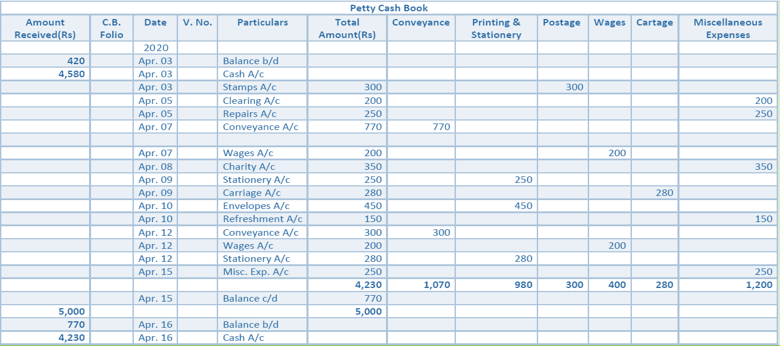

2020

April 3 Petty Cash in hand Rs. 420. Received cash to make-up the imprest.

Bought stamps for Rs. 300.

April 5 Paid for office cleaning Rs. 200 and repairs to furniture Rs. 250.

April 7 Paid bus fare Rs. 440, railway fare Rs. 330, wages Rs. 200.

April 8 Paid for charity Rs. 350

April 9 Bought shorthand note book for office Rs. 250, Carriage on parcels Rs. 280.

April 10 Bought envelopes Rs. 450, served refreshment to customers Rs. 150.

April 12 Paid for conveyance Rs. 300. Wages Rs. 200. Stapler pins Rs. 280.

April 15 Gave tips to office peon Rs. 250.

Solution 29:

Working Note:-

Petty Cash Book is the book which is used for the purpose of recording expenses involving petty amounts. Besides petty expenses, receipts from main cash are recorded. Petty Cash Book is prepared by Petty Cashier and acts as the Petty Cash Account. It is maintained as in a business besides large payments, number of small payments, such as for conveyance, stationary, cartage, etc., have to be made. If all these payments are recorded in the Cash Book, it will become unnecessarily large. Also, the main cashier will be overburdened with work