Read DK Goel Class 11 Accountancy Solutions for Chapter 15 Bank Reconciliation Statement below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 15 Bank Reconciliation Statement should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 15 Bank Reconciliation Statement DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 15 Bank Reconciliation Statement in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 15 Bank Reconciliation Statement Class 11 Accountancy

Long Answer Question

Question 1. What is a Bank Reconciliation Statement? Explain any four points regarding need and importance of preparing a Bank Reconciliation Statement.

Solution 1: Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Need and Importance of Bank Reconciliation Statement:-

(1) A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

(2) By Preparing a bank reconciliation statement, the customer becomes sure of the correctness of the bank balance shown by the cash book. It helps him in making further transactions with the bank.

(3) A reconciliation statement facilitates the preparation of a revised cash book.

(4) Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

(5) A reconciliation statement helps in revealing the unnecessary delay in the collection of cheque by the bank.

(6) It also help in keeping a track of cheque which have been sent to the bank for collection.

Short Answer Question

Question 1. What is the purpose of preparing Bank Reconciliation Statement?

Solution 1:

Bank Reconciliation Statement is prepared for the following reasons:

- It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

- Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

- Regular reconciliation discourages embezzlements. Reconciliation helps the management to verify the accuracy of entries recorded in the Cash Book.

- It shows actual bank balance.

Question 2. Give four causes of difference in the Cash Book balance (bank column) and Pass book balance.

Solution 2:

(i) Cheques drawn but not cleared.

(ii) Interest on bank overdraft.

(iii) Cheques paid into the bank but not collected.

(iv) Interest on investment collected by the bank.

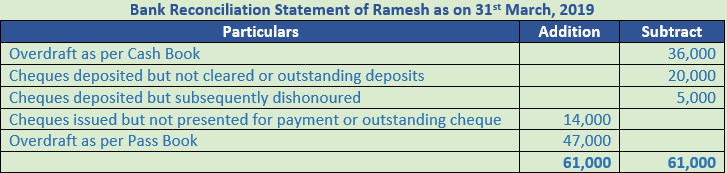

Question 3. Prepare a bank reconciliation statement, taking imaginary figures, starting from the credit balance as per Cash Book.

Solution 3:

Question 4. State any six reasons when the cash book balance will be higher than the pass book balance.

Solution 4: Cheque issued but not yet presented for payment in the bank.

- Bank charges and commission charged by the bank.

- Direct deposit by customer into the bank.

- Direct payment made by the bank on behalf of customers.

- Transaction wrongly debited in cash book.

- Transaction wrongly credited in pass book.

Question 5. In which column (Plus or Minus) you will write the following while prepare Bank Reconciliation Statement from the cash bank overdraft balance?

(i) Cheques drawn but not cleared.

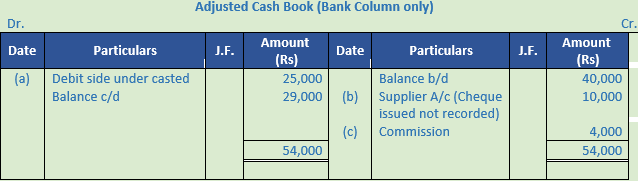

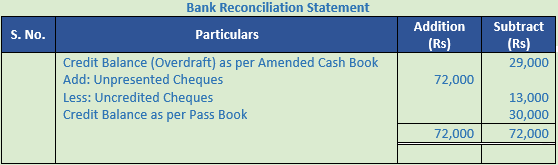

(ii) Interest on bank overdraft.

(iii) Cheques paid into the bank but not collected.

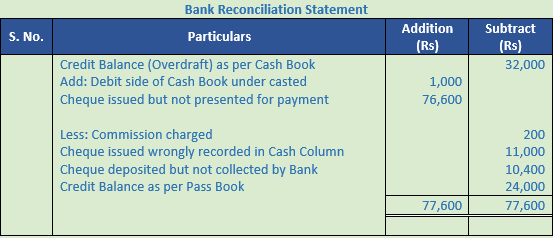

(iv) Interest on investment collected by the bank.

Solution 5:

(i) Plus

(ii) Minus

(iii) Minus

(iv) Plus

Question 6. In which Column (Plus or Minus) you will write the following while preparing Bank Reconciliation Statement from the Cash Book overdraft balance.

(i) Cheques deposited but dishonoured.

(ii) The receipt side of cash book overcast.

(iii) Interest on overdraft.

(iv) Direct amount deposited by the customer into bank.

Solution 6:

(i) Minus

(ii) Minus

(iii) Minus

(iv) Plus

Question 7. While preparing bank reconciliation statement from the debit balance of the pass book indicate whether the following items will be written in Plus or Minus column.

(i) Insurance premium paid by the bank.

(ii) Interest and dividend collected by the bank.

(iii) Payment of ‘Bills Payable’ by the bank on behalf of the customer.

(iv) Interest allowed by the bank.

(v) Cheque deposited into the bank but not yet cleared.

Solution 7:

Question 8.

While preparing Bank Reconciliation Statement from the balance of Cash Book indicate whether the following items will be written in Plus or Minus column.

(i) Cheques issued but not yet presented for payment.

(ii) Cheques paid into the bank not yet cleared.

(iii) Dividend collected by the bank on customer’s investments.

(iv) Payment of club fee by the bank according to the standing instructions.

(v) Direct payment into the bank by a customer.

(vi) Any wrong entry on the debit side of the pass book.

(vii) Dishonour of the cheques deposited into the bank.

Solution 8:

Bank Reconciliation Statement Practical Questions Class 11 BRS

Numerical Questions

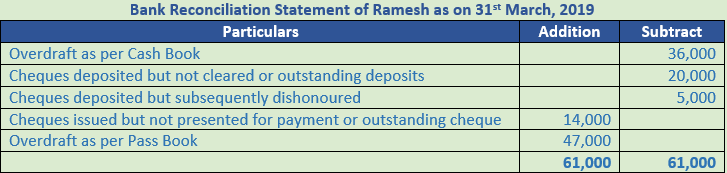

Question 1. Rim Zim Ltd. maintains a current account with the State Bank of India. On 31st March, 2017, the bank column of its cash book showed a debit balance of Rs. 1,54,300. However, the bank statement showed a different balance as on that date. The following were the reasons for the difference :

(i) Cheques deposited, but not yet credited by the bank 75,450

(ii) Cheques issued, but not yet presented for payment 80,760

(iii) Bank charges not yet recorded in the cash book 1,135

(iv) Cheques received by the bank directly from trade debtors 1,35,200

(v) Insurance premium paid by the bank as per standing instructions, but not yet recorded in the cash book 15,400

(vi) Dividend collected by the bank, but not yet recorded in the cash book 1,000

Find out the balance as per the bank statement as on 31st March, 2017.

Solution 1.

Point of Knowledge:-

- Regular reconciliation discourages embezzlements. Reconciliation helps the management to verify the accuracy of entries recorded in the Cash Book.

- Bank reconciliation statement shows actual bank balance.

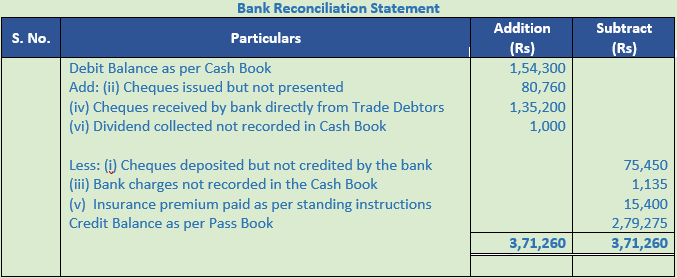

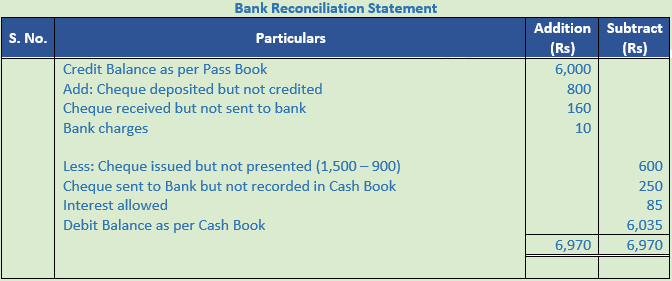

Question 2. The balance of cash at bank as shown by the Cash Book of Pan & Co. on 31st December, 2016, was Rs. 7,500. On checking the entries in the Cash Book with the Pass Book, it was ascertained that cheques of Rs. 500 and Rs. 700 respectively paid in on 30th December, were not credited until the 2nd January following and three cheques of Rs. 600, Rs. 800 and Rs. 1,200 issued on the 28th December were not presented until the 3rd of January. There was a credit of Rs. 125 in the Pass Book in respect of interest under date 31st December, which was not entered in the Cash Book. There were also Bank Charges debited in the Pass Book amounting in all to Rs. 10 which were not entered in the Cash Book.

Prepare a Bank Reconciliation Statement as at 31st December, 2016.

Solution 2:

Working Note:-

- Cheque issued but not presented for payment = Rs. 600 + Rs. 800 + Rs. 1,200 = Rs. 2,600

- Cheque deposited but not credited by the bank = Rs. 500 + Rs. 700 = Rs. 1,200

Point of Knowledge:-

- It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

- Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

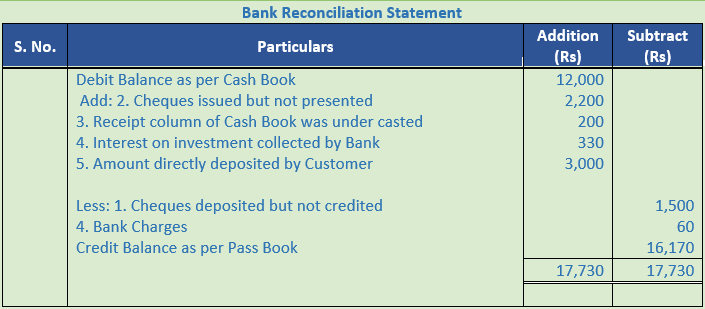

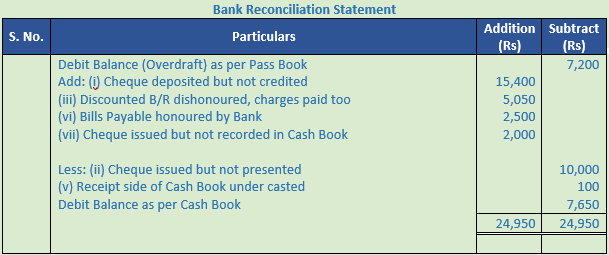

Question 3. On 30th June, 2020, the bank column of Mohan Kapoor's Cash Book showed a debit balance of Rs. 12,000. On checking the Cash Book with bank statement you find that:-

- Cheques paid into Bank Rs. 8,000, but out of these only cheques of Rs. 6,500 were cleared and credited by the Bankers upto 30th June.

- Cheques of Rs. 9,200 were issued but out of these only cheques of Rs. 7,000 were presented for payment upto 30th June.

- The receipt column of the Cash Book has been undercast by Rs. 200.

- The Pass Book shows a credit of Rs. 330 as interest on investments collected by bankers and debit of Rs. 60 for bank charges.

- On 29th June a Customer deposited Rs. 3,000 direct in the bank account but it was entered only in the Pass Book.

Prepare a Bank Reconciliation Statement.

Solution 3:

Working Note:-

1.) Cheques issued but not presented = 9,200 – 7,000 = 2,200

2.) Cheques deposited but not credited = 8,000 – 6,500 = 1,500

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

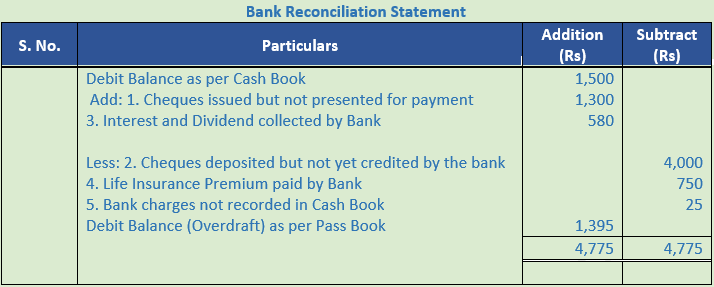

Question 4. On 30th June 2020, the bank balance as per Sanjay Yadav's Cash Book was Rs. 1,500. On comparing with the Pass Book the following information was received:-

- Cheques amounting to Rs. 7,290 were issued on 28th June, of which one cheque of Rs. 1,300 was presented in the bank for payment on 4th July.

- Cheques deposited into bank for Rs. 10,000, but of these cheques for Rs. 4,000 were cleared and credited in July.

- Interest and Dividend on investments Rs. 580 collected by bank and credited to his account but he did not have any information for this.

- Life Insurance Premium Rs. 750 paid by bank according to his standing orders.

- Bank Charges Rs. 25 not recorded in the Cash Book.

Prepare a Bank Reconciliation Statement.

Solution 4:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

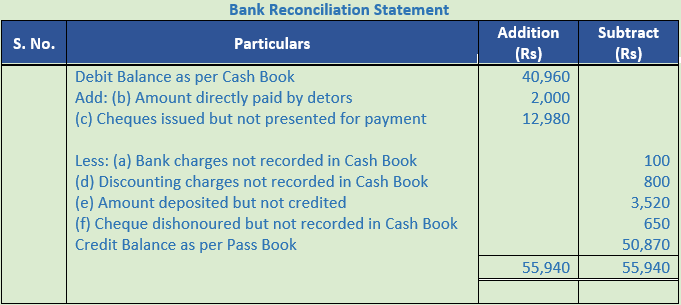

Question 5. On comparing the Cash Book with Pass Book of Naman it is found that on March 31, 2017, bank balance of Rs. 40,960 showed by the Cash Book differs from the bank balance with regard to the following:

(a) Bank charges Rs. 100 on March, 31 2017, are not entered in the Cash Book.

(b) On March 21, 2017, a debtor paid Rs. 2,000 into the company's bank in settlement of his account, but no entry was made in the Cash Book of the company in respect of this.

(c) Cheques totalling Rs. 12,980 were issued by the company and duly recorded in the Cash Book before March 31, 2017, but had not been presented at the bank for payment until after that date.

(d) A bill for Rs. 6,900 discounted with the bank is entered in the Cash Book without recording the discount charge of Rs. 800.

(e) Rs. 3,520 is entered in the Cash Book as paid into bank on March 31st 2017, but not credited by the bank until the following day.

(f) No entry has been made in the Cash Book to record the dishonour on March 15, 2017 of a cheque for Rs. 650 received from Bhanu.

Prepare a reconciliation Statement as on March 31, 2017.

Solution 5 :

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

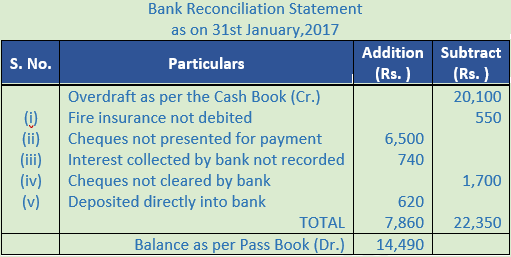

Question 6. Prepare Bank Reconciliation Statement as on 31st January, 2017, if Cash Book of Mr. Sanjay showed a credit balance of Rs. 20,100.

(i) The bank had paid fire insurance premium of Rs. 550 which does not appear in the Cash Book.

(ii) Cheques for Rs. 25,000 issued during January, but cheques for only Rs. 18,500 were presented for payment.

(iii) Interest collected by bank Rs. 740.

(iv) Cheques of Rs. 8,700 were deposited into bank, but cheques for Rs. 7,000 were cleared till 31st January, 2017.

(v) A customer deposited Rs. 620 directly into bank without informing Mr. Sanjay.

Solution 6 :

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

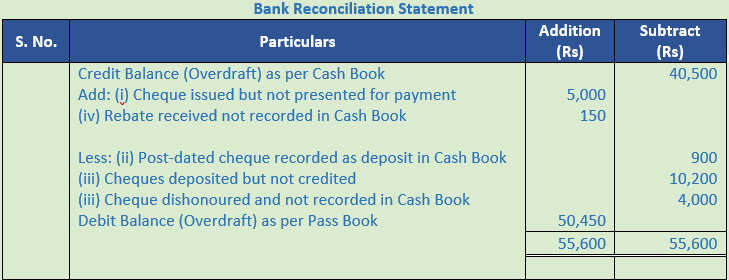

Question 7. Tiwari and Sons find that the bank balance shown by their Cash Book on December 31, 2016 is Rs. 40,500 (Credit) but the Pass Book shows a difference due to the following reasons:

(i) A cheque for Rs. 5,000 drawn in favour of Manohar has not yet been presented for payment.

(ii) A post-dated cheque for Rs. 900 has been debited in the bank column of the Cash Book but it could not have been presented in any case.

(iii) Cheques totalling Rs. 10,200 deposited with the bank have not yet been collected and an another cheque for Rs. 4,000 deposited in the account has been dishonoured.

(iv) A Bill Payable for Rs. 10,000 was retired by the Bank under a rebate of Rs. 150 but the full amount of the bill was credited in the bank column of the cash book.

Prepare a Bank Reconciliation Statement and find out the balance as per Pass Book.

Solution 7:

Point of knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

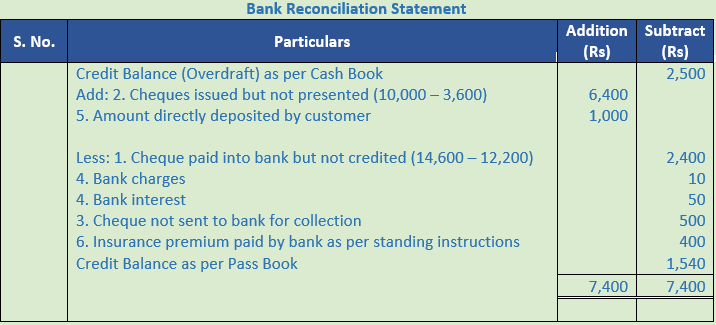

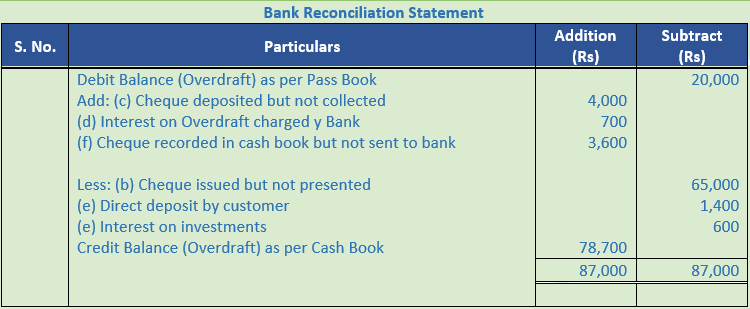

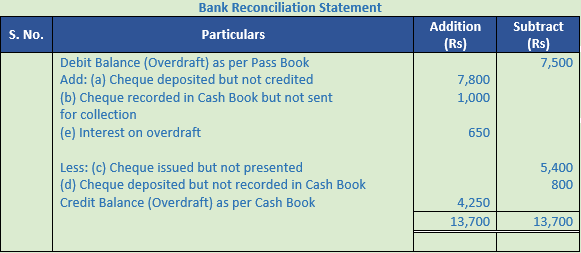

Question 8. On 30th June 2020, the Cash Book of a trader shows a bank overdraft of Rs. 2,500. Following informations are available:-

- Cheques amounting to Rs. 14,600 had been paid to the bank, but of these only Rs. 12,200 were credited in the Pass Book, up to 30th June, 2019.

- He had also issued cheques amounting to Rs. 10,000, out of which only Rs. 3,600 had been presented for payment.

- A cheque of Rs. 500 which he had debited to the bank account was not sent to bank for collection by mistake.

- There is a debit in the Pass Book of Rs. 10 for Bank Charges and Rs. 50 for interest.

- A customer directly paid into his bank Rs. 1,000, but it was not shown in the Cash Book.

- Bank has paid insurance premium of Rs. 400 according to his instructions, but this is not recorded in the Cash Book.

Prepare a Bank Reconciliation Statement.

Solution 8:

Working Note:-

Cheques issued but not presented = Rs. 10,000 – Rs. 3,600 = Rs. 6,400

Cheque paid into bank but not credited Rs. 14,600 – Rs. 12,200 = Rs. 2,400

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

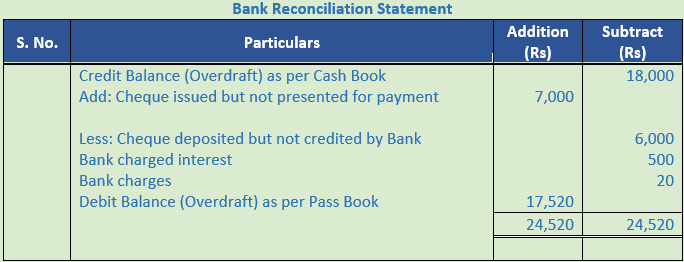

Question 9. On 31st December, 2019 the Cash Book of Basu showed an overdraft of Rs. 18,000 with the Bank of India. The balance did not agree with balance as shown by the Bank Pass Book and you find that Basu had paid into the Bank on 26th December four cheques for Rs. 10,000; Rs. 12,000; Rs. 6,000 and Rs. 8,000. Of these the cheque for Rs. 6,000 was credited by the bank in January, 2020. Basu had issued on 24th December three cheques for Rs. 15,000, Rs. 12,000, and Rs. 7,000. The first two cheques were presented to the bank for payment in December and the third in January, 2020.

You also find that on 31st December, 2019, the bank had debited Basu's Account for Rs. 500 for interest and Rs. 20 for charges but Basu has not recorded these amounts in his books.

You are required to prepare a Bank Reconciliation Statement as on 31st December, 2019 and ascertain the balance as per bank Pass Book.

Solution 9:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

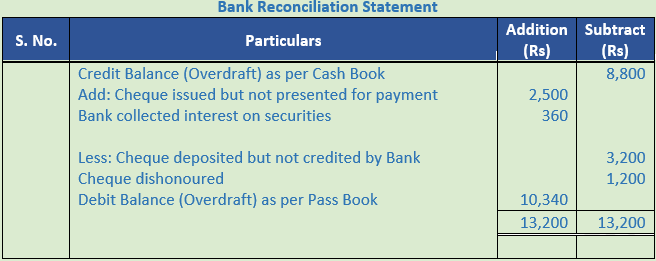

Question 10. On 31st December, 2019 my Cash Book showed a credit balance of Rs. 8,800. I had paid into Bank three cheques amounting to Rs. 6,000 on 24th December of which I found Rs. 3,200 have been credited in the Pass Book under date 5th January 2020. I had issued cheques amounting to Rs. 8,000 before 31st December of which I found Rs. 2,500 have been debited in the Pass Book after 1st January 2020. I find a debit of Rs. 50 in respect of bank charges in the Pass Book which I have adjusted in the Cash Book on 31st Dec. There is a credit of Rs. 360 for interest on securities in the Pass Book which remains to be adjusted. A cheque of Rs. 1,200 deposited into bank has been dishonoured.

Prepare Bank Reconciliation Statement as on 31st Dec. 2019.

Solution 10:

Point of knowledge:-

- It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

- Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

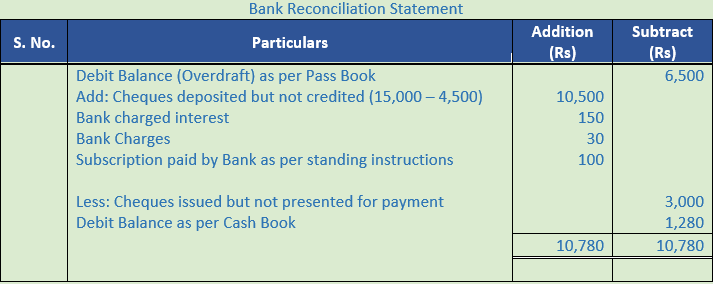

Question 11. My bank Pass Book showed an overdraft of Rs. 6,500 on 31st March, 2017. This does not agree with the Cash Book balance. From the following particulars ascertain the Cash Book balance:-

Cheques amounting to Rs. 15,000 were paid into bank in March, out of which, it appears, only cheques amounting to Rs. 4,500 were credited by bank. Cheques issued during March amounted in all to Rs. 11,000. Out of these cheques for Rs. 3,000 were unpaid on 31st March, 2017. The Pass Book stands debited with Rs. 150 for interest and with Rs. 30 for bank charges. The bank had paid the annual subscription of Rs. 100 to my club according to my instructions. The entries for interest, bank charges and subscription have not yet been made in Cash Book.

Solution 11:

Working Note:-

Cheques deposited but not credited = Rs. 15,000 – Rs. 4,500 = Rs. 10,500

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

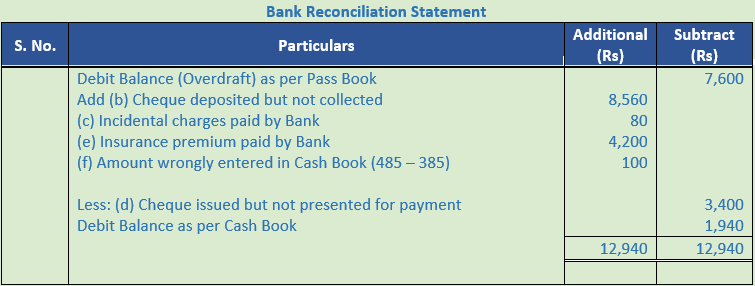

Question 12. Prepare the Bank Reconciliation Statement from the following particulars for the period ending 31st December, 2012.

(a) Overdraft as per Pass Book on 31-12-2012 Rs. 7,600.

(b) Cheques deposited but not collected by the bank Rs. 8,560.

(c) Incidental charges not recorded in Cash Book Rs. 80.

(d) Cheques were issued for Rs. 7,800 but only Rs. 4,400 were presented for payment.

(e) Insurance premium paid by bank not recorded in the Cash Book Rs. 4,200.

(f) On 31st December, 2012 cash was deposited in bank Rs. 385 but the cashier debited the bank column with Rs. 485 by mistake.

Solution 12:

Point of knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

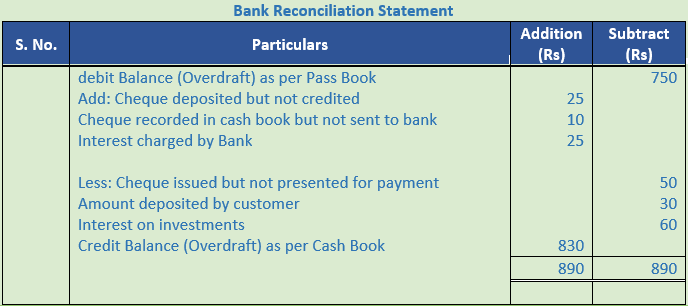

Question 13. Prepare a Bank Reconciliation Statement from the following particulars:-

On 31st December 2019, I had an overdraft of Rs. 750 as shown by my Pass Book. I had issued cheques amounting to Rs. 250 of which Rs. 200 worth only seem to have been presented for payment. Cheques amounting to Rs. 100 had been paid in by me on 30th December, but of these only Rs. 75 were credited in the Pass Book. I also find that a cheque for Rs. 10 which I had debited to bank account in my books has been omitted to be banked. There is a debit of Rs. 25 in my Pass Book for interest.

An entry of Rs. 30 of a payment by a customer direct into the bank appears in the Pass Book. My Pass Book also shows a credit of Rs. 60 to my account for interest on investments directly collected by my bankers.

Solution 13:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

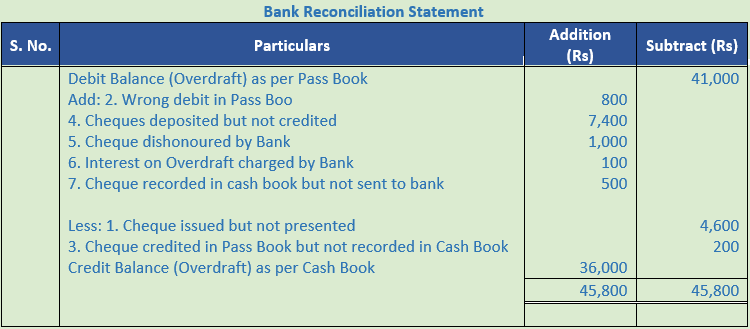

Question 14. On 31st January, 2017 the Pass Book of Shri M.L. Gupta shows a debit balance of Rs. 41,000. Prepare a bank reconciliation statement from the following particulars:-

- Cheques amounting to Rs. 15,600 were drawn on 27th January, 2017. Out of which cheques for Rs. 11,000 were encashed up to 31-1-2017.

- A wrong debit of Rs. 800 has been given by the bank in the Pass Book.

- A cheque for Rs. 200 was credited in the Pass Book but was not recorded in the Cash Book.

- Cheques amounting to Rs. 21,000 were deposited for collection. But out of these, cheques for Rs. 7,400 have been credited in the Pass Book on 5th February, 2017.

- A cheque for Rs. 1,000 was returned dishonoured by the bank and was debited in the Pass Book only.

- Interest on overdraft and bank charges amounting to Rs. 100 were not entered in the Cash Book.

- A cheque of Rs. 500 debited in the Cash Book omitted to be banked.

Solution 14:

Working Note:-

Cheque issued but not presented = Rs. 15,600 – Rs. 11,000 = Rs. 4,600

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

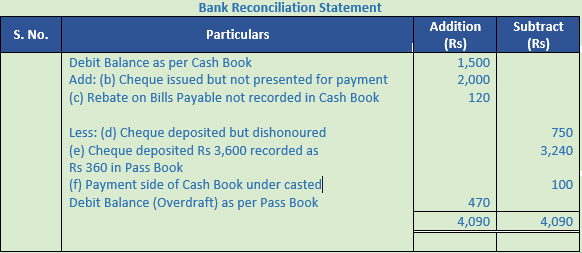

Question 15. Prepare a Bank Reconciliation Statement on 31 December, 2019 from the following particulars:-

(a) A's overdraft as per Pass Book Rs. 20,000 as at 31st Dec.

(b) On 30th December, cheques had been issued for Rs. 80,000, of which cheques worth Rs. 15,000 only had been encashed up to 31st December.

(c) Cheques amounting to Rs. 6,500 had been paid into the bank for collection but of these only Rs. 2,500 had been credited in the Pass Book.

(d) The bank has charged Rs. 700 as interest on overdraft and the intimation of which has been received on 2nd January 2020.

(e) The Bank Pass Book shows credit for Rs. 2,000 representing Rs. 1,400 paid by debtor of A direct into the bank and Rs. 600 collected direct by bank in respect of interest on A,s investment. A had no knowledge of these items.

(f) A cheque for Rs. 3,600 has been debited in bank column of Cash Book by A, but it was not sent to bank at all.

Solution 15:

Working Note:-

1. Cheque deposited but not collected = Rs. 6,500 – Rs. 2,500 = Rs. 4,000

2. Cheque issued but not presented = Rs. 80,000 – Rs. 15,000 = Rs. 65,000

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

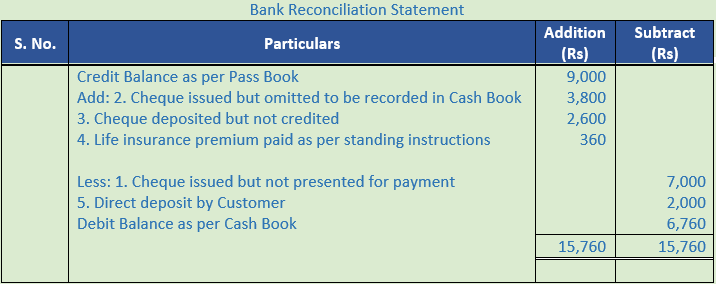

Question 16. On 31st March, 2020 the Pass Book shows a credit balance of Rs. 9,000. Prepare a Bank Reconciliation Statement from the following particulars:-

Rs.

1. Cheques issued but not yet presented for payment 7,000

2. Cheques issued but omitted to be recorded in the Cash Book 3,800

3. Cheques paid into bank but not yet collected by the bank 2,600

4. Premium on Life Policy paid by the bank on standing advice 360

5. Payments received from customers direct by the bank 2,000

Solution 16:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

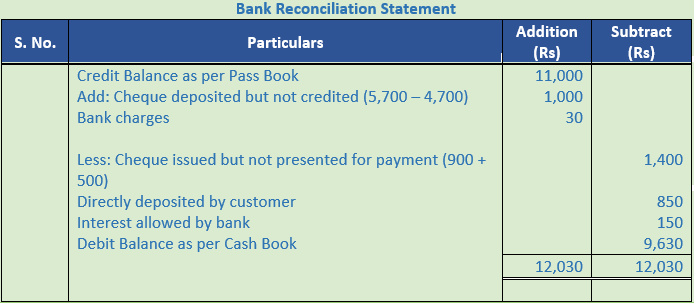

Question 17. From the following particulars, prepare a Bank Reconciliation Statement of Sh. Yadav on 31st December 2019:-

Balance as per Pass Book on 31st December, 2019 is Rs. 11,000. Cheques for Rs. 6,200 were issued during the month of December but of these cheques for Rs. 900 were presented in the month of January, 2020 and one cheque for Rs. 500 was not presented for payment. Cheque and cash amounting to Rs. 5,700 were deposited in bank during December but credit was given for Rs. 4,700 only. A customer had deposited Rs. 850 into the bank directly. The bank has credited the merchant for Rs. 150 as interest and has debited him for Rs. 30 as bank charges, for which there are no corresponding entries in Cash Book.

Solution 17:

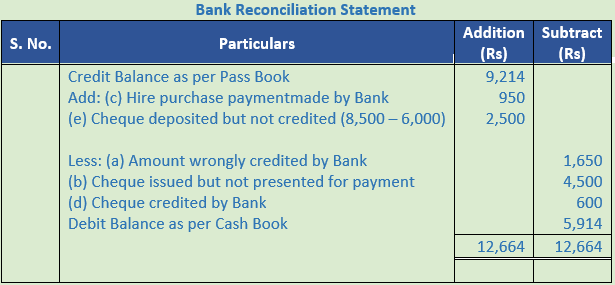

Question 18. Prepare Bank Reconciliation Statement from the following particulars on June 30, 2016:

Bank Statement showed a favourable balance of Rs. 9,214.

(a) On 29th June, the bank credited the sum of Rs. 1,650 in error.

(b) Certain cheques, valued at Rs. 4,500 issued before June 30, were not cleared.

(c) A hire purchase payment of Rs. 950, made by a standing order was not entered in the cash book.

(d) A cheque of Rs. 600 received, deposited and credited by bank, was accounted as a receipt in the cash column of the cash book.

(e) Other cheques for Rs. 8,500 were deposited in June but cheques for Rs. 6,000 only were cleared by the bankers.

Solution 18:

Working Note:-

Cheque deposited but not credited = Rs. 8,500 – Rs. 6,000 = Rs. 2,500

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

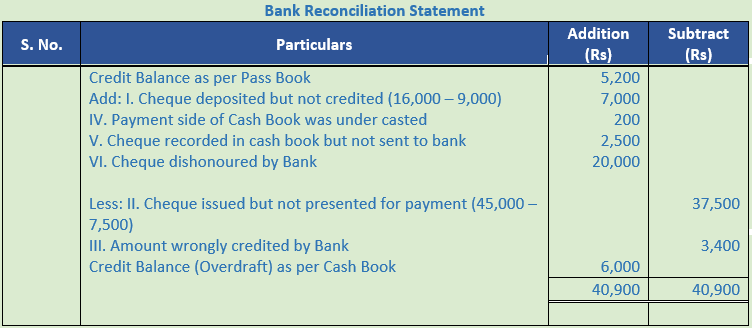

Question 19. On 30th June 2019 Pass Book showed a balance of Rs. 5,200. Prepare Bank Reconciliation Statement from the following particulars:-

1. Out of total cheques amounting to Rs. 16,000 deposited, cheques amounting to Rs. 9,000 were credited in June 2019, Cheques amounting to Rs. 3,000 were credited in July 2019, and the rest have not been collected so far.

2. Out of total cheques amounting to Rs. 45,000 drawn, cheques amounting to Rs. 7,500 were presented in June 2019, Cheques amounting to Rs. 18,000 were presented in July 2019, and the rest have not been presented so far.

3. Amount wrongly credited by bank Rs. 3,400.

4. Payment side of the Cash Book has been under cast by Rs. 200.

5. Cheques recorded in the Cash Book in June 2019 but sent to bank in July 2019 Rs. 2,500.

6. A cheque of Rs. 20,000 deposited in the bank has been dishonoured but no intimation was received till June 2019.

Solution 19:

Working Note:-

Cheque deposited but not credited Rs. 16,000 – Rs. 9,000 = Rs. 7,000

Cheque issued but not presented for payment = Rs.45,000 – Rs. 7,500 = Rs. 37,500

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

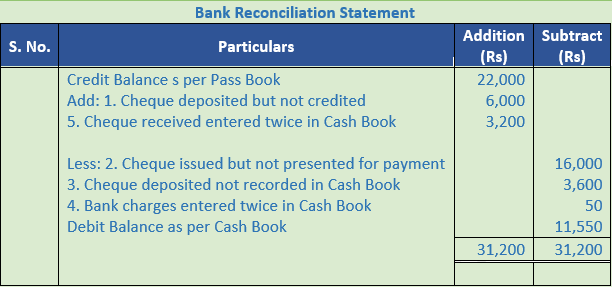

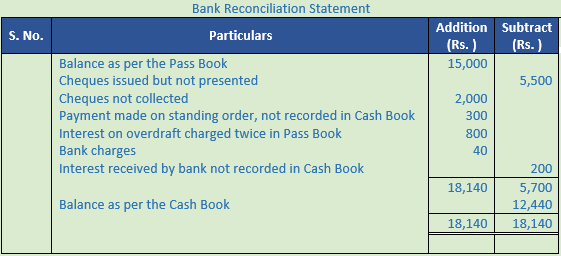

Question 20. On 30th June, 2019 the Pass Book of Sh. Mahabir Prashad showed a balance of Rs. 22,000. On comparing the Pass Book with Cash Book the following differences were found:-

- Mahabir Prashad had paid into the Bank on 26th June four cheques for Rs. 3,000; Rs. 6,000; Rs. 8,000 and Rs. 10,000. Of these, the cheque for Rs. 6,000 was credited by the bank in July 2019.

- On 23rd June three cheques were drawn for Rs. 12,000; Rs. 13,000 and Rs. 16,000. The first two cheques were presented to the bank for payment in June and the third in July 2019.

- Cheques amounting to Rs. 3,600 were deposited in the bank but no entry was passed in the Cash Book.

- Bank charges entered in Cash Book twice Rs. 50.

- Cheque received entered twice in the Cash Book Rs. 3,200.

Prepare a Bank Reconciliation Statement as on 30th June 2019.

Solution 20:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

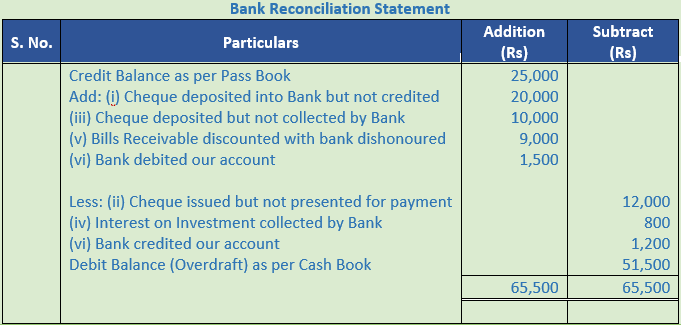

Question 21. On 31st March, 2017, Pass Book showed a balance of Rs. 25,000. Prepare a Bank Reconciliation Statement from the following particulars:

(i) Cheques of Rs. 20,000 were deposited in Bank on 27th March, 2017, out of which cheques of Rs. 5,000 were cleared on 1st April, 2017. Rest are not cleared.

(ii) On 28th March, 2017, cheques were issued amounting to Rs. 15,000, out of which cheques of Rs. 3,000 were presented in March, Rs. 4,000 on 2nd April and rest were not presented.

(iii) Cheques of Rs. 10,000 were deposited in Bank on 28th March, 2017, out of which cheques of Rs. 4,000 were cleared on 2nd April, 2017 and rest are dishonoured.

(iv) Interest on investment collected by bank does not appear in the Cash Book Rs. 800.

(v) A B/R of Rs. 9,000 previously discounted from the bank was dishonoured on 30th March, 2017 but no intimation was received from the bank till 31st March.

(vi) Bank has debited Rs. 1,500 and credited Rs. 1,200 in our account.

Solution 21:

Working Note:-

Cheque issued but not presented for payment Rs. 15,000 – Rs. 3,000 = Rs. 12,000

Point of knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

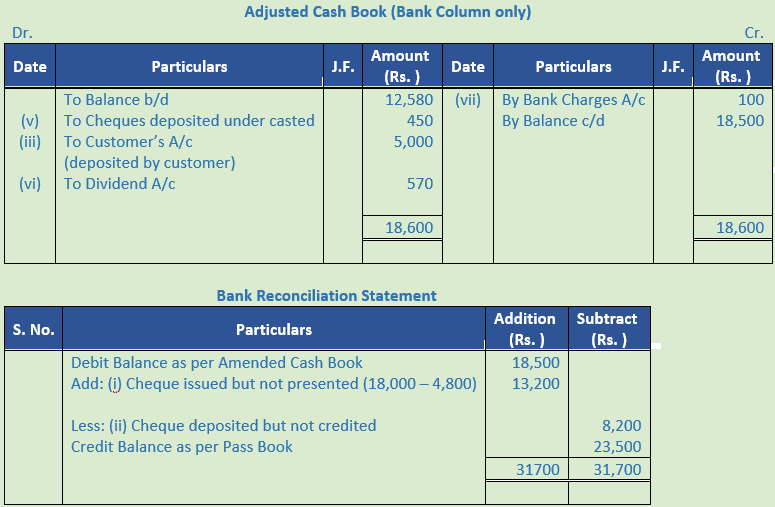

Question 22. On 31st March, 2019 the Cash Book of Gopal disclosed a balance of Rs. 12,580. On checking entries in the Cash Book with the bank statement, it was ascertained that:

(i) Cheques amounting to Rs. 18,000 were drawn on 25th March, of which cheques of Rs. 4,800 were cashed before 31st March.

(ii) Cheques for Rs. 18,000 were sent for collection out of which cheques for Rs. 8,200 were credit by bank after 31st March.

(iii) An amount of Rs. 5,000 paid directly into the merchant's account by a customer was not entered in the Cash Book.

(iv) On 31st March, cash was deposited into the bank Rs. 12,720 but the cashier debited the bank account with Rs. 12,270 by mistake.

(v) Dividend collected by bank on our behalf Rs. 570 does not appear in the Cash Book.

(vi) Rs. 300 is entered in the bank statement as bank charges. This was recorded as Rs. 200 in the cash book.

You are required:

(i) to prepare the Amended Cash Book, and

(ii) then prepare a Bank Reconciliation Statement.

Solution 22:

Working Note:-

Cheques deposited under casted = Rs. 12,720 – Rs. 12,270 = Rs. 450

Cheque issued but not presented = Rs. 18,000 – Rs. 4,800 = Rs. 13,200

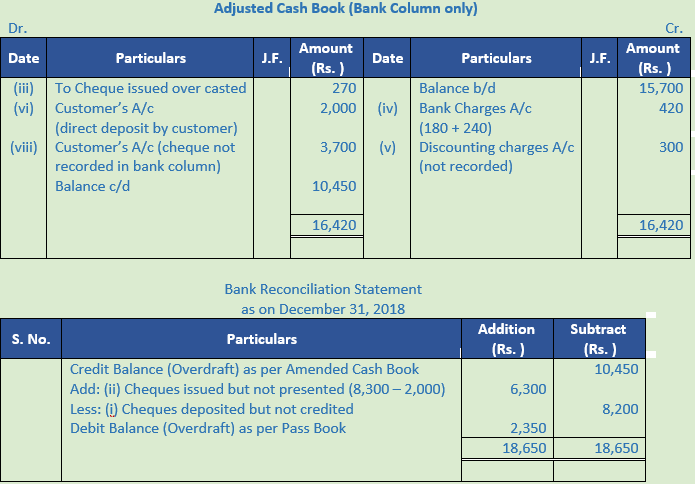

Question 23. The Cash Book of a merchant showed an overdraft balance of Rs. 15,700 on 31st December 2018. On comparing it with the Pass Book, the following differences were noted:

(i) Cheques amounting to Rs. 12,250 were deposited into the bank, out of which cheques for Rs. 8,200 have been credited in the Pass Book on 2nd January, 2019.

(ii) Cheques were issued amounting to Rs. 8,300 of which cheques for Rs. 2,000 have been cashed upto 31st Dec.

(iii) A cheque of Rs. 4,250 issued to a creditor, has been entered in the Cash Book as Rs. 4,520.

(iv) Bank charges of Rs. 180 on 30th November 2018 and Rs. 240 on 30th December 2018 have not been entered in the Cash Book.

(v) A B/R for Rs. 6,000 discounted with the bank is entered in the Cash Book without recording the discount charges of Rs. 300.

(vi) A cheque for Rs. 2,000 deposited into the bank appear in the Pass Book, but not recorded in the Cash Book.

(vii) A cheque for Rs. 3,700 deposited into the bank appear in the Pass Book, was recorded in the cash column of the Cash book.

You are required:

(i) to make appropriate adjustments in the cash book, bringing down the correct balance, and

(ii) to prepare a bank reconciliation statement with the adjusted balance

Solution 23:

Working Note:-

Cheque issued over casted Rs. 4,520 – Rs. 4,250 = Rs. 270

Bank Charges = Rs. 180 + Rs. 240 = Rs. 420

Cheques issued but not presented = Rs. 8,300 – Rs. 2,000 = Rs. 6,300

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

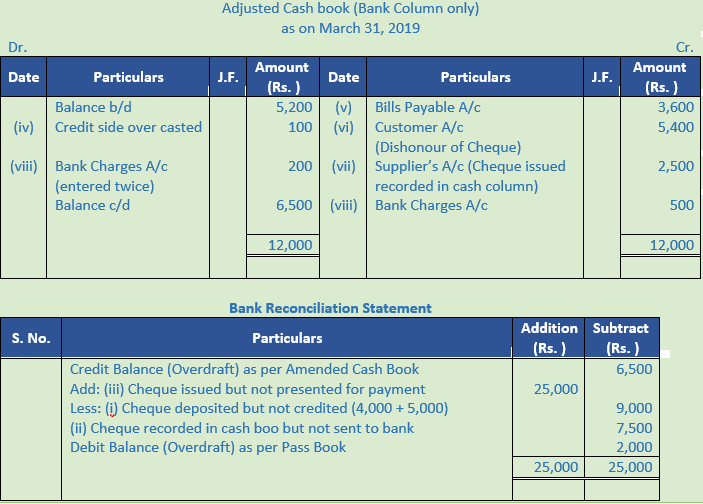

Question 24. On 31st March, 2019 the bank column of the Cash Book of Mr. Rajesh showed a debit balance of Rs. 5,200. On examining the Pass Book you find that:

(i) Cheques of Rs. 20,000 were sent to bank for collection; Out of these cheques of Rs. 4,000 and of Rs. 5,000 were credited respectively on 5th April and 6th April respectively and the remaining cheques were credited before 31st March.

(ii) A cheque for Rs. 7,500 received from a customer although entered in the bank column of the Cash Book, was omitted to be paid into the bank.

(iii) Cheques drawn for Rs. 25,000 were not presented for payment.

(iv) Credit side of the bank column of the Cash Book was overcast by Rs. 100.

(v) A B/P for Rs. 3,600 has been paid by the bank, but not yet recorded in the Cash Book.

(vi) No entry has been made in the Cash Book to record the dishonour on 28th March 2019, of a cheque for Rs. 5,400 received from a customer.

(vii) A cheque for Rs. 2,500 issued to a creditor was wrongly entered in the cash column of the Cash Book.

(viii) In the Cash Book, bank charges of Rs. 200 were entered twice while another bank charge of Rs. 500 was not recorded at all.

You are required to show the necessary corrections in the Cash Book and to prepare a statement reconciling the amended cash balance with that shown in bank Pass Book.

Solution 24:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

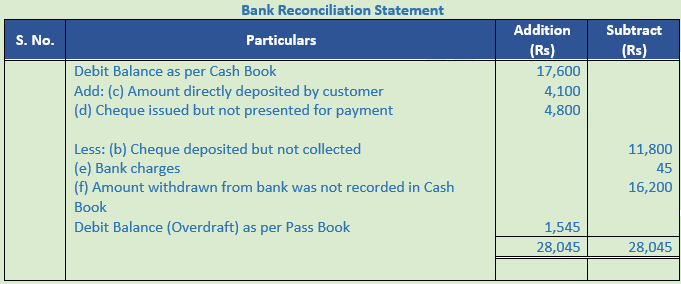

Question 25. From the following items prepare a Bank Reconciliation Statement on 31st May 2020:

(a) Bank balance as per Cash Book on 31st May 2020 Rs. 17,600.

(b) Cash and cheques totalling Rs. 36,000 were sent to bank during May but one cheque of Rs. 11,800 was shown in the Pass Book on 2nd June.

(c) As per instructions bankers have directly collected Rs. 4,100 from a customer but there is no mention of it in the Cash Book.

(d) Three cheques for Rs. 10,000, Rs. 12,000 and Rs. 4,800 respectively were drawn on 27th May but the cheque for Rs. 4,800 was encashed on 1st June.

(e) On 31st May bankers had debited Rs. 45 as bank charges but had intimated it on 3rd June.

(f) Rs. 16,200 was withdrawn from bank on 25th May but there is no entry for it in the Cash Book.

Solution 25:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

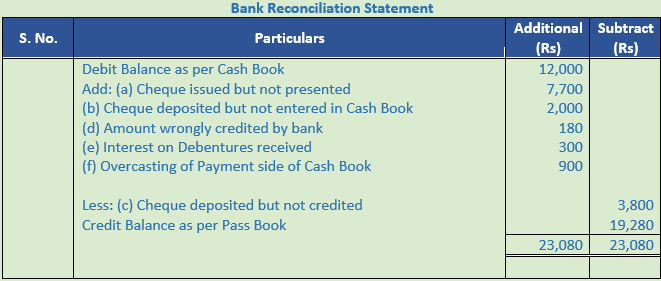

Question 26. On 31st December, 2019 the Cash Book of Gopal showed debit balance of Rs. 12,000. On comparing the Cash Book with the Pass Book, the following discrepancies were noted:-

(a) Cheques were issued for Rs. 15,000, but of them cheques for Rs. 7,700 have not yet been presented.

(b) Cheques for Rs. 8,000 were deposited in bank but of these cheques for Rs. 2,000 were not recorded in the Cash Book.

(c) Cheques deposited in bank but not credited Rs. 3,800.

(d) A cheque for Rs. 350 was paid into bank but bank credited the amount with Rs. 530 by mistake.

(e) Bank received interest on debentures on behalf of Gopal amounting to Rs. 300.

(f) It was also found that the total of one page on the payment side of the Cash Book was Rs. 4,520 but it was written on the next page as Rs. 5,420.

Prepare a Bank Reconciliation Statement.

Solution 26:

Working Note:-

Amount wrongly credited by bank Rs. 530 – Rs. 350 = Rs. 180

Overcasting of Payment side of Cash Book Rs. 5,420 – Rs. 4,520 = Rs. 900

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

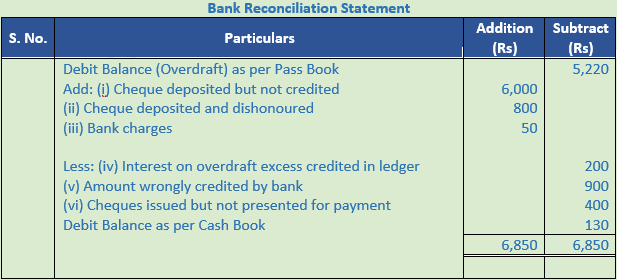

Question 27. On checking the Bank Pass Book it was found that it showed an overdraft of Rs. 5,220 as on 31.12.2019, while as per Ledger it was different to Bank Debit. The following differences were noted:

(i) Cheques deposited but not yet credited by bank Rs. 6,000.

(ii) Cheques dishonoured and debited by bank but not given effect to it in the Ledger Rs. 800.

(iii) Bank charges debited by bank but Debit Memo not received from bank Rs. 50.

(iv) Interest on overdraft excess credited in the Ledger Rs. 200.

(v) Wrongly credited by bank to account, deposit of some other party Rs. 900.

(vi) Cheques issued but not presented for payment Rs. 400.

Solution 27:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

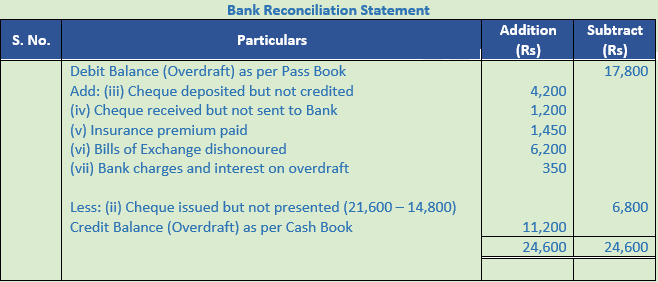

Question 28. Following information has been given by Rajendra. Prepare a Bank Reconciliation Statement as on 31st Dec. 2016, showing balance as per cash book:

(i) Debit balance shown by the pass book Rs. 17,800.

(ii) Cheques of Rs. 21,600 were issued in the last week of December, but of these Rs. 14,800 only were presented for payment.

(iii) Cheques of Rs. 10,750 were deposited in bank, out of them a cheque of Rs. 4,200 was credited in the first week of January, 2017.

(iv) A cheque of Rs. 1,200 was debited in the cash book but was not deposited in bank.

(v) Insurance premium paid by bank Rs. 1,450.

(vi) A bill of exchange for Rs. 6,200 which was discounted with bank, returned dishonoured but no entry was made in the cash book.

(vii) Bank charges and interest charged by bank are Rs. 350.

Solution 28:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

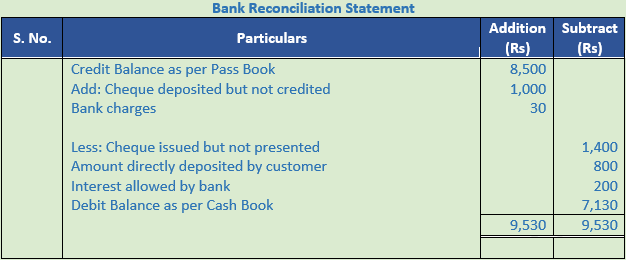

Question 29. From the following particulars prepare a bank reconciliation statement of Govil as on 31st December, 2019.

Balance as per Pass Book on 31st December 2019 is Rs. 8,500. Cheques for Rs. 5,100 were issued during the month of December but of these cheques for Rs. 1,200 were presented in the month of January 2020 and one cheque for Rs. 200 was not presented for payment. Cheques and cash amounting to Rs. 4,800 were deposited in bank during December but credit was given for Rs. 3,800 only. A customer has deposited Rs. 800 into bank directly. The bank credited the merchant for Rs. 200 as interest and has debited him for Rs. 30 as bank charges for which there are no corresponding entries in Cash Book.

Solution 29:

Working Note:-

Cheque deposited but not credited Rs. 4,800 – Rs. 3,800 = Rs. 1,000

Cheque issued but not presented Rs. 1,200 + Rs. 200 = Rs. 1,400

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

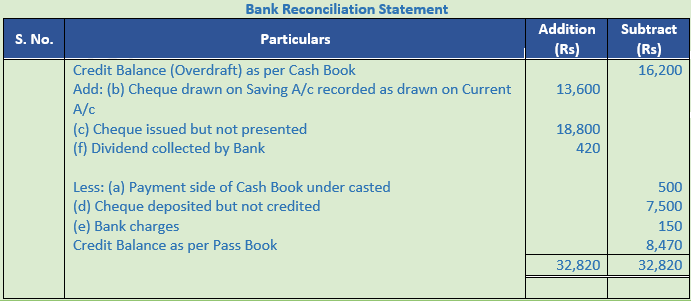

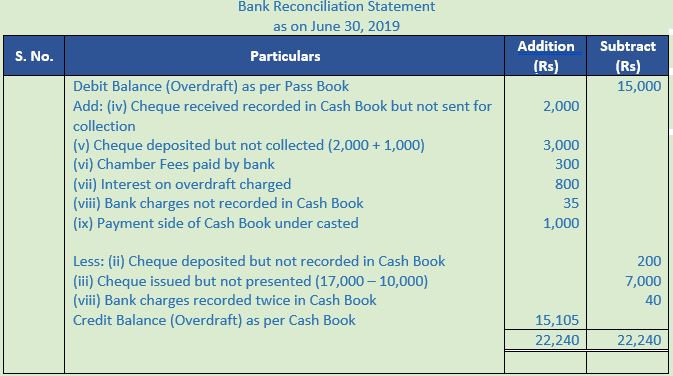

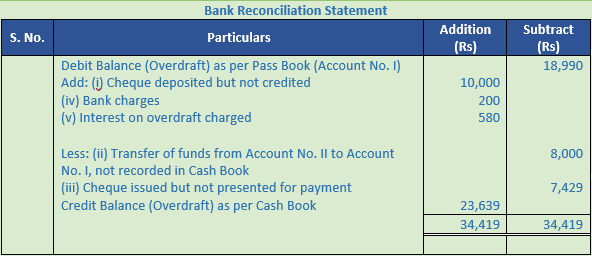

Question 30. On Checking Ram's Cash Book with the bank statement of his overdraft current account for the month of November 2019, you find the following:

(a) Cash Book showed an overdraft of Rs. 16,200.

(b) The payment side of the Cash Book had been undercast by Rs. 500.

(c) A cheque for Rs. 13,600 drawn on his saving deposit account has been wrongly recorded as drawn on current account in the Cash Book.

(d) Cheques amounting to Rs. 18,800 drawn and entered in the Cash Book had not been presented.

(e) Cheques amounting to Rs. 7,500 sent to the bank for collection though entered in the Cash Book, had not been credited by the bank.

(f) Bank charge of Rs. 150 as per bank statement of account had not been taken in the Cash Book.

(g) Dividend of the amount of Rs. 420 had been paid direct to the bank and not entered in the Cash Book.

You are requested to arrive at the balance as it would appear in the bank statement as on 30th November 2019.

Solution 30:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 31. On 31st March 2020 your bank Pass Book showed a balance of Rs. 6,000 to your credit. Before that date you had issued cheques amounting to Rs. 1,500 of which cheques worth Rs. 900 only have been presented. You also deposited cheques worth Rs. 2,000 of which cheque of Rs. 800 paid by you into bank on 29th March is not yet credited in Pass Book. You had also received a cheque for Rs. 160 which although entered by you in the bank column of the Cash Book, was omitted to be paid into the bank. On 31st March a cheque of Rs. 250 received by you was paid into the bank but the same was omitted to be entered in the cash book. There was a credit of Rs. 85 for interest on current account and debit of Rs. 10 for bank charges. Draw up a Reconciliation Statement showing adjustment between your Cash Book and pass book.

Solution 31:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

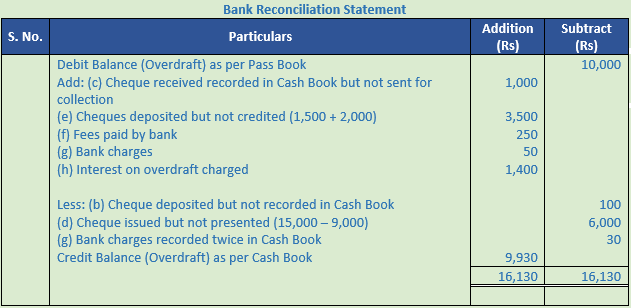

Question 32. Prepare bank reconciliation statement of Dinesh on 30th June 2019 with following particulars:

(i) Pass Book showed an overdraft of Rs. 15,000 on 30th June 2019.

(ii) A cheque of Rs. 200 was deposited in bank but not recorded in Cash Book.

(iii) Cheques of Rs. 17,000 were issued but cheques worth only Rs. 10,000 were presented for payment up to 30th June 2019.

(iv) Cheques of Rs. 2,000 were received and recorded in Cash Book but not sent to bank.

(v) Cheques of Rs. 10,000 were sent to bank for collection; out of these cheques of Rs. 2,000 and of Rs. 1,000 were credited respectively on 8th July and 10th July and the remaining cheques were credited before 30th June 2019.

(vi) Bank paid Rs. 300 fee of Chamber of Commerce on behalf of Dinesh, which was not recorded in Cash Book.

(vii) Bank charged interest on overdraft Rs. 800 which was not recorded in Cash Book.

(viii) Rs. 40 for bank charges were recorded two times in Cash Book and bank expenses of Rs. 35 were not at all recorded in Cash Book.

(ix) Total of credit side of bank column of Cash Book was undercast by Rs. 1,000 by mistake.

Solution 32:

Working Note:-

Cheque deposited but not collected = Rs. 2,000 + Rs. 1,000 = Rs. 1,000

Cheque issued but not presented = Rs. 17,000 – Rs. 10,000 = Rs. 7,000

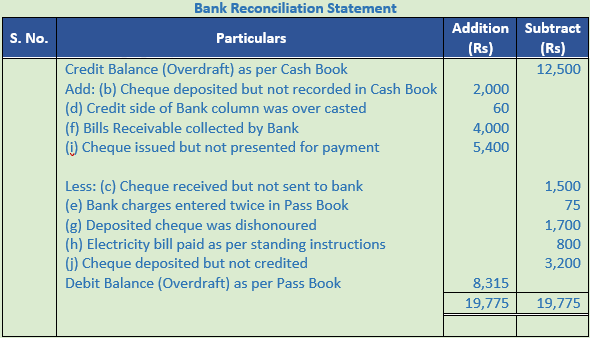

Question 33. Prepare a Bank Reconciliation Statement as on 31st March 2020 from the following informations:

Rs.

(a) Cash Book Balance (Overdraft) 12,500

(b) Cheques deposited but not recorded in Cash Book 2,000

(c) Cheque received but not sent to Bank 1,500

(d) Credit side of the Bank Column has been overcast 60

(e) Bank charges entered in Pass Book twice 75

(f) Bills Receivable directly collected by the Bank 4,000

(g) Deposited cheques returned dishonoured by Bank 1,700

(h) Electricity Bill paid by Bank as per instruction 800

(i) Cheques issued but not presented for payment 5,400

(j) Cheques deposited but not cleared 3,200

Solution 33:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

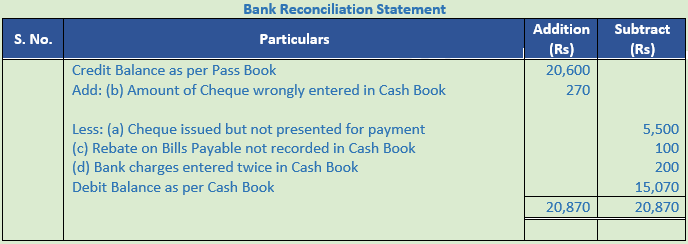

Question 34. On 31st March, 2020 the Pass Book of Mr. Janaki Dass showed a credit balance of Rs. 20,600. Prepare a Bank Reconciliation Statement from the following information:

(i) Cheques amounting to Rs. 15,000 were drawn in March 2020, out of which cheques for Rs. 5,500 were presented for payment on 3rd April.

(ii) A cheque for Rs. 5,475 was deposited into the bank, but wrongly entered in the Cash Book as Rs. 5,745.

(iii) A cheque of Rs. 5,000 which was received from a customer was entered in the cash column of the Cash Book in March 2020 but was omitted to be banked in the month of March.

(iv) A B/P of Rs. 10,000 was retired by the bank under a rebate of Rs. 100 but the full amount of the bill was credited in the Cash Book.

(v) Bank charges entered in the Cash Book twice Rs. 200.

Solution 34:

Working Note:-

Amount of Cheque wrongly entered in Cash Book = Rs. 5,745 – Rs. 5,475 = Rs. 270

Point of Knowledge:-

The third transaction in above question will not effect on the balance of bank as the cheque is not represented into bank.

Question 35. Prepare a Bank Reconciliation Statement from the following particulars as on 31st March 2020:

(i) Cheques were deposited into bank on 25th March for Rs. 20,000. Out of these cheques for Rs. 8,000 were cleared on 4th April, cheques for Rs. 6,000 on 6th April and one cheque for Rs. 1,400 was dishonoured on 7th April.

(ii) Cheques amounting to Rs. 12,000 were issued in March, out of which cheques for Rs. 2,000 were encashed upto 31st March.

(iii) A bill for Rs. 5,000 (discounted with the bank in January) dishonoured on 30th March 2020 and noting charges paid by bank Rs. 50. No information regarding the dishonour was received from the bank in March 2020.

(iv) Cheque issued to a creditor for Rs. 2,000 was through mistake entered in the cash column of the Cash Book. The same has not been presented for payment till today.

(v) Receipt side of the Cash Book (bank column) was undercast by Rs. 100.

(vi) Bank has paid a bill payable amounting to Rs. 2,500 but it has not been entered in the Cash Book.

(vii) A cheque for Rs. 2,000 issued to Mr. X was omitted to be recorded in Cash Book.

(viii) Dr. balance as per Pass Book was Rs. 7,200.

Solution 35:

Working Note:-

Cheque deposited but not credited Rs. 8,000 + Rs. 6,000 + Rs. 1,400 = Rs. 15,400

Cheque issued but not presented Rs. 12,000 – Rs. 2,000 = Rs. 10,000

Point of Knowledge:-

The fourth transaction in above question will not effect on the balance of bank as the cheque is not represented into bank.

Question 36. From the following particulars prepare bank reconciliation statement as on 31st March 2020:

(a) Debit balance as per Cash Book Rs. 1,500.

(b) A cheque for Rs. 2,000 issued in favour of X has not been presented for payment.

(c) A bill for Rs. 4,000 retired by bank under a rebate of Rs. 120. The full amount of the bill was credited in Cash Book.

(d) A cheque for Rs. 750 deposited in bank has been dishonoured.

(e) A sum of Rs. 3,600 deposited in the bank has been credited as Rs. 360 in the Pass Book.

(f) Payment side of Cash Book has been undercast by Rs. 100.

Solution 36:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 37. From the following particulars prepare bank reconciliation statement as on 31st March 2020:

(a) Debit balance as per Cash Book Rs. 1,500.

(b) A cheque for Rs. 2,000 issued in favour of X has not been presented for payment.

(c) A bill for Rs. 4,000 retired by bank under a rebate of Rs. 120. The full amount of the bill was credited in Cash Book.

(d) A cheque for Rs. 750 deposited in bank has been dishonoured.

(e) A sum of Rs. 3,600 deposited in the bank has been credited as Rs. 360 in the Pass Book.

(f) Payment side of Cash Book has been undercast by Rs. 100.

Solution 37:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 38. From the following particulars, prepare a Bank Reconciliation Statement of Alpha Electronic Motor. Private Ltd. as on 30th September, 2019:

(a) Overdraft on 30th September 2019 as per Pass Book Rs. 10,000.

(b) Cheque deposited in the bank but not recorded in Cash Book Rs. 100.

(c) Cheque received and recorded in the Cash Book but not sent to bank for collection Rs. 1,000.

(d) Several cheques were drawn in the last week of September, totalling Rs. 15,000; of these cheques totalling only Rs. 9,000 were cashed before 30th September.

(e) Similarly, several cheques, totaling Rs. 9,000 were sent for collection; of these cheques of the value of Rs. 1,500 were credited on 5th October and Rs. 2,000 on 7th October, balance being credited before 30th September.

(f) Fees of Rs. 250 was paid directly by the bank but was not recorded in the Cash Book.

(g) In the Cash Book, a bank charge of Rs. 30 was recorded twice while another bank charge of Rs. 50 was not recorded at all.

(h) Interest of Rs. 1,400 was charged by the bank but was not recorded in the Cash Book.

Solution 38:

Working Note:-

Cheques deposited but not credited = Rs. 1,500 + Rs. 2,000 = Rs. 3,500

Cheque issued but not presented = Rs. 15,000 – Rs. 9,000 = Rs. 6,000

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 39. The following information relate to the business of Mohit Raina, who requests you to prepare his amended Cash Book and reconcile his Cash Book balance with his Pass Book balance:

Balance as per Cash Book (Cr.) 40,000

Unpresented cheques 72,000

Uncredited cheques 13,000

You have been given the following additional information:

(a) The debit side of the Cash Book (Bank Column) has been undercast by Rs. 25,000.

(b) A cheque for Rs. 10,000 paid to a creditor has been wrongly entered in the Cash Column.

(c) Bank commission and other charges Rs. 4,000 have not been recorded in the Cash Book.

Solution 39:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

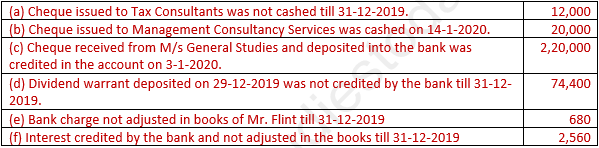

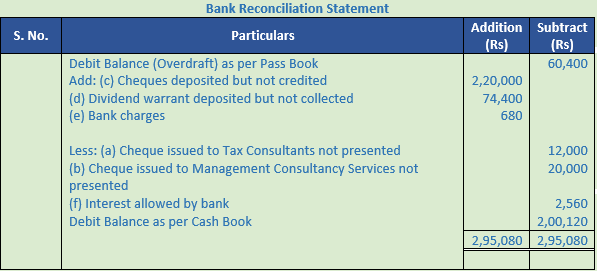

Question 40. The bank statement of Mr. James Flint showed an overdraft to the tune of Rs. 60,400 as on 31-12-2019. Cash Book showed a debit balance of Rs. 2,00,120 as on the same date. The following further facts are available:

Prepare a Bank Reconciliation Statement of Mr. James Flint as on 31-12-2019.

Solution 40:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 41. The following facts were extracted as at 31st December 2019 from the books of Rajesh Dogra who keeps a double column Cash Book:

Bank balance as per Cash Book (overdrawn) 32,000

Balance as per bank statement (in favour) 24,000

Rs. 200 commission charged by bank on outstation cheques yet to be taken into account.

A cheque for Rs. 11,000 paid to Shashi Bhushan wrongly entered in the cash column.

Debit side of Cash Book (bank column) under cast by Rs. 1,000. Cheques received from customers Rs. 10,400 deposited on 31-12-2019 but credited by the bank on 2-1-2020.

Cheques issued to supplier’s Rs. 76,600 during 2019 not yet presented for encashment.

Prepare a Bank Reconciliation Statement as at 31-12-2019.

Solution 41:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

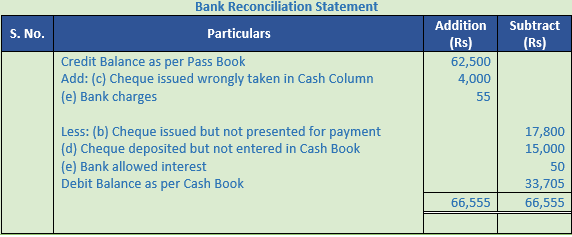

Question 42. Prepare a Bank Reconciliation Statement in the books of Bharti as on 31st January 2017:

(a) Balance as per Pass Book as on 31st January, 2017 was Rs. 62,500.

(b) Cheque of Rs. 17,800 was issued by her on 28th January 2017 but this was not presented for payment till 31st January 2017.

(c) A cheque of Rs. 4,000 issued to Mr. Rahim, was taken in the cash column.

(d) A cheque of Rs. 15,000 was paid into bank but was omitted to be entered in the cash book.

(e) The bank has charged Rs. 55 as its commission and has allowed interest Rs. 50.

Solution 42:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

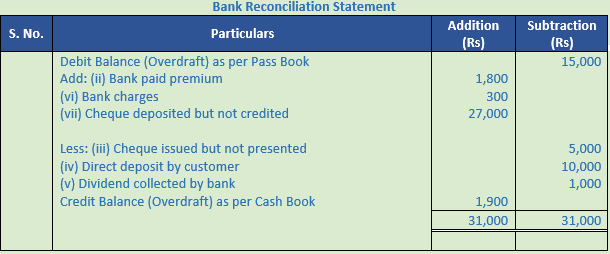

Question 43. Prepare a Bank Reconciliation Statement as on 31st Dec., 2012 from the following transactions:

(i) Bank overdraft as per Pass Book Rs. 22,000 as on 31st Dec.

(ii) On 28th Dec., cheques had been issued for Rs. 50,000 of which cheques worth Rs. 6,000 only had been encashed upto 31st Dec.

(iii) Cheques amounted to Rs. 4,500 had been paid into the bank for collection but out of these only Rs. 1,000 had been credited in the Pass Book.

(iv) The bank has charged Rs. 1,500 as interest on overdraft and the intimation of which has not been received as yet.

(v) Bank has collected Rs. 1,600 directly in respect of interest on investment.

(vi) A cheque of Rs. 1,200 has been debited in bank column of Cash Book, but it was not sent to bank at all.

Solution 43:

Working Note:-

Cheque deposited but not credited Rs. 4,500 – Rs. 1,000 = Rs. 3,500

Cheque issued but not presented Rs. 50,000 – Rs. 6,000 = Rs. 44,000

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 44. While comparing the cash book of Mayank with the bank pass book on 30th September, 2016 you find the following:

(i) The bank pass book showed a debit balance of Rs. 15,000.

(ii) Bank paid insurance premium Rs. 2,000, but it was recorded as Rs. 200 only in cash book.

(iii) Cheques issued in favour of suppliers in September, 2016 amounted to Rs. 55,000, but cheques for Rs. 50,000 only were presented for payment upto 30th September, 2016.

(iv) Direct deposit of Rs. 10,000 in Mayank's bank account by a customer on 25th September, 2016 had not been recorded in the cash book.

(v) Dividend collected by bank, but not recorded in cash book Rs. 1,000.

(vi) Bank charged Rs. 300 for its services, but they were yet to be recorded in cash book.

(vii) Cheques amounting to Rs. 78,000 were deposited with bank in the last week of September, 2016 but cheques for Rs. 51,000 only had been cleared before 1st October, 2016.

Prepare the bank reconciliation statement ascertaining bank balance/overdraft as per cash book.

Solution 44:

Working Note:-

Bank paid premium = Rs. 2,000 – Rs. 200 = Rs. 1,800

Cheque deposited but not credited = Rs. 78,000 – Rs. 51,000 = Rs. 27,000

Cheque issued but not presented = Rs. 55,000 – Rs. 50,000 = Rs. 5,000

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

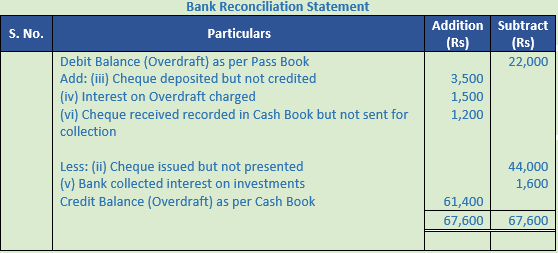

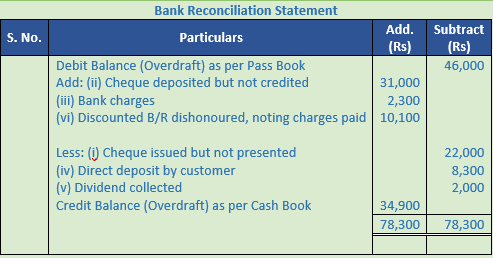

Question 45. On 30th June, 2016, the pass book of Nataraj showed a bank overdraft of Rs. 46,000. The following additional information is available. You are required to prepare a bank reconciliation statement as on the above mentioned date:

(i) Out of total cheques issued, cheques for Rs. 22,000 have not been presented for payment so far.

(ii) Cheques paid into bank for collection, but not yet cleared total Rs. 31,000.

(iii) Bank has charged Rs. 2,300 as interest on overdraft; it does not appear in cash book.

(iv) A customer has directly deposited Rs. 8,300 with bank in Nataraj's account for which there is no entry in cash book.

(v) Dividend on shares collected by bank and credited in the pass book amounts to Rs. 2,000 for which no intimation has been given to Nataraj so far.

(vi) A bill for Rs. 10,000 discounted with the bank was dishonoured on maturity. Bank has debited Nataraj with Rs. 10,100 including Rs. 100 for noting charges, the transaction has not yet been recorded in cash book.

Solution 45:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 46. On 31st December, 2019, pass book shows debit balance of Rs. 7,500. From the following particulars, prepare a Bank Reconciliation Statement:

(a) Cheques paid in for collection amounted to Rs. 20,600 but cheques of Rs. 7,800 were credited on 3rd January, 2020.

(b) A cheque of Rs. 1,000 debited in cash book was omitted to be banked.

(c) Cheques of Rs. 7,800 were drawn on 27th December of which cheques of Rs. 2,400 were cashed upto 31st December.

(d) A cheque of Rs. 800 was banked and credited, but omitted to be recorded in cash book.

(e) Bank charged interest on Overdraft Rs. 650.

Solution 46:

Working Note:-

Cheque issued but not presented Rs. 7,800 – Rs. 2,400 = Rs. 5,400

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 47. From the following particulars make out the Bank Reconciliation Statement as on 31st December 2016.

(a) Pass book showed a credit balance of Rs. 15,000 on 31st December 2016.

(b) Cheques of Rs. 17,500 were issued but cheques of Rs. 12,000 only presented for payment till 31st December.

(c) Cheques of Rs. 10,000 were sent to the bank for Collection. Out of which cheques of Rs. 2,000 were credited in the month of January 2017.

(d) Bank paid Rs. 300 as per standing instructions but no record made in the cash book.

(e) Bank charged interest on overdraft Rs. 800 and it was entered twice in pass book by bank.

(f) Rs. 40 as bank charges not recorded in the cash book.

(g) Bank receives Rs. 200 as interest on debentures, but no information being sent to the customer.

Solution 47:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.