Read DK Goel Class 11 Accountancy Solutions for Chapter 16 Depreciation below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 16 Depreciation should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 16 Depreciation DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 16 Depreciation in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 16 Depreciation Class 11 Accountancy

Short Answer Questions

Question 1. Define depreciation. State any two reasons for providing depreciation.

Solution 1: Depreciation may be defined as the permanent and continuing diminution in the quality, quantity or the value of an asset.

Below are the two reasons for providing depreciation:-

1.) For ascertaining the true profit or loss by profit & loss account.

2.) For showing the true financial position by the balance sheet.

Question 2. Give four advantages of Straight Line Method of providing depreciation.

Solution 2: Below are advantages of using Straight Line Method:-

1.) Simplicity

2.) Assets can be completely written off

3.) Knowledge of Original Cost and Up-to-date depreciation

4.) Equity of Depreciation Burden

Question 3. State four merits of written down value method of providing depreciation.

Solution 3: Below are merits of using written down value Method:-

1.) Easy Calculation

2.) Equal charge against income

3.) No undue pressure in later years

4) Balance of assets is never written off to zero

Question 4. State two demerits of Reducing Instalment Method of providing depreciation.

Solution 4: Below are demerits of Reducing Instalment Method:-

1.) Asset cannot be completely written off

2.) Omission of Interest Factor

Question 5. Distinguish between ‘Straight Line Method’ and ‘Written Down Value Method’ of providing depreciation.

Solution 5:

Question 6. Write short note on ‘Original Cost Method’ of providing depreciation with a suitable example.

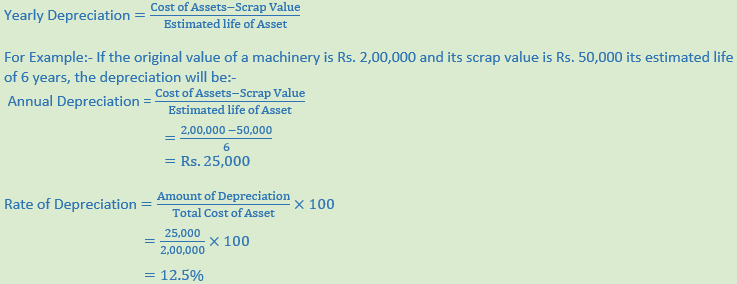

Solution 6: Straight line method is known as Original Cost Method. Under this method depreciation charged at a fixed percentage on the original cost of the asset. The amount of depreciation remains equal from year and as such the method is also known as ‘Equal Instalments Method’ and ‘Fixed Instalment Method’. Under this Method the amount of deprecation is calculated by the following formula:-

Question 7. What is asset disposal account? Why is it prepared? Give journal entries for preparation of this account when an asset is disposed off.

Solution 7: When part of the asset is sold or disposed off, it is appropriate to open a new account called “asset disposal account’. It provides a complete and clear view of all the transactions involved in the sale of an asset and shows the profit and loss on sale of asset.

(i) transfer the book value of asset to Asset disposal account:-

Asset Disposal A/c Dr.

To Asset A/c

(ii) Sale of Asset:-

Bank A/c Dr.

To Asset Disposal A/c

(iii) Profit on sale of asset

Asset Disposal A/c Dr.

To Profit on sale of asset A/c

Or

Loss on sale of asset

Loss on sale of asset A/c Dr.

To Asset Disposal A/c

Practical Questions

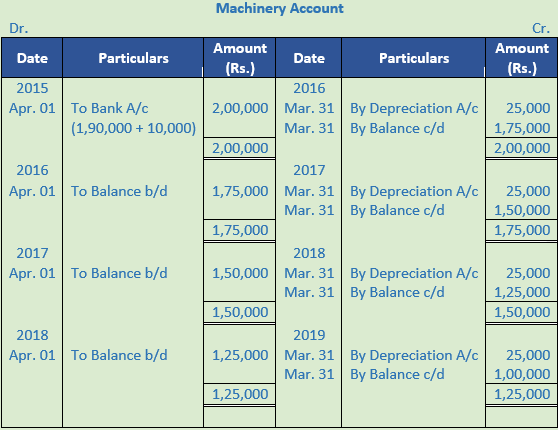

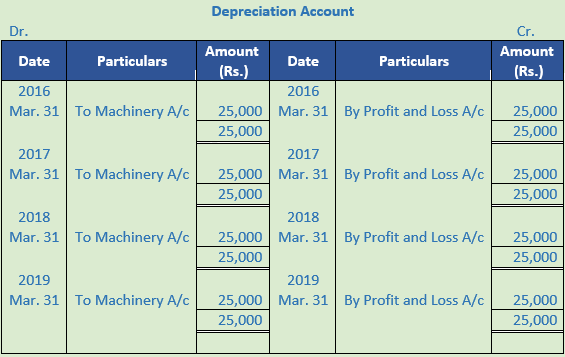

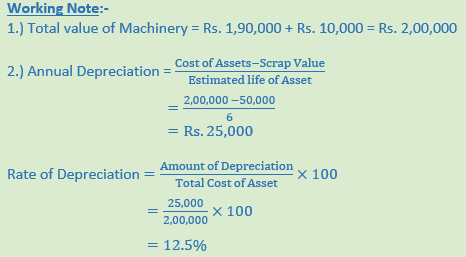

Question 1. On 1st April, 2015, a limited company purchased a Machine for Rs. 1,90,000 and spent Rs. 10,000 on its installation. At the date of purchase, it was estimated that the scrap value of the machine would be Rs. 50,000 at the end of sixth year.

Give Machine Account and Depreciation A/c in the books of the Company for 4 years after providing depreciation by Fixed Instalment Method. The books are closed on 31st March every year.

Solution 1:

Point of Knowledge:-

Methods of Calculating Depreciation:-

- Straight Line Method

- Written Down Value Method

- Annuity Method

- Depreciation Fund Method

- Insurance Policy Method

- Revaluation Method

- Depletion Method

- Machine Hour Rate Method

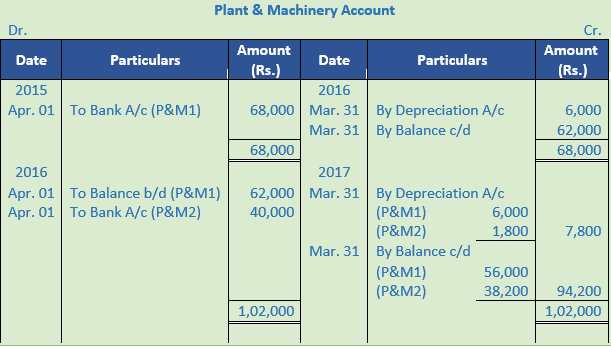

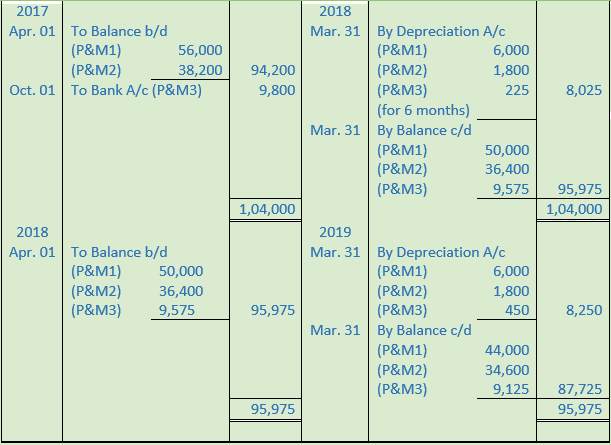

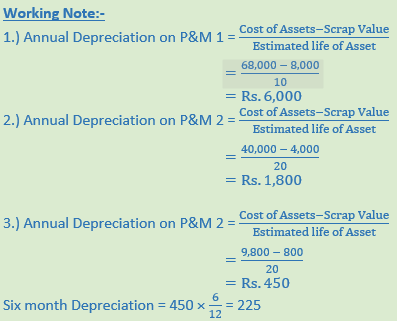

Question 2. On 1st April, 2015, a Company bought Plant and Machinery costing Rs. 68,000. It is estimated that its working life is 10 years, at the end of which it will fetch Rs. 8,000. Additions are made on 1st April, 2016 to the value of Rs. 40,000 (Residual value Rs. 4,000). More additions are made on Oct. 1, 2017 to the value of Rs. 9,800 (Break up value Rs. 800). The working life of both the additional Plant and machinery is 20 years.

Show the Plant and Machinery account for the first four years, if depreciation is written off according to Straight Line Method. The accounts are closed on 31st March every year.

Solution 2:

Point of Knowledge:-

Straight line method is known as Original Cost Method. Under this method depreciation charged at a fixed percentage on the original cost of the asset. The amount of depreciation remains equal from year and as such the method is also known as ‘Equal Instalments Method’ and ‘Fixed Instalment Method’.

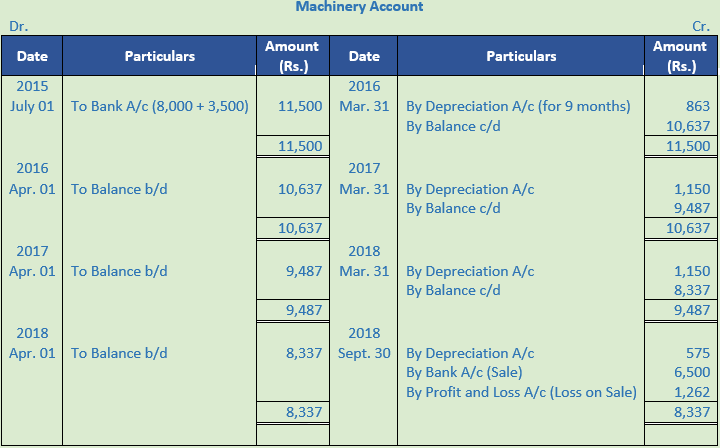

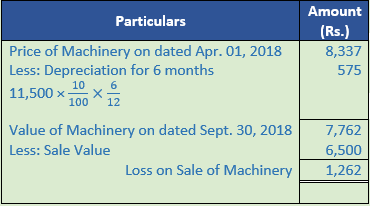

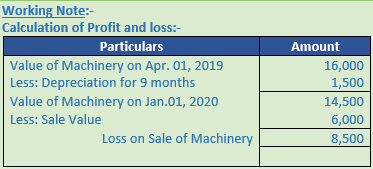

Question 3. Chandra Ltd. purchased a second-hand machine for Rs. 8,000 plus CGST and SGST @ 6% each on 1st July, 2015. They spent Rs. 3,500 on its overhaul and installation.

Depreciation is written off 10% p.a. on the original cost. On 30th September, 2018, the machine was found to be unsuitable and sold for Rs. 6,500. Prepare the Machinery A/c for four years assuming that accounts are closed on 31st March.

Solution 3:

Working Note:-

Value of machinery = Rs. 8,000 + Rs. 3,500 = Rs. 11,500

Calculation of Profit and Loss:-

Point of Knowledge:-

1.) For ascertaining the true profit or loss by profit & loss account.

2.) For showing the true financial position by the balance sheet.

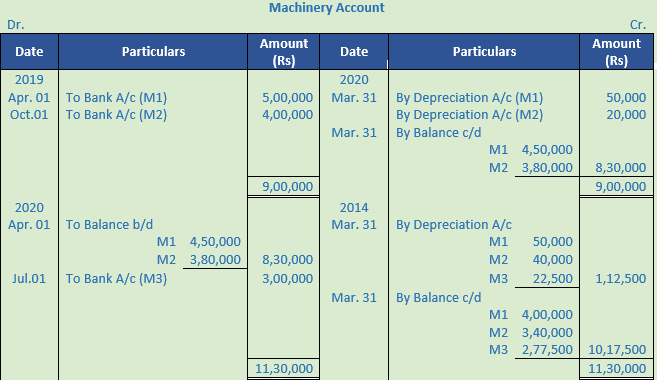

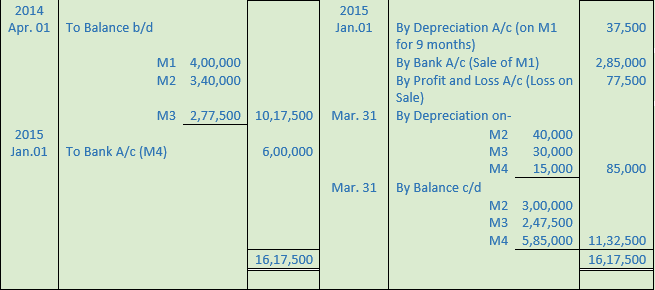

Question 4. A Ltd. purchased a machine for Rs. 5,00,000 on 1st April, 2019. Further addition were made on 1st October 2019 and on 1st July 2020 for Rs. 4,00,000 and Rs. 3,00,000 respectively. On 1st January, 2015, 1st machine was sold for Rs. 2,85,000 and new machine was purchased for Rs. 6,00,000.

Prepare Machine A/c for three years ending 31st March, 2015 if depreciation is to be charged @ 10% p.a. on straight line basis.

Solution 4:

Point of Knowledge:-

The amount of depreciation to be charged for the year is calculated by using various methods. But the two main methods for calculating depreciation are:

- Fixed Percentage on Original Cost or Fixed Instalment or Straight Line Method.

- Fixed Percentage on Diminishing Balance or Reducing Instalment Method or Written Down Value Method.

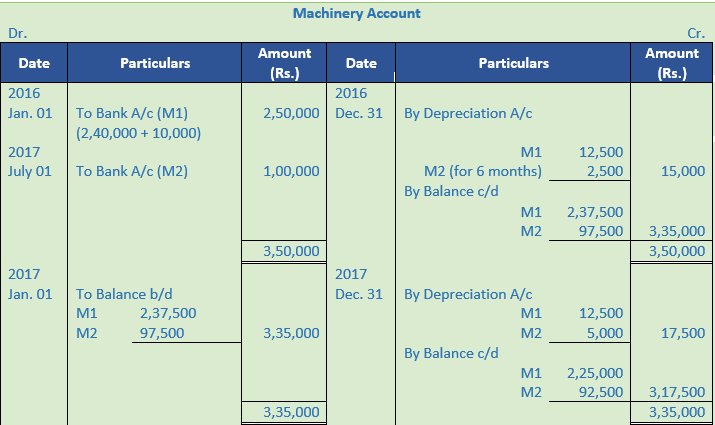

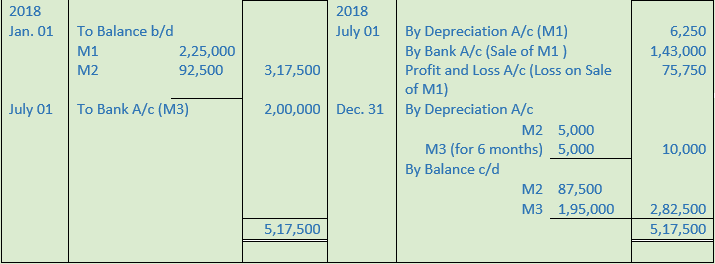

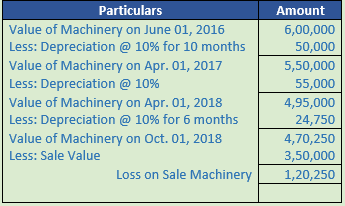

Question 5. On 1st January, 2016, A Ltd. Purchased a machine for Rs. 2,40,000 and spent Rs. 10,000 on its erection. On 1st July, 2016 an additional machinery costing Rs. 1,00,000 was purchased. On 1st July, 2018 the machine purchased on 1st January, 2016 was sold for Rs. 1,43,000 and on the same date, a new machine was purchased at a cost of Rs. 2,00,000.

Show the Machinery Account for the first three calendar years after charging depreciation at 5% by the Straight Line Method.

Solution 5:

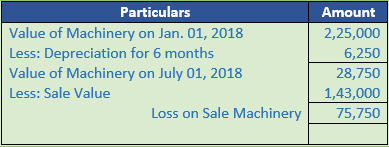

Working Note:-

Calculation of profit and loss:-

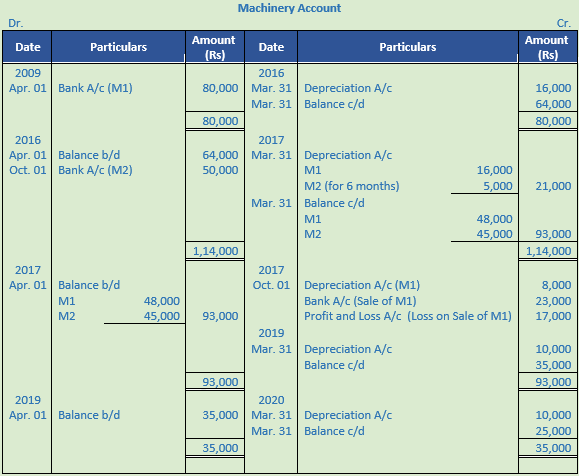

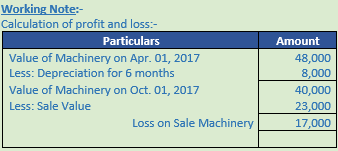

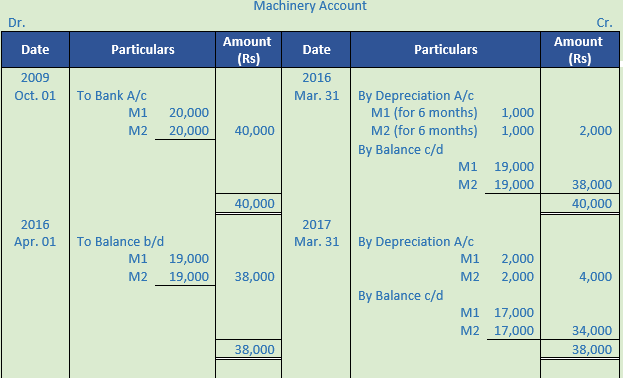

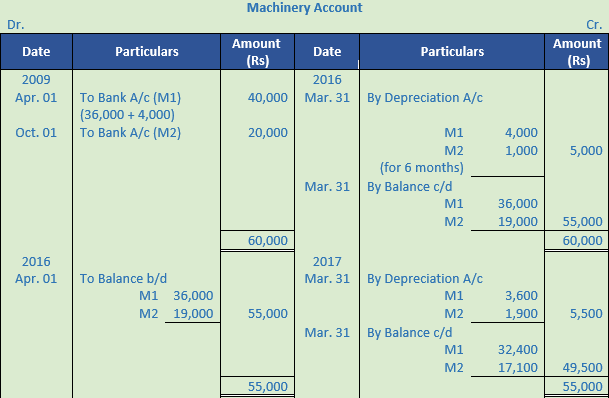

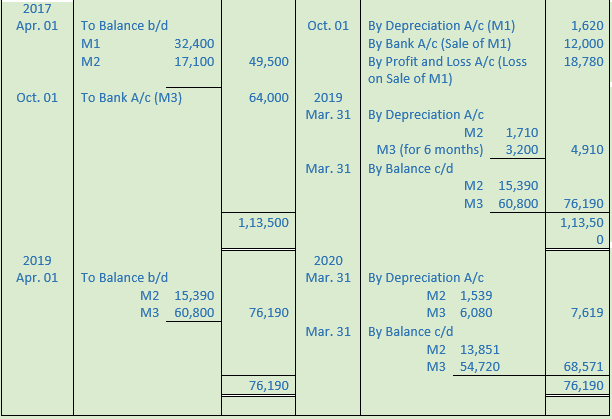

Question 6. A company purchased on 1st April, 2009, a machinery for Rs. 80,000. On 1st October, 2016, it purchased another machine for Rs. 50,000 and on 1st October, 2017, it sold off the first machine purchased in 2009 for Rs. 23,000. Depreciation was provided on the machinery at the rate of 20% p.a. on the original cost annually.

Give the Machinery Account for four years commencing from 1st April, 2009.

Accounts are closed on 31st March every year.

Solution 6:

Point of Knowledge:-

- It is a simple method of calculating the depreciation.

- In this method, assets can be depreciated up to the estimated scrap value or zero value.

- It is easy to calculate the amount of depreciation under this method.

- The Profit and Loss Account is debited or charged with same amount of depreciation every year and uniformity is maintained on the expenditure.

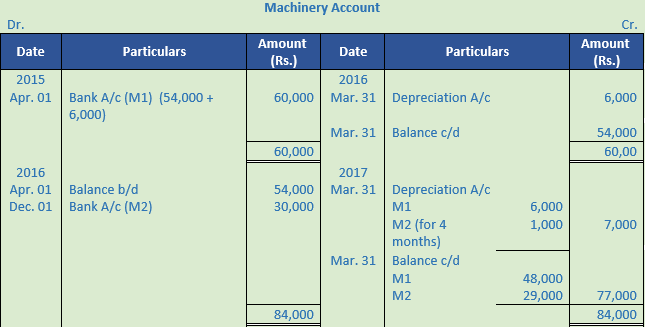

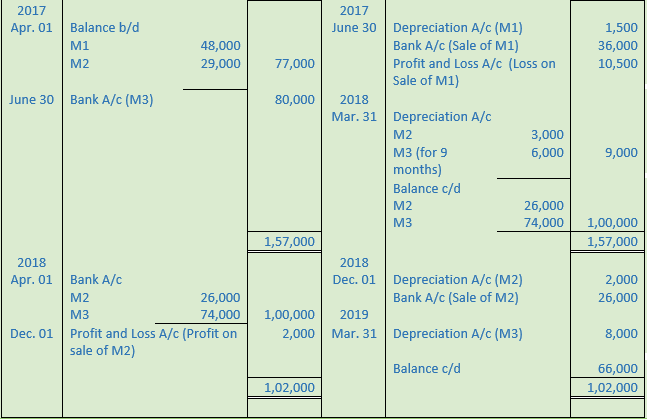

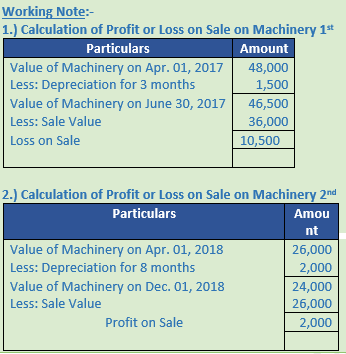

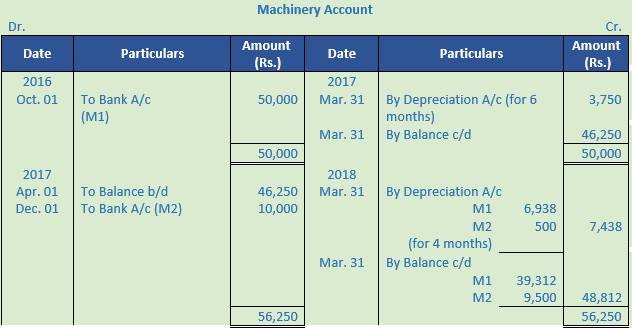

Question 7. Bhushan & Company purchased a Machinery on 1st April, 2015, for Rs. 54,000 and spent Rs. 6,000 on its installation. On 1st December, 2016, it purchased another machine for Rs. 30,000.

On 30th June 2017, the first machine purchased on 1st April, 2015, is sold for Rs. 36,000 and on the same date it purchased a new machinery for Rs. 80,000.

On December 1, 2018, the second machine (purchased on December 1, 2016) was also sold off for Rs. 26,000.

Depreciation was provided on machinery @ 10% p.a. on Original Cost Method annually on 31st March. Give the machinery account for four years.

Solution 7:

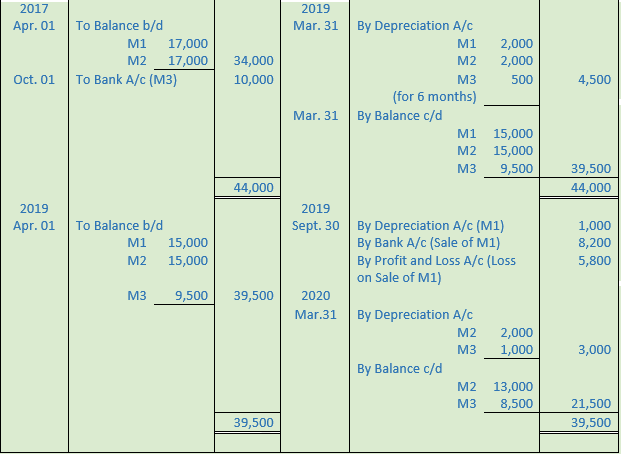

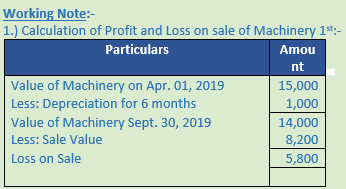

Question 8. On 1st October, 2009, Raj & Co. purchased machinery worth Rs. 40,000. On 1st October, 2017, it buys additional machinery worth Rs. 10,000. On 30th September, 2019, half of the machinery purchased on 1st Oct., 2009, is sold for Rs. 8,200. The company writes off 10 per cent p.a. on the original cost. The accounts are closed every year on 31st March.

Show the Machinery Account for four years.

Solution 8:

Point of Knowledge:-

- It is a simple method of calculating the depreciation.

- In this method, assets can be depreciated up to the estimated scrap value or zero value.

- It is easy to calculate the amount of depreciation under this method.

- The Profit and Loss Account is debited or charged with same amount of depreciation every year and uniformity is maintained on the expenditure.

Question 9.

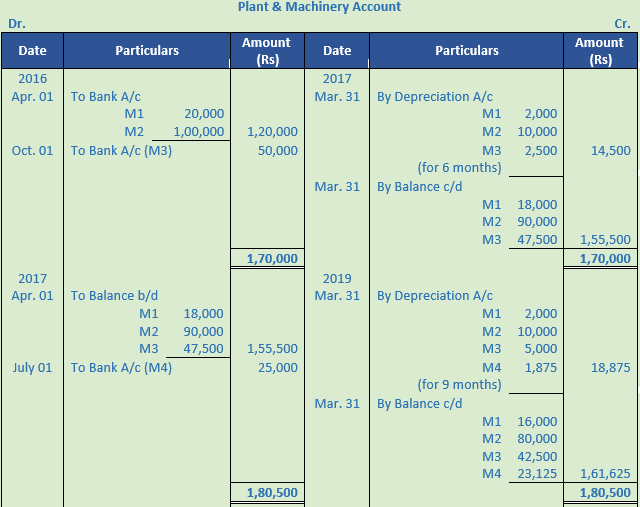

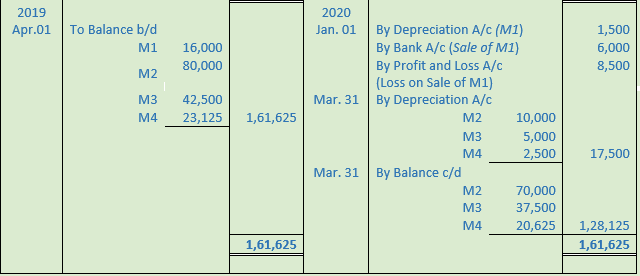

On 1st April, 2016, Plant and Machinery was purchased for Rs. 1,20,000. New machinery was purchased on 1st Oct., 2016, for Rs. 50,000 and on 1st July, 2017, for Rs. 25,000.

On 1st January, 2020, a machinery of the original value of Rs. 20,000 which was included in the machinery purchased on 1st April, 2016, was sold for Rs. 6,000. Prepare Plant & Machinery A/c for three years after providing depreciation at 10% p.a. on Straight Line Method. Accounts are closed on 31st March every year.

Solution 9:

Point of Knowledge:-

- There is same weightage on Profit and Loss Account of depreciation and repair expenses.

- This method is easier than Straight Line Method.

- In case of expansion and increase in assets, the depreciation can be computed easily by this method.

- This method is acceptable by the Government under the Income Tax Act.

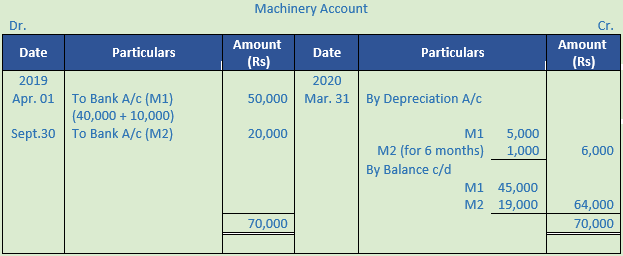

Question 10. From the following transactions of a concern, prepare Machinery Account for the year ending 31st March, 2020 :-

2019

April 1 : Purchased a second-hand machinery for Rs. 40,000.

April 1 : Spent Rs. 10,000 on repairs for making it serviceable.

Sept. 30 : Purchased additional new machinery for Rs. 20,000.

Dec. 31 : Repairs and renewals of machinery Rs. 2,000.

2020

March 31 : Depreciate the machinery at 10% p.a.

Solution 10:

Point of Knowledge:-

Repair charges of Rs. 2,000 have been incurred on Dec., 31 whereas the machinery has been purchased on Sept. 30. As such, it is an expenditure of revenue nature and hence will not be recorded in Machinery A/c

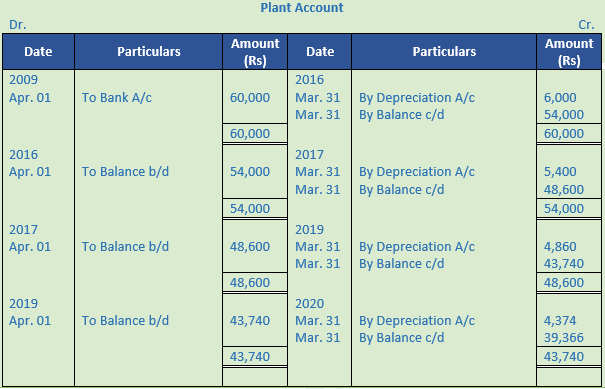

Question 11. A plant is purchased for Rs. 60,000 on 1st April, 2009. It is estimated that the residual value of this plant at the end of its working life of 10 years will be Rs. 20,920. Depreciation is to be provided at 10% p.a. on diminishing balance method.

You are required to show the Plant Account for 4 years, assuming that the books are closed on 31st March every year.

Solution 11:

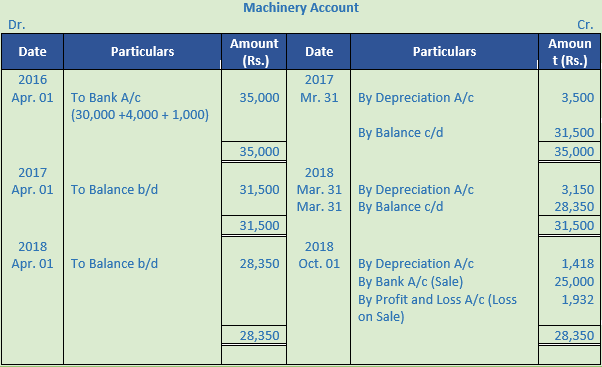

Question 12. A Company purchased a second-hand machine on 1st April, 2016, for Rs. 30,000 and immediately spent Rs. 4,000 on its repair and Rs. 1,000 on its installation. On Oct. 1, 2018, the machine was sold for Rs. 25,000. Prepare Machine Account after charging depreciation @ 10% p.a. by diminishing balance method, assuming that the books are closed on 31st March every year. IGST was charged @ 12% on purchase and sale of machine.

Solution 12:

Working Note:-

Total Value of Machinery = 30,000 + 4,000 + 1,000 = 35,000

Calculation of Profit and loss:-

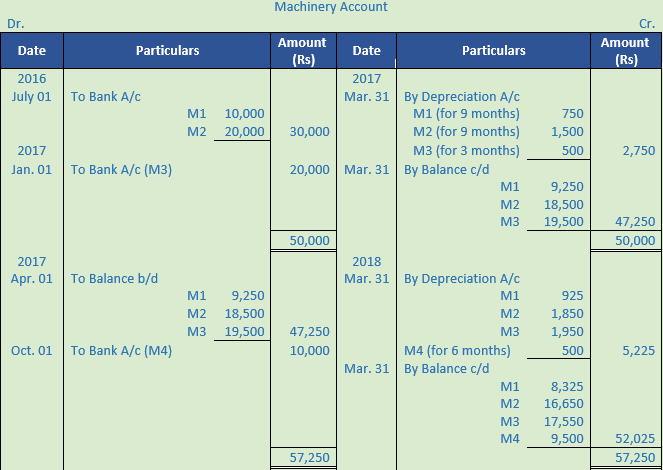

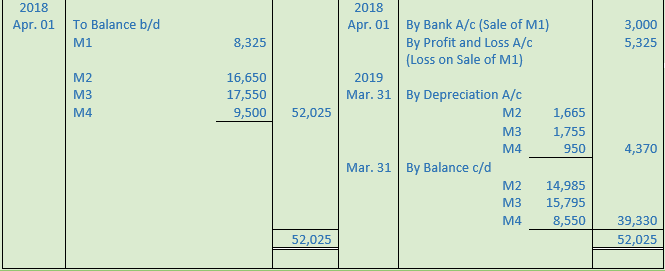

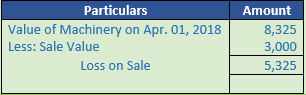

Question 13. A firm purchased on 1st April, 2009, a second-hand Machinery for Rs. 36,000 and spent Rs. 4,000 on its installation. On 1st Oct. in the same year another Machinery costing Rs. 20,000 was purchased. On 1st Oct., 2017, the Machinery bought on 1st April, 2009 was sold off for Rs. 12,000 and on the same date a fresh Machine was purchased for Rs. 64,000. Depreciation is provided annually on 31st March, @ 10% p.a. on the Written Down Value Method. Show the Machine A/c from 1st April, 2009 to 31st March, 2020.

Solution 13:

Point of Knowledge:-

The following are the disadvantages of the Written Down Value Method:

- In this method the value of the asset can never be zero.

- It is a difficult task to ascertain the proper rate of depreciation.

- There is no provision of interest on capital invested in use of assets.

Question 14. A Company purchased a machinery for Rs. 50,000 on 1st Oct., 2016. Another machinery costing Rs. 10,000 was purchased on 1st Dec., 2017. On 31st March, 2019, the machinery purchased in 2016 was sold at a loss of Rs. 5,000. The Company charges depreciation at the rate of 15% p.a. on Diminishing Balance Method. Accounts are closed on 31st March every year.

Prepare Machinery account for 3 years.

Solution 14:

Working Note:-

Calculation of Profit and Loss on Sale of Machinery:-

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

Question 15.

Ashoka Ltd. bought a machine on 1st April, 2016 for Rs. 2,40,000 and spent Rs. 4,000 on its carriage and Rs. 6,000 towards installation cost. On 1st July, 2017 it purchased a second hand machinery for Rs. 75,000 and spent Rs. 25,000 on its overhauling.

On 1st January, 2019 it decided to sell the machinery bought on 1st April, 2016 at a loss of Rs. 20,000. It bought another machine on the same date for Rs. 40,000. Company decided to charge depreciation @ 15% p.a. on written down value method. Prepare machinery account for 3 years. Books are closed each year on 31st March.

Solution 15:

Working Note:-

Value of Machine 1 = Rs. 2,40,000 + Rs. 4,000 + Rs.6,000 = Rs. 2,50,000

Value of Machine 2 = Rs. 75,000 + Rs. 25,000 = Rs. 1,00,000

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

Question 16.

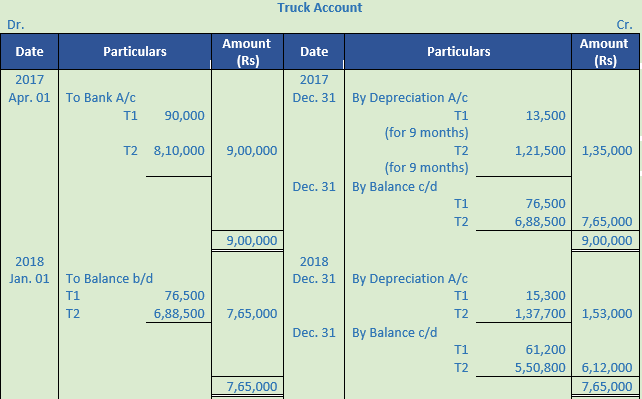

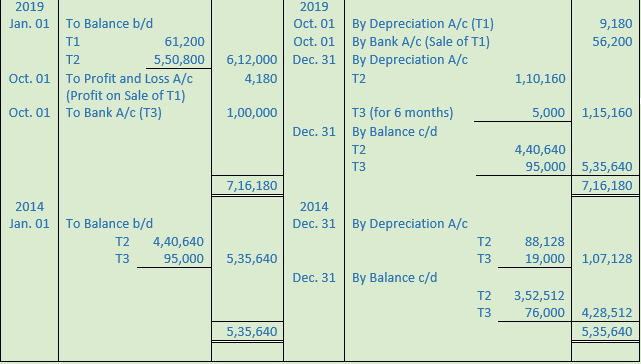

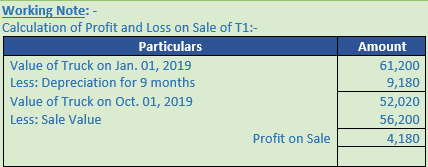

The Sameer Transport Company purchased 10 Trucks at Rs. 90,000 each on 1st April 2017. On 1st October 2019 one of the Trucks was involved in an accident and is completely destroyed. Rs. 56,200 was received from the Insurance company in full settlement. On the same date another truck was purchased by the company for the sum of Rs. 1,00,000. The company writes off 20% per annum on the Diminishing Balance Method. The company maintains the calendar year as its financial year. Show the Truck Account for four years ending 31st December, 2014.

Solution 16:

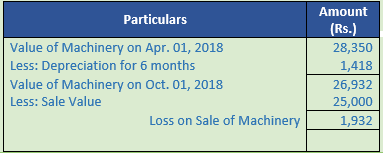

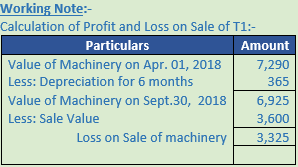

Question 17. Raja Textiles Co. which closes its books on 31st March, purchased a machine on 1-4-2009 for Rs. 50,000. On 1-10-2016, it purchased an additional machine for Rs. 30,000. The part of the machine which was purchased on 1-4-2009 costing Rs. 10,000 was sold for Rs. 3,600 on 30th Sept., 2018. Prepare the Machine Account for four years, if the depreciation is provided at the rate of 10% p.a. on Diminishing Balance Method.

Solution 17:

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

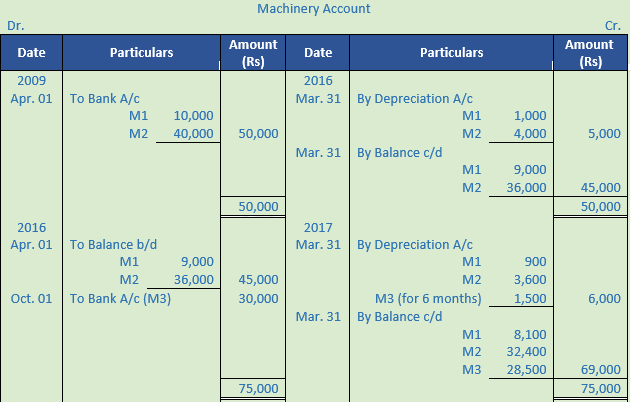

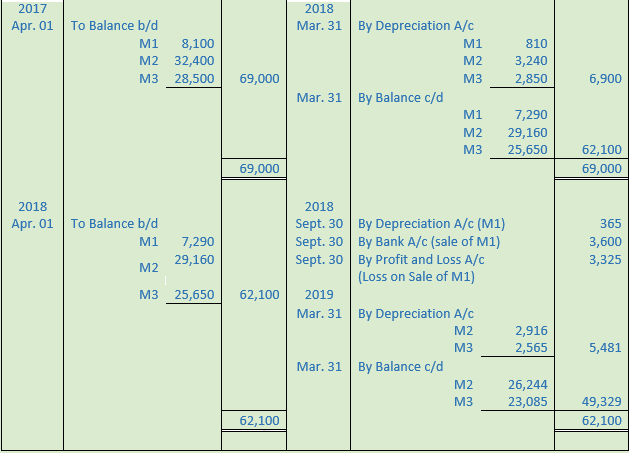

Question 18. A Company, which closes its books on 31st March every year, purchased on 1st July, 2016, machinery costing Rs. 30,000. It purchased further machinery on 1st January, 2017, costing Rs. 20,000 and on 1st October, 2017, costing Rs. 10,000. On 1st April, 2018, one-third of the machinery installed on 1st July, 2016, became obsolete and was sold for Rs. 3,000.

Show how the machinery account would appear in the books of the Company, it being given that machinery was depreciated by Diminishing Balance Method at 10% per annum. What would be the balance of Machinery Account on 1st April, 2019?

Solution 18:

Working Note:-

Calculation of Profit and loss on Sale of assets:-

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

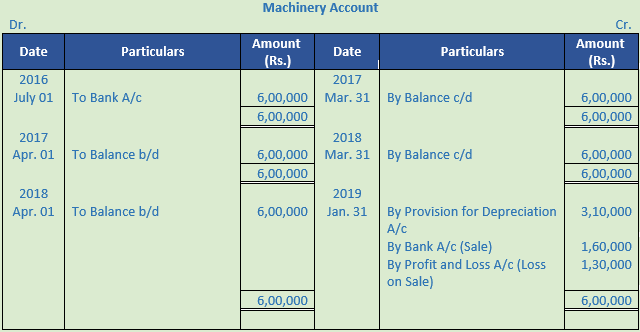

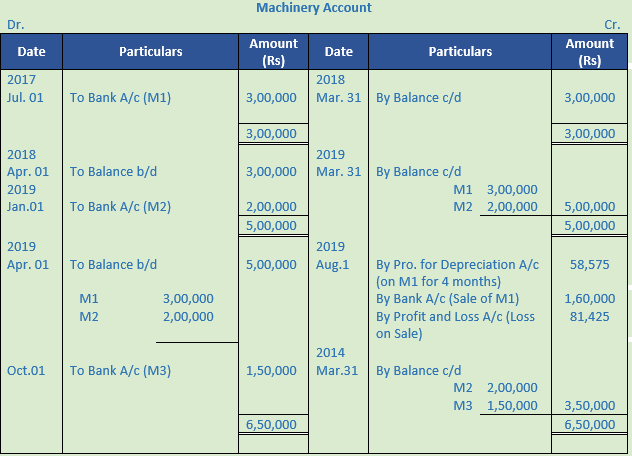

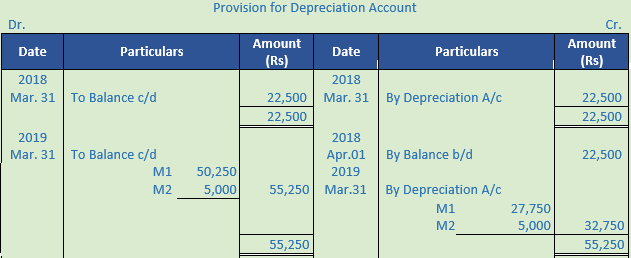

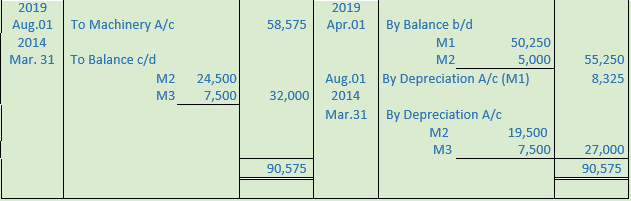

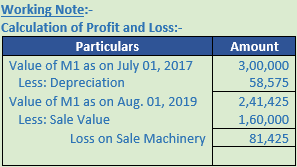

Question 19. On July 1, 2016 Pushpak Ltd. purchased a machinery for Rs. 5,70,000 and paid Rs. 30,000 for its overhauling and installation. Depreciation is provided @ 20% p.a. on Original Cost Method and the books are closed on 31st March every year. The machine was sold on 31st January 2019 for a sum of Rs. 1,60,000. You are required to show the Machinery Account and Provision for Depreciation Account for three years.

Solution 19:

Working Note:-

Value of Machinery = Rs. 5,70,000 + Rs. 30,000 = Rs. 6,00,000

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

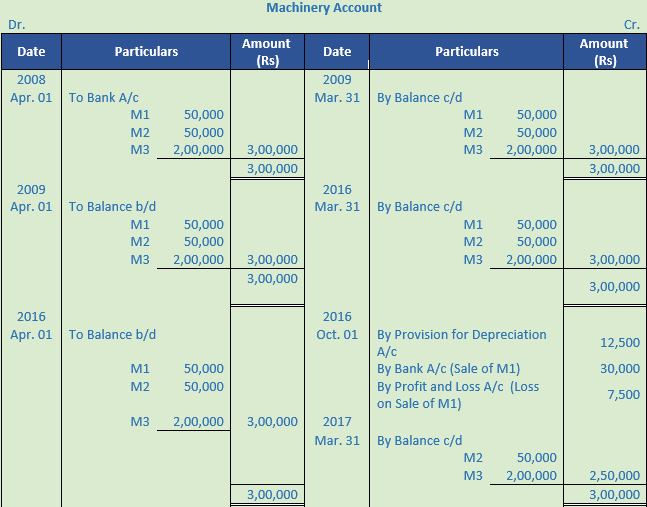

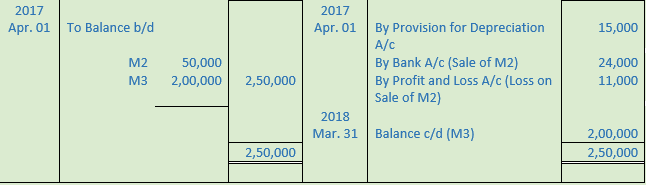

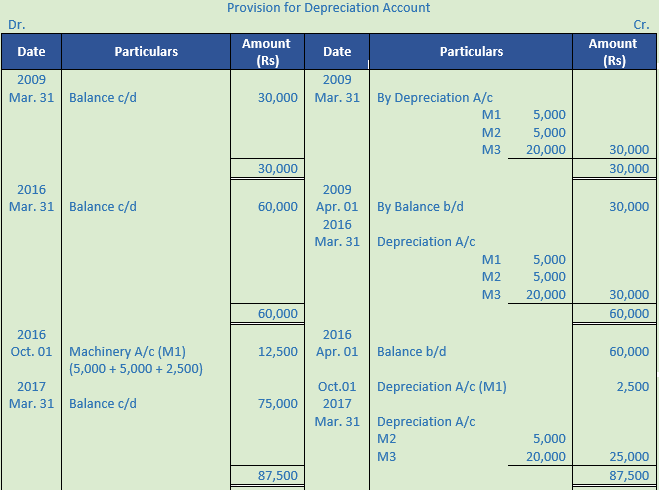

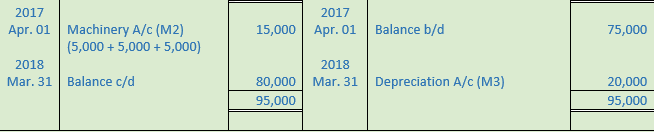

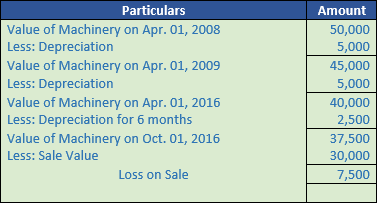

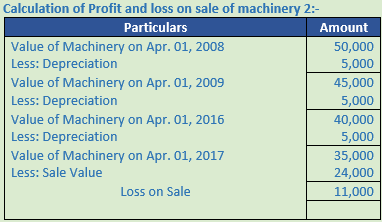

Question 20. On 1st April 2008, a Company purchased 6 machines for Rs. 50,000 each. Depreciation at the rate of 10% p.a. is charged on Straight Line Method. The accounting year of the Company ends on 31st March and the depreciation is credited to a separate 'Provision for Depreciation Account'.

On 1st October, 2016, one machine was sold for Rs. 30,000 and on 1st April, 2017 a second machine was sold for Rs. 24,000.

You are required to prepare Machinery Account and Provision for Depreciation Account for four years ending 31st March, 2018.

Solution 20:

Working Note:-

Value of Machinery 1 = Rs. 5,000 + Rs. 5,000 + Rs. 2,500 = Rs. 12,500

Value of Machinery 2 = Rs. 5,000 + Rs. 5,000 + Rs. 5,000 = Rs. 15,000

Calculation of Profit and loss on sale of machinery 1:-

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

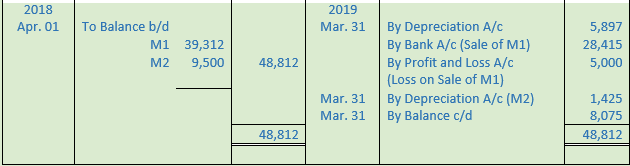

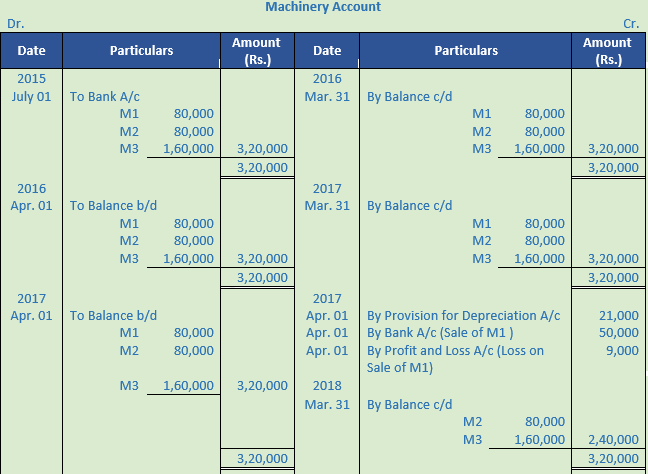

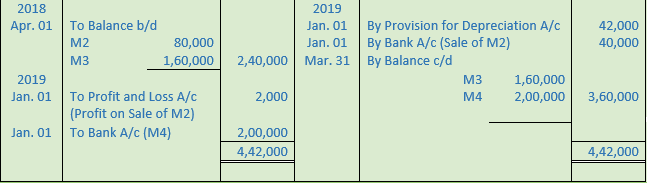

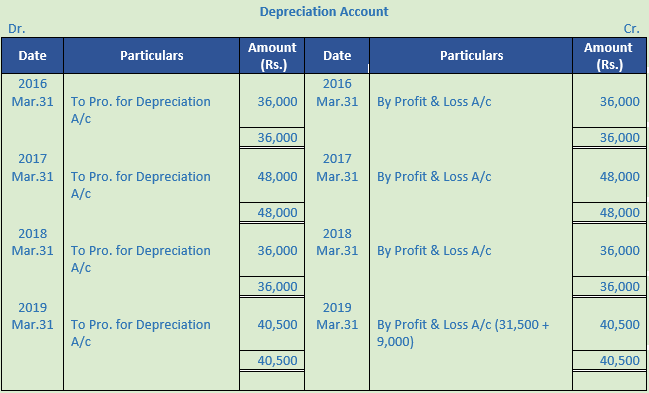

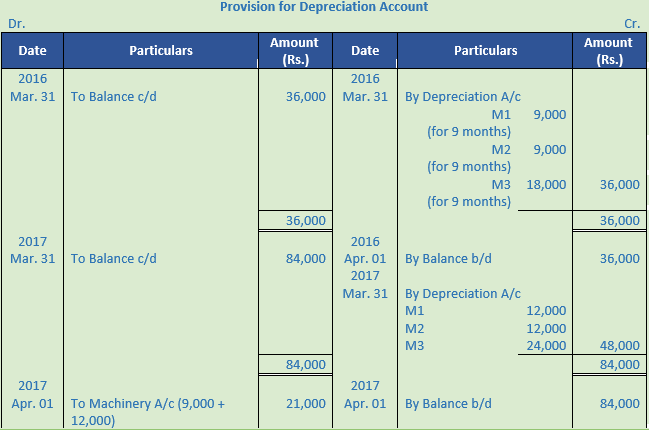

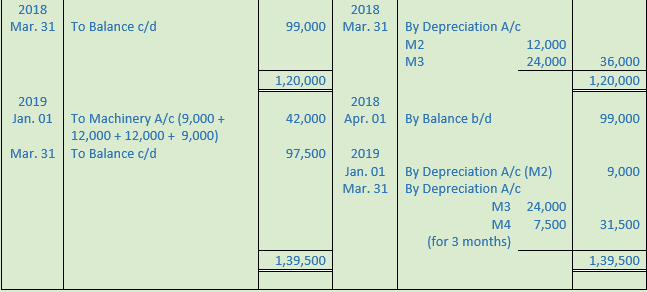

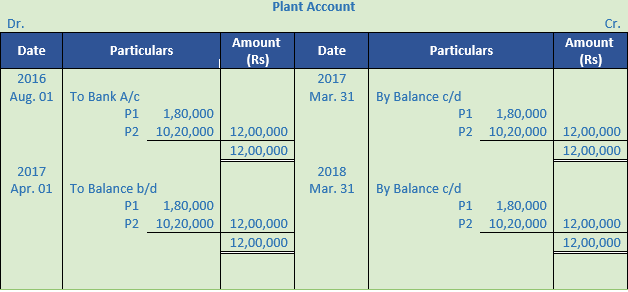

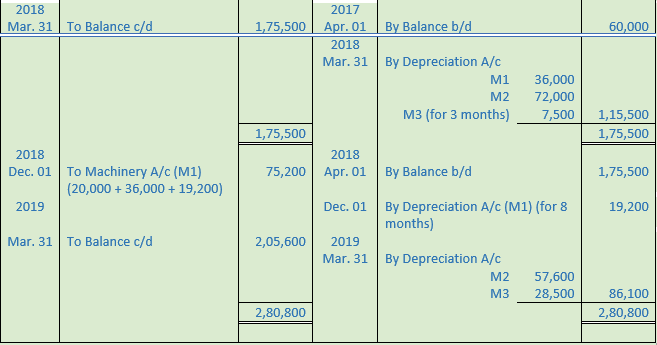

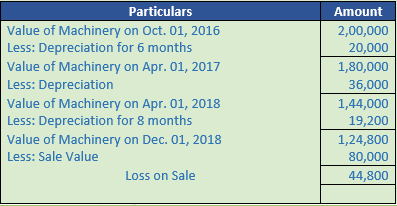

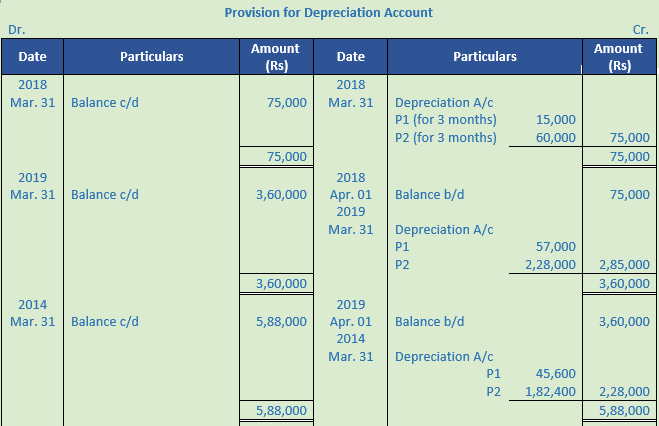

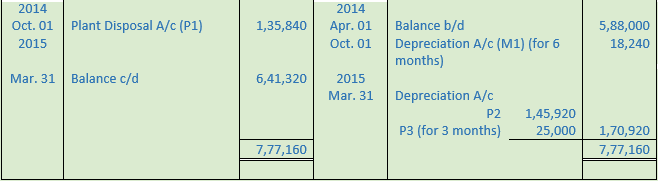

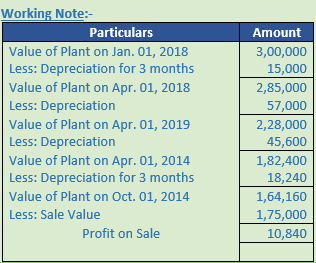

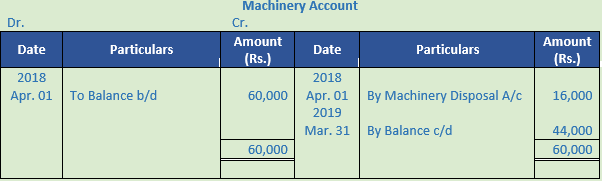

Question 21. On 1st July 2015, ABC Ltd. purchase 4 machines for Rs. 80,000 each. The accounting year of the company ends on 31st March every year. Depreciation is provided at the rate of 15% p.a. on original cost.

On 1st April, 2017 one machine was sold for Rs. 50,000 and on 1st January, 2019 a second machine was sold for Rs. 40,000. Another machine with a higher capacity which cost Rs. 2,00,000 was purchased on 1st January, 2019.

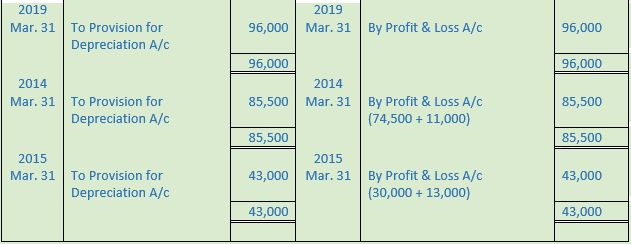

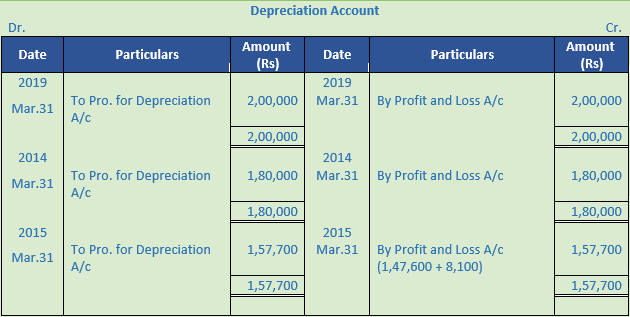

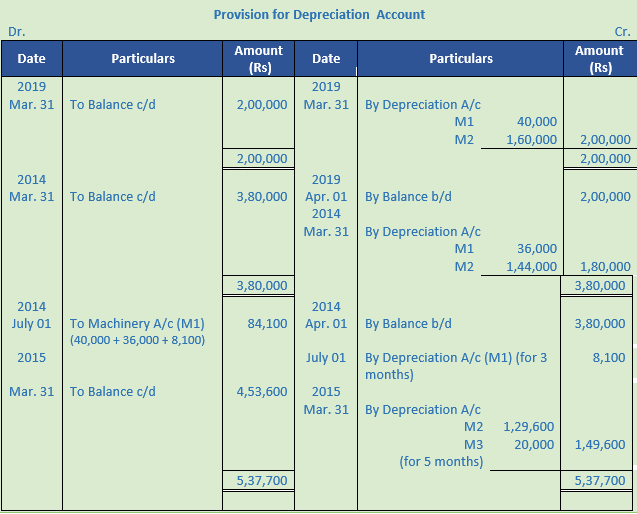

You are required to show: (i) Machinery Account, (ii) Depreciation Account, and (iii) Provision for Depreciation Account for four years ending 31st March, 2019.

Solution 21:

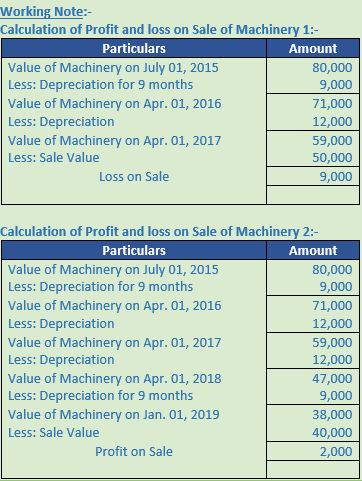

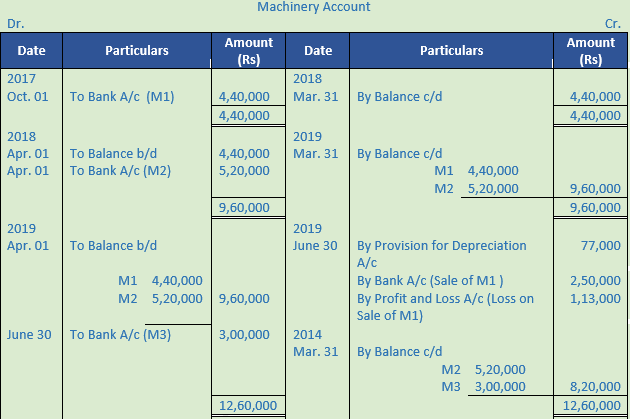

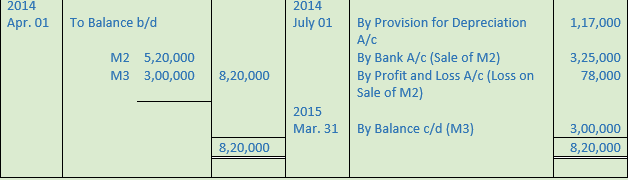

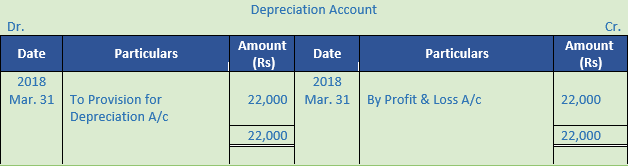

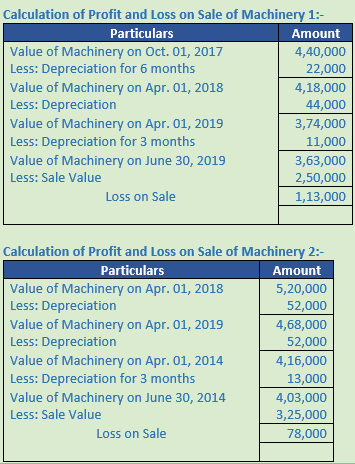

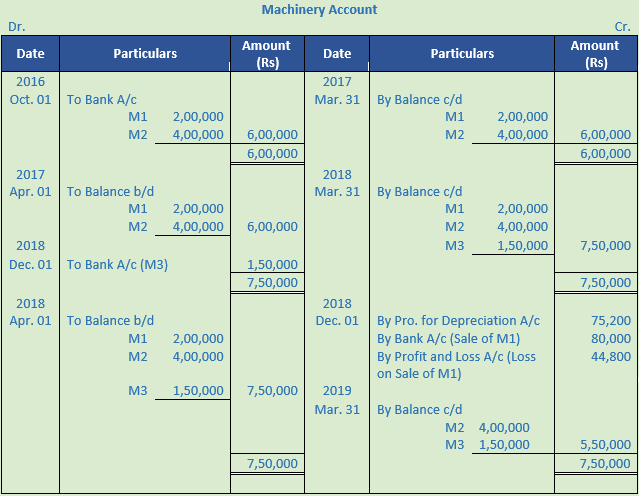

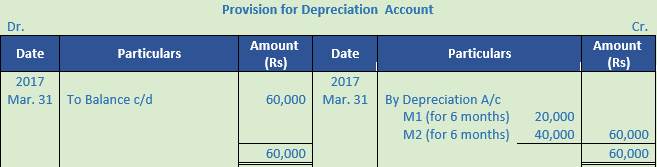

Question 22. X Ltd. which closes its books of account every year on 31st March, purchased on 1st October, 2017 machinery costing Rs. 4,40,000. It purchased further machinery on 1st April, 2018 costing Rs. 5,20,000. On 30th June, 2019, the first machine was sold for Rs. 2,50,000 and on the same date a fresh machine was installed at a cost of Rs. 3,00,000. On 1st July 2014, the second machine purchased on 1st April 2018 was also sold for Rs. 3,25,000.

The company writes off depreciation at 10% p.a. on the Straight Line Method each year. Show the Machinery A/c, Depreciation A/c and Provision for Depreciation A/c for all the four years.

Solution 22:

Working Note:-

Value of Machinery 1 = Rs. 22,000 + Rs. 44,000 + Rs. 11,000 = Rs. 77,000

Value of Machinery 2 = Rs. 52,000 + Rs. 52,000 + Rs. 13,000 = Rs. 1,17,000

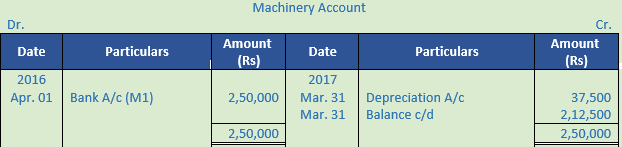

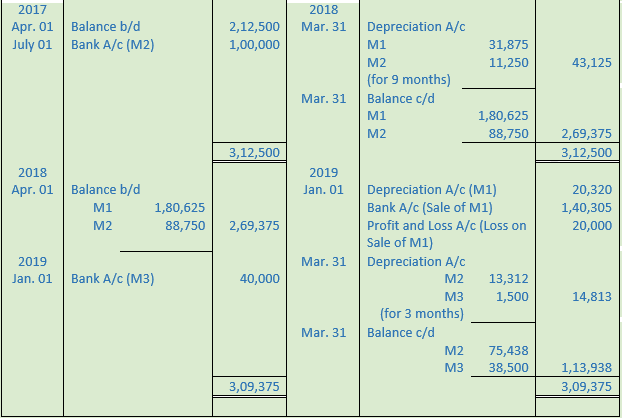

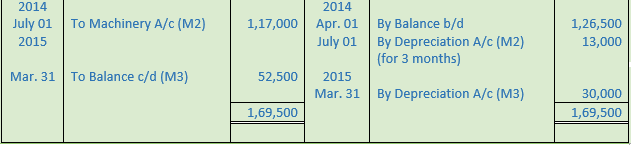

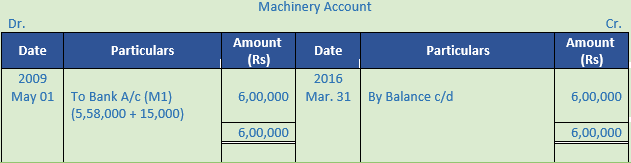

Question 23. A company purchased second-hand machinery on 1st May, 2009 for Rs. 5,85,000 and immediately spent Rs. 15,000 on its erection. On 1st October, 2016, it purchased another machine for Rs. 4,00,000. On 31st July, 2017, it sold off the first machine for Rs. 2,50,000 and bought another for Rs. 4,20,000. On 1st November, 2018, the second machine was also sold off for Rs. 3,00,000. Depreciation was provided on the machinery @ 15% p.a. on Equal Instalment Method.

Show the Machinery Account, Depreciation Account and Provision for Depreciation Account assuming that the books are closed on 31st March every year.

Solution 23:

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

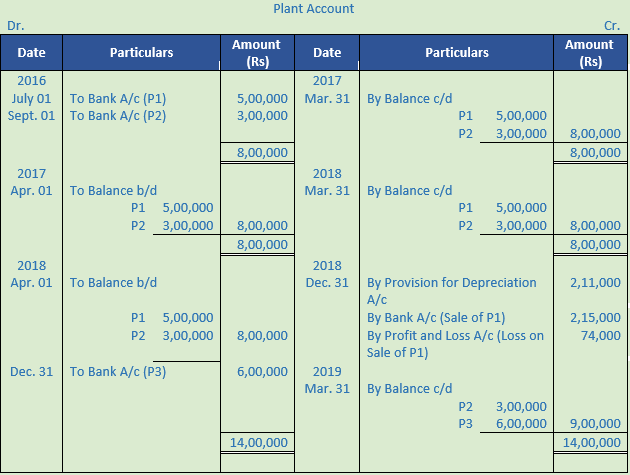

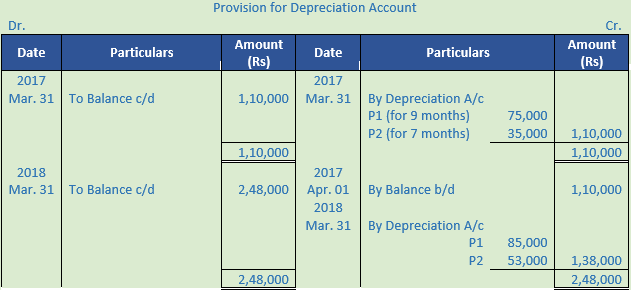

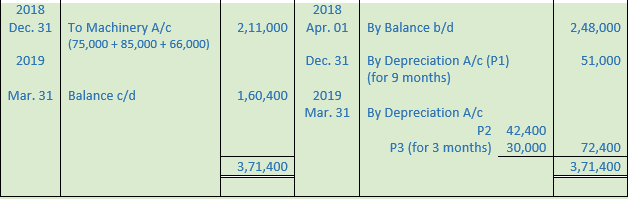

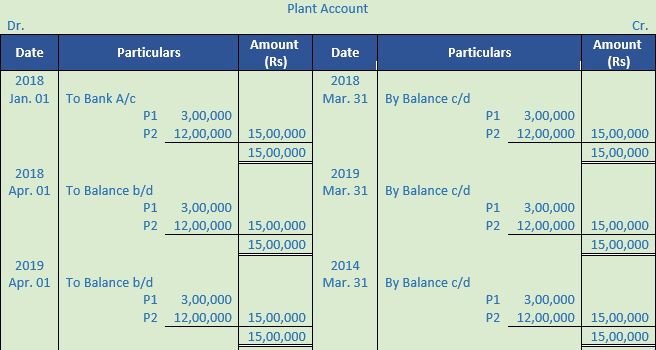

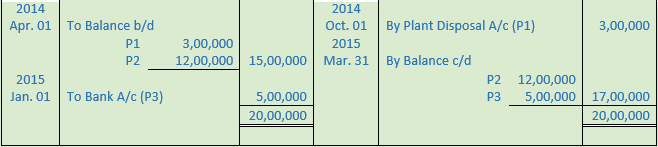

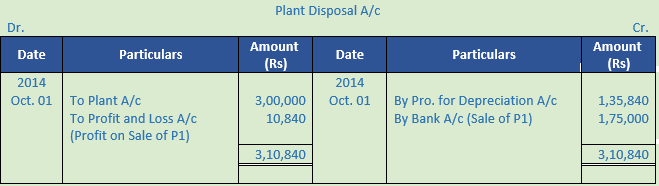

Question 24. X Ltd. purchased a plant on 1st July, 2016 costing Rs. 5,00,000. It purchased another plant on 1st September, 2016 costing Rs. 3,00,000. On 31st December, 2018, the plant purchased on 1st July, 2016 got out of order and was sold for Rs. 2,15,000. Another plant was purchased to replace the same for Rs. 6,00,000. Depreciation is to be provided at 20% p.a. according to Written Down Value Method. The accounts are closed every year on 31st March.

Show the Plant Account and Provision for Depreciation Account.

Solution 24:

Working Note:-

Calculation of Profit and Loss on Sale of Machinery 1:-

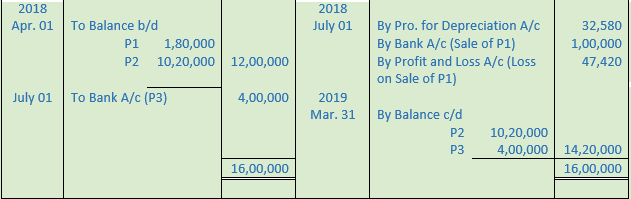

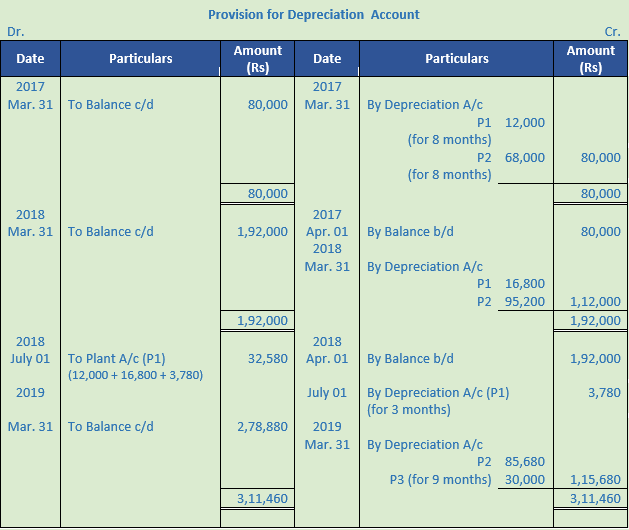

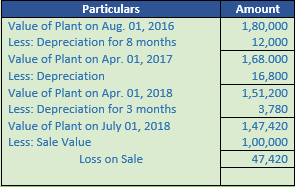

Question 25. On 1st August, 2016, Hindustan Toys Ltd. purchased a plant for Rs. 12,00,000. The firm writes off depreciation at 10% p.a. on the diminishing balance and the books are closed on 31st March each year. On 1st July, 2018, a part of this plant of which the original cost was Rs. 1,80,000 was sold for Rs. 1,00,000 and on the same date a new plant was purchased for Rs. 4,00,000. Show the Plant Account and Provision for Depreciation Account for three years ending 31st March, 2019.

Solution 25:

Working Note:-

Calculation of Profit and Loss on Sale of Plant and Machinery 1:-

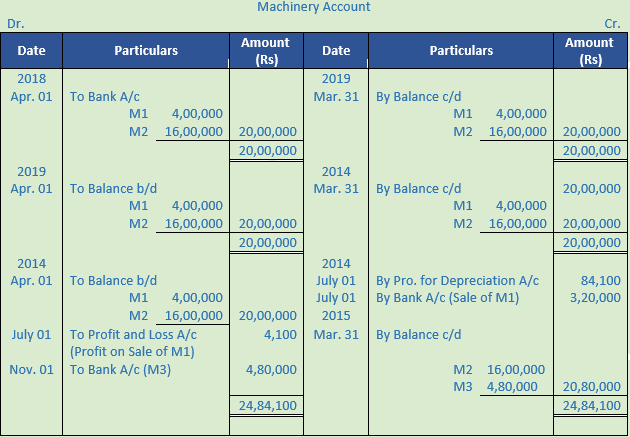

Question 26. On 1st April 2018, Banglore Silk Ltd. purchased a machinery for Rs. 20,00,000. It provides depreciation at 10% p.a. on the Written Down Value Method and closes its books on 31st March every year. On 1st July 2014, a part of the machinery purchased on 1st April 2018 for Rs. 4,00,000 was sold for Rs. 3,20,000. On 1st November 2014, a new machinery was purchased for Rs. 4,80,000. You are required to prepare Machinery Account, Depreciation Account and Provision for Depreciation Account for three years ending 31st March 2015.

Solution 26:

Question 27. Binny Textiles Ltd. which depreciates its machinery at 20% p.a. on diminishing balance method, purchased a machine for Rs. 6,00,000 on 1st October, 2016. It closes its books on 31st March every year. On 1st January, 2018, it purchased another machine for Rs. 1,50,000. On 1st December, 2018, one-third of the machinery purchased on 1st October, 2016 was sold for Rs. 80,000.

You are required to prepare Machinery A/c and Provision for Depreciation A/c for the relevant years.

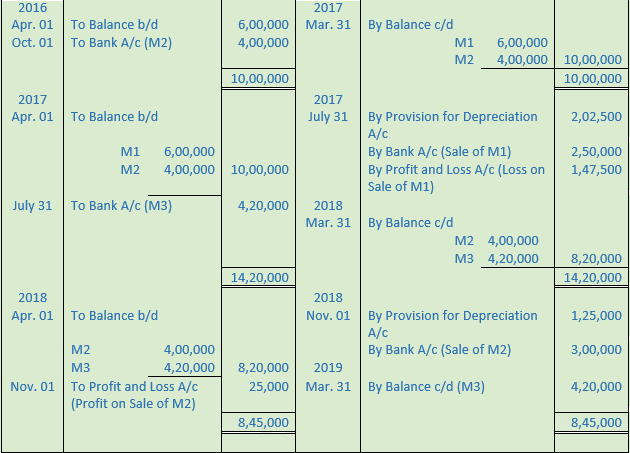

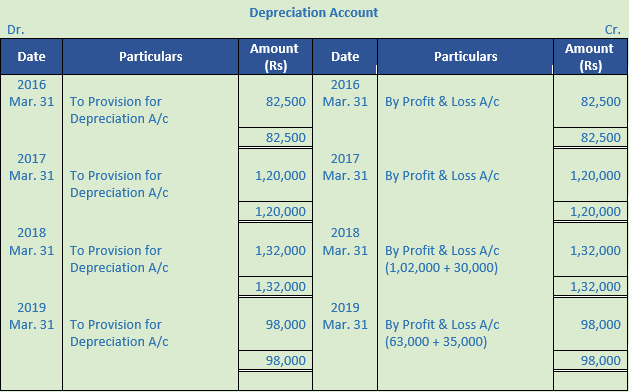

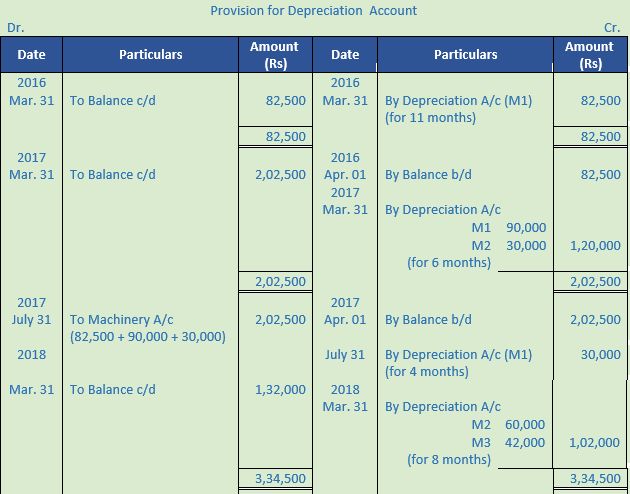

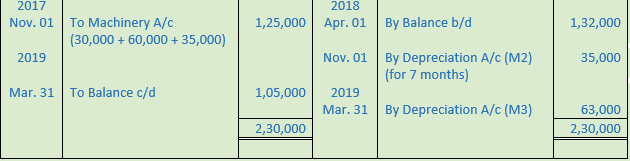

Solution 27:

Working Note:-

Calculation of Profit and Loss on sales of Machinery 1:-

Question 28. The following balances appear in the books of Y Ltd:

Rs.

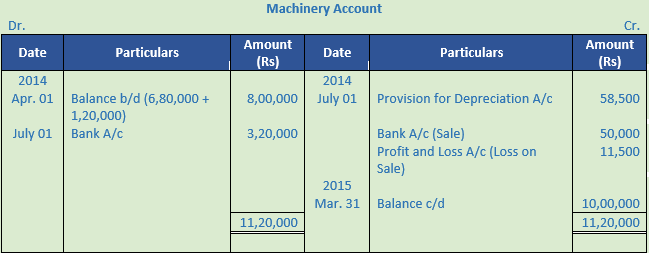

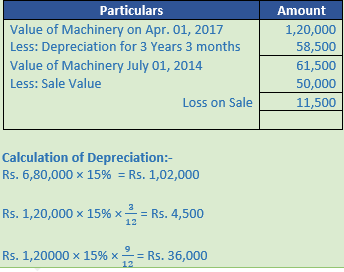

Machinery A/c as on 1-4-2014 8,00,000

Provision for Depreciation A/c as on 1-4-2014 3,10,000

On 1-7-2014, a machinery which was purchased on 1-4-2017 for Rs. 1,20,000 was sold for Rs. 50,000 and on the same date another machinery was purchased for Rs. 3,20,000.

The firm has been charging depreciation at 15% p.a. on Original Cost Method and closes its books on 31st March every year. Prepare the Machinery A/c and Provision for Depreciation A/c for the year ending 31st March 2015.

Solution 28:

Working Note:-

Value of Machinery = Rs. 6,80,000 + Rs. 1,20,000 = Rs. 8,00,000

Calculation of Profit and Loss on Sale of machinery:-

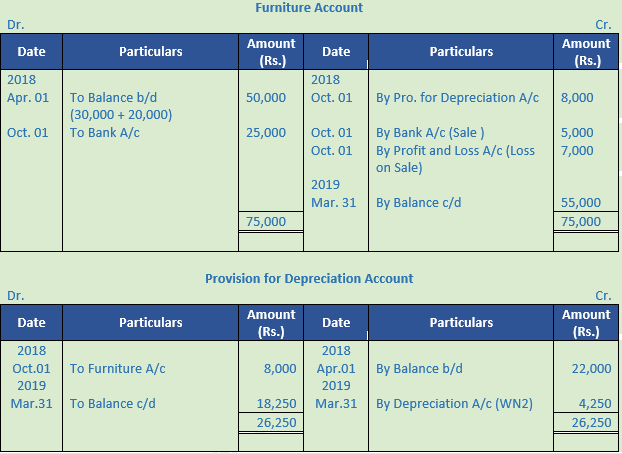

Question 29. On 1st April, 2018, following balances appeared in the books of M/s Krishna Traders:

Rs.

Furniture Account 50,000

Provision for Depreciation on Furniture Account 22,000

On 1st October, 2018 a part of Furniture purchased for Rs. 20,000 on 1st April, 2014 was sold for Rs. 5,000. On the same date a new furniture costing Rs. 25,000 was purchased.

The depreciation was provided @ 10% p.a. on original cost of the asset and no depreciation was charged on the asset in the year of sale. Prepare 'Furniture Account' and 'Provision for Depreciation Account' for the year ending 31st March, 2019.

Solution 29:

Working Note:-

Value of Machinery = Rs. 30,000 + Rs. 20,000 = Rs. 50,000

Calculation of Profit and Loss on Sale of Machinery:-

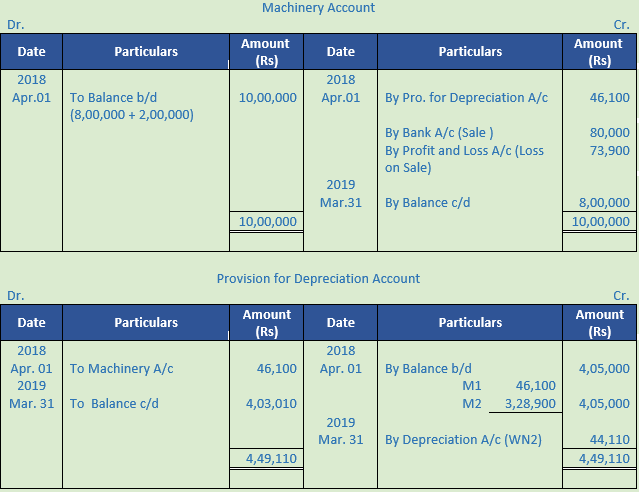

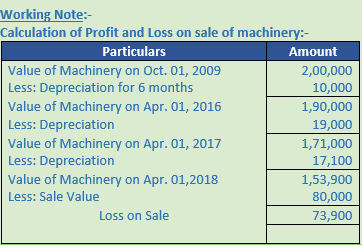

Question 30. Books of Mumbai Chemicals Ltd. showed the following balances on 1st April 2018:

Machinery A/c Rs. 10,00,000

Provision for Depreciation A/c Rs. 4,05,000

On 1st April, 2018, a machine which had a cost of Rs. 2,00,000 on 1st October, 2009 was sold for Rs. 80,000. The firm writes off depreciation @ 10% p.a. under the Reducing Balance Method and its accounts are made up on 31st March each year. You are required to prepare the Machinery A/c and Provision for Depreciation A/c for the year ending 31st March, 2019.

Solution 30:

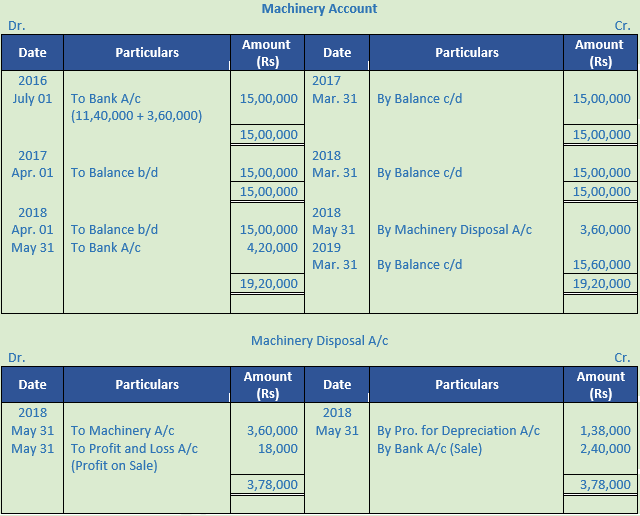

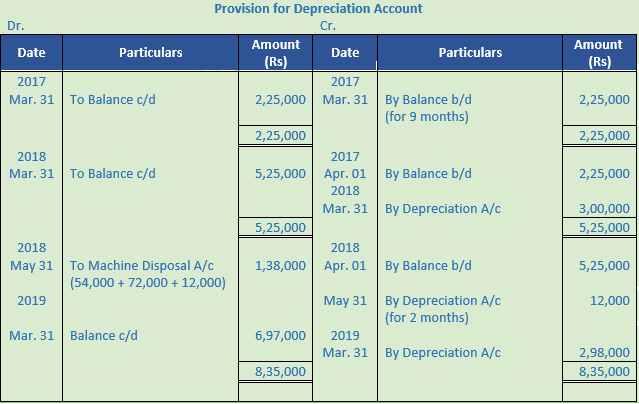

Question 31. On 1st July, 2016, X Ltd. purchased a machinery for Rs. 15,00,000. Depreciation is provided @ 20% p.a. on the original cost of the machinery and books are closed on 31st March each year. On 31st May, 2018, a part of this machine purchased on 1st July 2016 for Rs. 3,60,000 was sold for Rs. 2,40,000 and on the same date new machinery was purchased for Rs. 4,20,000. You are required to prepare (a) Machinery Account, (b) Provision for Depreciation Account, and (c) Machinery Disposal Account.

Solution 31:

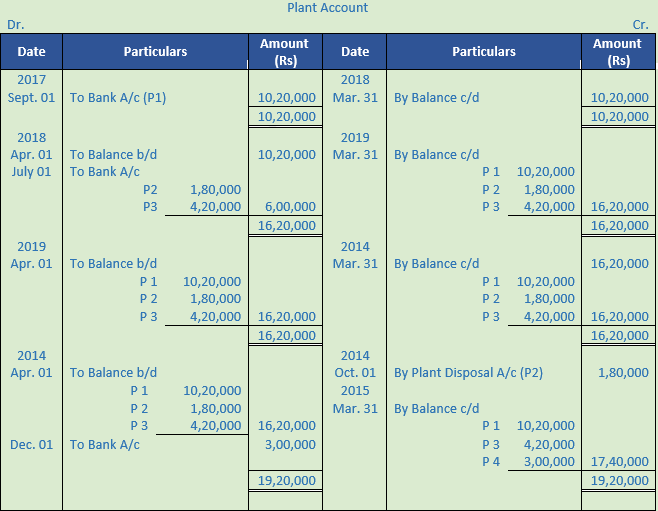

Question 32. On 1st September 2017, Gopal Ltd. purchased a plant for Rs. 10,20,000. On 1st July 2018 another plant was purchased for Rs. 6,00,000. The firm writes off depreciation @ 10% p.a. on original cost and its accounts are closed every year on 31st March. On 1st October 2014, a part of the second plant purchased on 1st July 2018 for Rs. 1,80,000 was sold for Rs. 1,10,000. On 1st December 2014, another plant was purchased for Rs. 3,00,000.

Prepare Plant Account, Provision for Depreciation Account and Plant Disposal Account.

Solution 32:

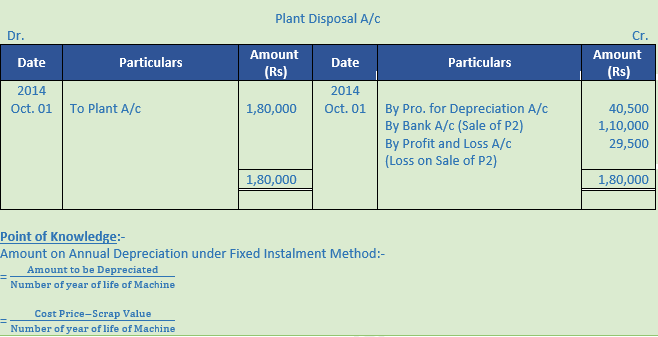

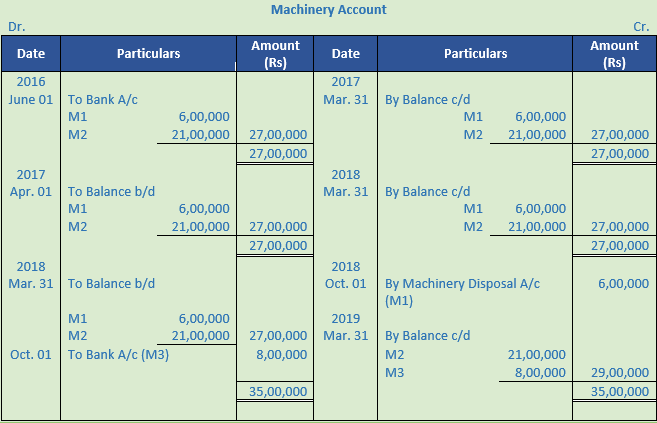

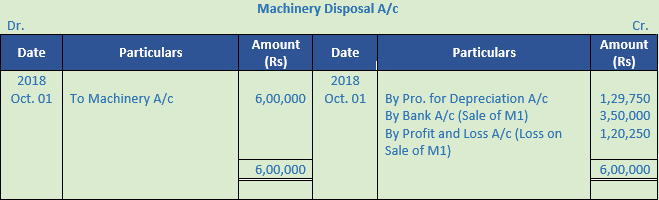

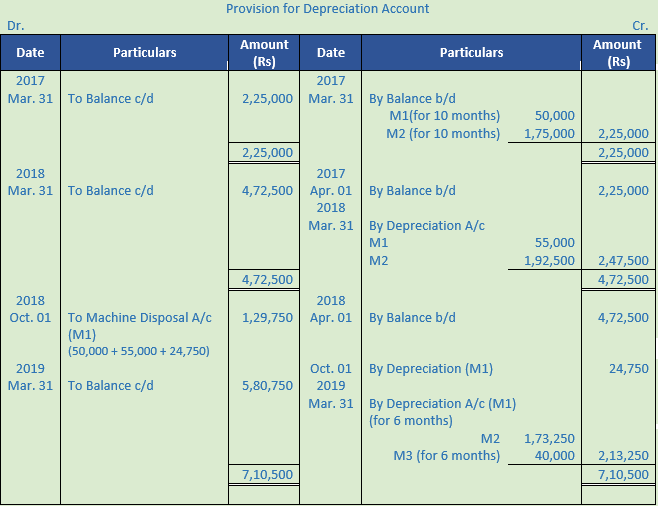

Question 33. On 1st June, 2016, Kedarnath Ltd. purchased a machinery for Rs. 27,00,000. Depreciation is provided @ 10% p.a. on diminishing balance method and the books are closed on 31st March each year. On 1st October, 2018, a part of the machinery purchased on 1st June, 2016 for Rs. 6,00,000 was sold for Rs. 3,50,000 and on the same date another machinery was purchased for Rs. 8,00,000. You are required to show (i) Machinery A/c, (ii) Provision for Dep. A/c, and (iii) Machinery Disposal A/c.

Solution 33:

Working Note:-

Calculation of Profit and loss on Sale of machinery:-

Point of Knowledge:-

Amount on Annual Depreciation under Straight Line Method:-

![]()

Question 34. On 1st Jan. 2018, Panjim Dryfruits Ltd. bought a plant for Rs. 15,00,000. The company writes off depreciation @ 20% p.a. on Written Down Value Method and closes its books on 31st March every year. On 1st Oct. 2014, a part of the plant purchased on 1st Jan. 2018 for Rs. 3,00,000 was sold for Rs. 1,75,000. On 1st Jan. 2015 a fresh plant was purchased for Rs. 5,00,000. Prepare Plant A/c, Provision for Dep. A/c and Plant Disposal A/c.

Solution 34:

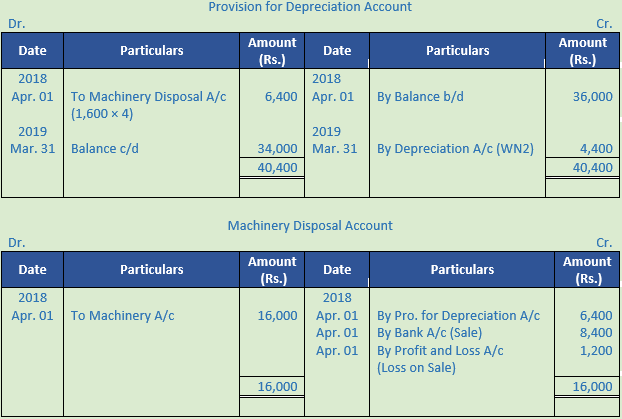

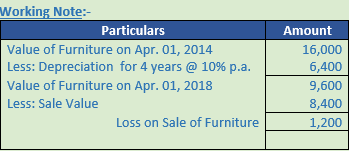

Question 35. The following balances appear in the books of M/s Amrit:

1st April, 2018 Machinery A/c 60,000

1st April, 2018 Provision for depreciation A/c 36,000

On 1st April, 2018, they decided to dispose off a machinery for Rs. 8,400 which was purchased on 1st April, 2014 for Rs. 16,000.

You are required to prepare Machinery A/c, Provision for Depreciation A/c and Machinery Disposal A/c for 2018-19. Depreciation was charged at 10% p.a on original cost method.

Solution 35:

Point of Knowledge:-

(i) Asset Disposal Account: In case of asset being sold. a new account named ‘Asset Disposal Account’ is opened in the ledger for the purpose of calculating profit or loss on the sale of an asset. Journal entries for sale or disposal of asset will depend upon the method of recording depreciation.

(ii) Written Down Value/Diminishing Balance/Reducing Balance Method of Charging Depreciation: Under this method, depreciation is charged at a fixed rate on the reducing balance or cost less depreciation every year. A fixed rate on the written down value of the asset is charged as depreciation every year the expected useful life of the asset.

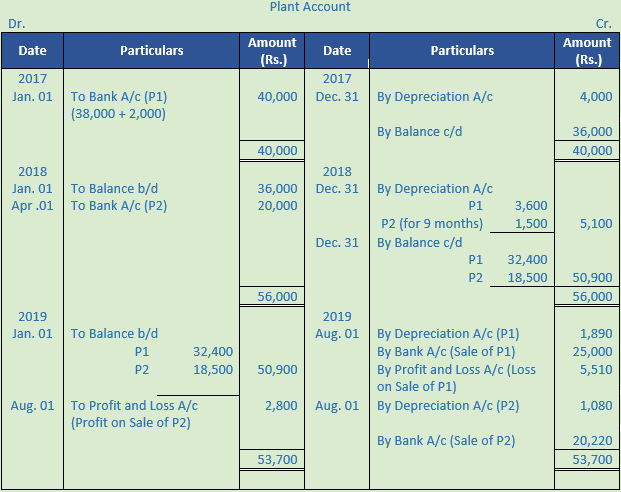

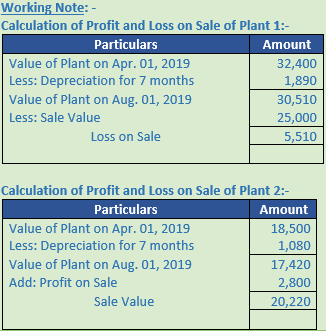

Question 36. A limited company purchased on 01-01-2017 a plant for Rs. 38,000 and spent Rs. 2,000 for carriage and brokerage. On 01-04-2018 it purchased additional plant costing Rs. 20,000. On 01-08-2019 the plant purchased on 01-01-2017 was sold for Rs. 25,000. On the same date, the plant purchased on 01-04-2018 was sold at a profit of Rs. 2,800. Depreciation is provided @10% per annum on diminishing balance method every year. Accounts are closed on 31st December every year. Show the plant A/c for 3 years.

Solution 36:

Question 37. A Limited purchased a machine on 1st July 2017 for Rs. 3,00,000 and on 1st January 2019 bought another machinery for Rs. 2,00,000. On 1st August 2019 machine bought in 2017 was sold for Rs. 1,60,000. Another machine was bought for Rs. 1,50,000 on 1st October 2019. It was decided to provide depreciation @ 10% p.a. on written down value method assuming books are closed on 31st March each year. Prepare Machinery Account and Provision for depreciation account for 3 years.

Solution 37:

Point of Knowledge:-

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

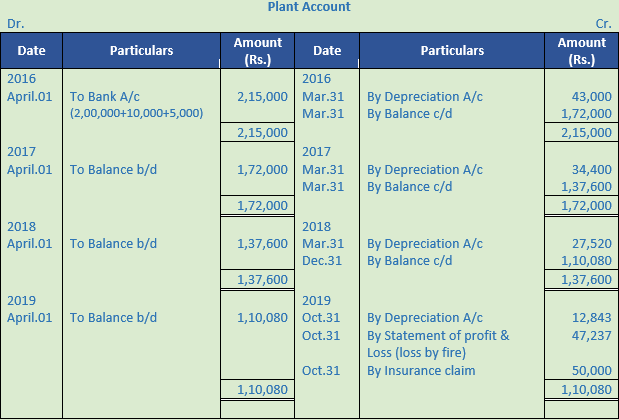

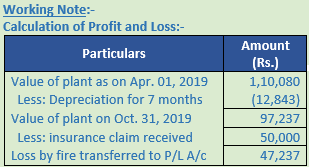

Question 38. On April 01, 2016 Jain & Sons purchased a second hand plant costing Rs. 2,00,000 and spent Rs. 10,000 on its overhauling. It also spent Rs. 5,000 on transportation and installation of the plant. It was decided to provide for depreciation @ 20% on written down value. The plant was destroyed by fire on Oct. 31, 2019 and an insurance claim of Rs. 50,000 was admitted by the insurance company. Prepare plant account assuming that the company closes its books on March 31, every year.

Solution 38:

Point of Knowledge:-

(i) Asset Disposal Account: In case of asset being sold. a new account named ‘Asset Disposal Account’ is opened in the ledger for the purpose of calculating profit or loss on the sale of an asset. Journal entries for sale or disposal of asset will depend upon the method of recording depreciation.

(ii) Written Down Value/Diminishing Balance/Reducing Balance Method of Charging Depreciation: Under this method, depreciation is charged at a fixed rate on the reducing balance or cost less depreciation every year. A fixed rate on the written down value of the asset is charged as depreciation every year the expected useful life of the asset.