Read DK Goel Class 11 Accountancy Solutions for Chapter 13 Ledger below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 13 Ledger should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 13 Ledger DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 13 Ledger in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 13 Ledger Class 11 Accountancy

Short Answer Question

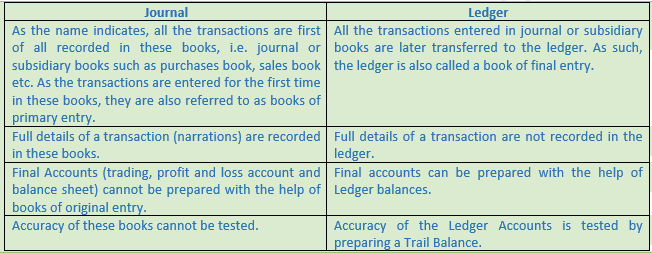

Question 1. Distinguish between Journal and Ledger.

Solution 1:

Question 2. Enumerate four advantages of Ledger.

Solution 2:

Below are the advantages of ledger:-

(1) All accounts are opened on separate pages in this book. Hence, all the transactions pertaining to an account are collected at one place in the ledger.

(2) A trail balance can be prepared with the help of ledger balances which helps in ascertaining the arithmetical accuracy of the accounts.

(3) A trading and profit and loss account can only be prepared with the help of ledger balances.

(4) A balance sheet can also be prepared with the help of ledger balances which depicts the financial position of the business.

Question 3. What are the rules of posting in the Ledger?

Solution 3:

Below are the rules of posting in the ledger:-

(i) All transactions relating to an account should be entered at one place. Two separate accounts should no the opened for posting transactions relating the same account.

(ii) The word ‘To’ is used before the accounts which appear on the debit side of a account. Similarly, the word ‘By’ is used before the accounts which appear on the credit side of an account.

(iii) If an account has been debited in the Journal entry, the posting in the ledger should also be made on the debit side of such account. In the particulars columns, the name of the other account which has been credited in the journal entry should be written for reference.

(iv) If an account has been credited in the Journal entry, the posting in the ledger should also be made on the credit side of such account. In the particulars columns, the name of the other account which has been debited in the journal entry should be written for reference.

(v) Similar amount which has been posted on the debit side of an account should also be posted on the credit side of another account.

Question 4. What are the purposes of posting J.F. number at the time entries are posted to the accounts.

Solution 4: Journal Folio (J.F.) Column in the ledger records Page No. of the journal from which the posting to the Ledger has taken place. Purpose of posting J.F. number is that it provides a ready reference for tracing the page of journal from where the entry has been posted.

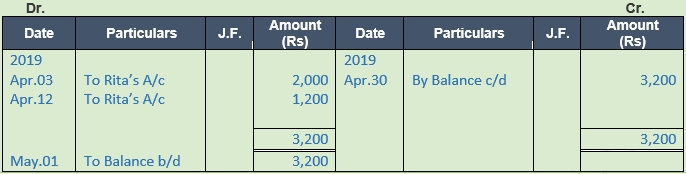

Question 5. Explain the procedure of balancing the personal accounts.

Solution 5:

An Account is balanced like we have to add the bigger side either debit or credit whichever may be and write down the bigger one in the parallel column. The debit column if bigger than the credit column. The difference is written on the credit side as 'By Balance c/d'. The totals are then entered in the two columns opposite one another and then on the debit side, the balance is written as 'To Balance b/d' to show the debit balance in hand in the beginning of the next period or vice versa for the credit balance.

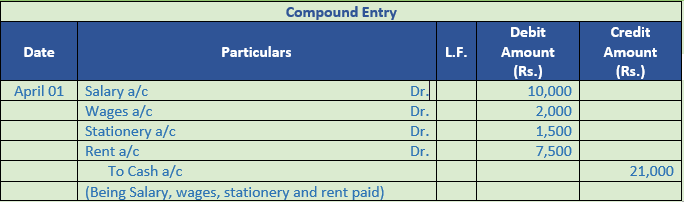

Question 6. Prepare a Compound Entry with the help of imaginary figures and show in posting.

Solution 6:

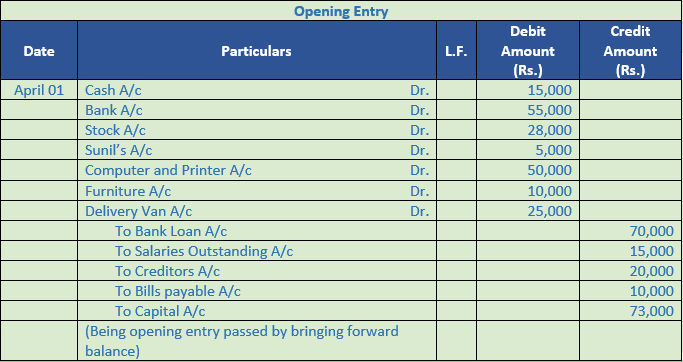

Question 7. Prepare on Opening Entry with the help of imaginary figures and show its posting.

Solution 7:

Question 8. Prepare a Purchase Book with at least two in it and show its posting.

Solution 8:

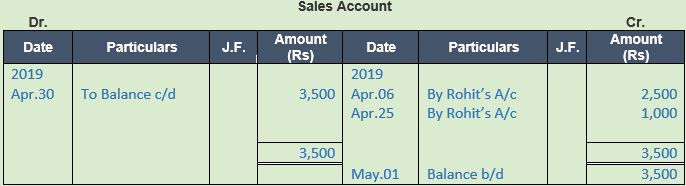

Question 9. Prepare a Sales Book with at least two items in it and show its posting.

Solution 9:

Numerical Questions

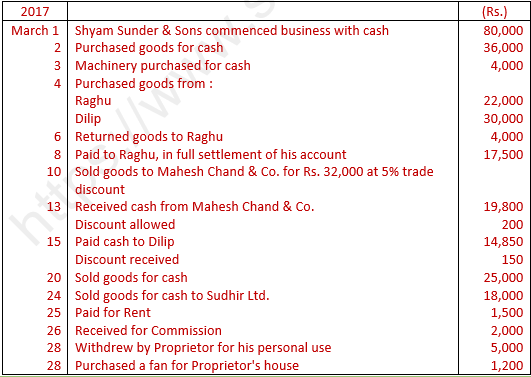

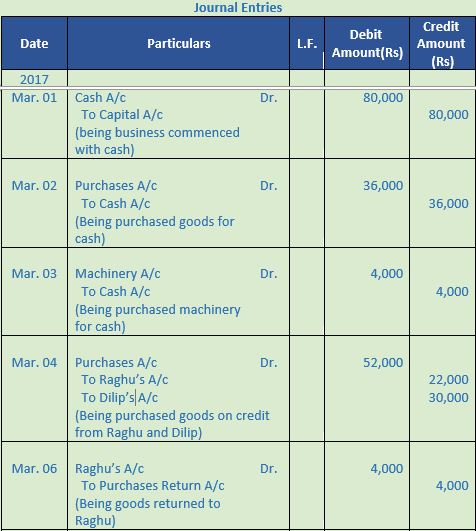

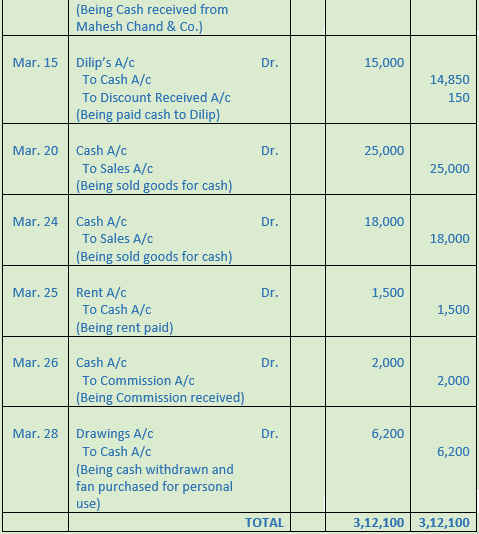

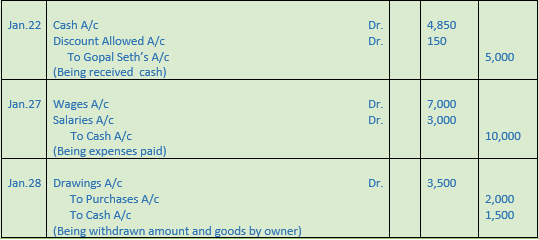

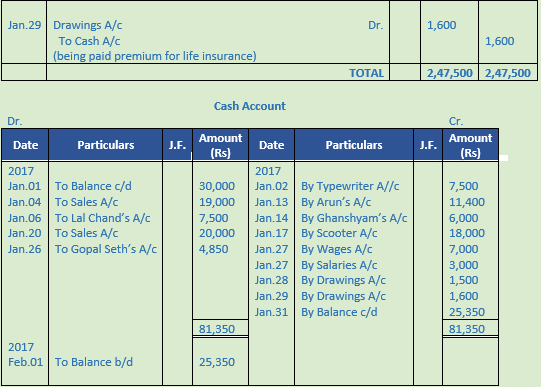

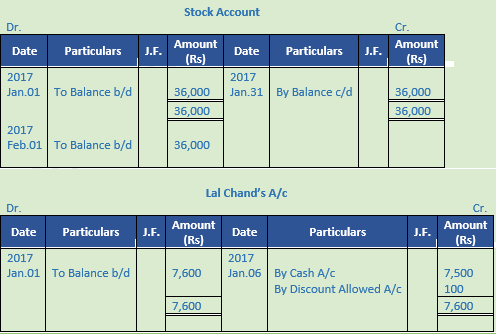

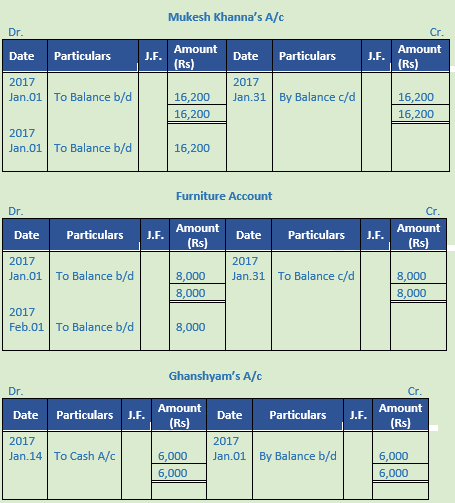

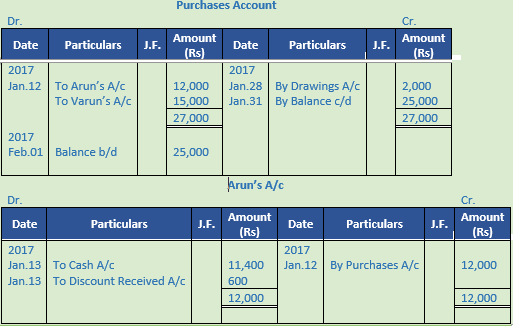

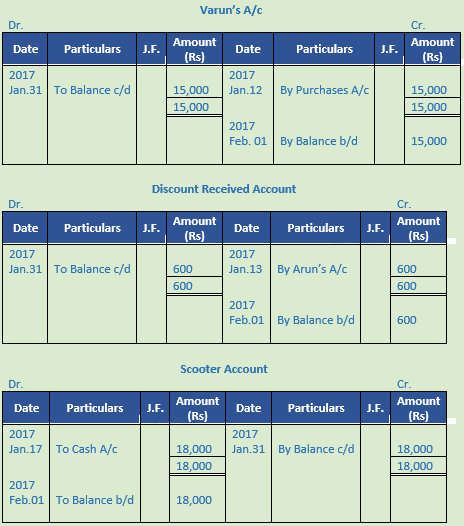

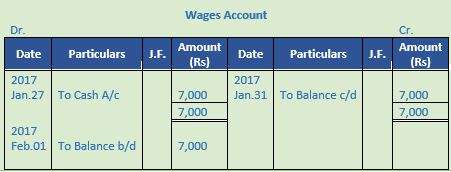

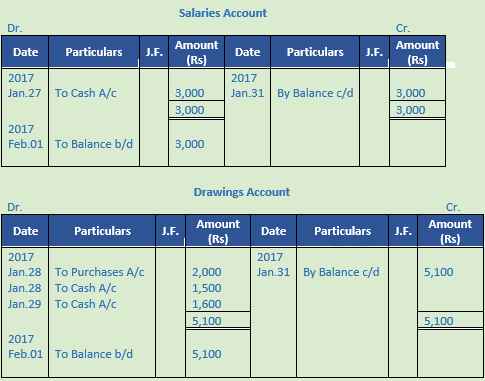

Question 1. Journalise the following transactions, post them into Ledger, balance the accounts and prepare a Trial Balance :−

Solution 1:

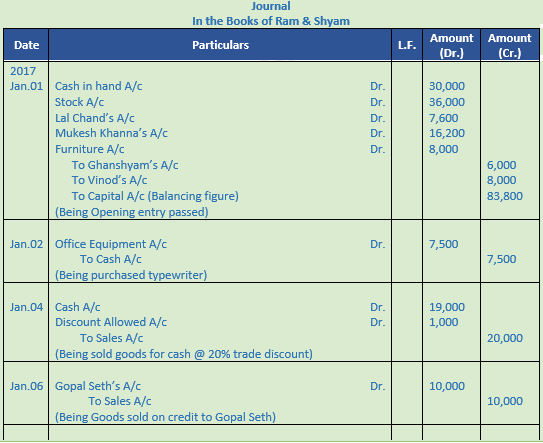

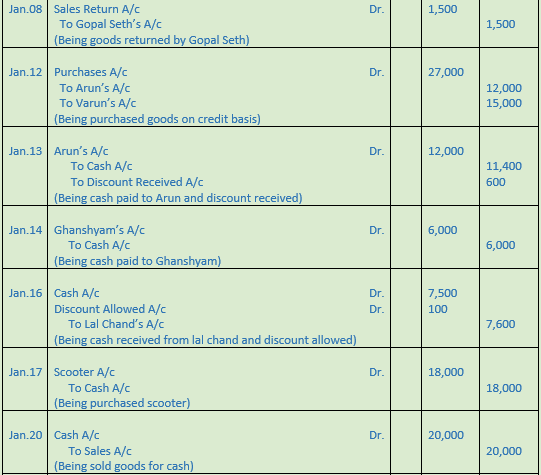

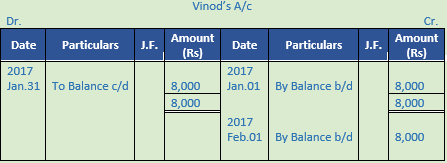

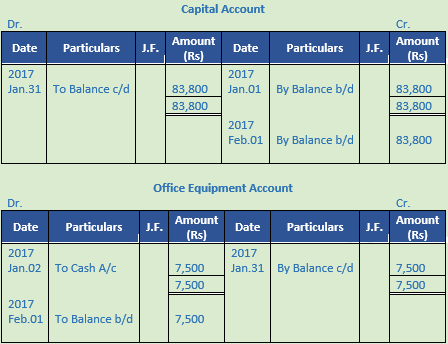

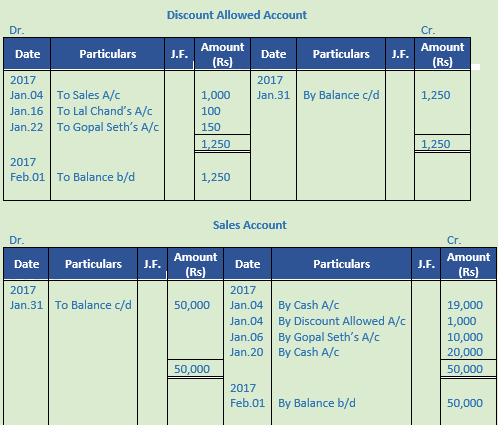

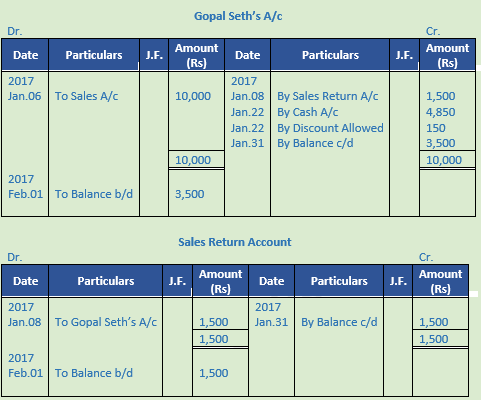

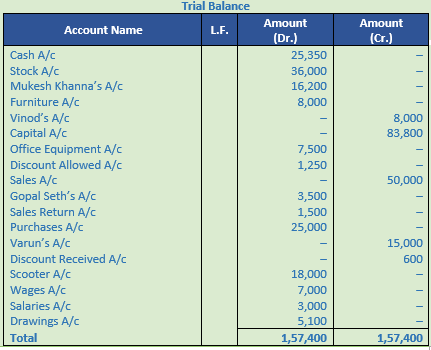

Question 2. Following balances appeared in the books of Ram & Shyam on January 1, 2017 :−

Assets : Cash in hand Rs. 30,000; Stock Rs. 36,000; Lal Chand Rs. 7,600; Mukesh Khanna Rs. 16,200; Furniture Rs. 8,000.

Liabilities : Ghanshyam Rs. 6,000; Vinod Rs. 8,000.

Following transactions took place during Jan. 2017 :−

Journalise the above transactions, post them into Ledger, balance them and prepare a Trial Balance.

Solution 2:

Point of Knowledge:-

A Cash Account is balanced like any other account. The debit column is always bigger than the credit column. The difference is written on the credit side as 'By Balance c/d'. The totals are then entered in the two columns opposite one another and then on the debit side, the balance is written as 'To Balance b/d' to show the cash balance in hand in the beginning of the next period.

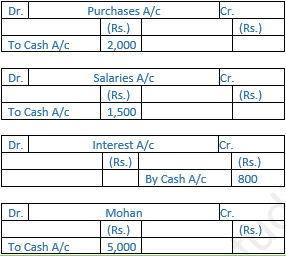

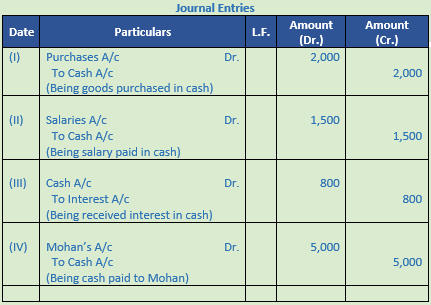

Question 3. Prepare Journal Entries of the following postings :-

Solution 3:

Point of Knowledge:-

In an account, transactions of one nature are posted or summarized. All the accounts put together constitute a 'Ledger'. A Ledger may be defined as a "book or register which contains, in a summarized and classified form, a permanent record of all transactions." It is the most important book of accounts, since, the Trial Balance is drawn from it and from the Trial Balance, and Financial Statements are prepared. Hence, the Ledger is called the Principal Book.

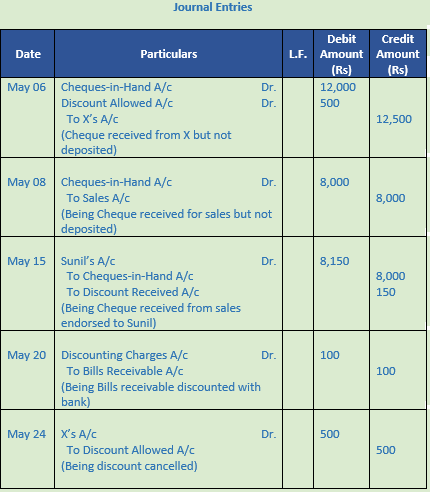

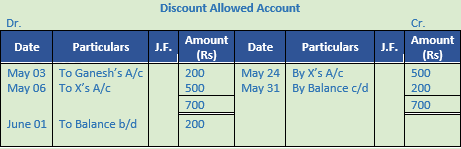

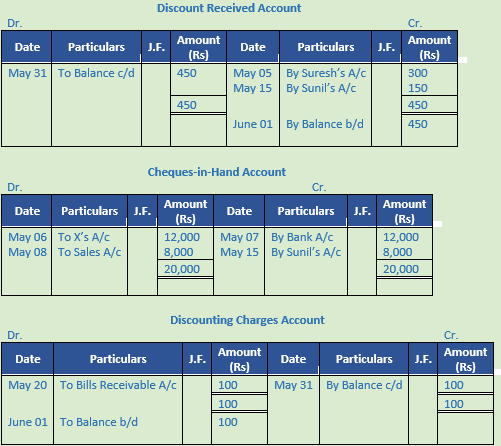

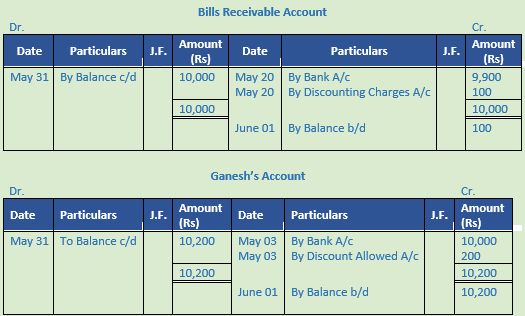

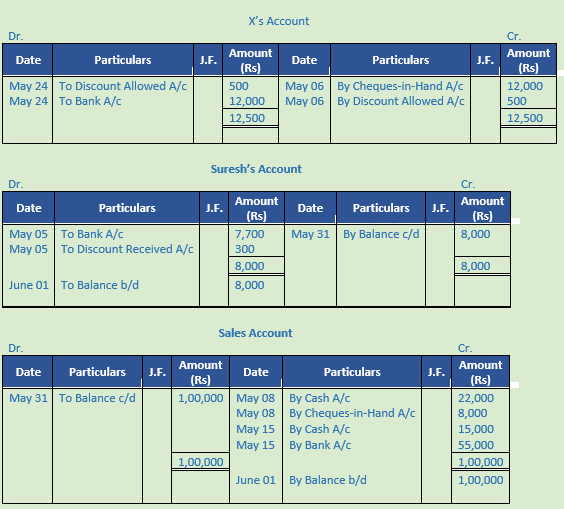

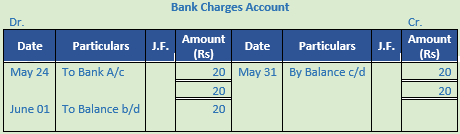

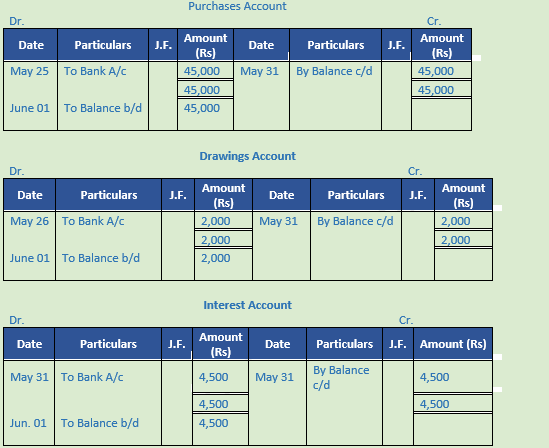

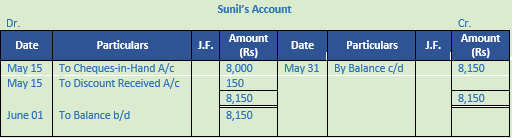

Question 4. Enter the following transactions in a Double Column Cash Book and Journal Proper and post them into Ledger:-

May 1 Balance of Cash in Hand Rs. 12,400; Bank Overdraft Rs. 36,000.

3 Direct deposit by Mr. Ganesh in our bank account Rs. 10,000. Discount allowed Rs. 200.

5 Issued a cheque of Rs. 7,700 to Mr. Suresh in full settlement of his account of Rs. 8,000.

6 Received a cheque from X for Rs. 12,000. Discount allowed Rs. 500. This cheque was deposited into bank on 7th May.

8 Received Cash Rs. 22,000 and cheque of Rs. 8,000 for cash sale.

12 Cash sale Rs. 70,000 of which Rs. 55,000 banked.

15 Cheque received on 8th May endorsed to Mr. Sunil. Discount received Rs. 150.

20 Discounted a B/R of Rs. 10,000 at 1% through bank.

24 Cheque received from X dishonoured, Bank debits Rs. 20 in respect of bank charges.

25 Purchased goods for Rs. 50,000 at a trade discount of 10%. Payment was made in cash.

2 Withdrew from bank Rs. 10,000 for office use and Rs. 2,000 for personal use.

31 Interest debited by Bank Rs. 4,500.

Solution 4:

Point of Knowledge:-

1. Identify in the Ledger the account to be debited.

2. Enter the date of the transaction in the 'Date' column on the debit side of the account.

3. Write the name of the account which has been credited in the respective entry in the 'Particulars' column on the debit side of the amount as 'To (name of account credited)'.

4. Record the page number of the Journal where the entry exists in the Journal folio (J,F.) column.

5. Enter the relevant amount in the 'Amount' column on the debit side.

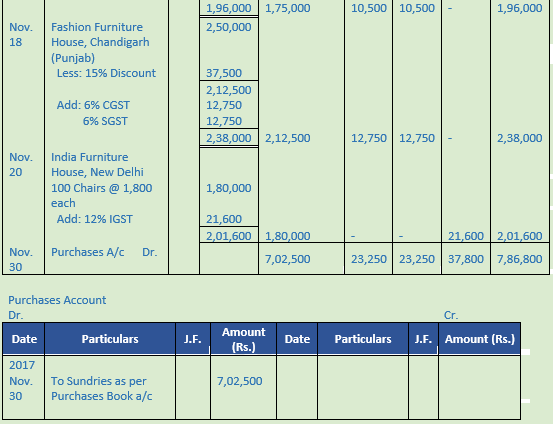

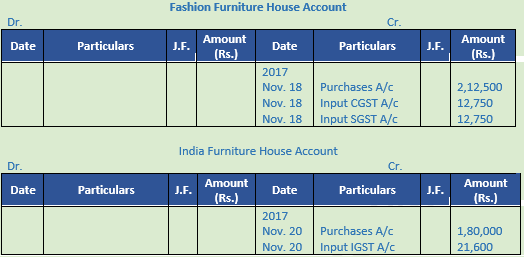

Question 5. Record the following transaction in the Purchases Book of Modern Furniture House, New Delhi assuming CGST @ 6% and SGST @ 6% and post it into Ledger:

Solution 5: Purchases Book of Modern Furniture House, New Delhi

Point of knowledge:-

- Identify in the Ledger the account to be debited.

- Enter the date of the transaction in the 'Date' column on the debit side of the account.

- Write the name of the account which has been credited in the respective entry in the 'Particulars' column on the debit side of the amount as 'To (name of account credited)'.

- Record the page number of the Journal where the entry exists in the Journal folio (J,F.) column.

- Enter the relevant amount in the 'Amount' column on the debit side.

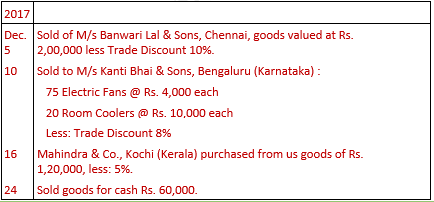

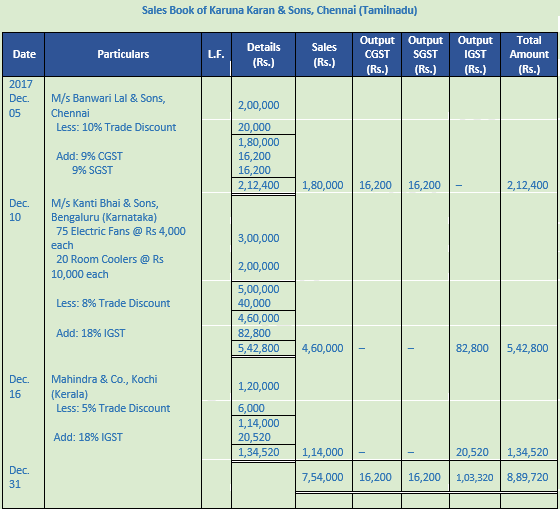

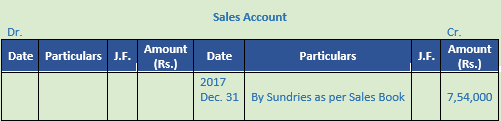

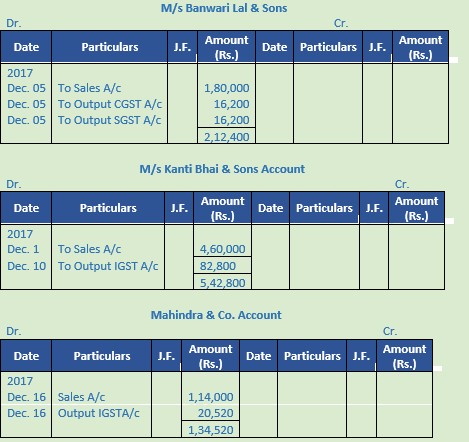

Question 6. Record the following transaction in the Sales Book of Karunakaran & Sons, Chennai (Tamilnadu) assuming CGST @ 90% and SGST @ 9% and post them into Ledger :-

Solution 6:

Point of knowledge:-

- Identify in the Ledger the account to be credited.

- Enter the date of the transaction in the 'Date' column on the credit side of the account.

- Write the name of the account which has been debited in the respective entry in the 'Particulars' column on the credit side of the account as 'By (name of account debited)'.

- Record the page number of the Journal where the entry exists in the Journal folio (J.F.) column.

- Enter the relevant amount in the 'Amount' column on the credit side.

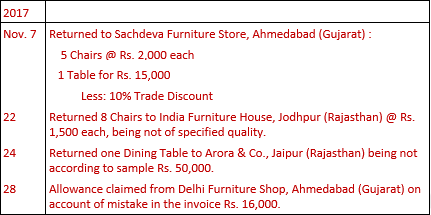

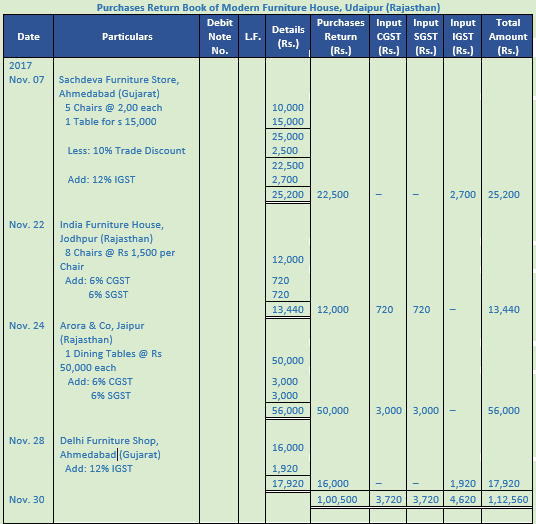

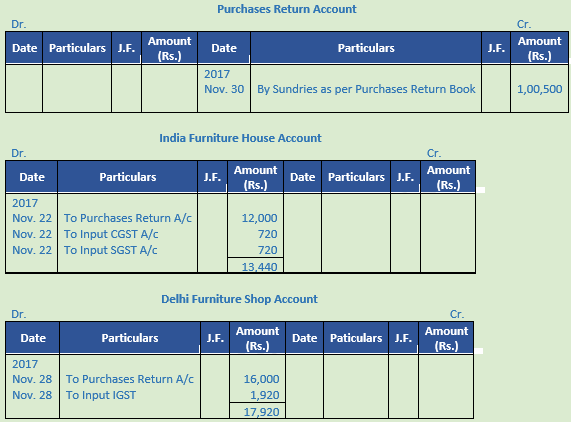

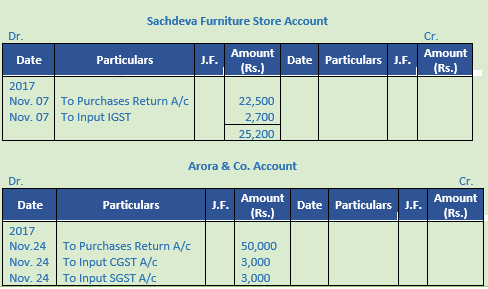

Question 7. Enter the following transactions in Return Outward Book of Modern Furniture House, Udaipur (Rajasthan) assuming CGST @ 6% and SGST @ 6% and post it into Ledger:-

Solution 7:

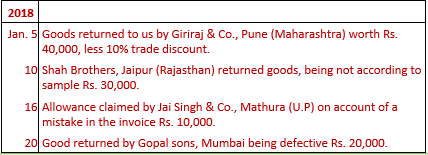

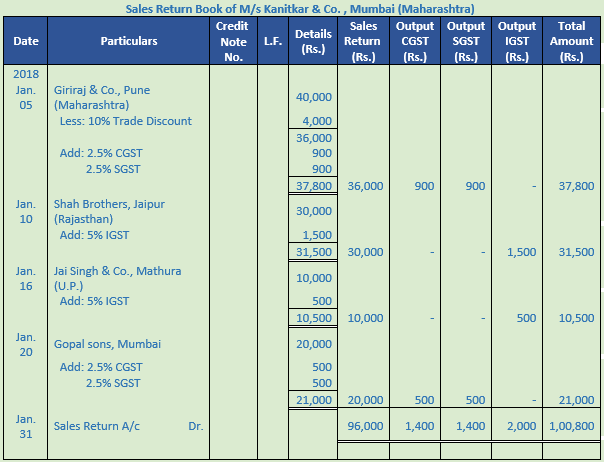

Question 8. Enter the following transactions in Return Inward Book of M/s Kanitkar & Co. of Mumbai (Maharashtra) assuming CGST @ 2.5% and SGST @ 2.5% and post it into Ledger:

Solution 8:

Point of knowledge:-

- Identify in the Ledger the account to be credited.

- Enter the date of the transaction in the 'Date' column on the credit side of the account.

- Write the name of the account which has been debited in the respective entry in the 'Particulars' column on the credit side of the account as 'By (name of account debited)'.

- Record the page number of the Journal where the entry exists in the Journal folio (J.F.) column.

- Enter the relevant amount in the 'Amount' column on the credit side.

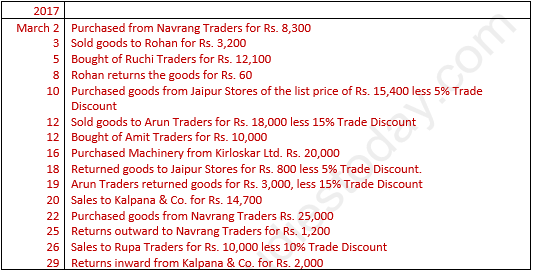

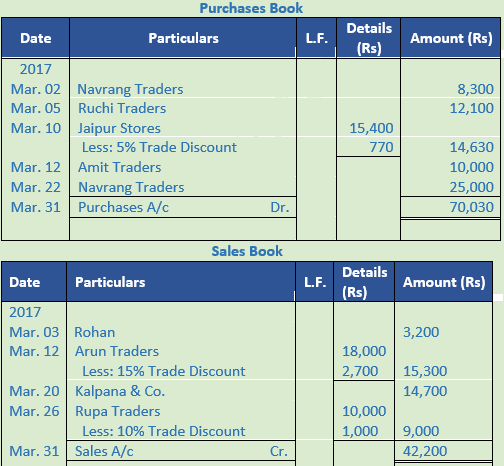

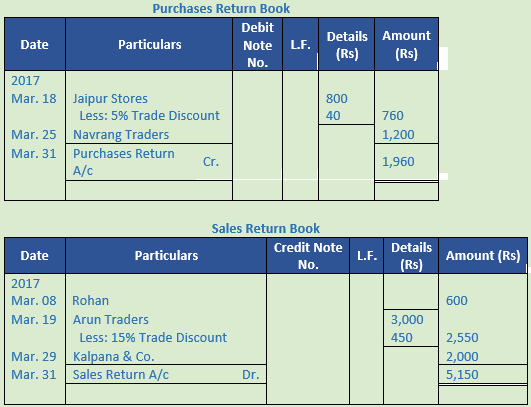

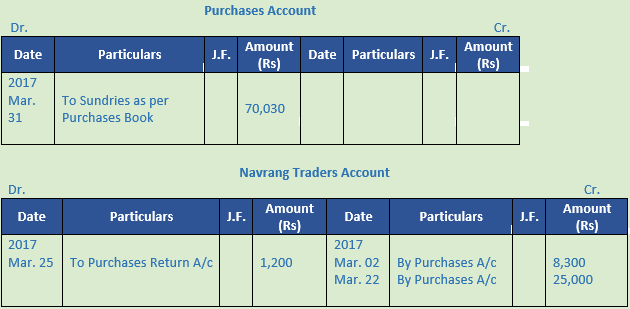

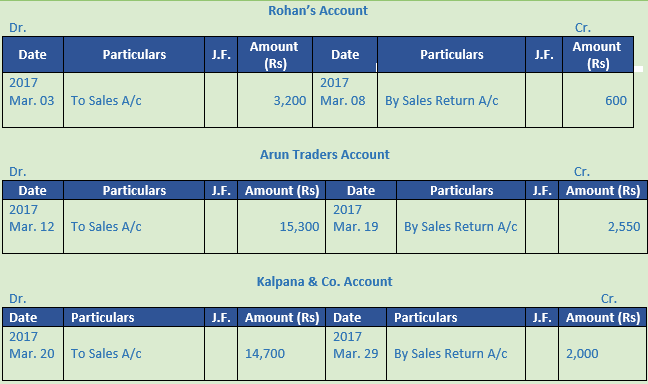

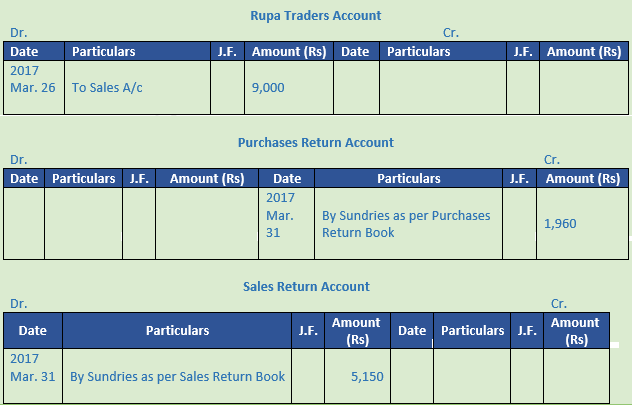

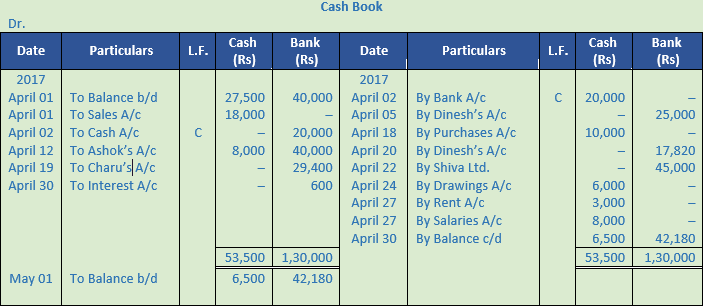

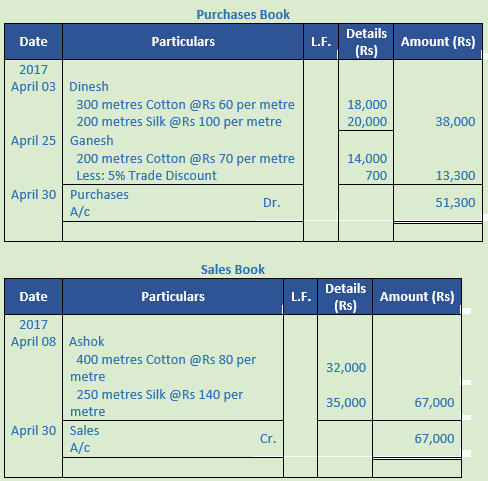

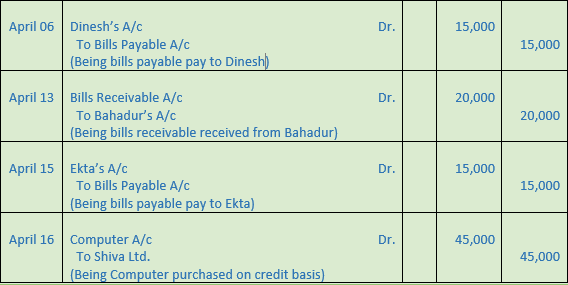

Question 9. Enter the following transactions in proper Subsidiary Books and post them into Ledger :−

Solution 9:

Point of knowledge:-

(1) If the debit side total is more than the credit side total write the difference on the credit side as “By Balance c/d”.

(2) If the credit side total is more than the debit side total write the difference on the credit side as “To Balance c/d”.

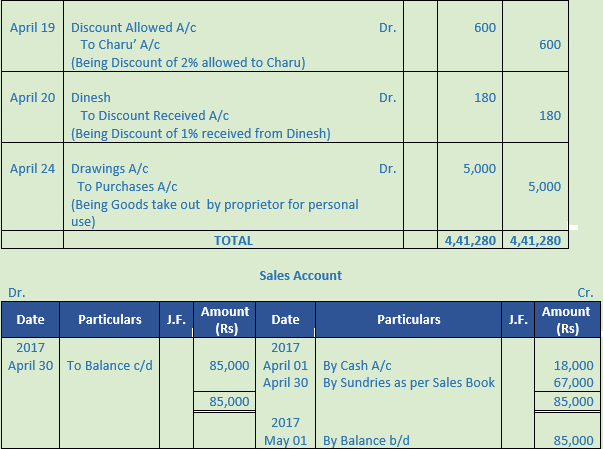

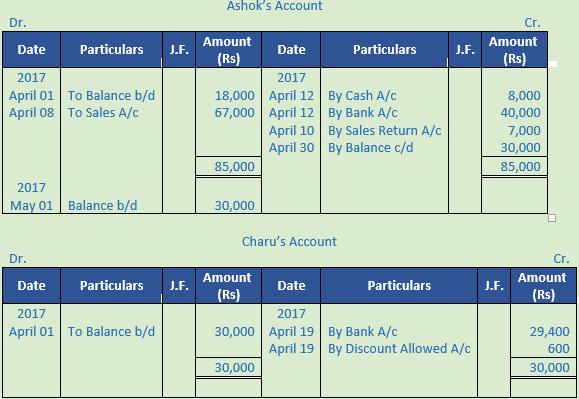

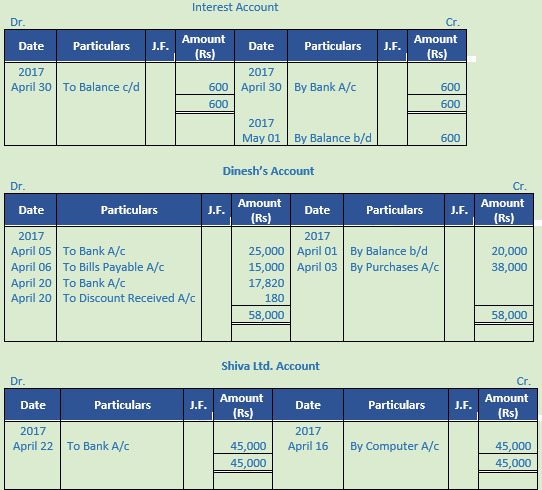

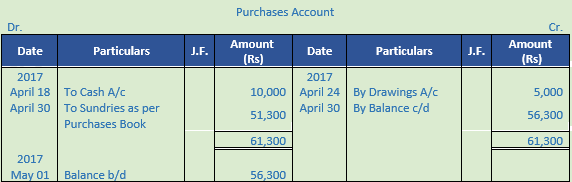

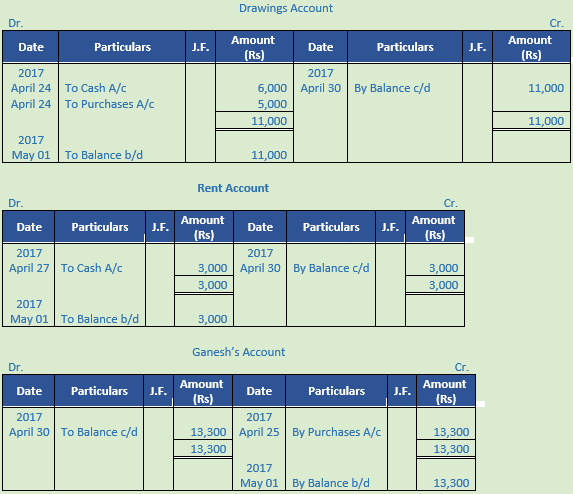

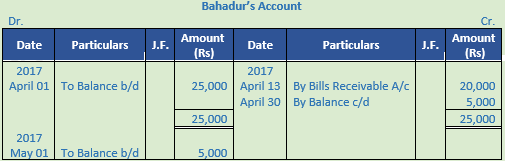

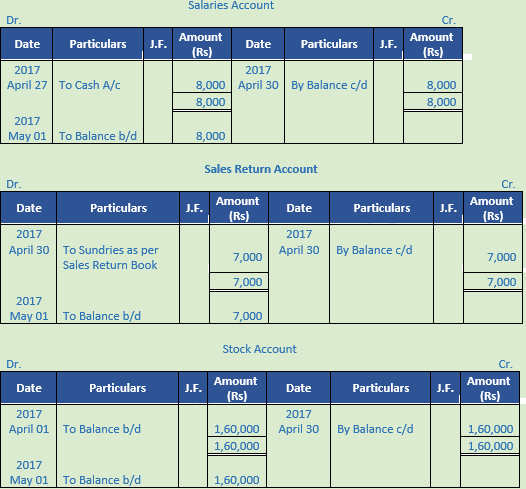

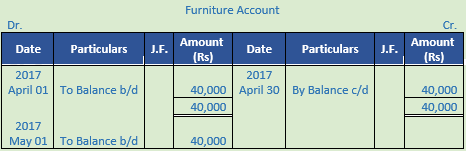

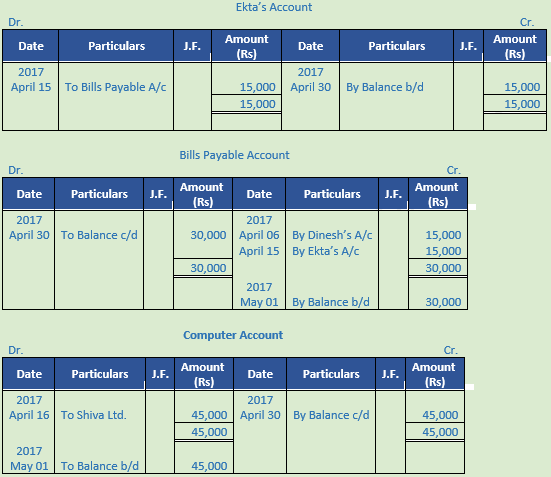

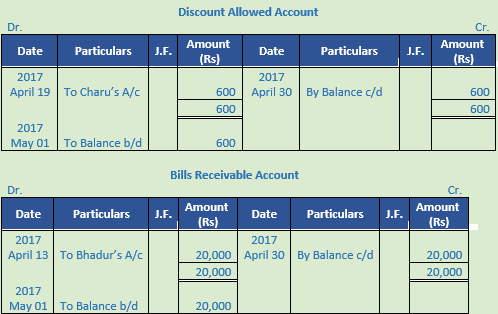

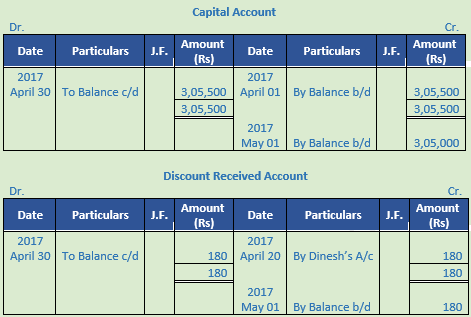

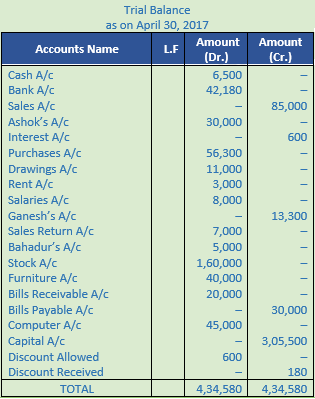

Question 10. Enter the following transactions in subsidiary books, post them into Ledger and prepare a Trial Balance:

The following balances existed in Sunil Bros. books on April 1, 2017:

Assets : Cash in hand Rs. 27,500; Bank Balance Rs. 40,000; Debtors : Ashok Rs. 18,000, Bahadur Rs. 25,000, Charu Rs. 30,000; Stock Rs. 1,60,000 and Furniture Rs. 40,000.

Liabilities : Creditors : Dinesh Rs. 20,000 and Ekta Rs. 15,000.

2017

April 1 Cash Sales Rs. 18,000.

2 Deposited into Bank Rs. 20,000.

3 Purchased from Dinesh :

300 metres Cotton @ Rs. 60 per metre

200 metres Silk @ Rs. 100 per metre

5 Cheque issued to Dinesh for Rs. 25,000.

6 Accepted a bill at one month for Rs. 15,000 drawn by Dinesh.

8 Sold to Ashok :

400 metres Cotton @ Rs. 80 per metre

250 metres Silk @ Rs. 140 per metre

10 Returned by Ashok 50 metres Silk.

12 Received Cash Rs. 8,000 and a Cheque for Rs. 40,000 from Ashok. Cheque was immediately sent to Bank.

13 Received a B/R from Bahadur for Rs. 20,000 at one month.

15 Accepted a bill at two months drawn by Ekta for the amount due to her.

16 Purchased a Computer for office use from Shiva Ltd. for Rs. 45,000 on Credit.

18 Cash purchases Rs. 10,000.

19 Received full payment from Charu by cheque, sent it to Bank. Discount allowed 2%.

20 Issued a cheque to Dinesh in full payment of his account after deducting 1% discount.

22 Settled the account of Shiva Ltd. by a cheque.

24 Proprietor took away goods worth Rs. 5,000 and Cash Rs. 6,000.

25 Purchased from Ganesh 200 metres Cotton @ Rs. 70 per metre subject to trade discount of 5%.

27 Paid Rent Rs. 3,000 and Salaries Rs. 8,000.

30 Interest allowed by bank Rs. 600.

Solution 10:

Point of knowledge:-

(1) If the debit side total is more than the credit side total write the difference on the credit side as “By Balance c/d”.

(2) If the credit side total is more than the debit side total write the difference on the credit side as “To Balance c/d”.

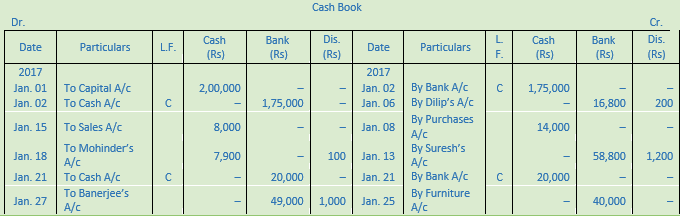

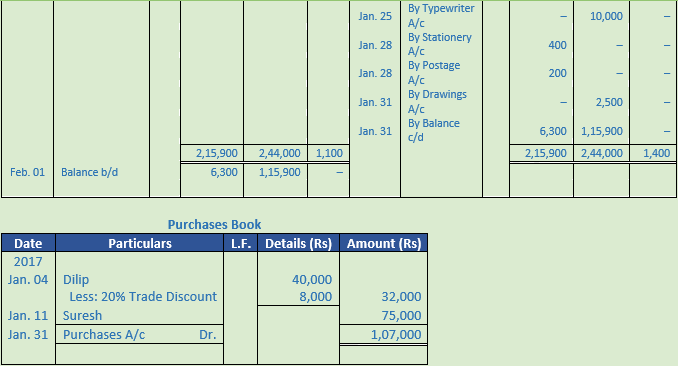

Question 11. Record the following transactions of M/s Mahipal Bros. in Proper Subsidiary Books, post them into the Ledger and take out a Trial Balance:

2017

Jan. 1 Commenced business with Cash Rs. 2,00,000.

2 Deposited into U.T.I Bank Rs. 1,75,000.

4 Purchased goods from Dilip for Rs. 40,000. Trade Discount 20%.

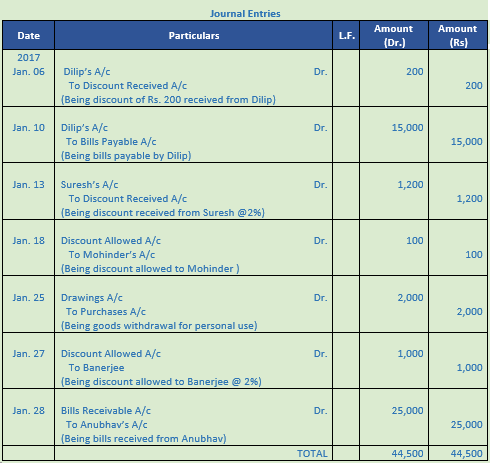

6 Gave a cheque to Dilip for Rs. 16,800 and discount allowed by him Rs. 200.

8 Goods bought from Nilesh for Cash Rs. 14,000.

10 Accepted a bill at 2 months for Rs. 15,000 drawn by Dilip.

11 Bought goods from Suresh Rs. 75,000.

13 Paid to Suresh a Cheque for Rs. 58,800 after receiving discount of 2%.

15 Cash sales made to Jyoti Parshad Rs. 8,000.

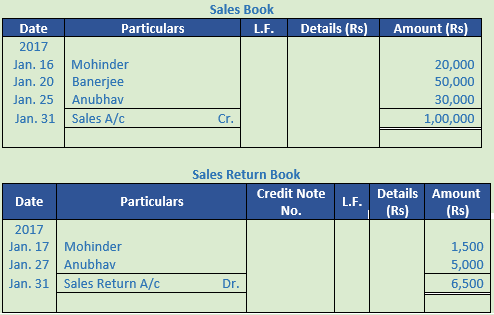

16 Sold goods to Mohinder for Rs. 20,000.

17 Goods returned by Mohinder for Rs. 1,500.

18 Received from Mohinder Rs. 7,900 after allowing a discount of 1.25%.

20 Goods sold to Banerjee Rs. 50,000.

21 Deposited into Bank Rs. 20,000.

25 Goods taken for personal use Rs. 2,000.

25 Purchased furniture Rs. 40,000 and Typewriter Rs. 10,000 for office use.

Payment for both the items is made by Cheque.

25 Sold goods to Anubhav Rs. 30,000.

27 Goods returned by Anubhav Rs. 5,000.

27 Received full payment from Banerjee by Cheque, sent it to Bank, Discount allowed 2%.

28 Acceptance received from Anubhav at 30 days for the amount due from him.

28 Paid for stationery Rs. 400 and for Postage Rs. 200.

31 Rent of proprietor's house paid by Cheque Rs. 2,500.

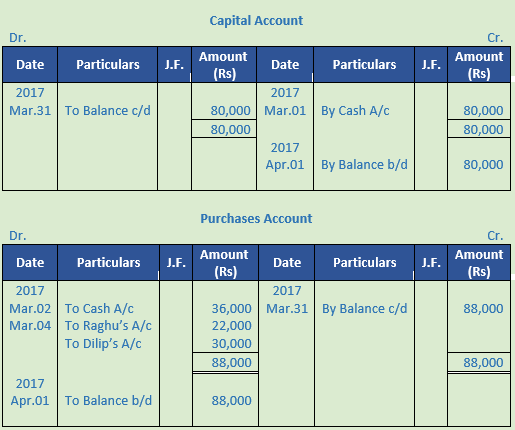

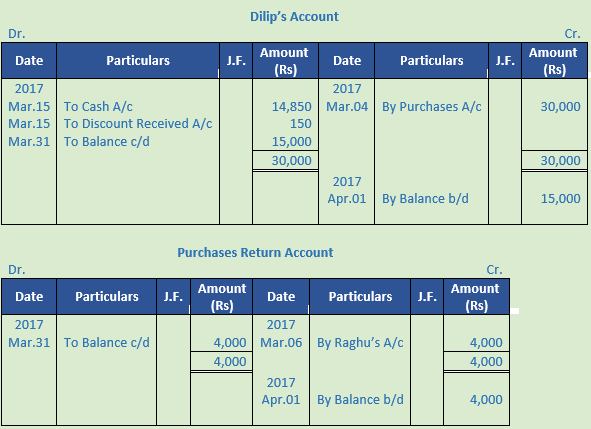

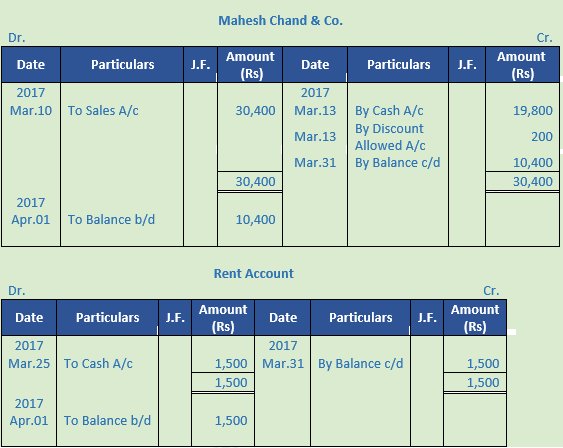

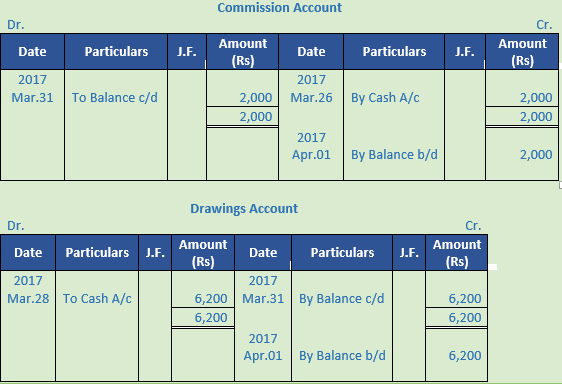

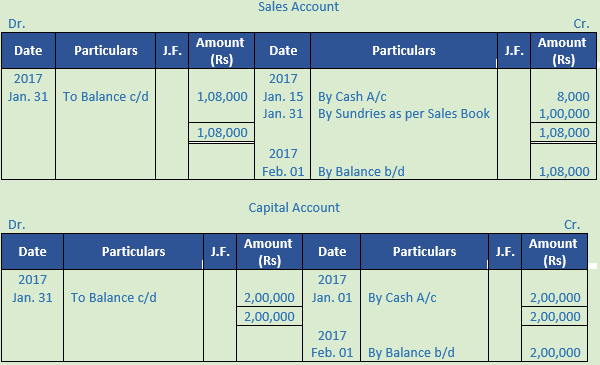

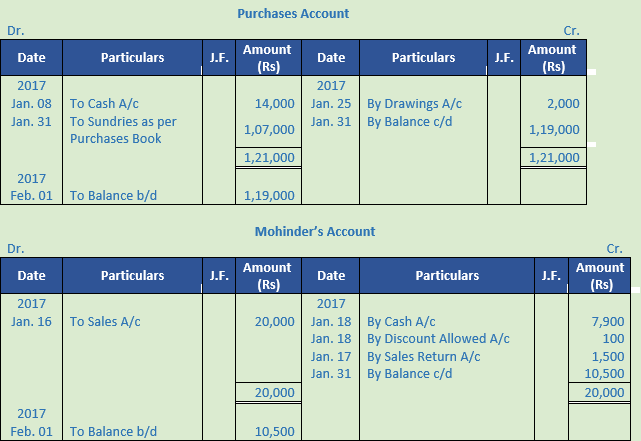

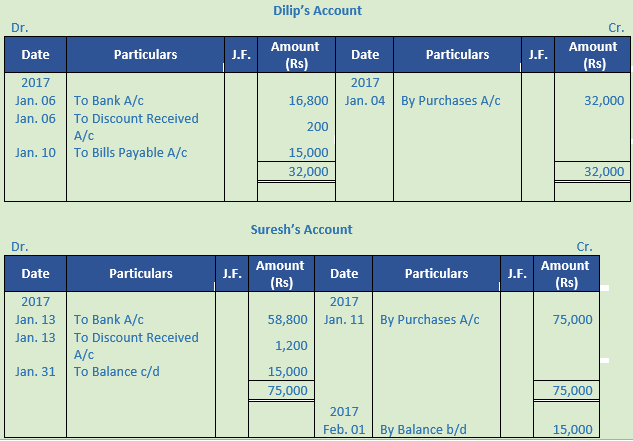

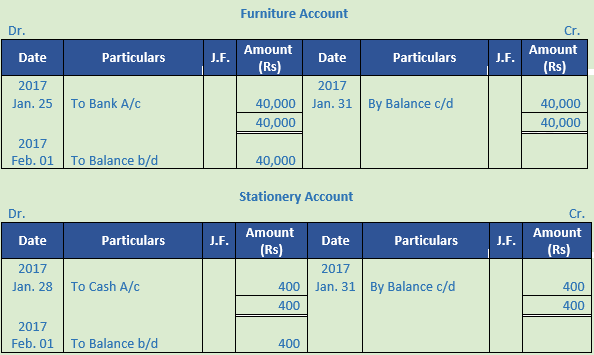

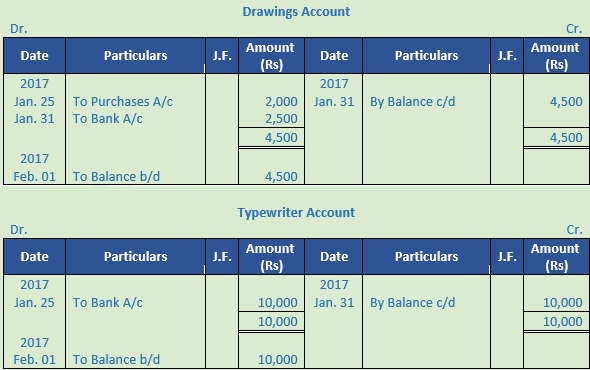

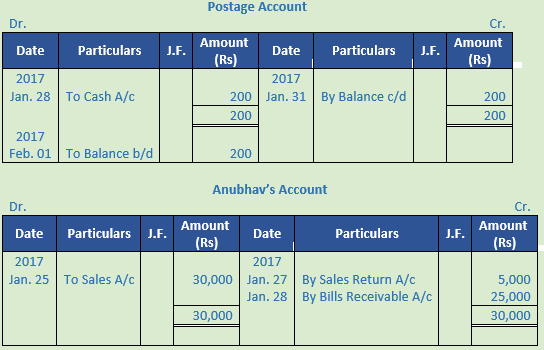

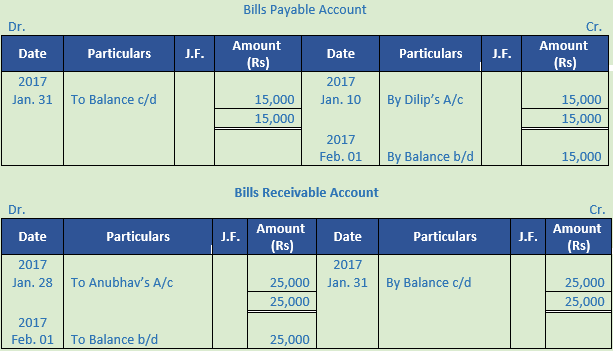

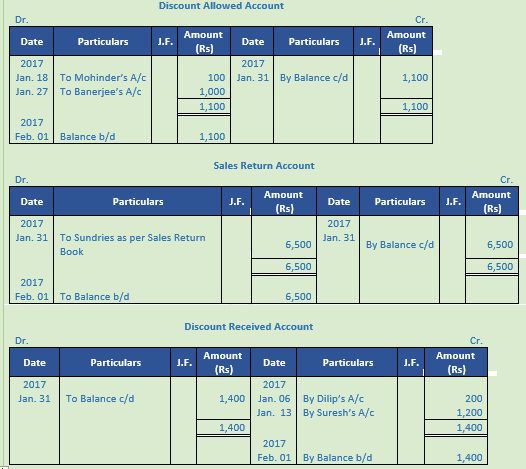

Solution 11:

Point of Knowledge:-

Journal Folio (J.F.) Column in the ledger records Page No. of the journal from which the posting to the Ledger has taken place. Purpose of posting J.F. number is that it provides a ready reference for tracing the page of journal from where the entry has been posted.

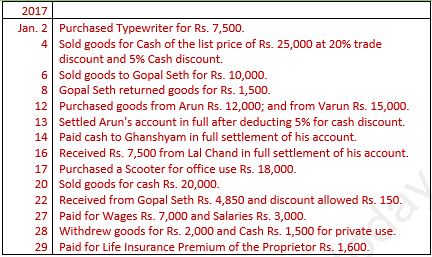

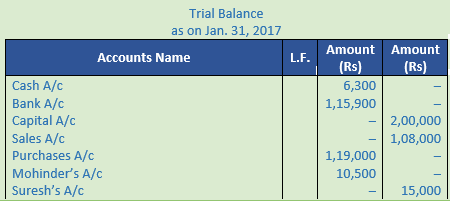

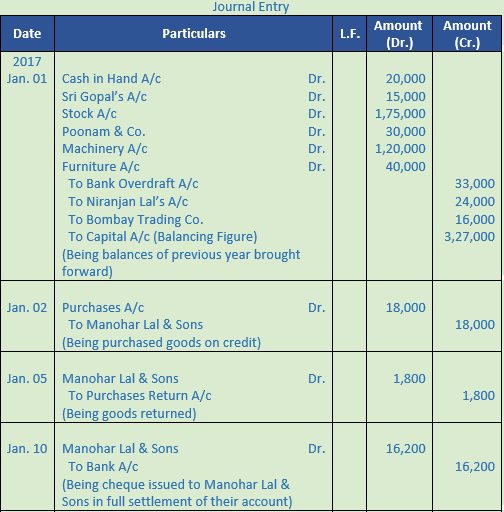

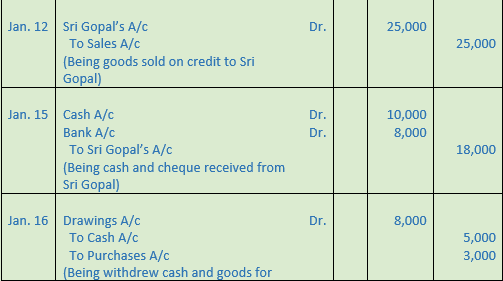

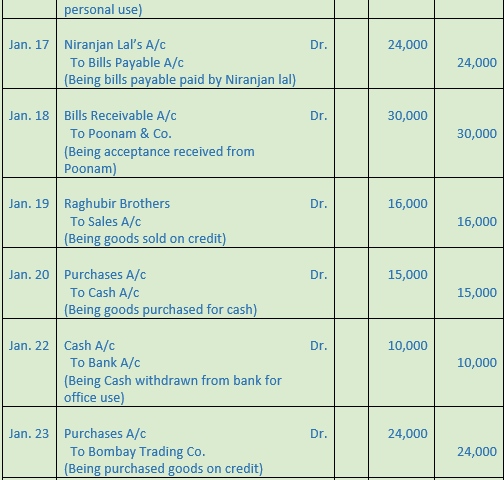

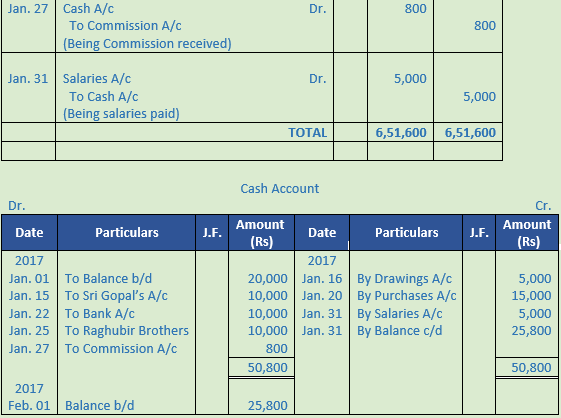

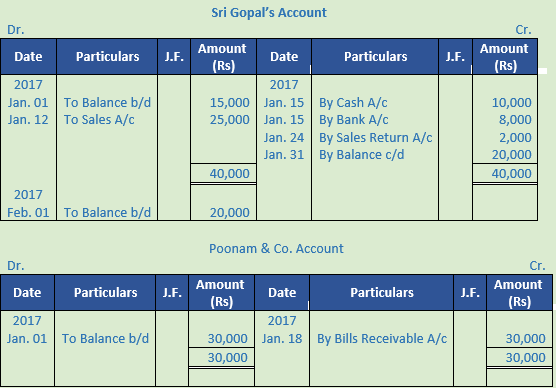

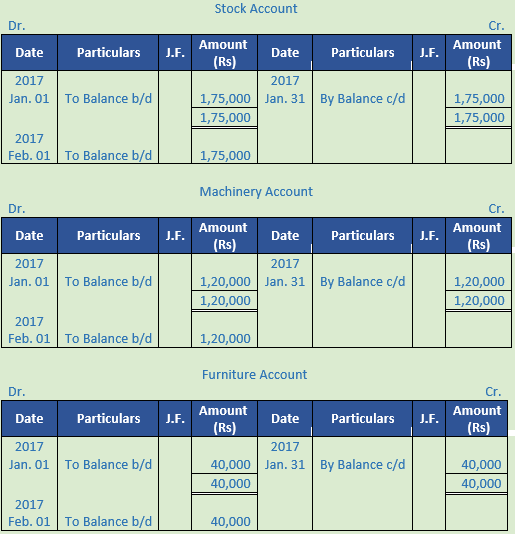

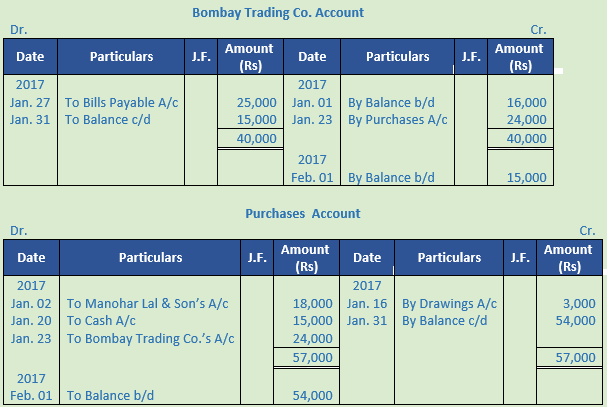

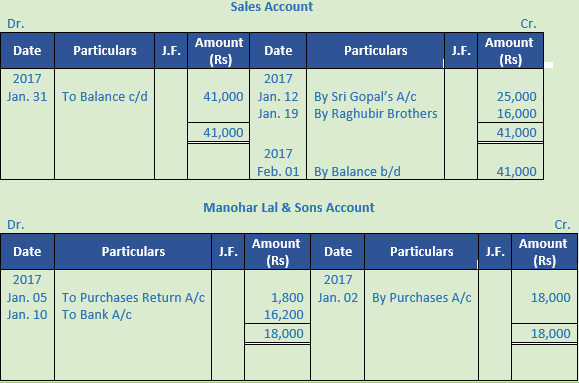

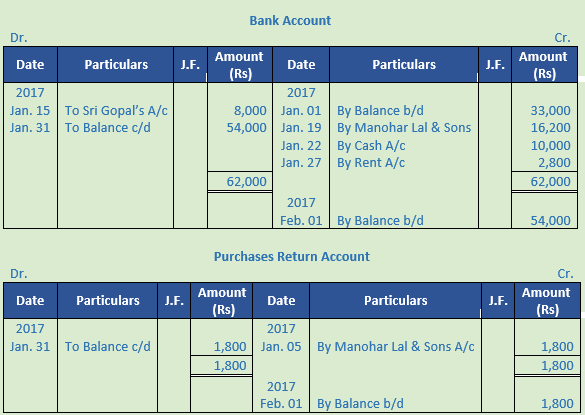

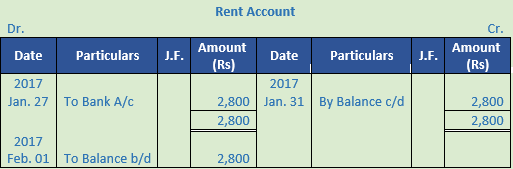

Question 12. Enter the following transactions in proper Subsidiary Books, post them into Ledger Accounts, balance the accounts and prepare a Trial Balance :

2017

Jan. 1 Assets : Cash in hand Rs. 20,000; Debtors : Sri Gopal Rs. 15,000, Poonam & Co. Rs. 30,000; Stock Rs. 1,75,000, Machinery Rs. 1,20,000; Furniture Rs. 40,000.

Liabilities: Bank Overdraft Rs. 33,000; Creditors : Niranjan Lal Rs. 24,000, Bombay Trading Co. Rs. 16,000.

Jan. 2 Purchased from Manohar Lal & Sons goods of the list price of Rs. 20,000 at 10% trade discount.

5 Returned to Manohar Lal & sons goods of the list price of Rs. 2,000.

10 Issued a Cheque to Manohar Lal & Sons in full settlement of their account.

12 Sold to Sri Gopal, goods worth Rs. 25,000.

15 Received Cash Rs. 10,000 and a Cheque for Rs. 8,000 from Sir Gopal. The Cheque was immediately sent to bank.

16 Withdrew for personal use : Cash Rs. 5,000 and goods Rs. 3,000.

17 Accepted a bill for 45 days drawn by Niranjan Lal for the amount due to him.

18 Acceptance received from Poonam & Co. for the amount due from them payable after 30 days.

19 Sold to Raghubir Brothers, goods valued Rs. 16,000.

20 Cash purchases Rs. 15,000.

22 Withdrew from bank fo office use Rs. 10,000.

23 Purchased from Bombay Trading Co., goods valued Rs. 24,000.

24 Sri Gopal returned goods worth Rs. 2,000.

25 Received from Raghubir Brothers Rs. 10,000.

27 Accepted a bill for Rs. 25,000 for 1 month drawn by Bombay Trading Co.

27 Paid Rent by Cheque Rs. 2,800.

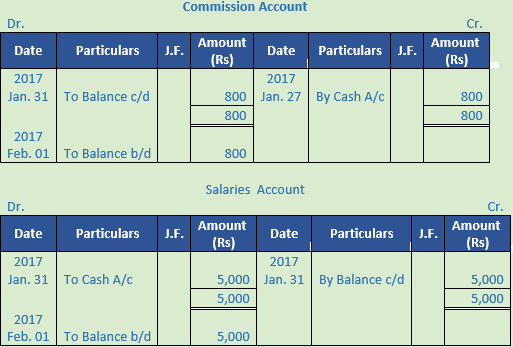

Received Commission in Cash Rs. 800.

31 Paid salaries Rs. 5,000.

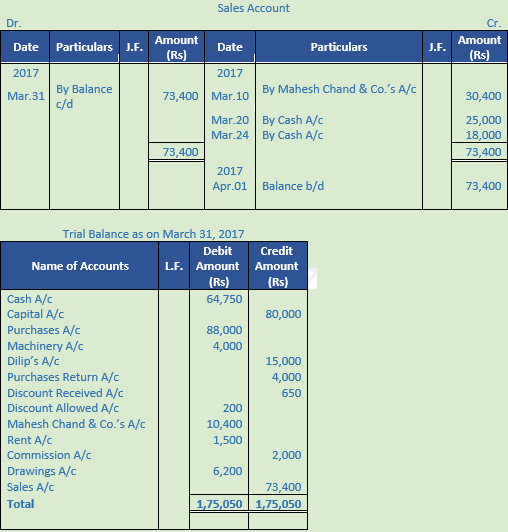

Solution 12:

Point of Knowledge:-

Earlier, we discussed the term Account. In an account, transactions of one nature are posted or summarized. All the accounts put together constitute a 'Ledger'. A Ledger may be defined as a "book or register which contains, in a summarized and classified form, a permanent record of all transactions." It is the most important book of accounts, since, the Trial Balance is drawn from it and from the Trial Balance, and Financial Statements are prepared. Hence, the Ledger is called the Principal Book.