Read DK Goel Class 11 Accountancy Solutions for Chapter 20 Capital and Revenue below. These DK Goel Accountancy Class 11 solutions have been prepared based on the latest book for DK Goel Class 11 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 11 Solutions help commerce students in class 11 understand accountancy and build a strong base in accounts. Students in Class 11 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 20 Capital and Revenue should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 11 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 20 Capital and Revenue DK Goel Class 11 Solutions

Class 11 Accountancy students should read the following DK Goel Solutions for Class 11 Chapter 20 Capital and Revenue in Standard 11. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 11 Accountancy will be very useful for exams and help you to score good marks in Class 11 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 11.

DK Goel Solutions Chapter 20 Capital and Revenue Class 11 Accountancy

Very Short Answer Questions

Question 1. What is Capital Expenditure?

Solution 1: Any expenditure which is incurred in acquiring or increasing the value of a fixed asset is treated as capital expenditure.

Question 2. Give two examples of capital expenditure.

Solution 2: Below are the examples of capital expenditure:-

1.) Purchases of Land and Building

2.) Purchases of Plant and Machinery

Question 3. Explain Revenue Expenditure with an example.

Solution 3: Any expenditure the benefit of which is received during the current year itself is termed a as revenue expenditure. For example:- Expenses incurred for the purpose of day to day running of business such as manufacturing expenses, office expenses, selling expenses etc.

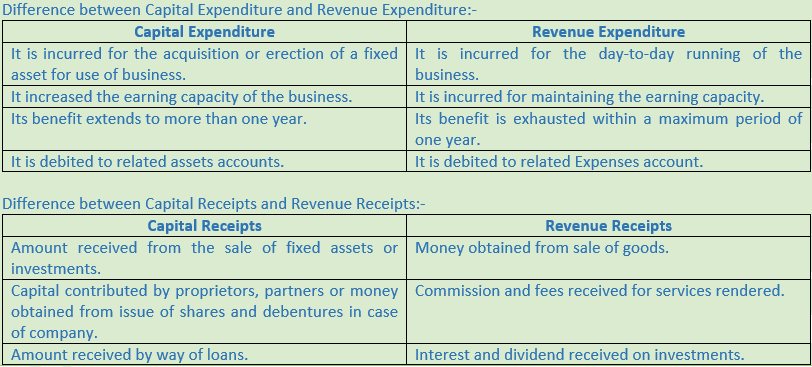

Question 4. Give two points of distinction between Capital Expenditure and Revenue Expenditure.

Solution 4:

Question 5. Distinguish between Capital Receipts and Revenue Receipts.

Solution 5:

Question 6. Wages paid on installation of a machine is a capital expenditure or revenue expenditure? Give reason.

Solution 6: Wages paid on installation of a machine is a capital expenditure because it will be treated as a cost of machine.

Long Answer Questions

Question 1. State the meaning of capital expenditure and revenue expenditure. What is the difference between them?

Solution 1: Any expenditure which is incurred in acquiring or increasing the value of a fixed asset is treated as capital expenditure. For example:- Purchases of Land and Building, Purchases of Plant and Machinery. Whereas Any expenditure the benefit of which is received during the current year itself is termed a as revenue expenditure. For example:- Expenses incurred for the purpose of day to day running of business such as manufacturing expenses, office expenses, selling expenses etc.

Question 2. “Capital expenditure is different from Revenue Expenditure.” Explain by giving suitable examples.

Solution 2: Any expenditure which is incurred in acquiring or increasing the value of a fixed asset is treated as capital expenditure. As such, the amount spent on the purchases of land and building, plant and machinery, furniture hence is written in assets.

Examples are:-

1.) Expenditure which results in the acquisition of a fixed asset such as land, building, plant, motor vehicles, trademarks etc. Such asset would be used in the business for a number of years.

2.) Expenditure in connection with the purchase or erection of a fixed asset such as wages paid to workers for erecting machines, cartages paid on acquiring plant and machinery, over-hauling of second-hand machines etc.

Any expenditure the benefit of which is received during the current year itself is termed a as revenue expenditure. As such, all the revenue expenditures are debited to trading and profit and loss account. Such expenditure does not result in an increase in the earning of the business but only helps in maintaining the existing earning capacity.

Examples are:-

1.) Expenses incurred for the purpose of day to day running of business such as manufacturing expenses, office expenses, selling expenses etc.

2.) Expenses incurred on the ordinary repairs and maintenance of fixed assets, white-washing of building etc.

Question 3. Distinguish between:-

(i) Capital Expenditure and Revenue Expenditure

(ii) Capital Receipts and Revenue Receipts

Solution 3:

Question 4. Classify the following as capital expenditure, revenue expenditure and deferred revenue expenditure for a cloth merchant?

(a) Preliminary Expenses

(b) Purchases of Furniture

(c) Payment of Salary

(d) Expenses paid for construction of building

Solution 4:

(a) Preliminary Expenses : Deferred Revenue Expenditure

(b) Purchases of Furniture : Capital Expenditure

(c) Payment of Salary : Revenue Expenditure

(d) Expenses paid for construction of building : Capital Expenditure

Practical Questions

Question 1. State with reasons whether the following are capital or revenue expenditures:

(i) A new machine is purchased for Rs. 60,000, Rs. 800 were spent on its carriage and Rs. 1,500 were paid as wages for its installation.

(ii) A sum of Rs. 10,000 was spent on painting the new factory.

(iii) Rs. 5,000 paid for the erection of a new machine.

(iv) Rs. 2,000 were spent on repairs before using a second hand generator purchased recently.

(v) Rs. 1,500 were spent on the repair of a machinery.

(vi) Rs. 10,000 was paid as brokerage on issue of shares and other expenses of issue were Rs. 25,000.

Solution 1:

(i) Capital Expenditure cost of installation is also a capital expenditure and include in machinery account. This expense will increase the earning capacity of the firm.

(ii) Capital Expenditure as the company has been painted at first time it will included in the assets. It will be treated as a capital expenditure.

(iii) Capital Expenditure all expenses related to new machine will be capital expenditure.

(iv) Capital Expenditure as repairs are done before the generator is use.

(v) Revenue Expenditure as repairs is done on regular basis.

(vi) Capital Expenditures as raising the capital will be treated as capital expenditure.

Question 2. State whether the following expenditure are Capital, Revenue or Deferred Revenue. Give reasons:

(i) Furniture of the book value of Rs. 10,000 were sold off at Rs. 2,500 and new furniture of the value of Rs. 6,000 were acquired, cartage on purchase Rs. 50.

(ii) Property purchased for Rs. 20,00,000 and Rs. 1,50,000 paid for its registration and legal fee.

(iii) Replacement of old machine by a new one.

(iv) Damages paid by a transport company to its passengers injured in an accident.

(v) Erection of shed for parking of vehicles at a cost of Rs. 10 Lac.

Solution 2:

(i) Revenue expenditure Book value = Rs. 10,000 – Rs. Sale price = Rs. 2,500 = Loss on sale of furniture of Rs. 7,500. Purchase of New furniture + cartage Rs. 6,050 will be Capital expenses.

(ii) Capital expenditure purchases of property and other related expense are capital expenditure.

(iii) Capital expenditure, as new machinery is purchased.

(iv) Capital expenditure, as damages paid on accident does not result in increasing the earning capacity of the firm.

(v) Capital expenditure, as new construction is done in increasing the earning capacity of the firm.

Question 3. Classify the following into Capital, Revenue and Deferred Revenue expenditure, stating reasons in each case:

(a) A sum of Rs. 32,000 has been spent on a machine as follows:

(i) Rs. 20,000 for addition to double the output, (ii) Rs. 5,000 for repairs necessitated by negligence and (iii) Rs. 7,000 for replacement of worn-out parts.

(b) Total expenditure on a cinema building during the year was Rs. 2,00,000 out of which 20% related to repairs and 80% represented improvements and additions.

(c) Compensation paid to a retrenched employee for the loss of employment.

(d) Second-hand furniture worth Rs. 40,000 was purchased and repairing of this furniture cost Rs. 15,000. The furniture was installed by own workmen-wages for this being Rs. 5,000.

(e) A person was injured by the motor car of the company. Rs. 10,000 was paid to him by way of compensation.

(f) Advertisement expenditure in special advertisement drive.

Solution 3:

(a) Here Rs. 20,000 is capital expenditure as it will increase the output of the firm. Rs. 5,000 is revenue expenditure Repairs as it is done on regular basis.

(b) Revenue Expenditure repairs of Rs. 40,000 is done on regular basis and Rs. 1,60,000 is done on improvements which will give future benefits, therefore its capital expenditure.

(c) Revenue expenditure, Compensation and remuneration to employees are done in normal course of business.

(d) Capital expenditure, Any expenses incurred on bringing the asset into operation will be capitalized.

(e) Revenue expenditure, Compensation and remuneration to employees are done in normal course of business.

(f) Deferred revenue expenditure benefit will be derived over a number of years.

Question 4. State with reasons whether the following receipts would be treated as Capital or Revenue:-

(a) Rs. 5,000 received from a customer whose account was previously written off as bad.

(b) Rs. 20,000 received from sale of old machine.

(c) Rs. 2,60,000 received from sale of stock-in-trade.

(d) Rs. 5,00,000 is contributed by a partner as capital.

(e) Took a loan of Rs. 10 Lac from Punjab National Bank.

(f) Received Rs. 4 Lac as subsidy from State Government.

(g) Received Rs. 8 Lac as grant from State Government for the construction of quarters for the staff.

Solution 4:

(a) Revenue receipt as this transaction belongs to normal business transaction.

(b) Capital receipt as it is a capital gain which arose by selling of machinery.

(c) Revenue receipt as it is received in normal course of business over exchange of goods.

(d) Capital receipt as it will improve the financial position of the company of the company.

(e) Capital receipt as it will enhance the productivity of the company.

(f) Revenue receipt as it is received regularly from the government.

(g) Capital receipt as it is received for construction and will it will result in increasing the earning capacity of the firm.