Read DK Goel Class 12 Accountancy Solutions for Chapter 9 Company Accounts Redemption of Debentures below. These DK Goel Accountancy Class 12 solutions have been prepared based on the latest book for DK Goel Class 12 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 12 Solutions help commerce students in class 12 understand accountancy and build a strong base in accounts. Students in Class 12 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 9 Company Accounts Redemption of Debentures should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 12 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 9 Company Accounts Redemption of Debentures DK Goel Class 12 Solutions

Class 12 Accountancy students should read the following DK Goel Solutions for Class 12 Chapter 9 Company Accounts Redemption of Debentures in Standard 12. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 12 Accountancy will be very useful for exams and help you to score good marks in Class 12 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 12.

DK Goel Solutions Chapter 9 Company Accounts Redemption of Debentures Class 12 Accountancy

Short Answer Questions

Question 1.

Solution 1

1.) Utilise Rs. 10,00,000 to write off Underwriting Commission.

2.) Utilise Balance Rs. 12,00,000 to write off Premium on Redemption of 9% Debentures.

Numerical Questions

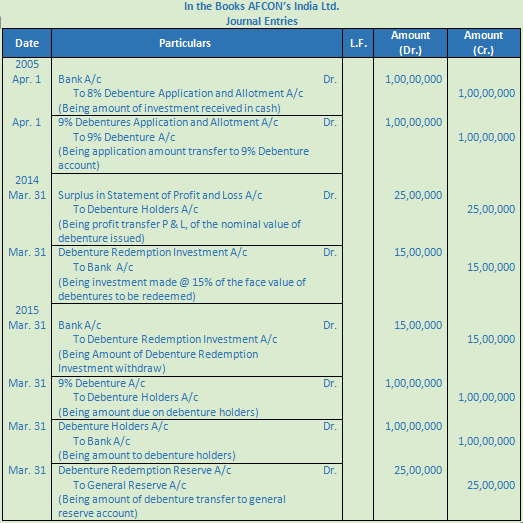

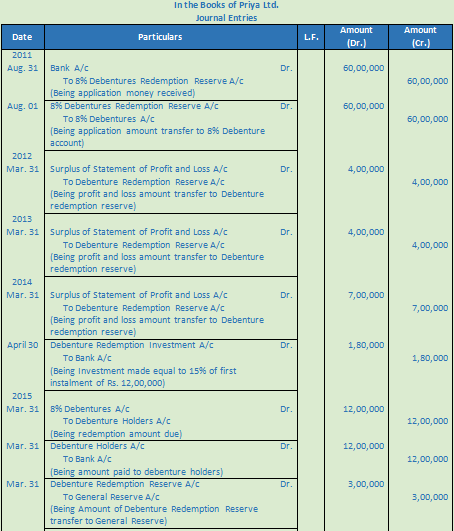

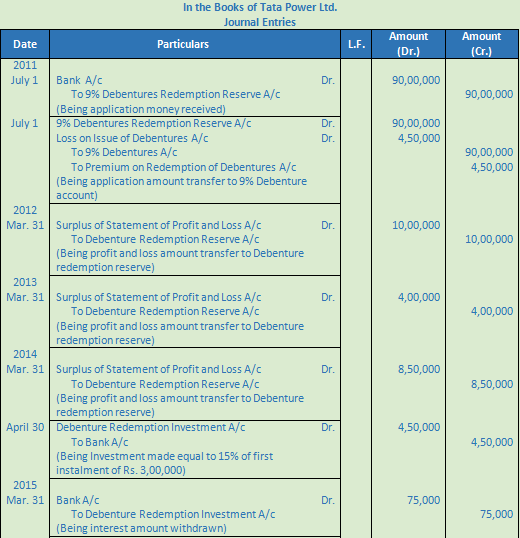

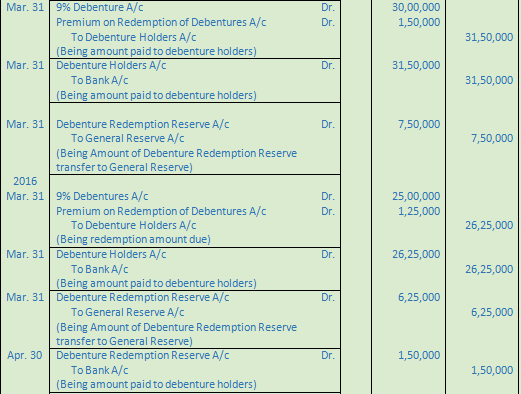

Question 1.

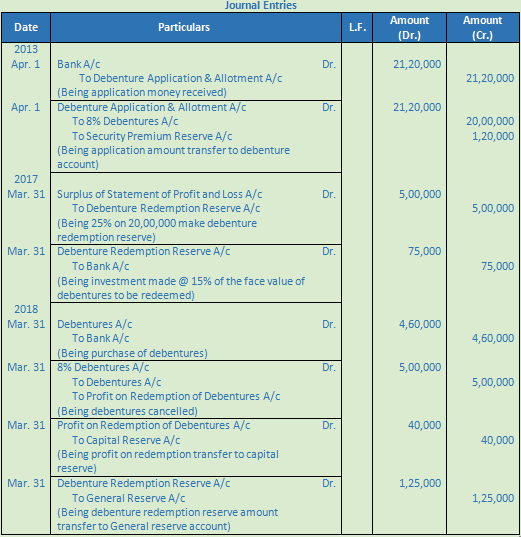

Solution 1

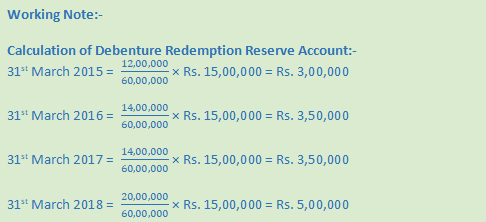

Working Note:-

1.) Interest on Investment is not calculated because rate of interest is not provided.

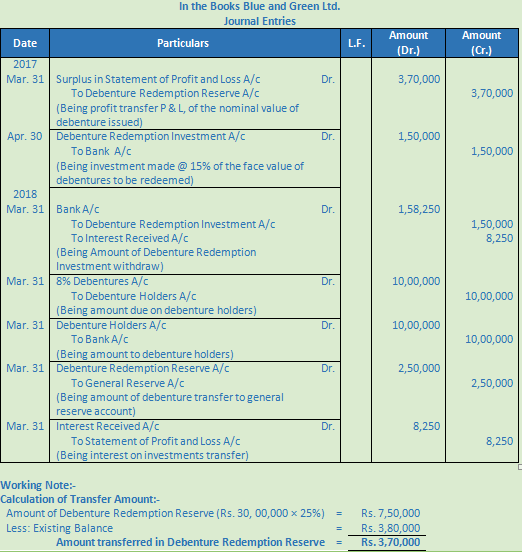

Question 2.

Solution 2

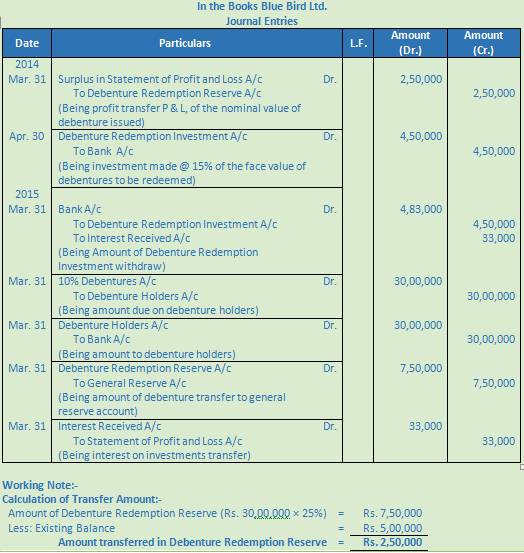

Question 3.

Solution 3

Point of Knowledge:-

A Company which is not required to create DRR is exempted from Investing 15% amount also.

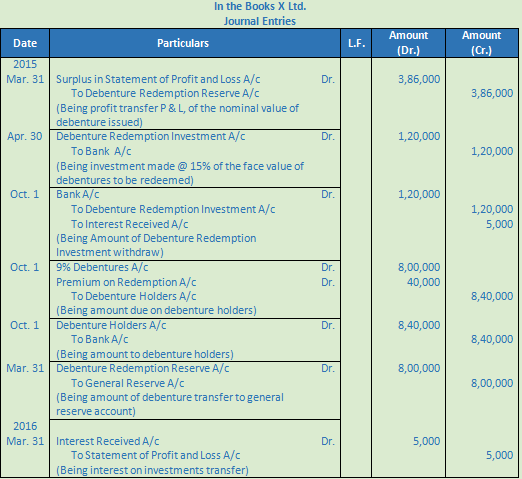

Question 4.

Solution 4

Point of Knowledge:-

A Company which is not required to create DRR is exempted from Investing 15% amount also.

Question 5.

Solution 5

Question 6.

Solution 6

Question 7.

Solution 7

Question 8.

Solution 8

Question 9.

Solution 9

Question 10.

Solution 10

Question 11.

Solution 11

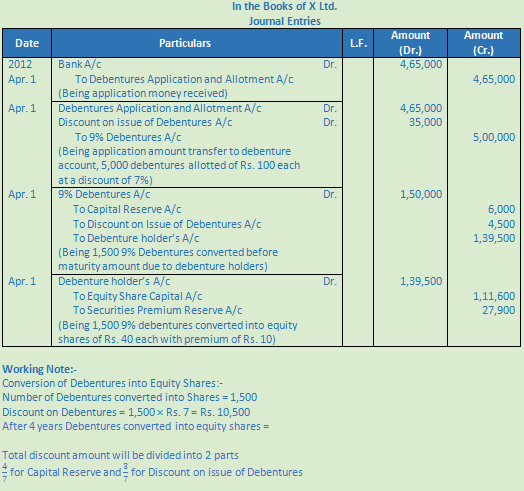

Question 12.

Solution 12

Working Note:-

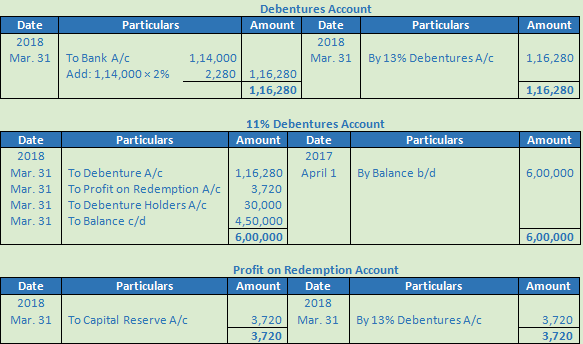

Calculation of Number of Debentures issued = = 6,30,000/105 Debentures @ Rs. 100 each.

Question 13.

Solution 13

Question 14.

Solution 14

Question 15.

Solution 15

Question 16.

Solution 16

Question 17.

Solution 17

Question 18.

Solution 18

Question 19.

Solution 19

Question 20.

Solution 20

Question 21.

Solution 21

Question 22.

Solution 22

Question 23.

Solution 23

Question 24.

Solution 24

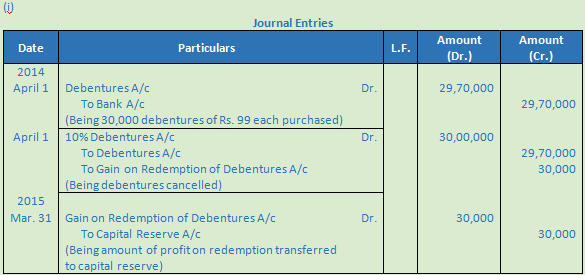

Question 25.

Solution 25

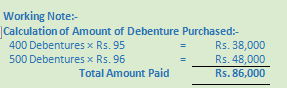

Working Note:-

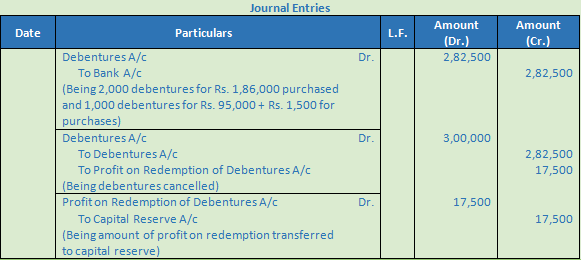

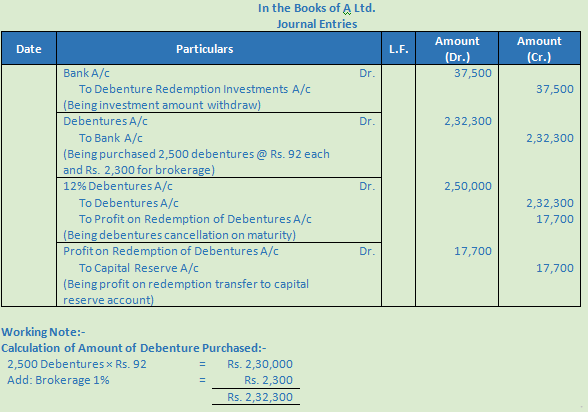

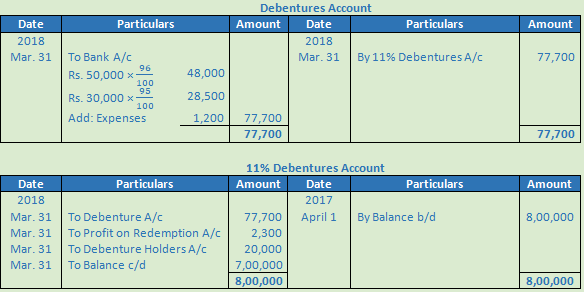

(i) Calculation of Amount paid for the purchase of debentures:

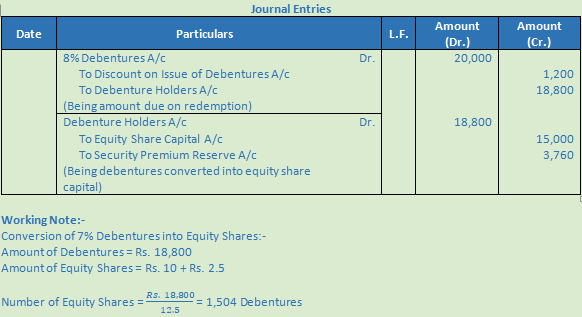

3,000 debentures × Rs. 90 per Debenture = Rs. 2,70,000

2,000 debentures × Rs. 95 per Debenture = Rs. 1,90,000

Total payment = Rs. 4,60,000

Question 26.

Solution 26

Question 27.

Solution 27

Question 28.

Solution 28

Question 29.

Solution 29

Question 30.

Solution 30

Question 31. (A)

Solution 31 (A)

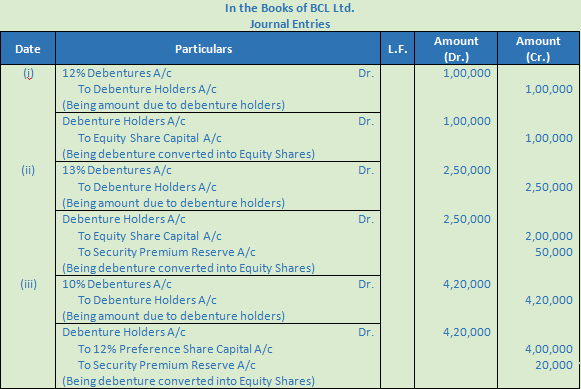

Question 32. (B)

Solution 32 (B)

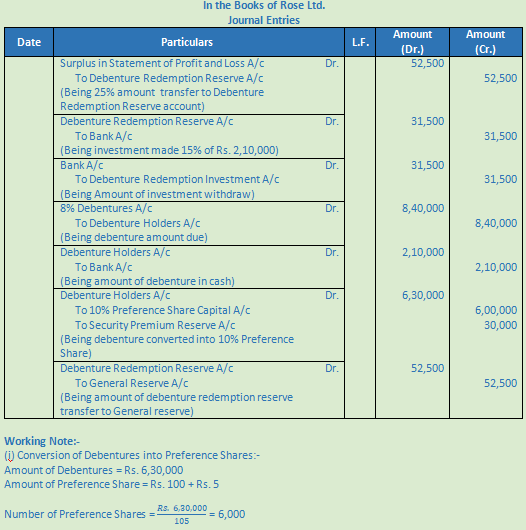

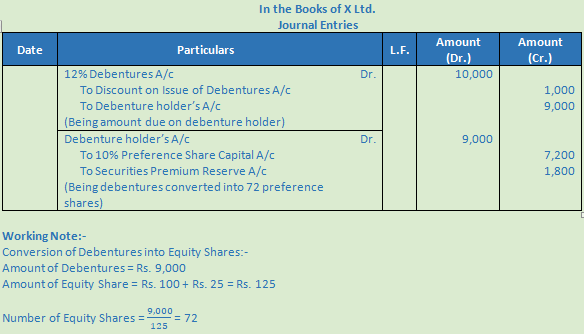

Working Note:-

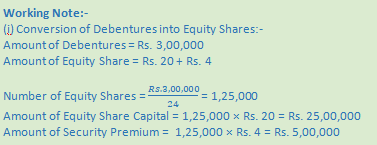

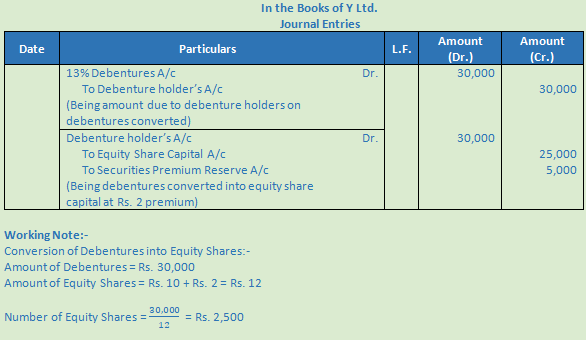

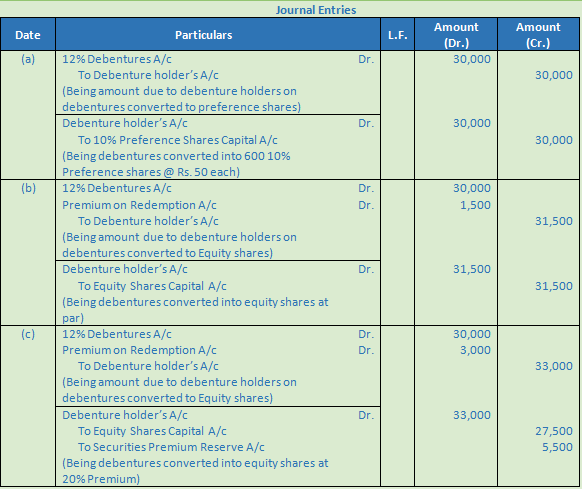

(i) Conversion of Debentures into Preference Shares:-

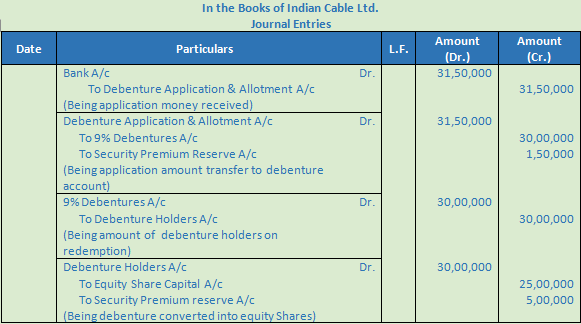

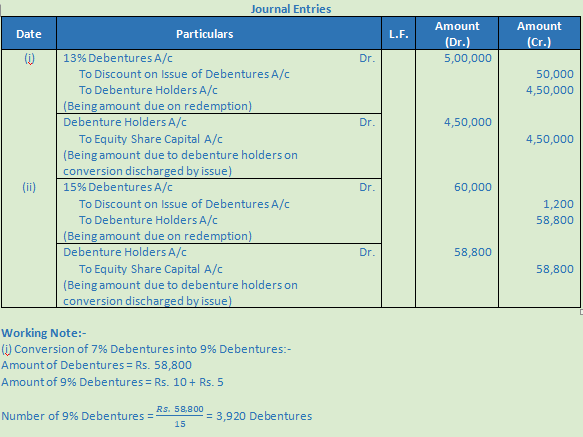

Amount of Debentures = Rs. 2,50,000

Amount of Preference Share = Rs. 10 + Rs. 12.5

Question 33.

Solution 33

Question 34.

Solution 34

Question 35.

Solution 35

Question 36.

Solution 36

Question 37.

Solution 37

Question 38.

Solution 38

Question 39.

Solution 39

Question 40.

Solution 40

Question 41.

Solution 41

Question 42.

Solution 42

Question 43.

Solution 43

Question 44.

Solution 44

Question 45.

Solution 45

Question 46.

Solution 46

Question 47.

Solution 47

Question 48.

Solution 48

Question 49.

Solution 49

Question 50.

Solution 50

Question 51.

Solution 51

Question 52.

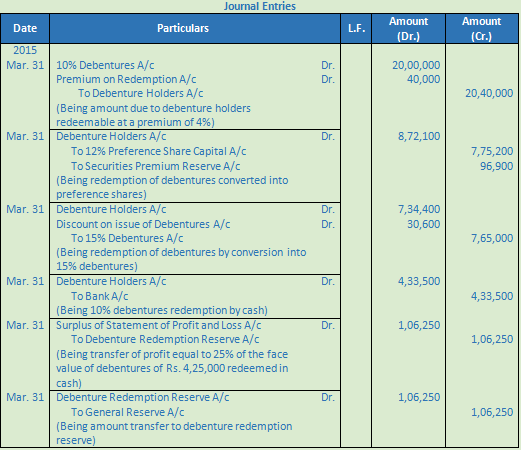

Solution 52

Working Note:-

(i) Conversion of Debentures into Preference Shares:-

Amount of Debentures = Rs. 60,000 + Rs. 3,000 (5% on Premium) = Rs. 63,000

Amount of Preference Share = Rs. 100 + Rs. 20

Number of Equity Shares = 63000/120 = 525

Amount of Equity Share Capital = 525 × Rs. 100 = Rs. 52,500

Amount of Security Premium = 525 × Rs. 20 = Rs. 10,500

Question 53. (A)

Solution 53 (A)

Question 53. (B)

Solution 53 (B)

Question 54.

Solution 54

Question 55.

Solution 55

Question 56.

Solution 56

Question 57.

Solution 57

Question 58.

Solution 58

Question 59.

Solution 59

Question 60.

Solution 60

Question 61.

Solution 61

Question 62.

Solution 62

Question 63.

Solution 63

Question 64.

Solution 64

Question 65.

Solution 65

Question 66.

Solution 66

Question 67.

Solution 67

Question 68.

Solution 68

Question 69.

Solution 69

Question 70.

Solution 70

Question 71.

Solution 71

Question 72.

Solution 72

Question 73.

Solution 73

Question 74.

Solution 74

Question 75.

Solution 75

Question 76.

Solution 76

Question 77.

Solution 77

Question 78.

Solution 78

Question 79.

Solution 79

Question 80.

Solution 80

Question 81.

Solution 81