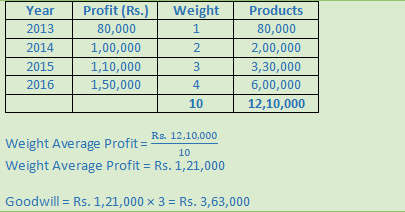

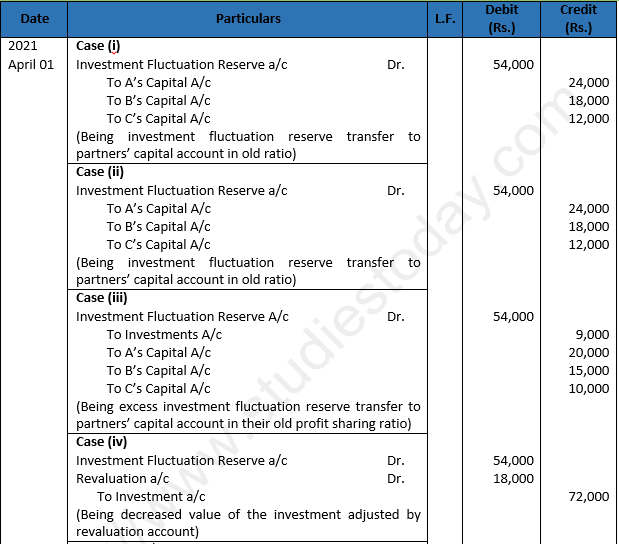

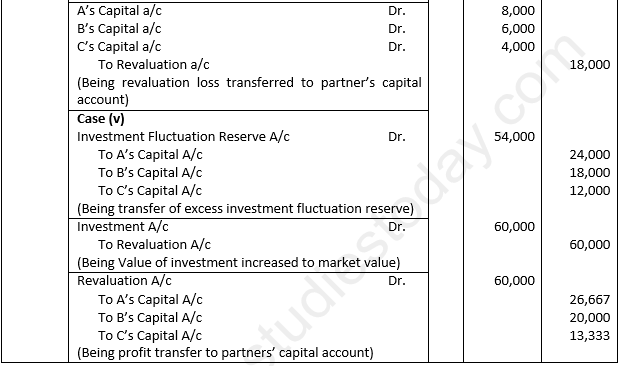

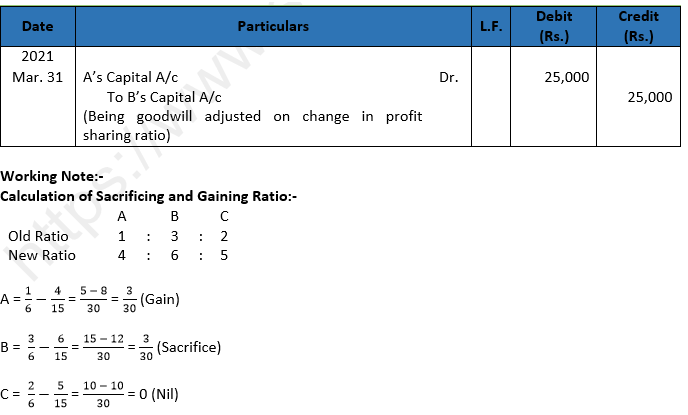

Read DK Goel Class 12 Accountancy Solutions for Chapter 3 Change in Profit Sharing Ratio Among the Existing Partners below. These DK Goel Accountancy Class 12 solutions have been prepared based on the latest book for DK Goel Class 12 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 12 Solutions help commerce students in class 12 understand accountancy and build a strong base in accounts. Students in Class 12 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 3 Change in Profit Sharing Ratio Among the Existing Partners should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 12 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 3 Change in Profit Sharing Ratio Among the Existing Partners DK Goel Class 12 Solutions

Class 12 Accountancy students should read the following DK Goel Solutions for Class 12 Chapter 3 Change in Profit Sharing Ratio Among the Existing Partners in Standard 12. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 12 Accountancy will be very useful for exams and help you to score good marks in Class 12 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 12.

DK Goel Solutions Chapter 3 Change in Profit Sharing Ratio Among the Existing Partners Class 12 Accountancy

Short Answer Questions

Question 1.

Solution 1. A firm is reconstituted on the occasions of :-

1.) Change in the profit sharing ratio among the existing partners.

2.) Admission of an existing partner.

3.) Retirement of an existing partner.

4.) Death of a partner.

5.) Amalgamation of two or more partnership firms.

Question 2.

Solution 2. Following adjustments are required at the time of reconstitution of a partnership firm:

(i) Determination of Sacrificing Ratio and Gaining Ratio

(ii) Accounting for Goodwill.

(iii) Accounting Treatment of Reserves and Accumulated Profits

(iv) Accounting for Revaluation of Assets and Liabilities.

(v) Adjustment of Capitals.

Question 3.

Solution 3. The purpose of calculating sacrificing ratio is to determine the amount of compensation to be paid by the gaining partner (i.e. the partner whose share has increased as a result of change) to the sacrificing partner (i.e. the partner whose share has decreased as a result of change). Such compensation is usually paid on the basis of proportionate amount of goodwill.

Question 4.

Solution 4 Below are the features of goodwill:-

1.) It is an intangible asset.

2.) It does not have an existence separate from that of an enterprise. Thus, is has realisable value when business is sold.

3.) The value of goodwill is the subjective assessment of the value.

Question 5.

Solution 5 Below are the four factors of affect the goodwill of a partnership firm:-

1.) Favourable Location of the business:- If the business is located at a convenient or prominent place, it will attract more customers and therefore will have more goodwill.

2.) Efficiency of Management:- If the business is run by experienced and efficient management, its profits will go on increasing which result in increase in the value of goodwill.

3.) Nature of Goodwill:- If a business deals in goods of daily use, it will have steady profit as the demand for these goods will be stable. Such business will have more goodwill. But if it deals in fancy goods, its profit will be uncertain and as such the value of the goodwill will be less.

4.) Capital Required:- The amount of capital required for a business will also influence the value of goodwill. If two business enterprises earn the same rate of profit, the business with lesser capital requirement shall enjoy more goodwill.

Question 6.

Solution 6 The need for valuing the goodwill in partnership arise in the following circumstances:

1.) When there is a change in the profit sharing ratio among the existing partners.

2.) When a new partner is admitted.

3.) When a partner retires or dies.

4.) When the firm is sold.

5.) When the firm is amalgamated with another firm.

Question 7.

Solution 7

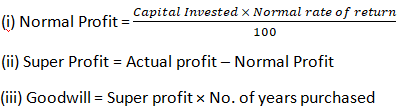

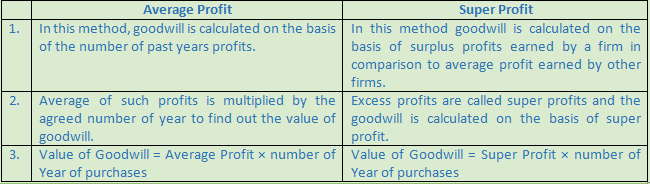

1.) Average Profit Method:- This is a very simple and widely followed method of valuation of goodwill. In this method, goodwill is calculated on the basis of the number of past year profits. Average of such profits is multiplied by the agreed number of years to find out the value of goodwill. Thus the formula is :

Value of Goodwill = Average Profit × Number of Year of Purchases.

2.) Super Profit Method:- In this method goodwill is calculated on the basis of surplus profit earned by a firm in comparison to average profits earned by other firms. If a business has no anticipated excess earning, it will have no goodwill. Of super profits.

Thus the formula is:

Question 8.

Solution 8 Number of year purchase is used to calculate the value of goodwill in average profit method and super profit method at the time of valuation of goodwill.

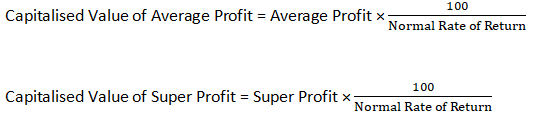

Example:- If a firm earns a profit of Rs. 60,000 p.a. on an average basis and the normal rate of return is 10% p.a. Capital employed amount Rs. 4,00,000. Capitalised value of average profit will be:

Rs. 60,000 × = Rs. 6,00,000

Goodwill = Rs. 6,00,000 – Rs. 4,00,000 = Rs. 2,00,000

Question 10.

Solution 10

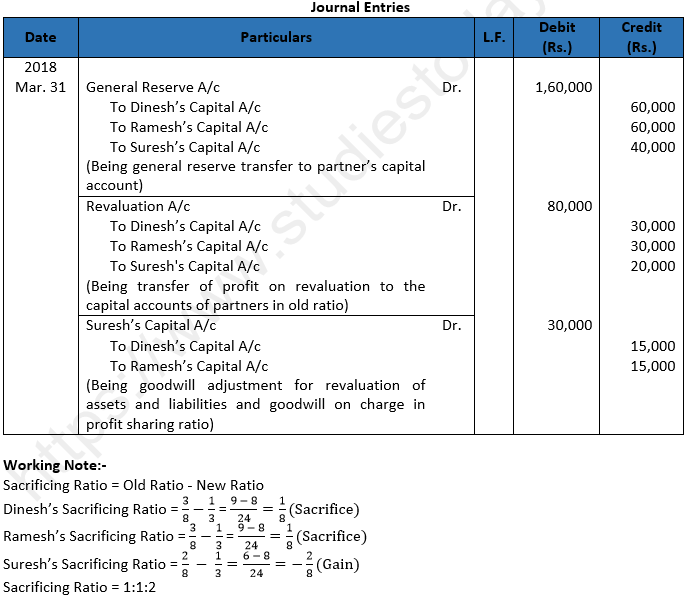

Question 11.

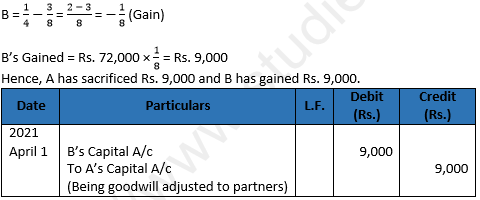

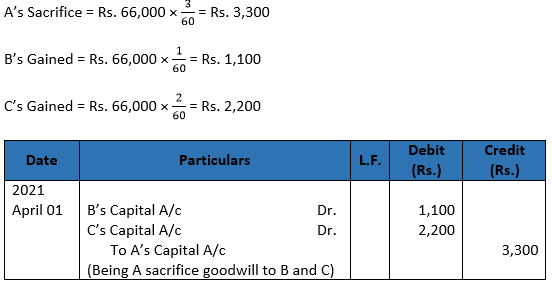

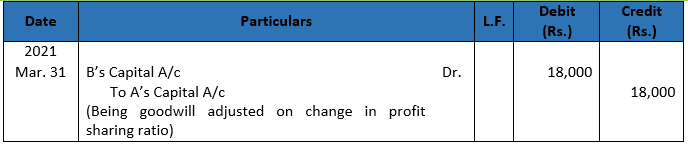

Solution 11 A change in profit sharing ratio basically implies that one partner is purchasing from another partner, a share of profit previously belonging to the latter. The purchasing or gaining partner must compensate the sacrificing partner by paying the proportionate amount of goodwill. In other word, the gaining partner should pay the sacrificing partner that share of goodwill which is equal to the share gained by him.

If the profits of the firm are Rs. 1,00,000 p.a. A will lose Rs. 20,000 and B will gain Rs. 20,000 annually. This must be compensated by B by paying to A an amount equal to 1/5 th of total value of goodwill of the firm. If the goodwill is valued at Rs. 2,50,000 i.e. Rs. 50,000. Such an adjustment is made by passing an adjustment entry wherein B’s Capital Account will be debited and A’s Capital Account will be Credited with Rs. 50,000.

Question 12.

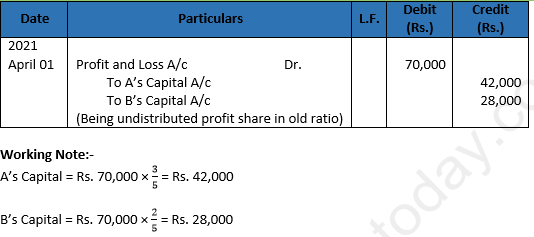

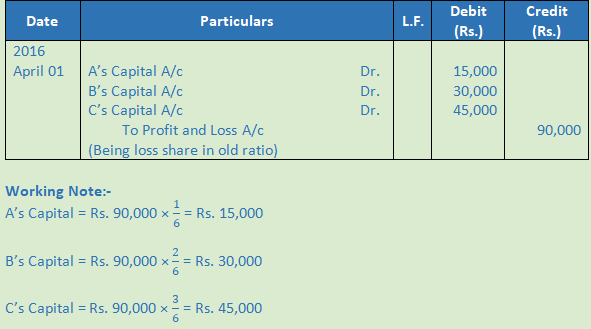

Solution 12 At the time of change in the profit sharing ratio, there are Reserves or Accumulated profits/losses existing in the books of the firm, these should be transferred to the Partner’s Capital Accounts or to Current Accounts in their old profit sharing ratio.

Question 13.

Solution 13 Yes, it is necessary to revalue Assets and liabilities of a firm must also be revalued at the time of change in profit sharing ratio of existing partners. The reason is that the realisable of actual value of assets and liabilities may be different from those shown in the balance sheet. It is possible that will the passage of time some of the assets might have appreciated in value while the value of certain other assets might have decreased and no record has been made of such changes in the books of accounts.

Question 14.

Solution 14 Reserves and accumulated profits are credited to the capital accounts of all partners in their old profit sharing ratio because they have been set apart out of the profits earned in the period before change. If they are not adjusted at present, they will get adjusted later in their new profit sharing ratio which will result in loss to the sacrificing partner and gain to the gaining partner.

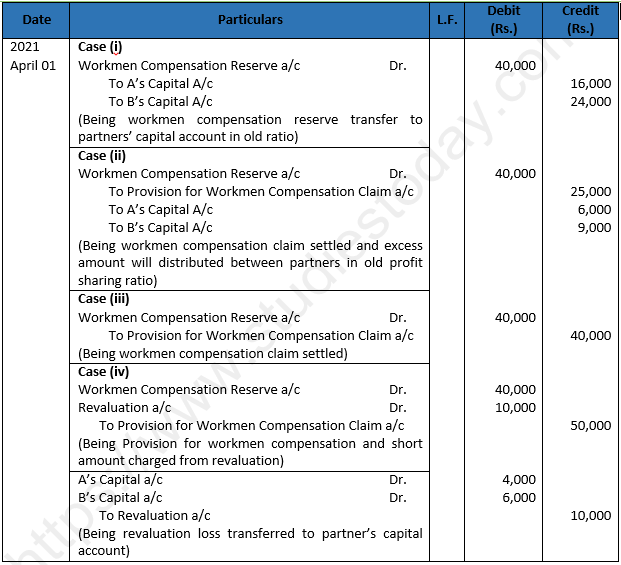

Question 15.

Solution 15 Anand would have given the argument that Workmen Compensation Reserve was created out of profits when their profit sharing ratio was 2 : 1. Hence, it should be credited in the old profit sharing ratio.

Question 16.

Solution 16 Priya would have given the argument that unrecorded asset belonged old firm when the profit sharing ratio was 2 : 1. Hence it should be Credited to Revaluation Account so that the profit on account of this asset shared in 2:1.

Question 17.

Solution 17 Dinesh must have given the argument that liability towards salaries related to the old firm when the profit sharing ratio was 3:1. Hence, it should be debited to Revaluation Account so that the loss on account of this liability could be bome 3:1. If it was recorded at the time of actual payment, the partners will bear the loss in 2:1.

Numerical Questions

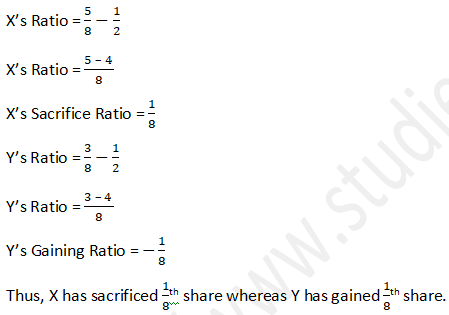

Question 1. (A)

Solution 1 (A) Old Ratio of X and Y = 5 : 3

New Ratio of X and Y = 1 : 1

Calculation of Sacrifice or Gaining Ratio =

Point of Knowledge:-

Here the negative value of is gaining and positive value is sacrificing.

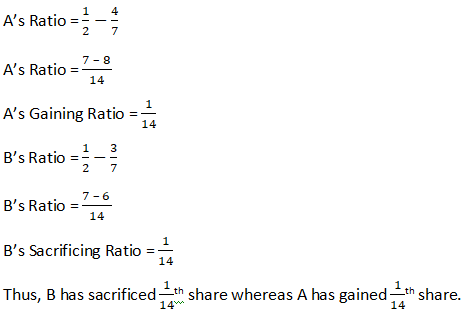

Question 1.(B)

Solution 1 (B)

Old Ratio of A and B = 1 : 1

New Ratio of A and B = 4 : 3

Calculation of Sacrifice or Gaining Ratio =

Point of Knowledge:-

Here the negative value of is gaining and positive value is sacrificing.

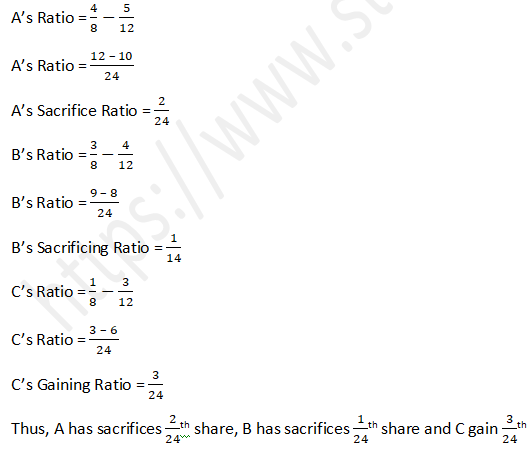

Question 2. (A)

Solution 2 (A)

Old Ratio of A, B and C = 4 : 3 : 1

New Ratio of A, B and C = 5 : 4 : 3

Calculation of Sacrificing or Gaining Ratio =

Point of Knowledge:-

Here the negative value of is gaining and positive value is sacrificing.

Question 2. (B)

Solution 2 (B)

Old Ratio of Mahesh, Naresh and Om = 2 : 3 : 4

New Ratio of Mahesh, Naresh and Om = 1 : 2 : 3

Calculation of Sacrificing or Gaining Ratio =

Point of Knowledge:-

Here the negative value of is gaining and positive value is sacrificing.

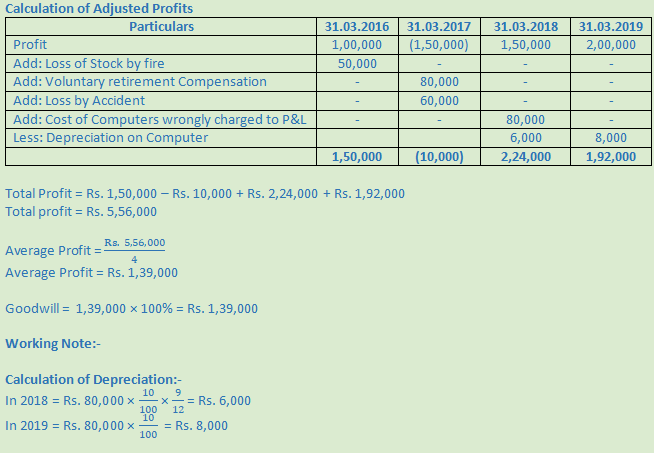

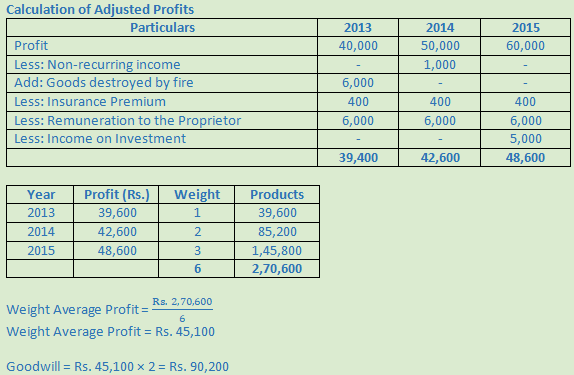

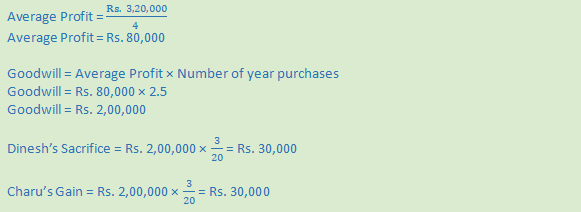

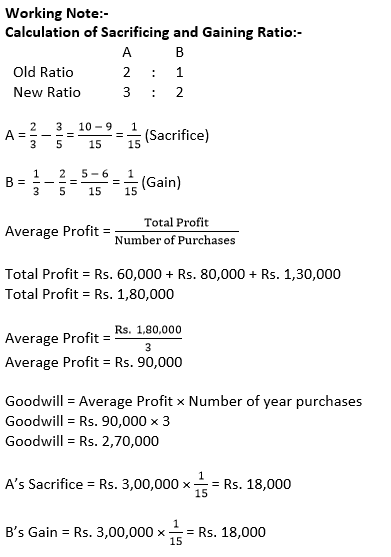

Question 3.

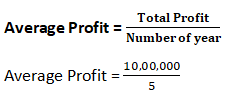

Solution 3. Total Profit = Rs. 2,00,000 – Rs. 3,00,000 + (Rs. 4,50,000 – Rs. 50,000) + Rs. 3,50,000 + Rs. 2,60,000

Total Profit = Rs. 10,00,000

Goodwill = Average Profit × Number of year purchases

Goodwill = 2,00,000 × 4

Goodwill = 8,00,000

Question 4.

Solution 4.

Question 5.

Solution 5

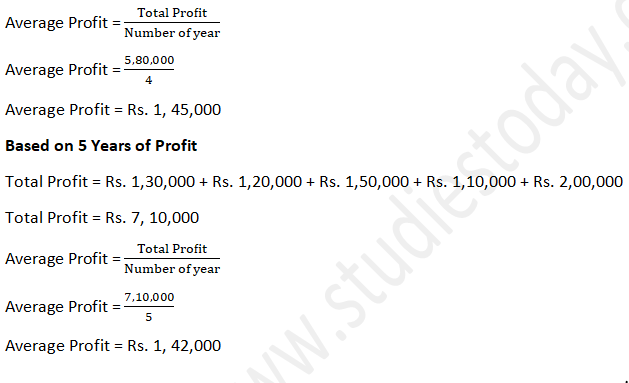

Based on 4 Years of Profit

Total Profit = Rs. 1,20,000 + Rs. 1,50,000 + Rs. 1,10,000 + Rs. 2,00,000

Total Profit = Rs. 5,80,000

Four years average profit is more than 5 years average profit. Therefore the value of goodwill will be

Goodwill = Average Profit × Number of year purchases

Goodwill = 1,45,000 × 3

Goodwill = 4,35,000

Question 6.

Solution 6

Question 7.

Solution 7

Question 8.

Solution 8.

Question 9.

Solution 9.

Question 10.

Solution 10.

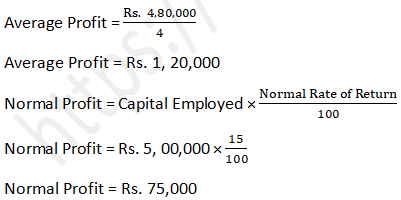

Total Profit = Rs. 80,000 + Rs. 1,00,000 + Rs. 1,20,000 + Rs. 1,80,000

Total Profit = Rs. 4,80,000

Super Profit = Actual Average Profit – Normal Profit

Super Profit = Rs. 1,20,000 – Rs. 75,000

Super Profit = Rs. 45,000

Goodwill = Super Profit × Number of year Purchases

Goodwill = Rs. 45,000 × 3

Goodwill = Rs. 1,35,000

Question 11.

Solution 11

Calculation of Actual Average Profit:-

Actual Average Profit = Average Profit + Abnormal Loss

Actual Average Profit = Rs. 41,000 + Rs. 2,000

Actual Average Profit = Rs. 43,000

Super Profit = Actual Average Profit – Normal Profit

Super Profit = Rs. 43,000 – Rs. 30,000

Super Profit = Rs. 13,000

Goodwill = Super Profit × Number of year Purchases

Goodwill = Rs. 13,000 × 5

Goodwill = Rs. 65,000

Question 12.

Solution 12

Calculation of Actual Average Profit:-

Actual Average Profit = Average Profit – Remuneration to Partners

Actual Average Profit = Rs. 1,00,000 - Rs. 10,000

Actual Average Profit = Rs. 90,000

Super Profit = Actual Average Profit – Normal Profit

Super Profit = Rs. 90,000 – Rs. 75,000

Super Profit = Rs. 15,000

Goodwill = Super Profit × Number of year Purchases

Goodwill = Rs. 15,000 × 2

Goodwill = Rs. 30,000

Question 13.

Solution 13

Goodwill = Super Profit × Number of year’s Purchases

Rs. 1,50,000 = Super Profit × 3

Super Profit = Rs. 1,50,000 ÷ 3

Super Profit = Rs. 50,000

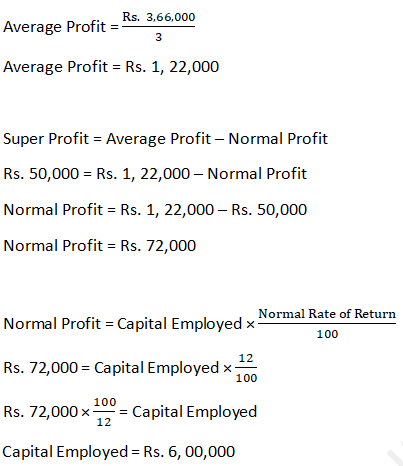

Total Profit = Rs. 80,000 + Rs. 1,30,000 + Rs. 1,56,000

Total Profit = Rs. 3,66,000

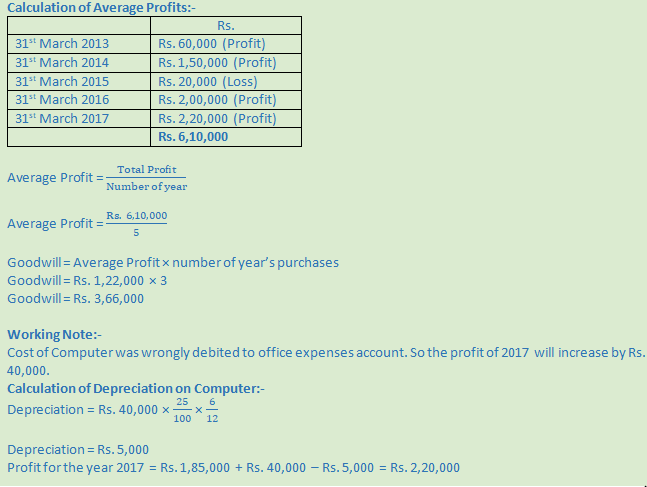

Question 14.

Solution 14

Calculation of Capital Employed

Capital Employed = Rs. 5,00,000 + Rs. 4,00,000 + Rs. 1,50,000 + Rs. 30,000

Capital Employed = Rs. 10,80,000

Super Profit = Actual Average Profit – Normal Profit

Super Profit = Rs. 2,00,000 – Rs. 1,62,000

Super Profit = Rs. 38,000

Goodwill = Super Profit × Number of year Purchases

Goodwill = Rs. 38,000 × 3

Goodwill = Rs. 1,14,000

C’s Share of Goodwill = Rs. 1,14,000 × 1/4

C’s Share of Goodwill = Rs. 28,500

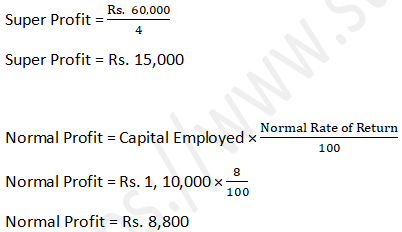

Question 15.

Solution 15

Goodwill = Super Profit × Number of year Purchases

Rs. 60,000 = Super Profit × 4

Super Profit = Average Profit – Normal Profit

Rs. 15,000 = Average Profit – Rs. 8,800

Average Profit = Rs. 15,000 + Rs. 8,800

Average Profit = Rs. 23,800

Working Note:-

Calculation of Capital Employed:-

Capital Employed = Total Assets – Current liabilities

Capital Employed = Rs. 1,20,000 – Rs. 10,000

Capital Employed = Rs. 1,10,000

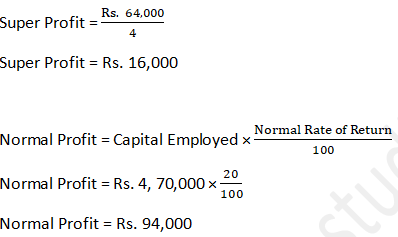

Question 16.

Solution 16

Goodwill = Super Profit × Number of year Purchases

Rs. 64,000 = Super Profit × 4

Super Profit = Average Profit – Normal Profit

Rs. 16,000 = Average Profit – Rs. 94,000

Average Profit = Rs. 16,000 + Rs. 94,000

Average Profit = Rs. 1,10,000

Working Note:-

Calculation of Capital Employed:-

Capital Employed = Total Assets – Creditors

Capital Employed = Rs. 5,00,000 – Rs. 30,000

Capital Employed = Rs. 4,70,000

Question 17.

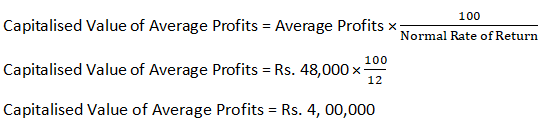

Solution 17.

Capital Employed = Assets – Liabilities

Capital Employed = Rs. 8,00,000 – Rs. 5,00,000

Capital Employed = Rs. 3,00,000

Goodwill = Capitalised Value of Average Profits – Capital Employed

Goodwill = Rs. 4,00,000 – Rs. 3,00,000

Goodwill = Rs. 1,00,000

Question 18.

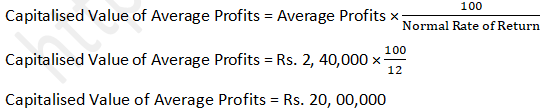

Solution 18

Capital Employed = Assets – Liabilities

Capital Employed = Rs. 6,00,000 + Rs. 5,00,000 + Rs. 5,00,000 – Rs. 60,000 – Rs. 30,000 + Rs. 10,000

Capital Employed = Rs. 15,20,000

Goodwill = Capitalised Value of Average Profits – Capital Employed

Goodwill = Rs. 20,00,000 – Rs. 15,20,000

Goodwill = Rs. 4,80,000

Question 19.

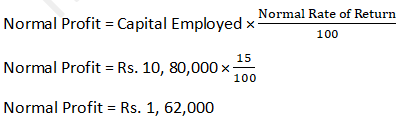

Solution 19 Capital Employed = Assets – Liabilities

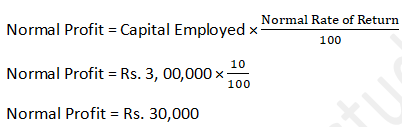

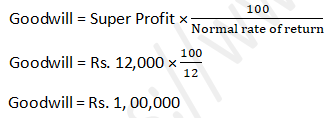

Capital Employed = Rs. 8,00,000 – Rs. 5,00,000

Capital Employed = Rs. 3,00,000

Normal Profit = Rs. 3,00,000 × 12%

Normal Profit = Rs. 36,000

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 48,000 – Rs. 36,000

Super Profit = Rs. 12,000

Question 20.

Solution 20

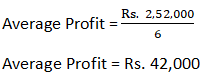

Total Profit = Rs. 20,000 + Rs. 60,000 – Rs. 10,000 + Rs. 60,000 + Rs. 50,000 + Rs. 72,000

Total Profit = Rs. 2,52,000

(i) Four year's purchase of average profits:

Value of goodwill at 4 year’s purchase of average profits = Rs. 42,000 × 4 = Rs 1,68,000

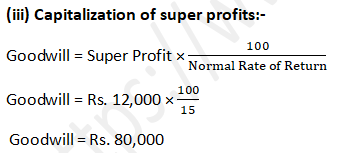

(ii) Four year’s purchases of super profits:

Normal Profit = Rs. 2,00,000 × 15%

Normal Profit = Rs. 30,000

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 42,000 – Rs. 30,000

Super Profit = Rs. 12,000

Value of Goodwill at 4 year’s Purchases of Super profit = Rs. 12,000 × 4 = Rs. 48,000

Question 21.

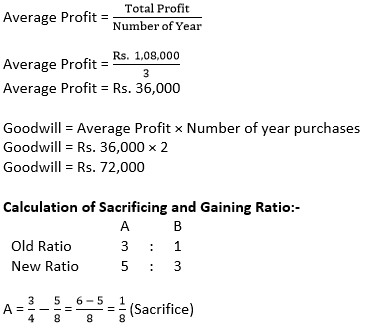

Solution 21 Total Profit = Rs. 36,000 + Rs. 32,000 + Rs. 40,000

Total Profit = Rs. 1,08,000

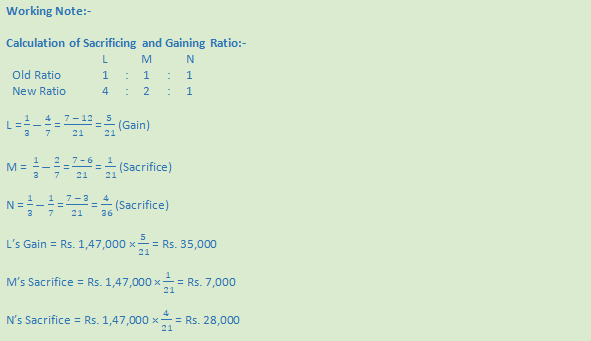

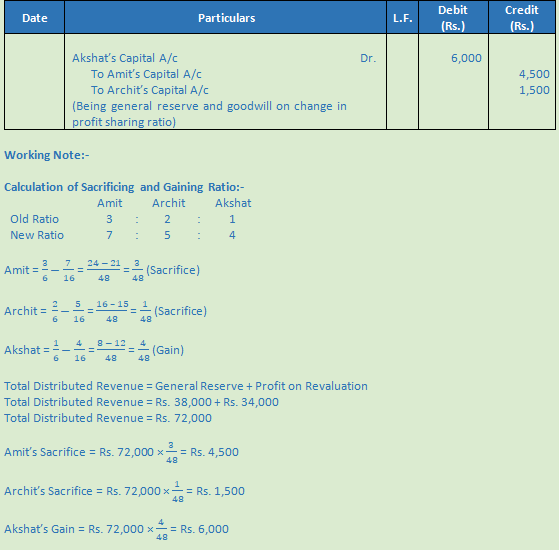

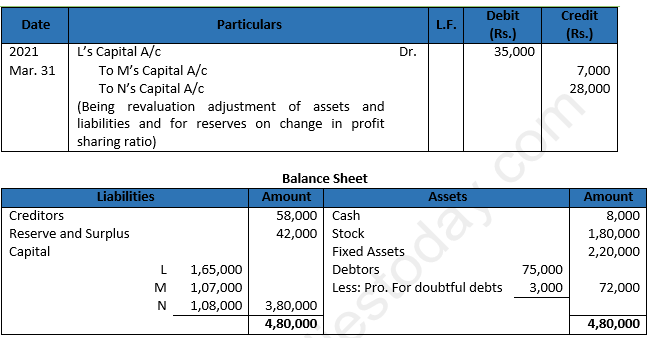

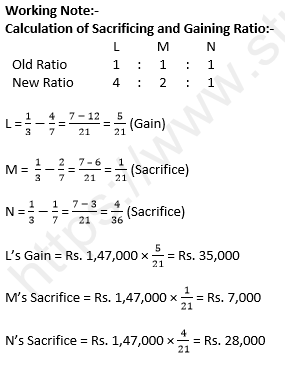

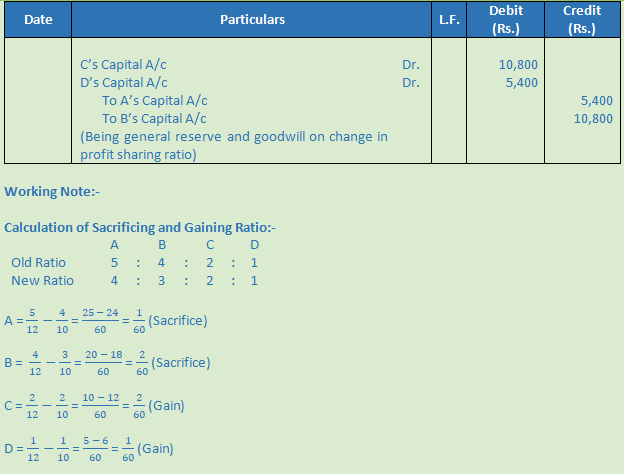

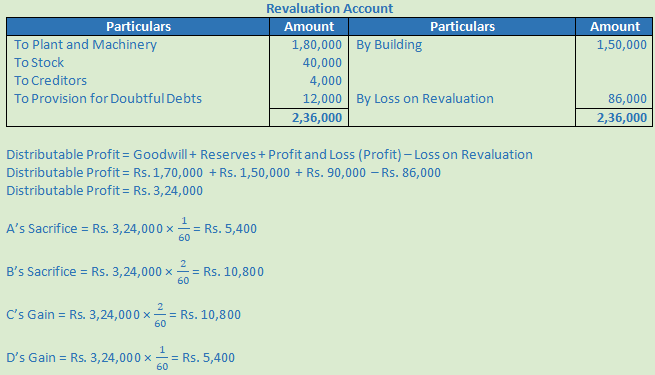

Question 22.

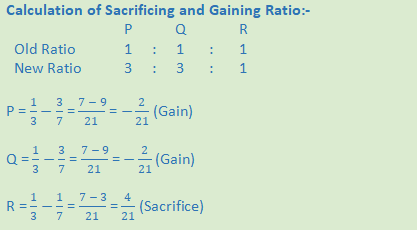

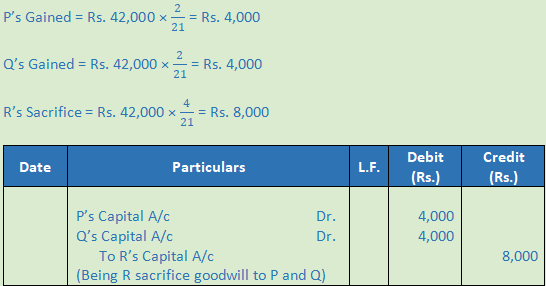

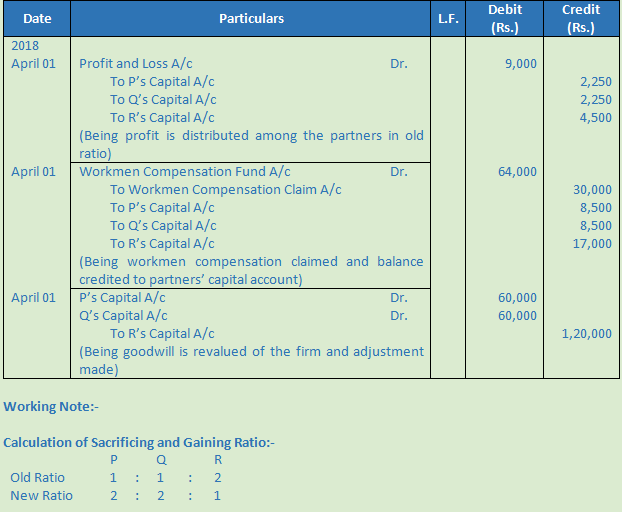

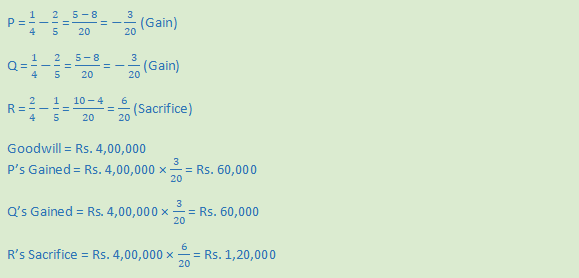

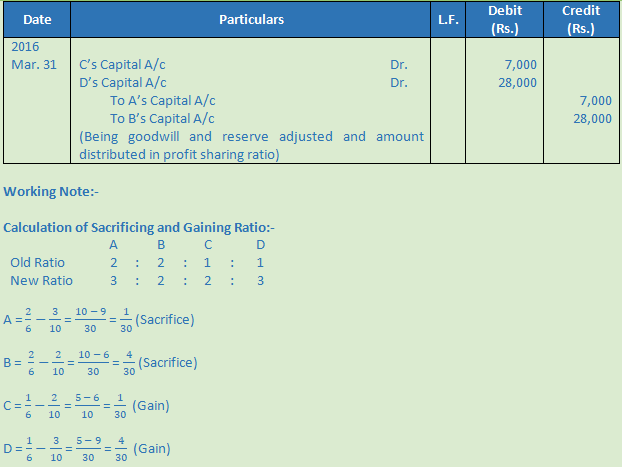

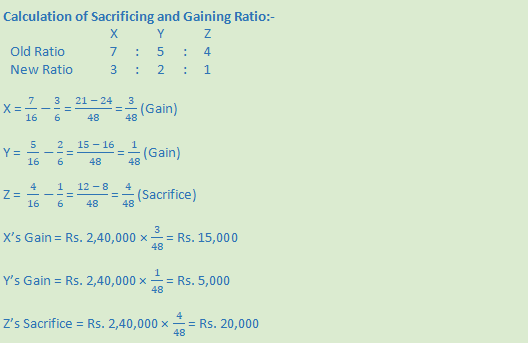

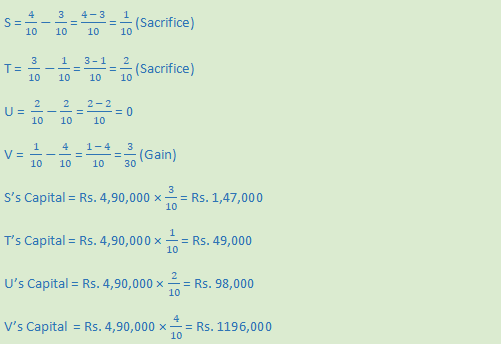

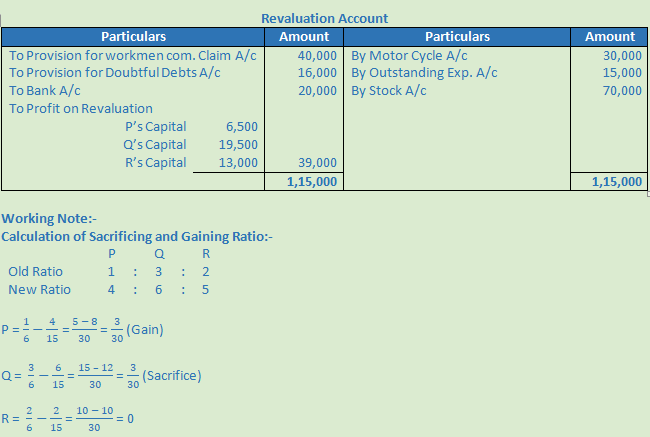

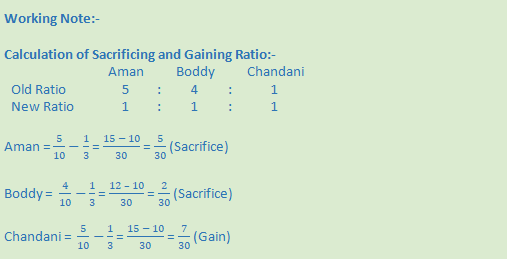

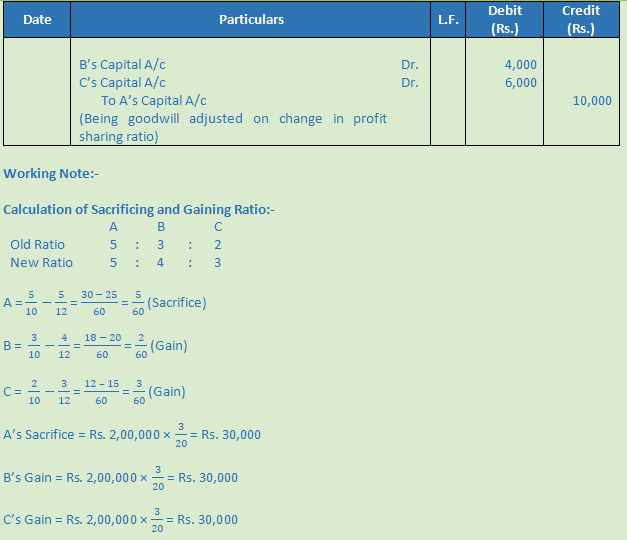

Solution 22 Calculation of Sacrificing and Gaining Ratio:-

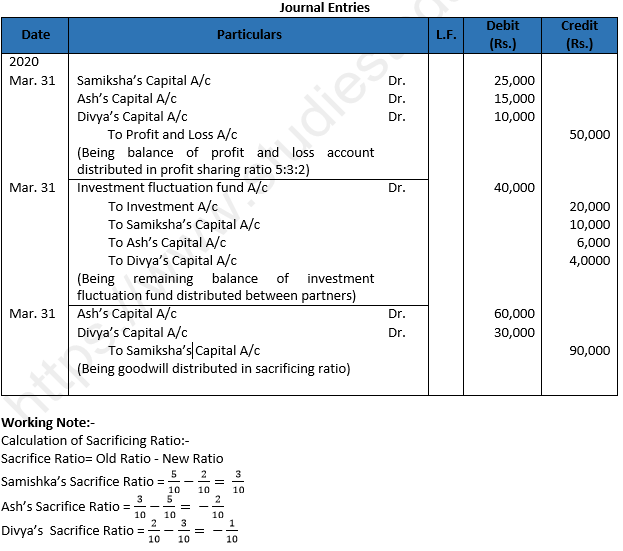

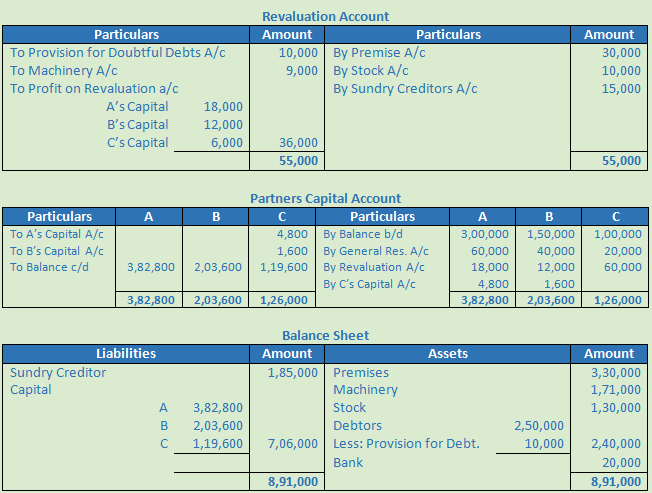

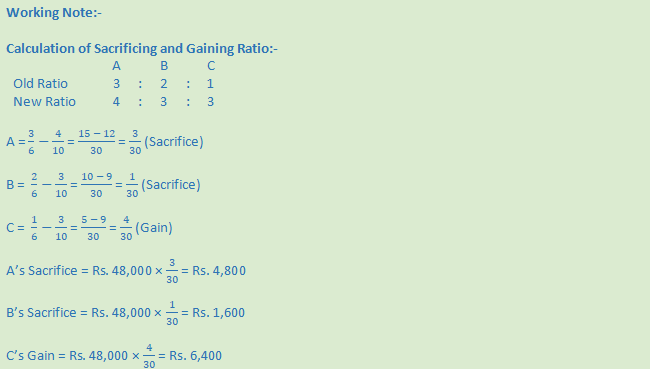

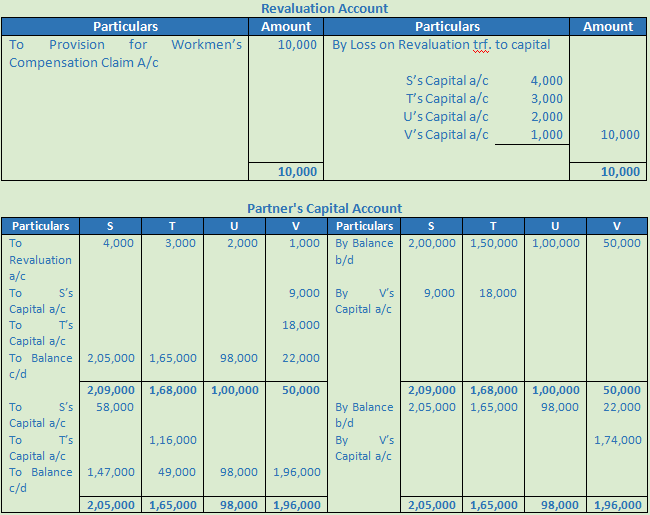

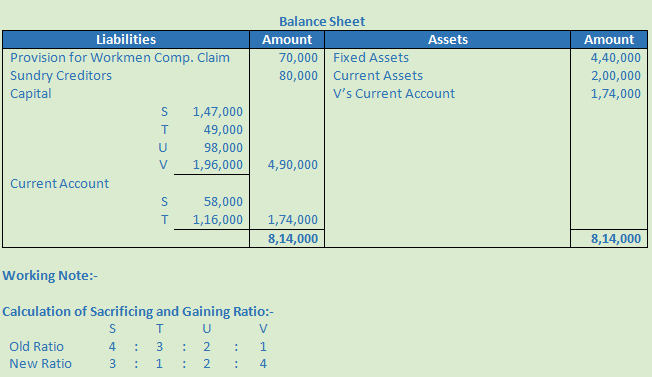

Question 23.

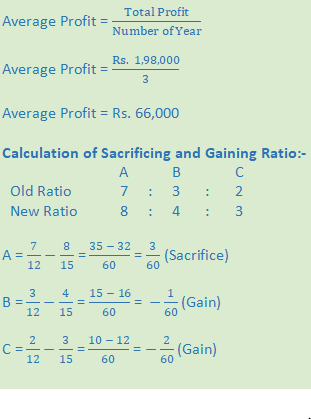

Solution 23 Total Profit = Rs. 48,000 + Rs. 60,000 + Rs. 90,000

Total Profit = Rs. 1,98,000

Question 24.

Solution 24

Question 25.

Solution 25.

Question 26.

Solution 26

Question 27.

Solution 27

Question 28.

Solution 28

Question 29.

Solution 29

Question 30.

Solution 30.

Question 31.

Solution 31

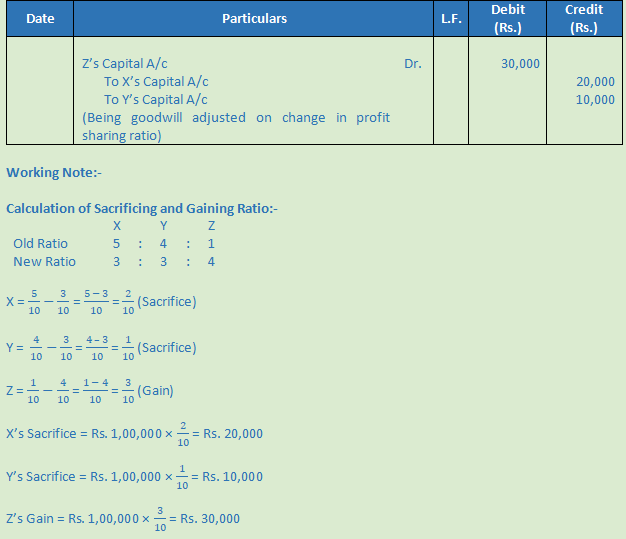

Question 32. (A)

Solution 32 (A)

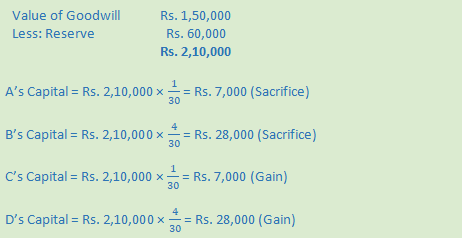

Question 32. (B)

Solution 32 (B)

Varun = 3/5-2/3 = (9 - 10)/15 = 1/15 (Gain)

Arun will Sacrifice for Varun = Rs. 4,50,000 × 1/15 = Rs. 30,000

Question 33.

Solution 33

Question 34.

Solution 34

Question 35.

Solution 35

Question 36.

Solution 36

Question 37.

Solution 37

Question 38.

Solution 38

Question 39.

Solution 39

Question 40 (new).

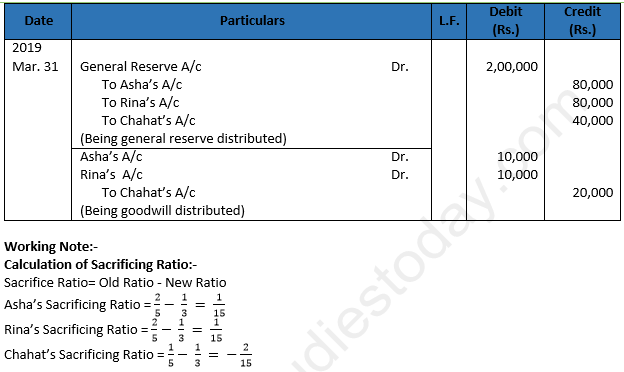

Solution 40 (new). Working Note:-

Calculation of Sacrificing Ratio:-

Sacrifice Ratio= Old Ratio - New Ratio

Question 40.

Solution 40

Question 41.

Solution 41

Question 42. (new).

Solution 42 (new).

Question 42.

Solution 42

Question 43.

Solution 43

Question 44.

Solution 44

Question 45.

Solution 45

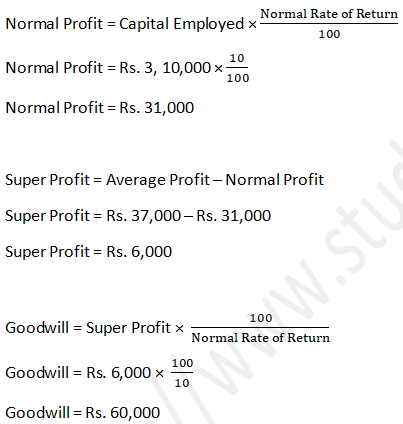

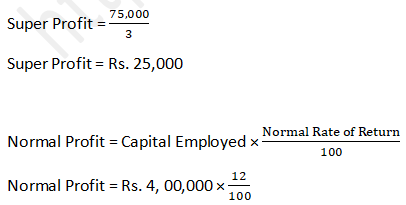

Normal Profit = Capita Employed × Normal Rate of Return

Normal Profit = Rs. 7,00,000 × 7/100

Normal Profit = Rs. 49,000

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 80,000 – Rs. 49,000

Super Profit = Rs. 31,000

Goodwill = Super Profit × Number of Year’s Purchase

Goodwill = Rs. 31,000 × 5

Goodwill = Rs. 1,55,000

Working Note:-

Adjustment Profit = Average Profit earned by the firm + Under Valuation of Stock

Adjustment Profit = Rs. 75,000 + Rs. 5,000

Adjustment Profit = Rs. 80,000

Question 46.

Solution 46

Question 47.

Solution 47

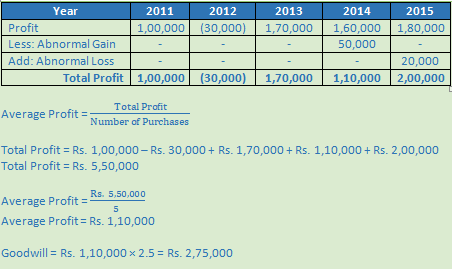

Question 48 (new).

Solution 48 (new).

Average Profit = (Total Profit)/(Number of Purchases )

Total Profit = Rs. 1,00,000 – Rs. 30,000 + Rs. 1,70,000 + Rs. 1,10,000 + Rs. 2,00,000

Total Profit = Rs. 5,50,000

Average Profit = (Rs. 5,50,000)/(5 )

Average Profit = Rs. 1,10,000

Goodwill = Rs. 1,10,000 × 2.5 = Rs. 2,75,000

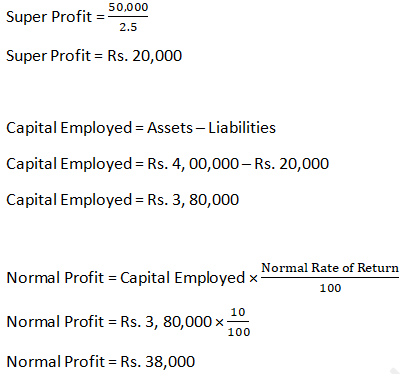

Question 48.

Solution 48

Working Note:-

Capital Employed = Assets – Liabilities

Capital Employed = Rs. 4,00,000 – Rs. 90,000

Capital Employed = Rs. 3,10,000

Question 49.

Solution 49

Goodwill = Super Profit × Number of year purchases

50,000 = Super Profit × 2.5

Super Profit = Average Profit – Normal Profit

Rs. 25,000 = Average Profit – Rs. 38,000

Average Profit = Rs. 25,000 + Rs. 38,000

Average Profit = Rs. 63,000

Question 50.

Solution 50

Goodwill = Super Profit × Number of year purchases

75,000 = Super Profit × 3

Normal Profit = Rs. 48,000

Super Profit = Average Profit – Normal Profit

Rs. 20,000 = Average Profit – Rs. 48,000

Average Profit = Rs. 48,000 + Rs. 20,000

Average Profit = Rs. 68,000

Question 51.

Solution 51

(i) Value of Goodwill on the basis of two year’s purchase of Super profits:

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 1,20,000 – Rs. 60,000

Super Profit = Rs. 60,000

Goodwill = Super Profit × Number of year purchases

Goodwill = Rs. 60,000 × 2

Goodwill = Rs. 1,20,000

Goodwill = Capitalised Value of Average Profit – Net Assets

Goodwill = Rs. 8,00,000 – Rs. 4,00,000

Goodwill = Rs. 4,00,000

Question 52.

Solution 52

Normal Profit = Rs. 20,00,000 × 12% = Rs. 2,40,000

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 3,00,000 – Rs. 2,40,000

Super Profit = Rs. 60,000

Question 53 (new). Yash and Karan were partners in an interior designer firm. Their fixed capitals were Rs. 6,00,000 and Rs. 4,00,000 respectively. There were credit balances in their current accounts of Rs. 4,00,000 and Rs. 5,00,000 respectively. The firm had a balance of Rs. 1,00,000 in General Reserve. The firm did not have any liability. They admitted Radhika into partnership for 1/4th share in the profits of the firm. The average profits of the firm for the last five years were Rs. 5,00,000. Calculate the value of goodwill of the by capitalization of average profit method. The normal rate of return in the business is 10%.

Solution 53 (new). Calculation of Goodwill:-

Average profit of the firm = Rs. 5,00,000

Capitalised value of business = Rs. 50,00,000

Net Assets = All Assets – Outside liabilities

Net Assets = Rs. 6,00,000 + Rs. 4,00,000 + Rs. 4,00,000 + Rs. 5,00,000 + Rs. 1,00,000

Net Assets = Rs. 20,00,000

Capitalisation of average profit method:-

Goodwill = Capitalised value of business – Net Assets

Goodwill = Rs. 50,00,000 – Rs. 20,00,000

Goodwill = Rs. 30,00,000

Question 53.

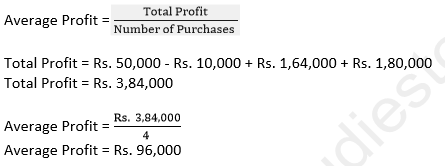

Solution 53

(i) Three year’s purchase of average profit:-

Goodwill = Average Profit × Number of year purchases

Goodwill = Rs. 96,000 × 3

Goodwill = Rs. 2,88,000

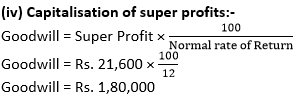

(ii) Three year’s purchase of super profit:-

Normal Profit = Rs. 6,20,000 × 12% = Rs. 74,400

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 96,000 – Rs. 74,400

Super Profit = Rs. 21,600

Goodwill = Super Profit × Number of year purchases

Goodwill = Rs. 21,600 × 3

Goodwill = Rs. 64,800

Question 54 (new).

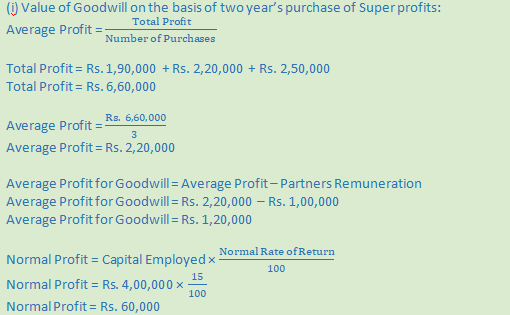

Solution 54 (new). (i) Value of Goodwill on the basis of two year’s purchase of Super profits:

Average Profit = Total / number of purchases

Total Profit = Rs. 1,90,000 + Rs. 2,20,000 + Rs. 2,50,000

Total Profit = Rs. 6,60,000

Average Profit = Rs. 6,60,000 / 3

Average Profit = Rs. 2,20,000

Average Profit for Goodwill = Average Profit – Partners Remuneration

Average Profit for Goodwill = Rs. 2,20,000 – Rs. 1,00,000

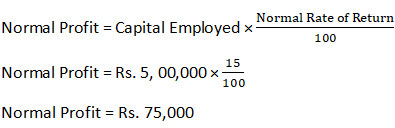

Average Profit for Goodwill = Rs. 1,20,000

Normal Profit = Capital Employed × Noramal Rate of Return / 100

Normal Profit = Rs. 4,00,000 × 15 / 100

Normal Profit = Rs. 60,000

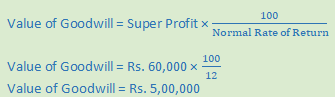

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 1,20,000 – Rs. 60,000

Super Profit = Rs. 60,000

Goodwill = Super Profit × Number of year purchases

Goodwill = Rs. 60,000 × 2

Goodwill = Rs. 1,20,000

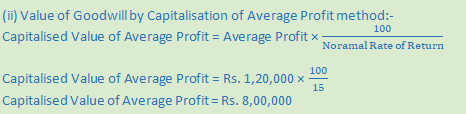

(ii) Value of Goodwill by Capitalisation of Average Profit method:-

Capitalised Value of Average Profit = Average Profit × 100 / Noramal Rate of Return

Capitalised Value of Average Profit = Rs. 1,20,000 × 100 / 15

Capitalised Value of Average Profit = Rs. 8,00,000

Goodwill = Capitalised Value of Average Profit – Net Assets

Goodwill = Rs. 8,00,000 – Rs. 4,00,000

Goodwill = Rs. 4,00,000

Question 54.

Solution 54

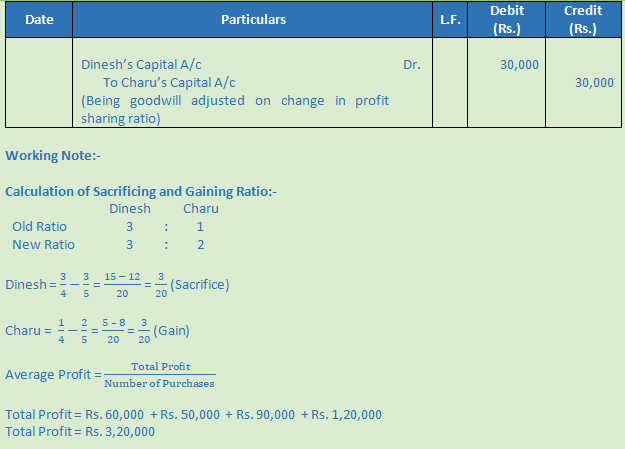

Question 55.

Solution 55

Question 56 (new).

Solution 56 (new).

(i) Three year’s purchase of average profit:-

Goodwill = Average Profit × Number of year purchases

Goodwill = Rs. 96,000 × 3

Goodwill = Rs. 2,88,000

(ii) Three year’s purchase of super profit:-

Normal Profit = Rs. 6,20,000 × 12% = Rs. 74,400

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 96,000 – Rs. 74,400

Super Profit = Rs. 21,600

Goodwill = Super Profit × Number of year purchases

Goodwill = Rs. 21,600 × 3

Goodwill = Rs. 64,800

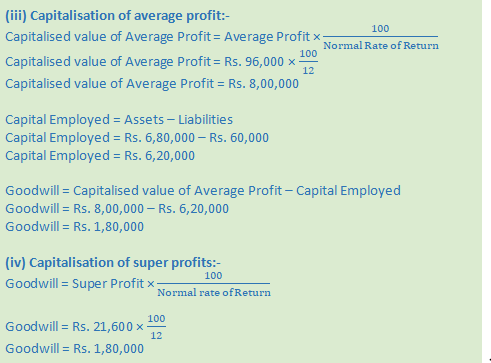

Capitalised value of Average Profit = Rs. 8,00,000

Capital Employed = Assets – Liabilities

Capital Employed = Rs. 6,80,000 – Rs. 60,000

Capital Employed = Rs. 6,20,000

Goodwill = Capitalised value of Average Profit – Capital Employed

Goodwill = Rs. 8,00,000 – Rs. 6,20,000

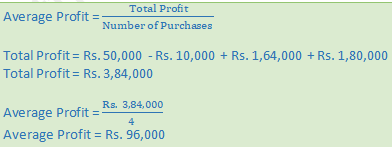

Goodwill = Rs. 1,80,000

Question 56.

Solution 56

Question 57.

Solution 57

Question 58.

Solution 58

Question 59.

Solution 59

Question 60 (new).

Solution 60 (new).

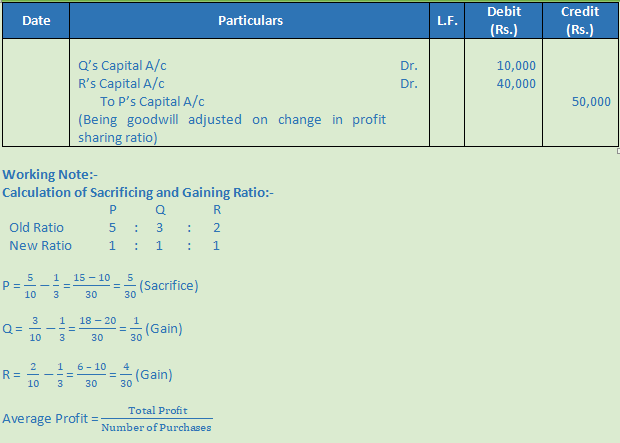

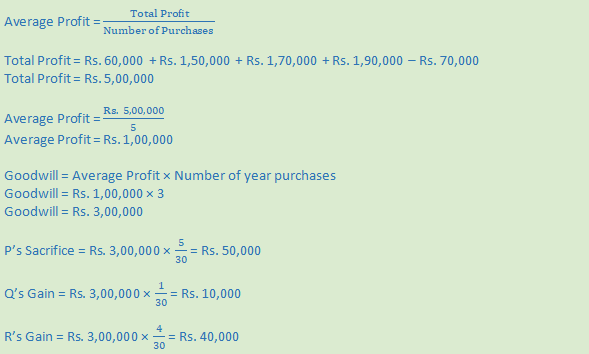

Total Profit = Rs. 60,000 + Rs. 1,50,000 + Rs. 1,70,000 + Rs. 1,90,000 – Rs. 70,000

Total Profit = Rs. 5,00,000

Question 60.

Solution 60

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 1,08,000 – Rs. 66,000

Super Profit = Rs. 42,000

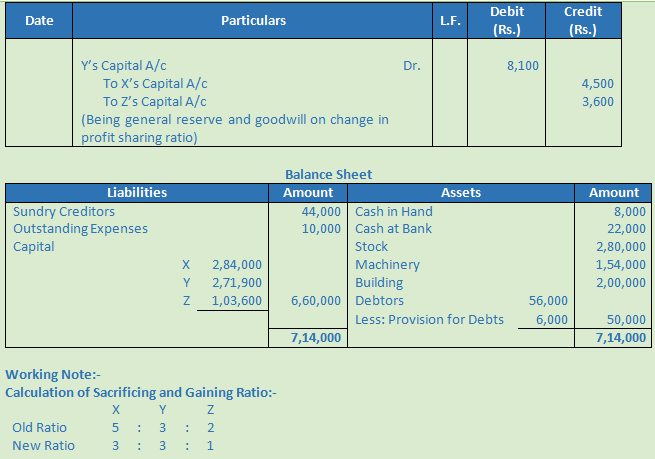

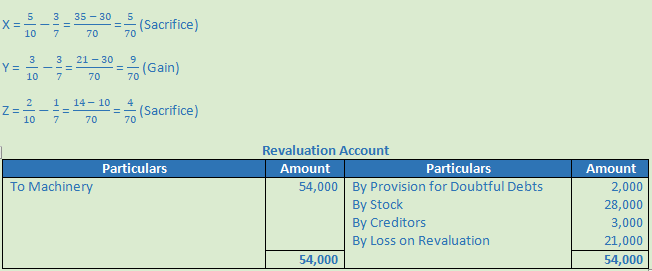

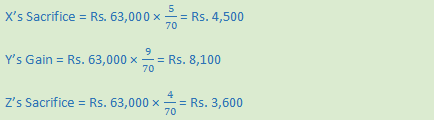

Goodwill = Super Profit × Number of year purchases

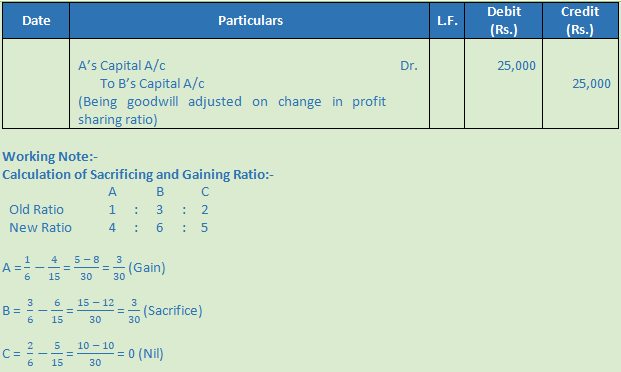

Goodwill = Rs. 42,000 × 2

Goodwill = Rs. 84,000

Distributable Profit = Goodwill – Loss on Revaluation

Distributable Profit = Rs. 84,000 – Rs. 21,000

Distributable Profit = Rs. 63,000

Question 61 (new).

Solution 61 (new).

Question 61.

Solution 61

Question 62 (new).

Solution 62 (new).

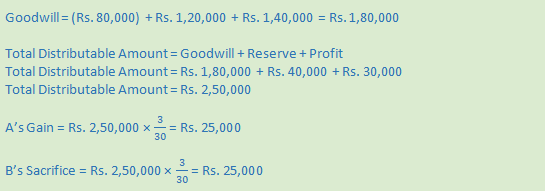

Goodwill = (Rs. 80,000) + Rs. 1,20,000 + Rs. 1,40,000 = Rs. 1,80,000

Total Distributable Amount = Goodwill + Reserve + Profit

Total Distributable Amount = Rs. 1,80,000 + Rs. 40,000 + Rs. 30,000

Total Distributable Amount = Rs. 2,50,000

Question 62.

Solution 62

Question 63 (new).

Solution 63 (new).

Question 64 (new).

Solution 64 (new).