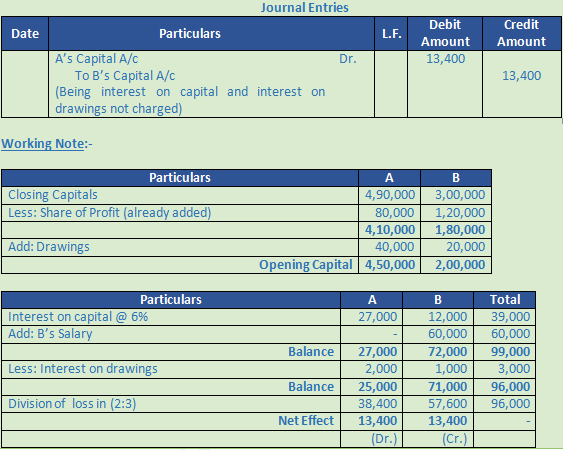

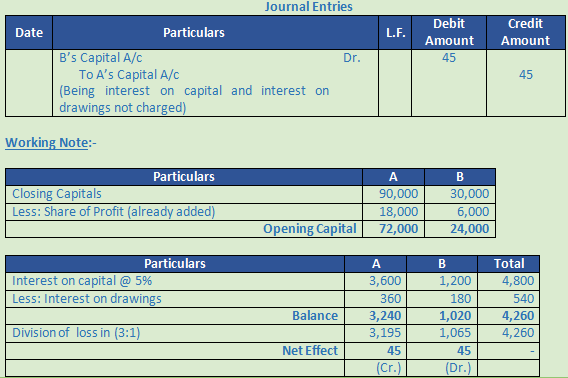

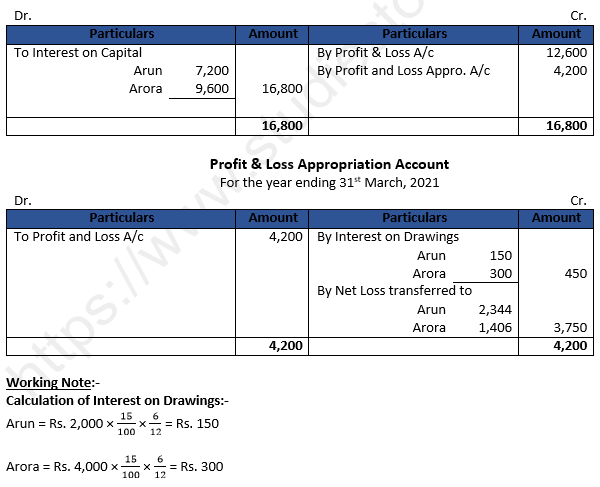

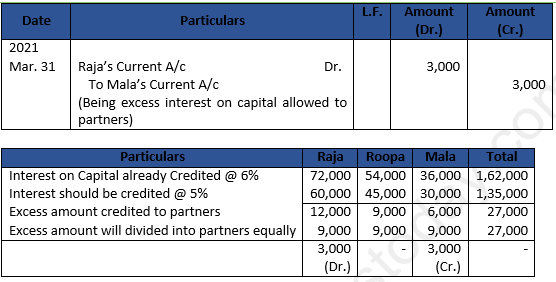

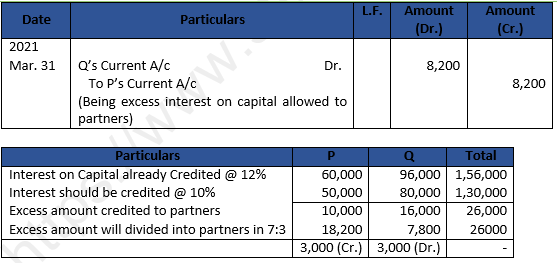

Read DK Goel Class 12 Accountancy Solutions for Chapter 2 Accounting for Partnership Firms Fundamentals below. These DK Goel Accountancy Class 12 solutions have been prepared based on the latest book for DK Goel Class 12 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 12 Solutions help commerce students in class 12 understand accountancy and build a strong base in accounts. Students in Class 12 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 2 Accounting for Partnership Firms Fundamentals should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 12 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 2 Accounting for Partnership Firms Fundamentals DK Goel Class 12 Solutions

Class 12 Accountancy students should read the following DK Goel Solutions for Class 12 Chapter 2 Accounting for Partnership Firms Fundamentals in Standard 12. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 12 Accountancy will be very useful for exams and help you to score good marks in Class 12 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 12.

DK Goel Solutions Chapter 2 Accounting for Partnership Firms Fundamentals Class 12 Accountancy

Short Answer Questions

Question 1.

Solution 1.

1.) Sharing of Profit/Losses:- Profit/Losses are shared equally by the partners.

2.) Interest on Capital:- Interest on capital is not paid to partners.

3.) Interest on Drawings:- Interest on drawings in not charged from partners.

4.) Interest on Loan:- Interest at the rate of 6% p.a. is to be allowed on a partner’s loan to the firm. Such interest shall be paid even if there are losses to the firm.

Question 2.

Solution 2.

Below are the provisions of the partnership Act, in the absence of Partnership Deed:-

1.) If all the partners agree, a minor may be admitted for the benefit of partnership.

2.) A person may be admitted as a partner either with the consent of all the existing partners or in accordance with an express agreement among the partners.

3.) Registration of the firm is optional and not compulsory.

4.) A partner may retire from the firm either with the consent of all the other partners or in accordance with an express agreement among the partners.

Question 3.

Solution 3.

1.) Salaries of Partners

2.) Commission of Partners

3.) Interest on Partners Capital

4.) Interest on Partners Drawings

5.) Profit transferred to Capital account

6.) Net Profit transferred from P&L account

Question 4.

Solution 4.

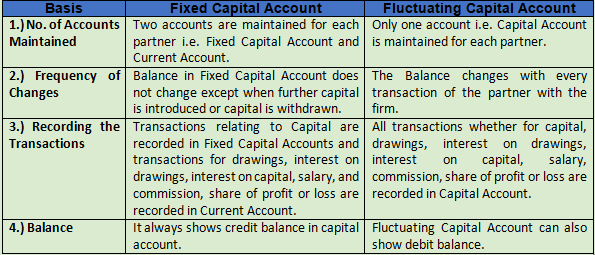

(a) Fixed Capitals and Fluctuating Capitals

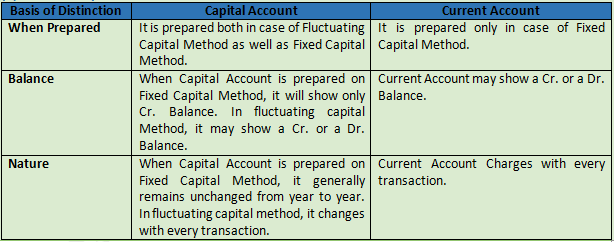

(b) Partner’s Capital Accounts and Current Accounts

Question 5.

Solution 5.

(a) Salaries of Partners:- No partner is entitled to any salary or commission for taking part in running the firm’s business.

(b) Interest on Partner’s Capital:- No interest on Capital shall be allowed to the partners.

(c) Interest on Loan:- Interest at the rate of 6% p.a. is to be allowed on a partner’s loan to the firm. Such interest shall be paid even if there are losses to the firm.

(d) Profit sharing ratio:- Profit and losses are to be shared equally irrespective of their capital contribution.

(e) Interest on Partner’s drawings:- No interest is to be charged on drawings.

Question 6.

Solution 6.

(a) Debit of Current A/c

(b) Credit of Current A/c

(c) Credit of Capital A/c

(d) Credit of Current A/c

(e) Debit to Current A/c

Question 7.

Solution 7. Below are the items appears on the debit side of the Capital Account of partner when the capitals are fluctuating:-

(1) Drawings

(2) Interest on Drawings

(3) Share of loss

(4) Loss on revolution

(5) Any assets taken by partner

(6) Closing Cr. Balance of the Capital

Question 8.

Solution 8. Below are the items that may appear on the credit side of the Capital Account of a partner when the capitals are fluctuating:-

(1) Opening credit balance of Capital

(2) Additional Capital introduced

(3) Share of profit

(4) Interest on capital

(5) Salary to a partner

Question 9.

Solution 9. In the absence of a partnership deed, the under mentioned provisions of the Partnership Act, 1932 will be applicable:-

(1) Profit and losses are to be shared equally.

(2) No interest is to be allowed on capitals.

(3) No interest is to be charged on drawings.

(4) No partner is entitled to any salary of commission for taking part in running the firm’s business.

(5) A partner is entitled to interest at the rate of 6% per annum on the loan given by him to the firm.

(6) Each partner can participate in the conduct of business.

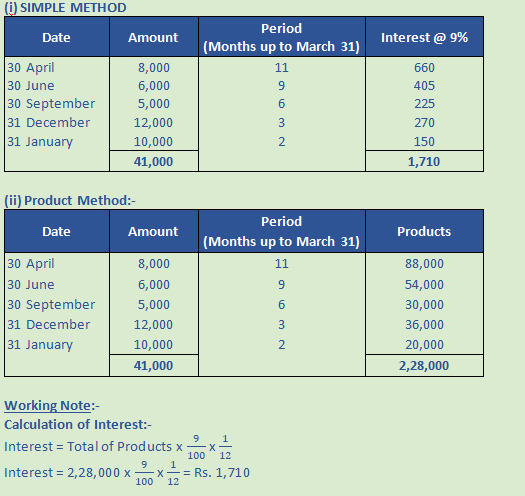

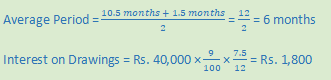

Question 10.

Solution 10. When drawings of equal amounts are made on the first day of every month, interest would be calculated on the total amount of drawings for 6 1/2 months. Thus,

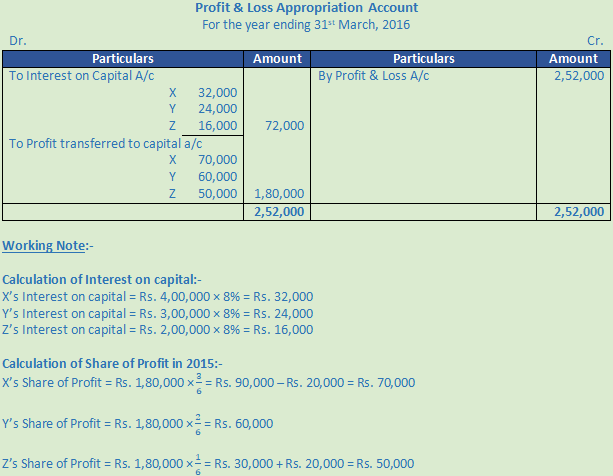

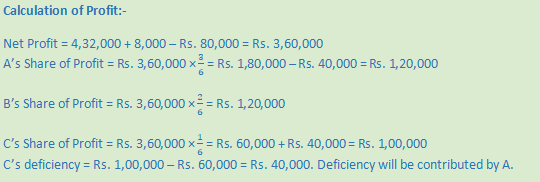

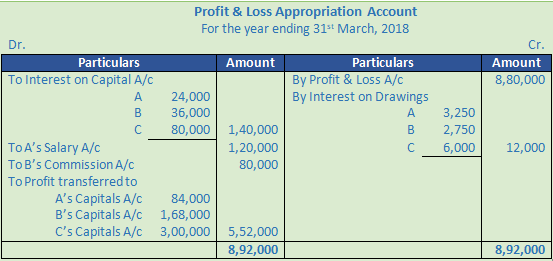

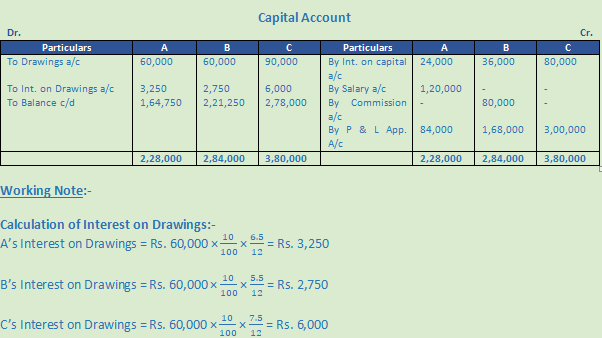

![]()

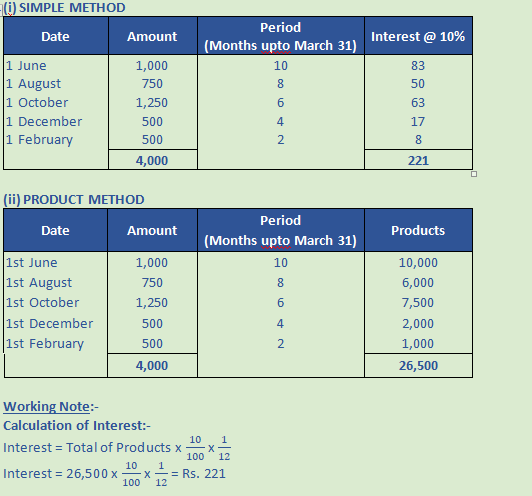

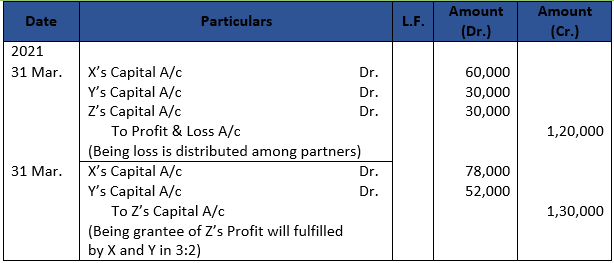

Question 11.

Solution 11. When drawings of equal amounts are made on the last day of every month, interest would be calculated on the total amount of drawings for 5 1/2 months. Thus,

![]()

Question 12.

Solution 12. When drawings of equal amounts are made in the middle of every month, interest would be calculated on the total amount of drawings for 6 months. Thus,

![]()

Question 13 (new).

Solution 13 (new). In the absence of partnership deed, the provision of partnership act 1932 will apply according to which:

1. No interest is payable on capitals.

2. Interest on loan by partner will be paid @ 6% p.a.

3. Profit will be shared equally.

4. No salary is payable to any partner.

Question 13.

Solution 13.

(i) Profit will be shared equally.

(ii) B will not get the salary.

Question 14.

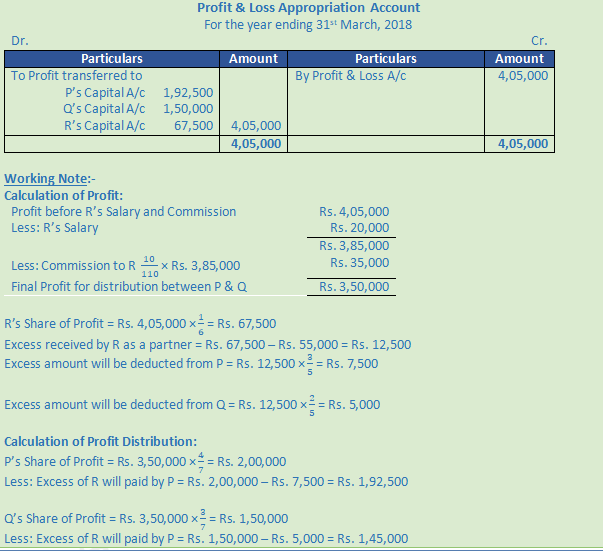

Solution 14.

(i) B will be given interest on his loan @ 6% p.a.

(ii) In the absence of any agreement of the contrary, profit will be shared equally, irrespective of their capitals.

Question 15.

Solution 15.

(a) No interest on capital will be allowed.

(b) X is not entitled to any salary

(c) X’s son cannot be admitted as a partner, if Y objects it.

(d) X is entitled to claim interest on his loan @ 6% p.a.

Question 16.

Solution 16.

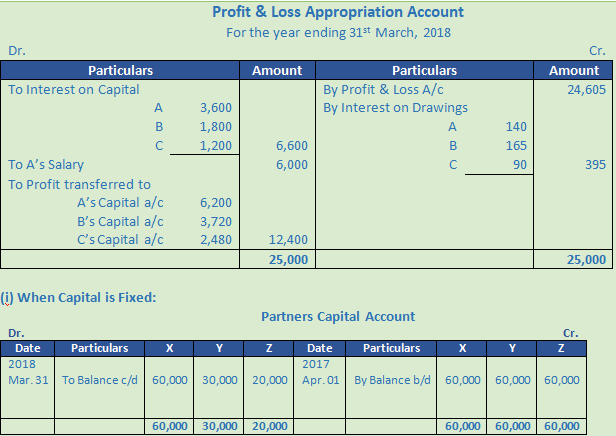

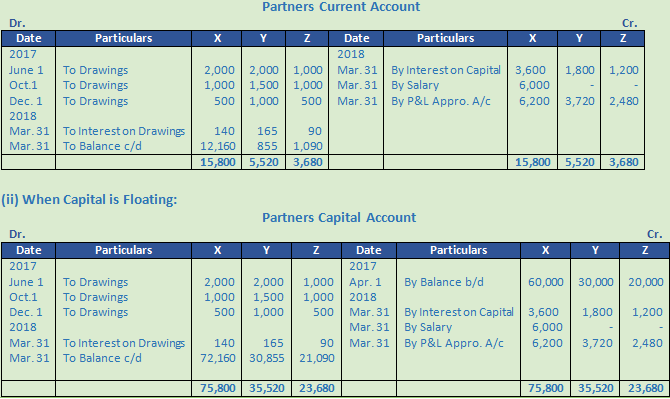

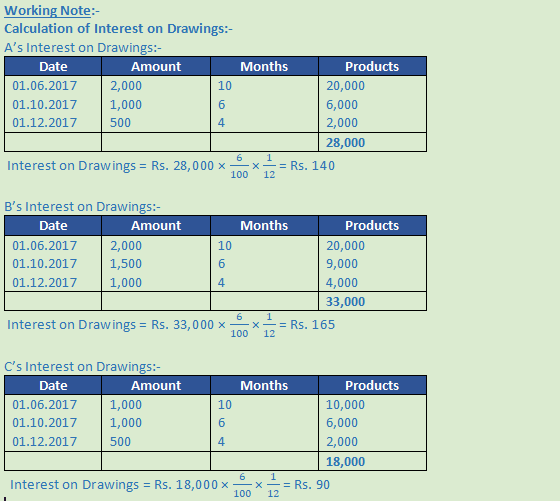

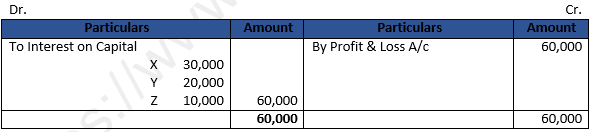

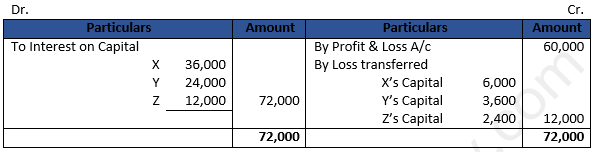

(a) A must return Rs. 1,75,000

(b) A must return Rs. 50,000;

(c) Mohan cannot be admitted

(d) Goods may be purchased from Raghubir.

Numerical Questions:-

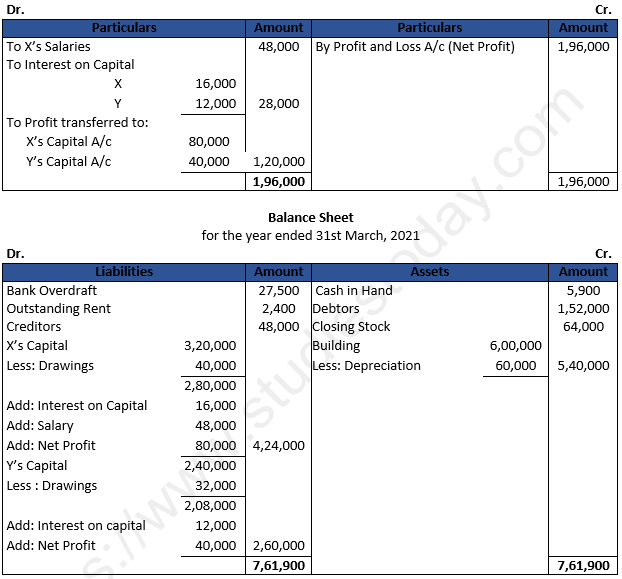

Question 1.

Solution 1.

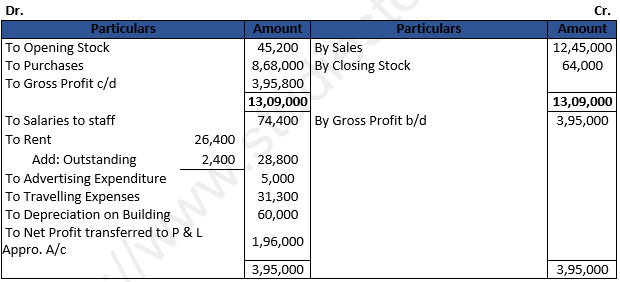

Trading and Profit and loss account

for the year ended 31st March, 2021

Question 2.

Solution 2.

Calculation of Interest on Capital For Girish:-

Capital for 4 months = Rs. 5,60,000

Rate of interest = 6%

Interest on Capital = Rs. 5,60,000 × 6% × 4/12

Interest on Capital = Rs. 11,200

Capital for 8 months = Rs. 5,00,000

Rate of interest = 6%

Interest on Capital = Rs. 5,00,000 × 6% × 8/12

Interest on Capital = Rs. 20,000

Total Interest on Capital paid to Girish = Rs. 11,200 + Rs. 20,000

Total Interest on Capital paid to Girish = Rs. 31,200

Calculation of Interest on Capital For Satish:-

Capital for 4 months = Rs. 4,75,000

Rate of interest = 6%

Interest on Capital = Rs. 4,75,000 × 6% × 4/12

Interest on Capital = Rs. 9,500

Capital for 8 months = Rs. 5,00,000

Rate of interest = 6%

Interest on Capital = Rs. 5,00,000 × 6% × 8/12

Interest on Capital = Rs. 20,000

Total Interest on Capital paid to Satish = Rs. 9,500 + Rs. 20,000

Total Interest on Capital paid to Satish = Rs. 29,500

Question 3.

Solution 3

Calculation of Interest on Capital For X:-

Capital for 3 months = Rs. 5,00,000

Rate of interest = 8%

Interest on Capital = Rs. 5,00,000 × 8% × 3/12

Interest on Capital = Rs. 10,000

Capital for 9 months = Rs. 6,00,000

Rate of interest = 8%

Interest on Capital = Rs. 6,00,000 × 8% × 9/12

Interest on Capital = Rs. 36,000

Total Interest on Capital paid to X = Rs. 10,000 + Rs. 36,000

Total Interest on Capital paid to X = Rs. 46,000

Calculation of Interest on Capital For Y:-

Capital for 3 months = Rs. 4,00,000

Rate of interest = 8%

Interest on Capital = Rs. 4,00,000 × 8% × 3/12

Interest on Capital = Rs. 8,000

Capital for 7 months = Rs. 4,80,000

Rate of interest = 8%

Interest on Capital = Rs. 4,80,000 × 8% × 7/12

Interest on Capital = Rs. 22,400

Capital for 2 months = Rs. 4,65,000

Rate of interest = 8%

Interest on Capital = Rs. 4,65,000 × 8% × 2/12

Interest on Capital = Rs. 6,200

Total Interest on Capital paid to Y = Rs. 8,000 + Rs. 22,400 + Rs. 6,200

Total Interest on Capital paid to Y = Rs. 36,600

Calculation of Interest on Capital For Z:-

Capital for 3 months = Rs. 3,00,000

Rate of interest = 8%

Interest on Capital = Rs. 4,00,000 × 8% × 3/12

Interest on Capital = Rs. 6,000

Capital for 9 months = Rs. 3,50,000

Rate of interest = 8%

Interest on Capital = Rs. 4,80,000 × 8% × 9/12

Interest on Capital = Rs. 21,000

Total Interest on Capital paid to Y = Rs. 6,000 + Rs. 21,000

Total Interest on Capital paid to Y = Rs. 27,000

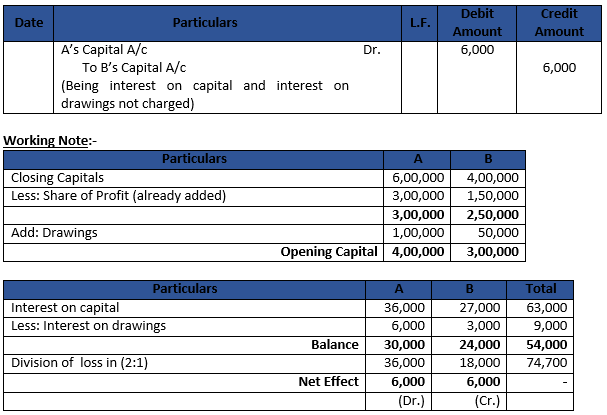

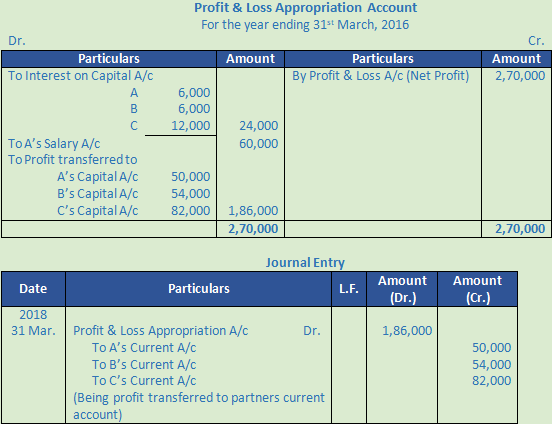

Question 4.

Solution 4 Calculation of Capital in the beginning of the year:-

Mountain:-

Capital at the end of the year on March 31, 2016 = Rs. 4,00,000

Add:- Drawings = Rs. 20,000

Less:- Share of Profit = Rs. 50,000

Capital in the beginning on 1st April, 2015 = Rs. 4,00,000 + Rs. 20,000 – Rs. 50,000 = Rs. 3,70,000

Calculation of Interest on Capital:-

Calculation of Interest on Capital = Rs. 3,70,000 × 10%

Calculation of Interest on Capital = Rs. 37,000

Hill:-

Capital at the end of the year on March 31, 2016 = Rs. 3,00,000

Add:- Drawings = Rs. 15,000

Less:- Share of Profit = Rs. 50,000

Capital in the beginning on 1st April, 2015 = Rs. 3,00,000 + Rs. 15,000 – Rs. 50,000 = Rs. 2,65,000

Calculation of Interest on Capital:-

Calculation of Interest on Capital = Rs. 2,65,000 × 10%

Calculation of Interest on Capital = Rs. 26,500

Rock:-

Capital at the end of the year on March 31, 2016 = Rs. 2,00,000

Add:- Drawings = Rs. 10,000

Less:- Share of Profit = Rs. 50,000

Capital in the beginning on 1st April, 2015 = Rs. 2,00,000 + Rs. 10,000 – Rs. 50,000 = Rs. 1,60,000

Calculation of Interest on Capital:-

Calculation of Interest on Capital = Rs. 1,60,000 × 10%

Calculation of Interest on Capital = Rs. 16,000

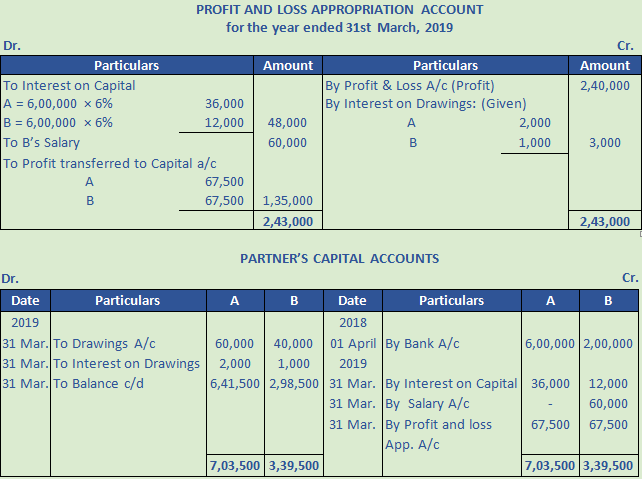

Question 5. (A)

Solution 5. (A)

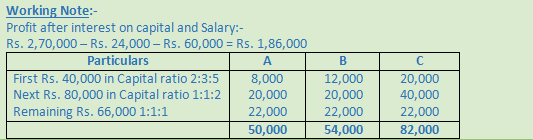

Working Note:-

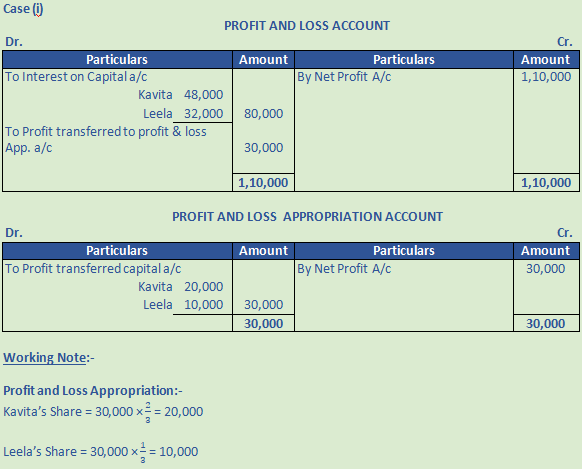

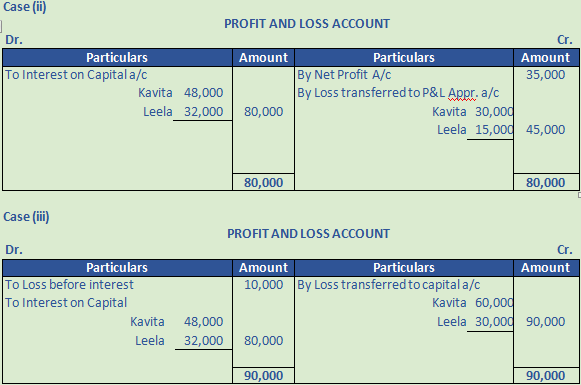

Profit will be distributed in equal ratio = 1 : 1

A’s Profit = Rs. 1,35,000 × 1/2 = Rs. 67,500

B’s Profit = Rs. 1,35,000 ×1/2 = Rs. 67,500

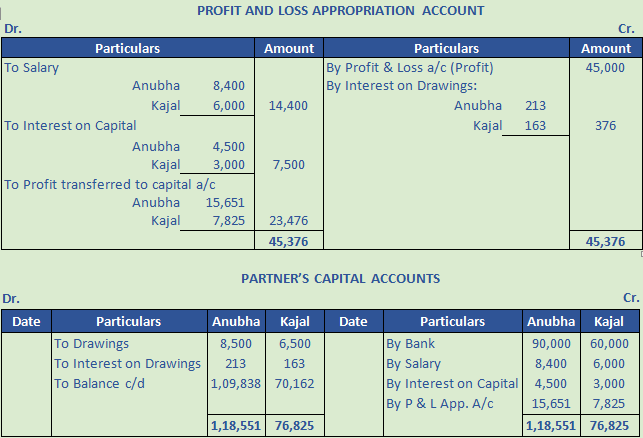

Question 5. (B)

Solution 5 (B).

Working Note:-

1. Salary of Anubha = Rs. 700 × 12 = 8,400

Salary of Kajal = Rs. 500 × 12 = 6,000

Question 6.

Solution 6.

PROFIT AND LOSS ACCOUNT

for the year ended 31st March, 2021

Working Note:-

1. B’s Salary = Rs. 2,500 × 12 = 30,000

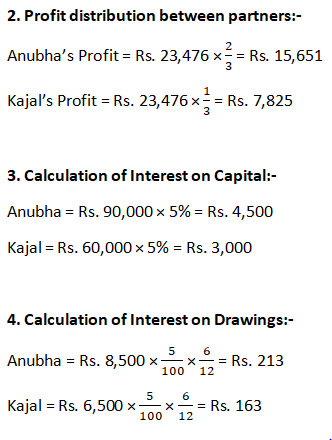

2. Profit distribution between partners:-

Anubha’s Profit = Rs. 1,20,000 × 3/5 = Rs. 72,000

Kajal’s Profit = Rs. 1,20,000 × 2/5 = Rs. 48,000

3. Calculation of Interest on Capital:-

A = Rs. 6,00,000 × 6% = Rs. 36,000

B = Rs. 4,00,000 × 6% = Rs. 24,000

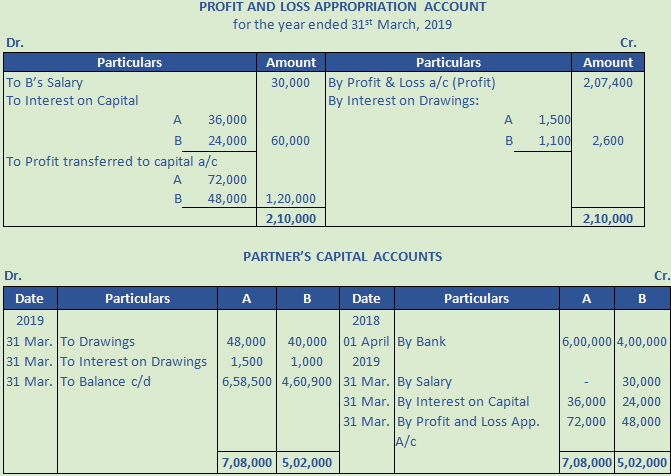

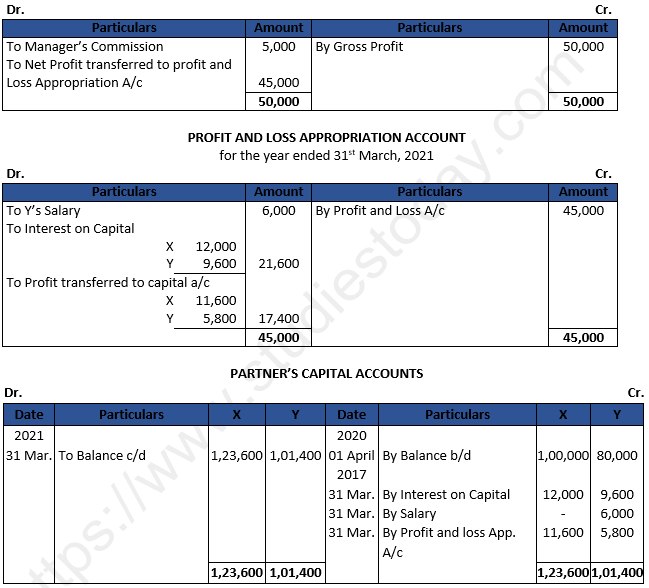

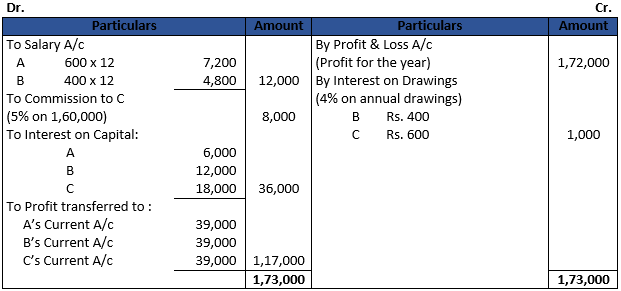

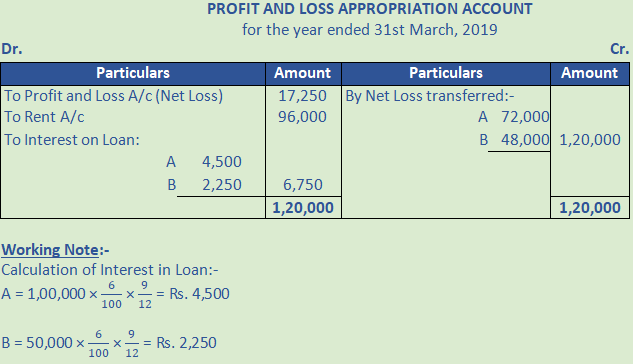

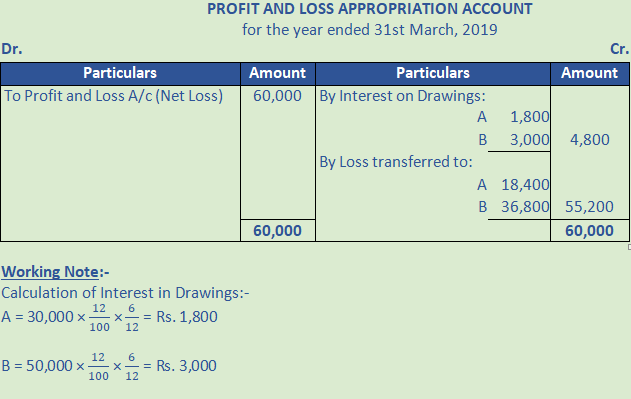

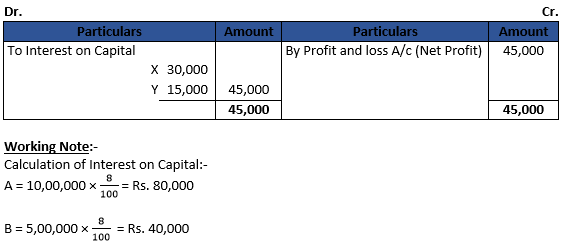

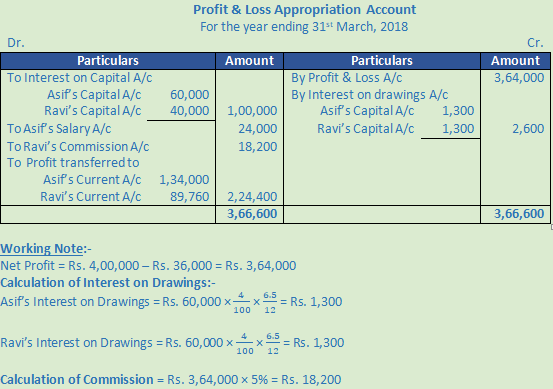

Question 7.

Solution 7.

PROFIT AND LOSS ACCOUNT

for the year ended 31st March, 2021

Working Note:-

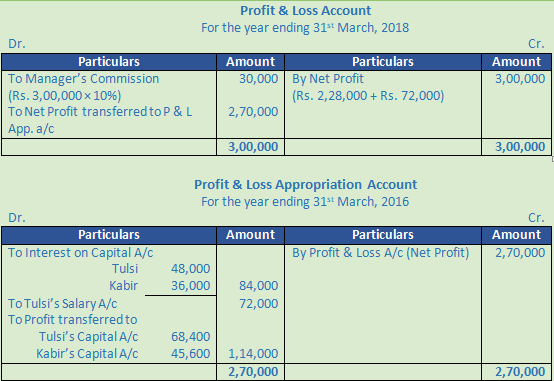

1. Calculation of Manager’s Commission = Rs. 50,000 × 10% = Rs. 5,000

2. Calculation of Interest on Capital:-

X = Rs. 1,00,000 × 12% = Rs. 12,000

Y = Rs. 80,000 × 12% = Rs. 9,600

3. Profit distribution between partners:-

X’s Profit = Rs. 17,400 × 2/3 = Rs. 11,600

Y’s Profit = Rs. 17,400 × 1/3 = Rs. 5,800

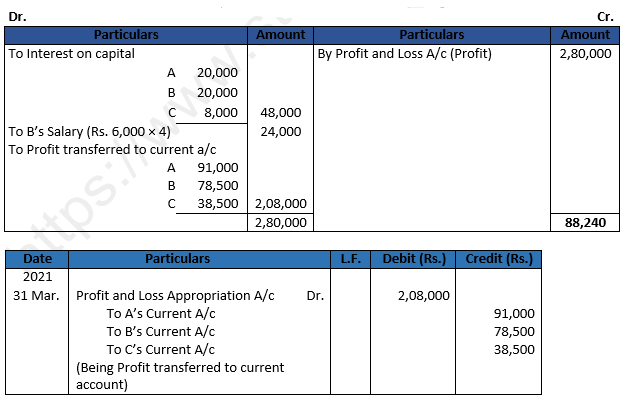

Question 8.

Solution 8.

PROFIT AND LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2021

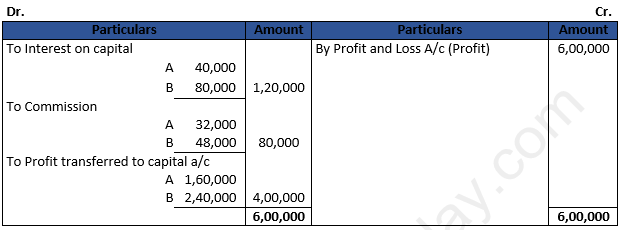

Question 9.

Solution 9.

PROFIT AND LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2020

Working Note:-

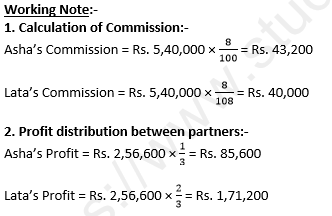

Calculation of Partner’s Commission:-

Profit after charging Interest on capital = Rs. 6,00,000 – Rs. 1,20,000 = Rs. 4,80,000

B’s Commission = Rs. 4,80,000 × 10/100 = Rs. 48,000

Profit after charging Interest on capital and B’s Commission = Rs. 6,00,000 – Rs. 1,20,000 – Rs. 48,000

Profit after charging Interest on capital and B’s Commission = Rs. 4,32,000

A’s Commission (after charging B’s commission own commission) = Rs. 4,32,000 × 8/108 = Rs. 32,000

Question 10.

Solution 10.

PROFIT AND LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2021

Question 11.

Solution 11.

Question 11. (B)

Solution 11. (B) Calculation of Adjustment of Capital:-

Total capital of the firm = Rs. 2,10,000 + Rs. 90,000 = Rs. 3,00,000

Profit sharing ratio = 2:1

A’s Capital will be = Rs. 3,00,000 × 2/3 = Rs. 2,00,000

B’s Capital will be = Rs. 3,00,000 × 1/3 = Rs. 1,00,000

Hence, on 1st August, 2016 A withdraw Rs. 10,000 and B will introduce additional capital of Rs. 10,000.

Question 12.

Solution 12.

PROFIT AND LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2021

Working Note:-

1. Calculation of Interest on Capital:-

A = Rs. 2,00,000 × 10% = Rs. 20,000

B = Rs. 2,00,000 × 10% = Rs. 20,000

C = Rs. 80,000 × 10% = Rs. 8,000

2. Calculation of Profit and Loss:-

Capital Ratio = 2,00,000 : 2,00,000 : 80,000

Capital Ratio = 5 : 5 : 2

Profit = 2,80,000 – 48,000 – Rs. 24,000

Profit = 2,08,000

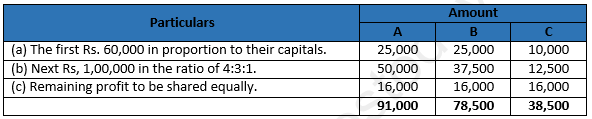

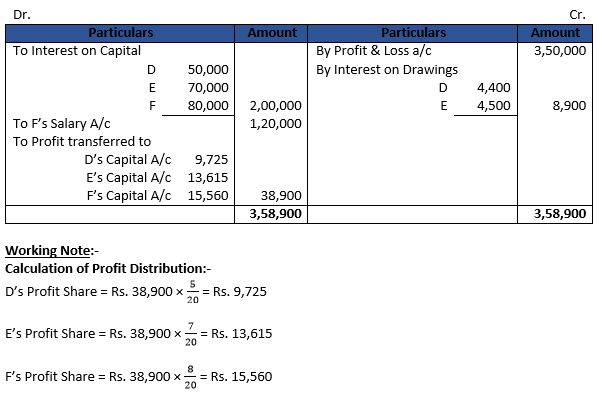

Question 13.

Solution 13.

PROFIT AND LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2021

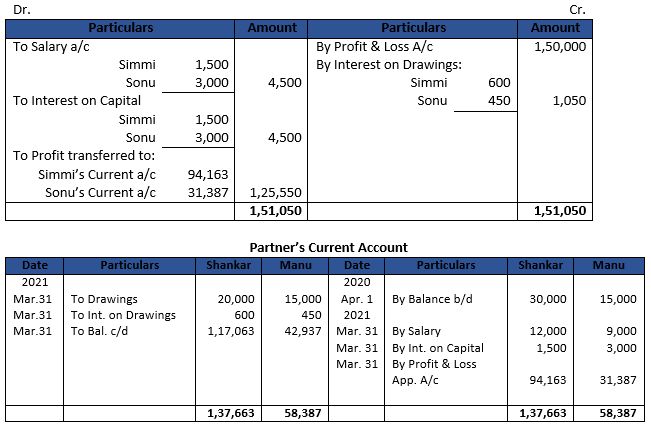

Question 14.

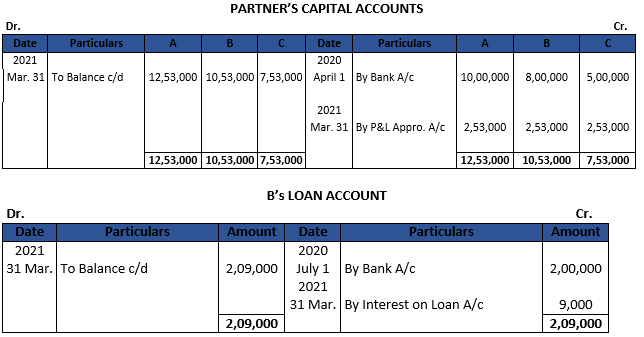

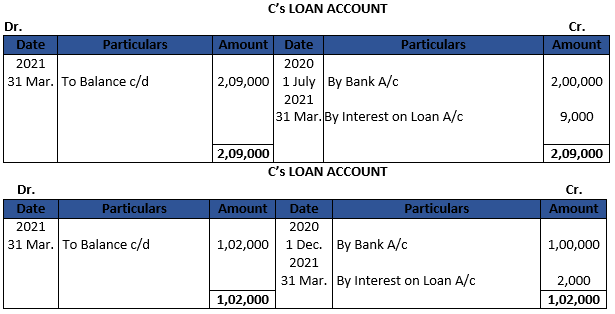

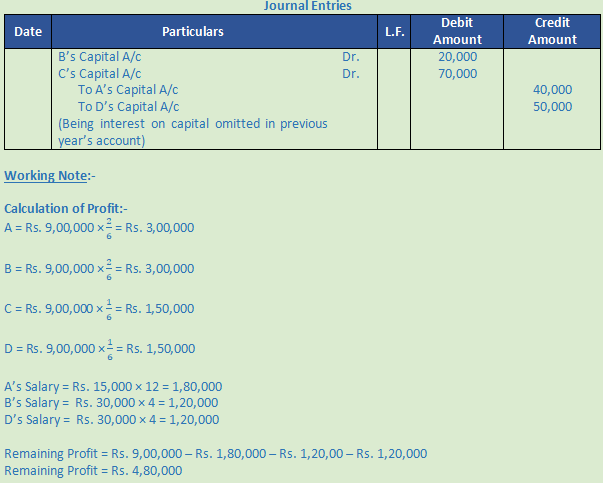

Solution 14. The Profit and Loss Account for the year ended 31.03.2021 disclosed a profit of Rs. 7,70,000 but the partners could not agree upon the rate of interest on loans and the profit sharing ratio. Prepare partner’s Capital account and Loan’s accounts.

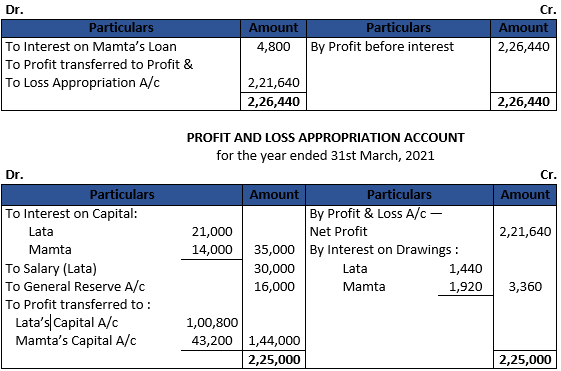

Question 15.

Solution 15.

PROFIT AND LOSS ACCOUNT

for the year ended 31st March, 2021

Working Notes:-

(1) Interest on Mamta’s Loan has been calculated at 6% p.a.

(2) Interest on Drawings has been calculated for an average period of 6 months.

(3) Distributable Profit = Total of Credit side – Debit Side

Total Credit Side = Rs. 2,25,000

Total of Debit side (Rs. 35,000 + Rs. 30,000) = Rs. 65,000

Rs. 2,25,000 – Rs. 65,000 = Rs. 1,60,000

General Reserve is 10% of Rs. 1,60,000 = Rs. 16,000

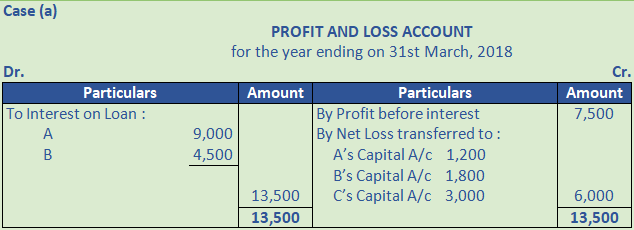

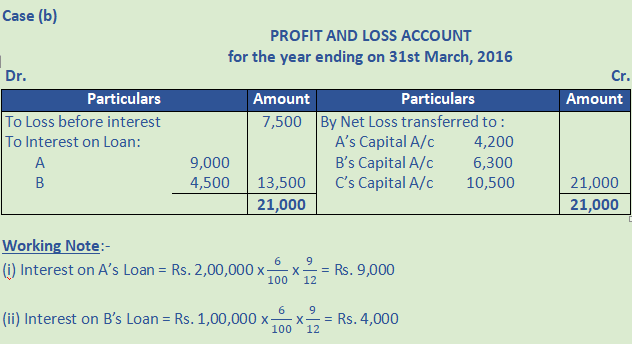

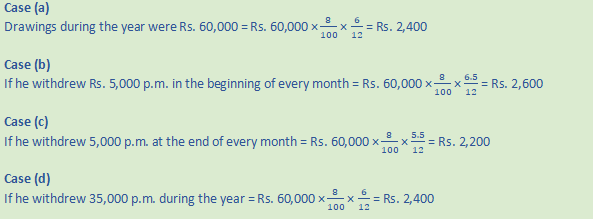

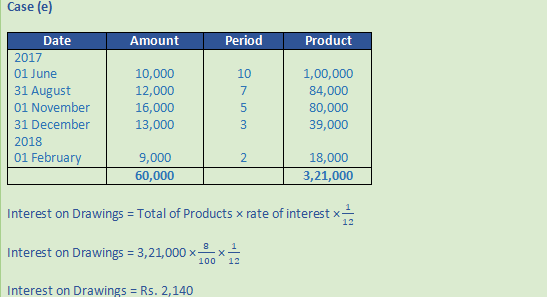

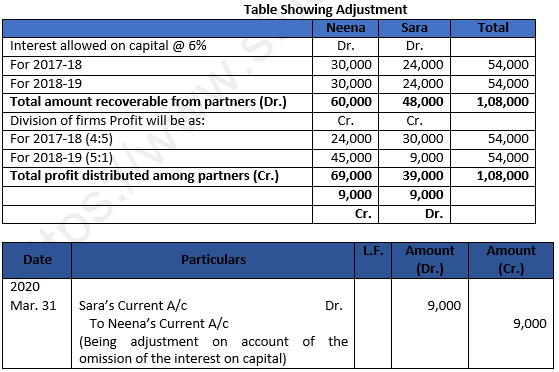

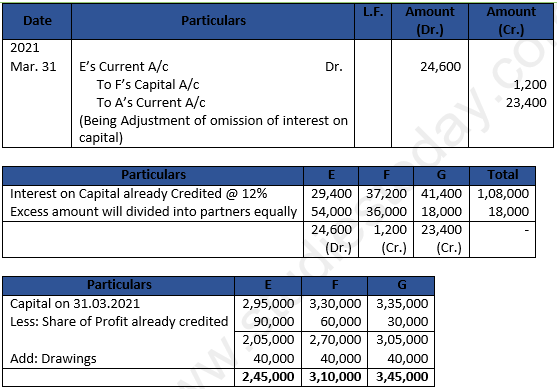

Question 16.

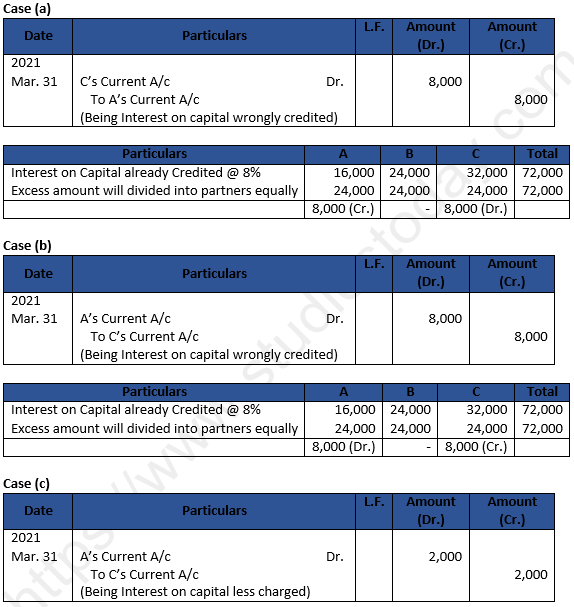

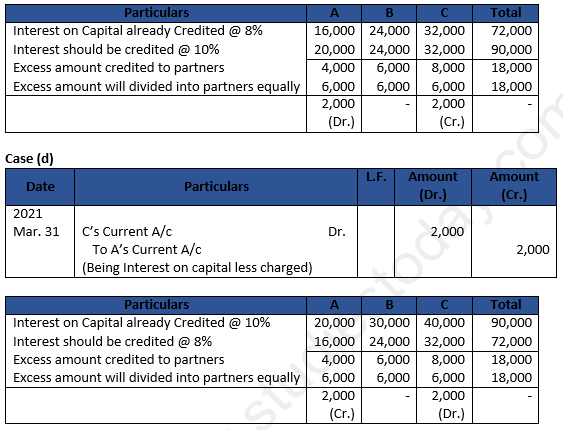

Solution 16. Case (a)

Question 17.

Solution 17.

Question 18.

Solution 18.

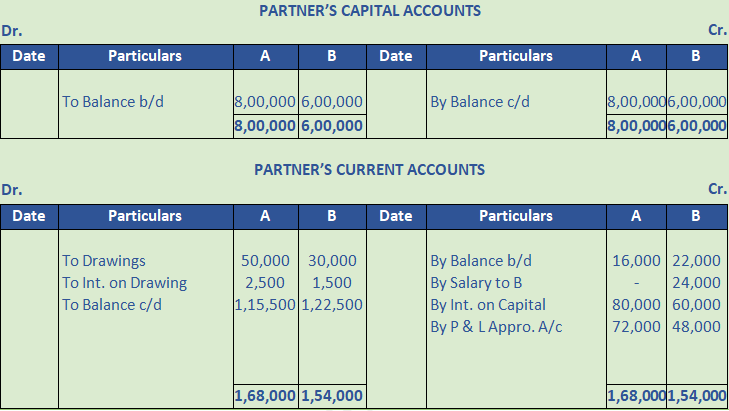

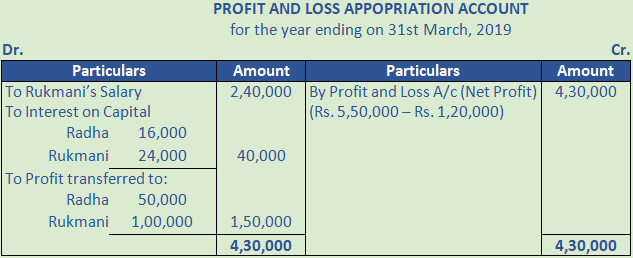

Working Note:-

1. Calculation of Net Profit = 5,50,000 – Rs. 1,20,000 = Rs. 4,30,000

2. Calculation of Interest on Capital:-

Radha = Rs. 2,00,000 × 8% = Rs. 16,000

Rukmani = Rs. 3,00,000 × 8% = Rs. 24,000

3. Calculation of Profit and Loss:-

Profit of transferred to Capital account = Rs. 4,30,000 – (Rs. 2,40,000 + Rs. 40,000)

Profit of transferred to Capital account = Rs. 1,50,000

Radha’s Profit = Rs. 1,50,000 × 1/3 = Rs. 50,000

Rukmani’s Profit = Rs. 1,50,000 × 1/3 = Rs. 1,00,000

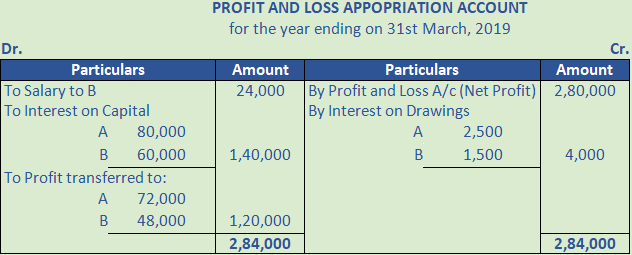

Question 19.

Solution 19.

PROFIT AND LOSS APPOPRIATION ACCOUNT

for the year ending on 31st March, 2021

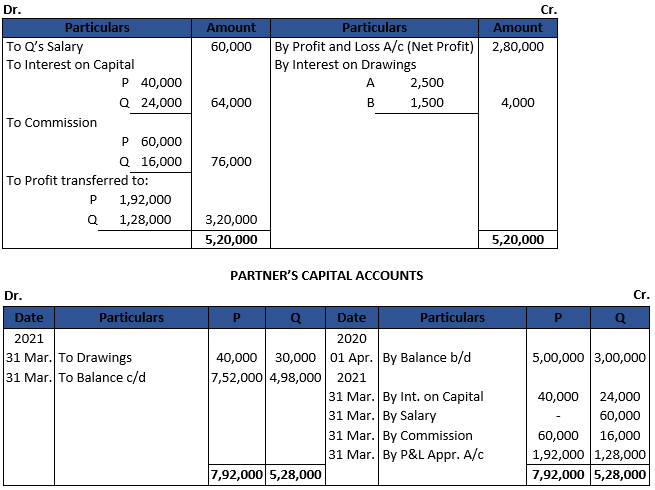

Working Note:-

1. Calculation of Net Profit = 7,60,000 – Rs. 2,40,000 = Rs. 5,20,000

2. Calculation of Interest on Capital:-

P = Rs. 5,00,000 × 8% = Rs. 40,000

Question = Rs. 3,00,000 × 8% = Rs. 24,000

3. Net Profit after deducting Expenses:-

Rs. 5,20,000 – (Rs. 64,000 + Rs. 60,000 + Rs. 60,000) = Rs. 3,36,000

Q’s Commission = 3,36,000 × 5/105 = Rs. 16,000

4. Calculation of Profit and Loss:-

P’s Profit = Rs. 3,20,000 ×60/100 = Rs. 1,92,000

Q’s Profit = Rs. 3,20,000 × 40/100 = Rs. 1,28,000

Question 20.

Solution 20.

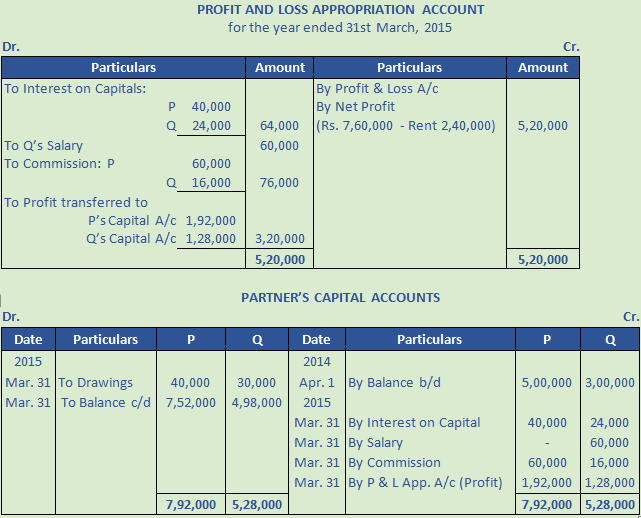

Working Note:-

(1) Net Profit transferred from P & L A/c to P & L App. A/c

Net Profit in P&L App. A/c = Net Profit in P&L A/c – Expenses (Rent)

Net Profit in P&L App. A/c = Rs. 7,60,000 – Rs. 2,40,000

Net Profit in P&L App. A/c = Rs. 5,20,000

(2) Net Profit after deducting interest on capitals, salary and P’s commission:

Rs. 5,20,000 – Rs. 64,000 – Rs. 60,000 – Rs. 60,000 = Rs. 3,36,000

Q's Commission = 3,36,000 x 5/105 = 16,000

Question 21.

Solution 21.

Question 22.

Solution 22.

Question 23.

Solution 23.

PROFIT AND LOSS APPROPRIATION ACCOUNT

for the year ended 31st March, 2021

Total profit needed = Rs. 80,000 + Rs. 40,000 = Rs. 1,20,000

Available profit = Rs. 45,000 which is less than appropriations Rs. 1,20,000. Profit will be distributed in the ratio of appropriations in interest on capital 80,000 : 40,000 = 2 : 1.

A’s share = 45,000 × 2/3 = 30,000

B’s share = 45,000 × 1/3 = 15,000

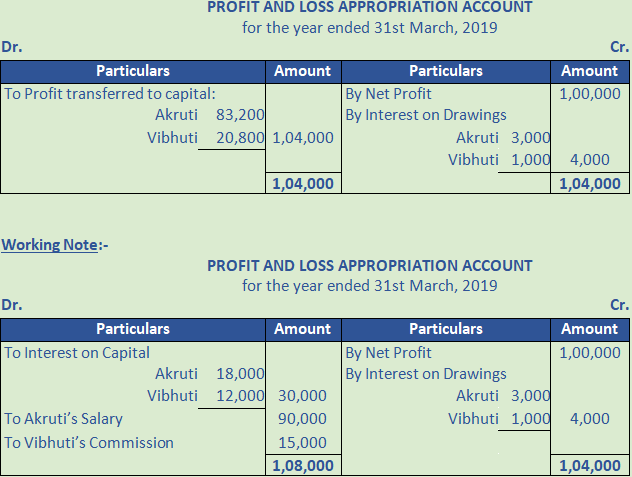

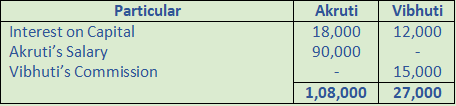

Question 24.

Solution 24.

New Ratio = 1,08,000 : 27,000

New Ratio = 108 : 27

New Ratio = 4 : 1

Profit and Loss Appropriation:-

Akruti’s Share = 1,04,000 × 4/5 = 83,200

Vibhuti’s Share = 1,04,000 × 1/5 = 20,800

Question 25. (A)

Solution 25 (A).

Question 25. (B)

Solution 25 (B).

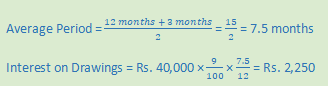

Question 26. (A)

Solution 26. (A) Gopal withdrew Rs. 1,000 p.m. regularly on the first day of every month during the year ended 31st March, 2014 for personal expenses. His interest on drawings will be calculated as follows:

Calculation of Interest on Drawings:-

![]()

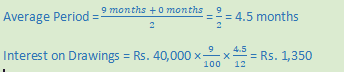

Question 26. (B)

Solution 26 (B)

Question 27.

Solution 27

Question 28.

Solution 28.

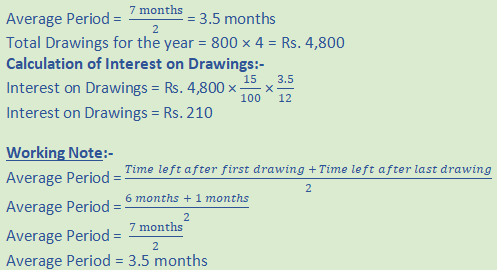

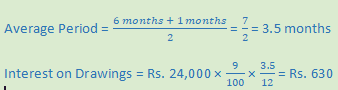

Question 29. (A)

Solution 29 (A) Gupta drew Rs. 800 at the beginning of every month for the six months ending 30th September, 2018. Hence, his drawings for the period of six months would be:

Period = 6 months + 1 months = 7 months

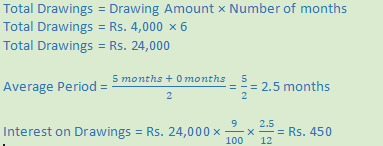

Question 29.(B)

Solution 29 (B) Gupta withdraws Rs. 800 at the end of every month for the six months ending 30th September, 2013.

Total drawings = 6 x Rs. 800 = Rs. 4,800

(Time left after first drawing + Time left after last drawing)/2

= (5 + 0)/2 = 2.5 months.

Rs. 4,800 x 15/100 x 2.5/12 = Rs. 150

Question 29. (C)

Solution 29 (C)

Total Drawings of A = Rs. 15,000 x 6 = Rs. 90,000

Total Drawings of B = Rs. 20,000 x 6 = Rs. 1,20,000

Total Drawings of C = Rs. 25,000 x 6 = Rs. 1,50,000

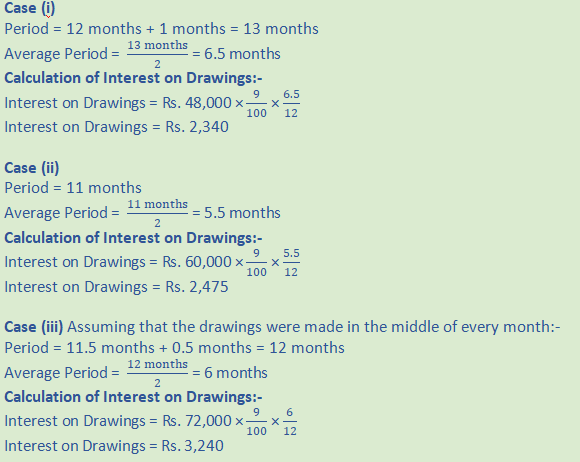

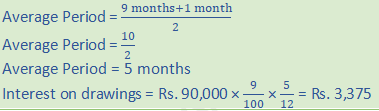

Question 30. (A)

Solution 30 (A) Total Drawings = 9 × Rs. 10,000 = Rs. 90,000

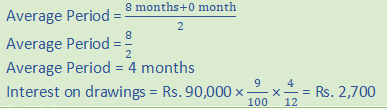

Question 30. (B)

Solution 30 (B) Total Drawings = 9 × Rs. 10,000 = Rs. 90,000

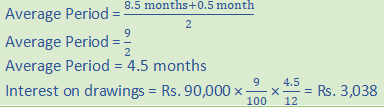

Question 30. (C)

Solution 30 (C) Total Drawings = 9 × Rs. 10,000 = Rs. 90,000

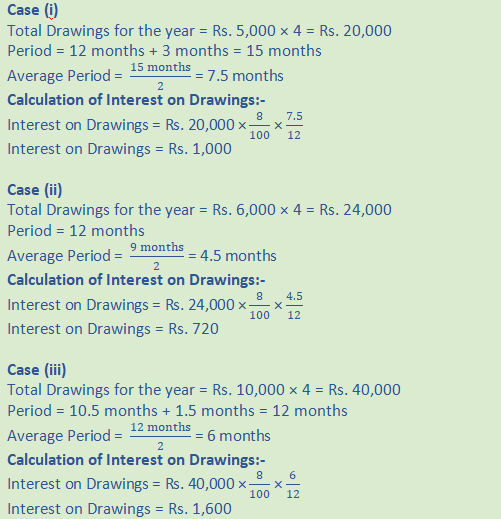

Question 31.

Solution 31. Case (i) Interest on Drawings = Rs. 60,000 × 8/100 × 6/12

Interest on Drawings = Rs. 2,400

Case (ii)

Calculation for 12 months Interest on Drawings:

Interest on Drawings = Rs. 60,000 × 8/100

Interest on Drawings = Rs. 4,800

Question 32.

Solution 32.

Question 33.

Solution 33.

Question 34.

Solution 34. Calculation of Interest on capitals:-

A = Rs. 3,00,000 × 10/(100 ) = Rs. 30,000

B = Rs. 2,00,000 × 10/(100 ) = Rs. 20,000

Calculation of Interest on Drawings:-

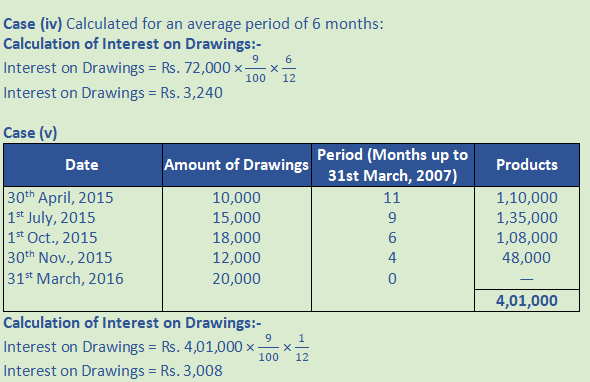

Date | Amount | Period | Products |

30-06-2020 | 20,000 | 9 months | 1,80,000 |

31-07-2020 | 10,000 | 8 months | 80,000 |

01-10-2020 | 10,000 | 6 months | 60,000 |

01-03-2021 | 16,000 | 1 month | 16,000 |

Total | 3,36,000 | ||

A’s Interest on Drawings = Total Products × 1/12 × (Rate of Interets )/100

A’s Interest on Drawings = Rs. 3,36,000 × 1/12 × (10 )/100

A’s Interest on Drawings = Rs. 2,800

B’s Interest Drawings:-

Total Drawings = Rs. 6,000 × 12 = Rs. 72,000

B’s Interest on Drawings = Rs. 72,000 × 10/100 × (5.5 )/12

B’s Interest on Drawings = Rs. 3,300

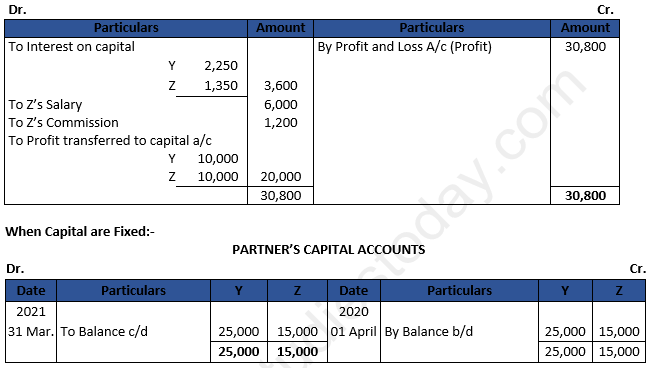

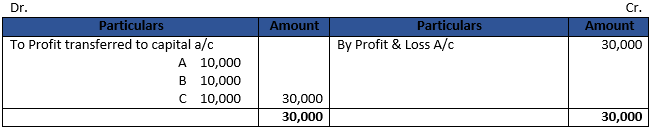

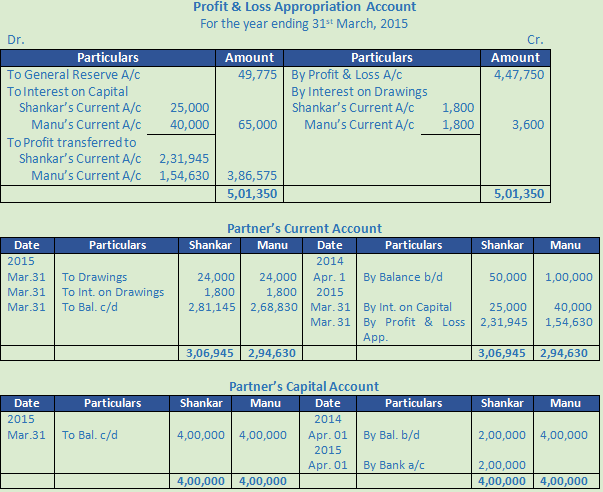

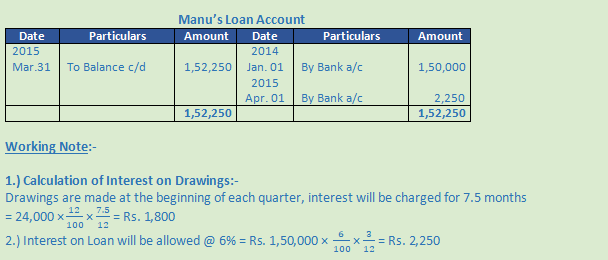

Question 35.

Solution 35.

Working Note:-

Calculation of Interest on Capital:-

X’s Interest on Capital = 50,000 × 6% = 3,000

Y’s Interest on Capital = 30,000 × 6% = 1,800

Profit and Loss Appropriation (Distribution of Profit):-

X’s Share = 4,200 × 2/3 = 2,800

Y’s Share = 4,200 × 1/3 = 1,400

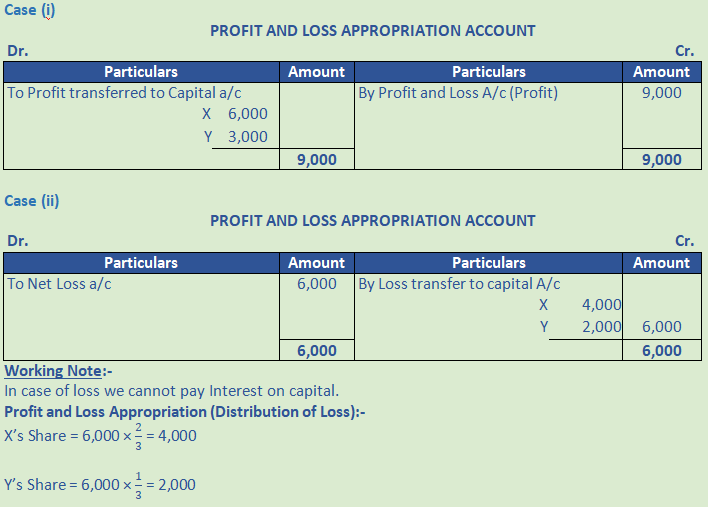

Question 36.

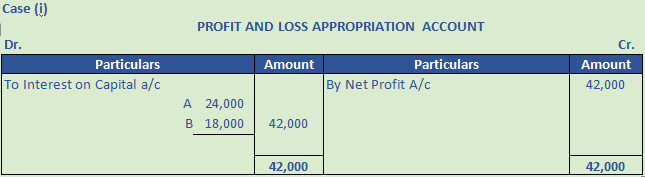

Solution 36.

Working Note:-

Calculation of Interest on Capital:-

A’s Interest on Capital = 4,00,000 × 8% = 32,000

B’s Interest on Capital = 3,00,000 × 8% = 24,000

The profit is Rs. 42,000 whereas Interest on capital is Rs. 56,000. So the expenses divided into their expenses ratio which is 32,000 : 24,000 or 4 : 3

Question 37.

Solution 37.

Working Note:-

Calculation of Interest on Capital:-

P’s Interest on Capital = 10,00,000 × 12% = 1,20,000

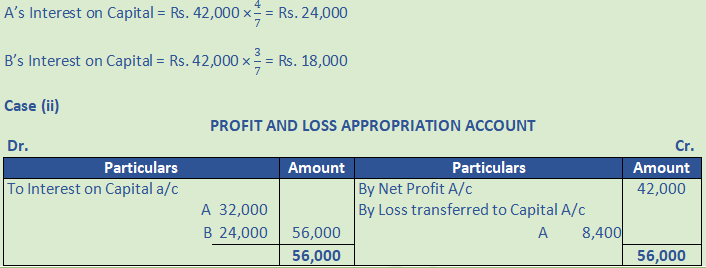

Q’s Interest on Capital = 6,00,000 × 12% = 72,000

Profit and Loss Appropriation (Distribution of Loss):-

P’s Share = 42,000 × 3/4 = 31,500

Q’s Share = 42,000 × 1/4 = 10,500

Question 38.

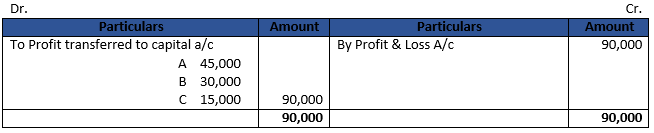

Solution 38.

PROFIT AND LOSS APPROPRIATION ACCOUNT

For the year ended 31st March, 2021

Working Note:-

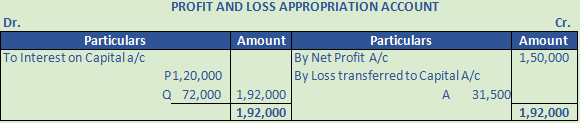

Calculation of Interest on Capital:-

A’s Interest on Capital = 10,00,000 × 12% = 1,20,000

B’s Interest on Capital = 15,00,000 × 12% = 1,80,000

The profit is Rs. 2,00,000 whereas Interest on capital is Rs. 3,00,000. So the expenses divided into their expenses ratio which is 1,20,000 : 1,80,000 or 2 : 3

A’s Interest on Capital = Rs. 2,00,000 × 2/5 = Rs. 80,000

B’s Interest on Capital = Rs. 2,00,000 × 3/5 = Rs. 1,20,000

Question 39.

Solution 39.

Question 40.

Solution 40.

Question 41.

Solution 41.

Question 42.

Solution 42.

Question 43.

Solution 43.

Question 44.

Solution 44.

Question 45.

Solution 45.

Question 46.

Solution 46.

Question 47.

Solution 47.

Question 48.

Solution 48.

Question 49.

Solution 49.

Question 50. (A)

Solution 50 (A).

Question 50. (B)

Solution 50 (B).

Question 51.

Solution 51.

Question 52.

Solution 52.

Question 53.

Solution 53.

Question 54.

Solution 54.

Question 55.

Solution 55.

Question 56.

Solution 56.

Question 57.

Solution 57.

Question 58.

Solution 58.

Question 59.

Solution 59.

Question 60.

Solution 60.

Question 61. (A)

Solution 61 (A).

Question 61. (B)

Solution 61 (B).

Question 61. (C)

Solution 61 (C).

Question 62.

Solution 62.

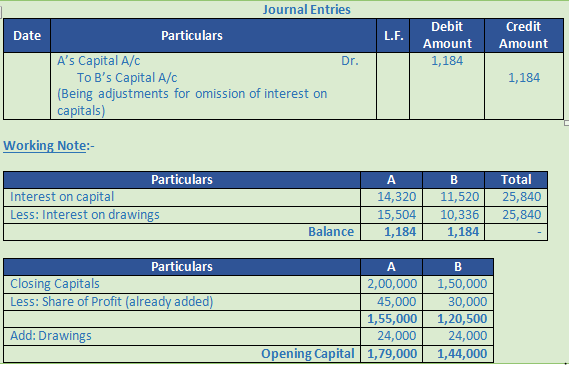

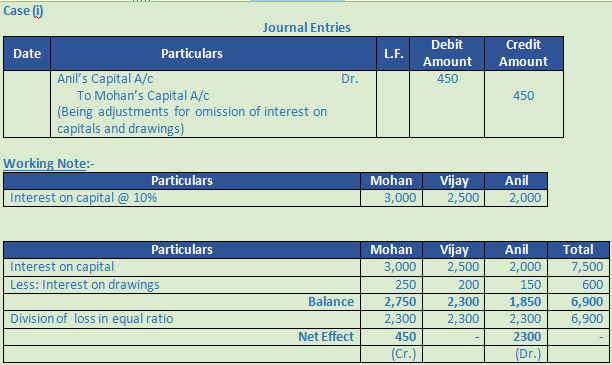

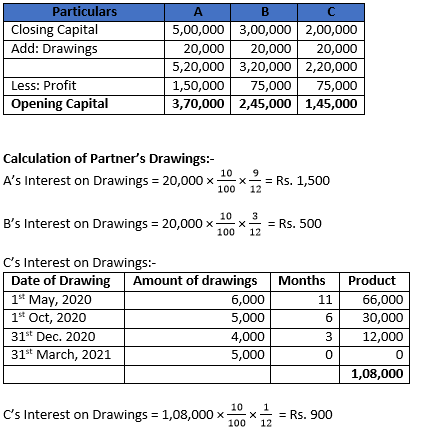

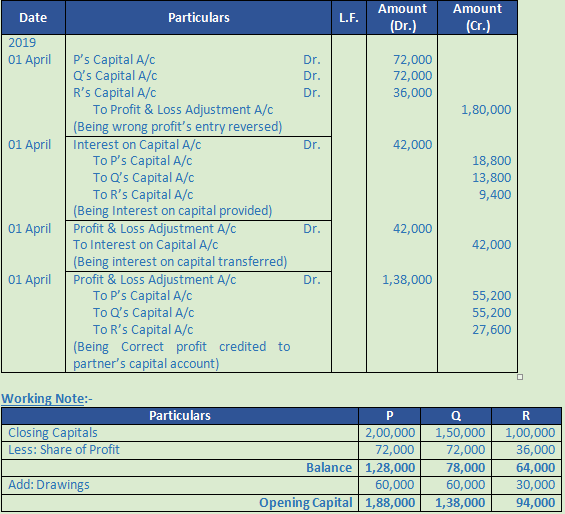

Question 63 (new).

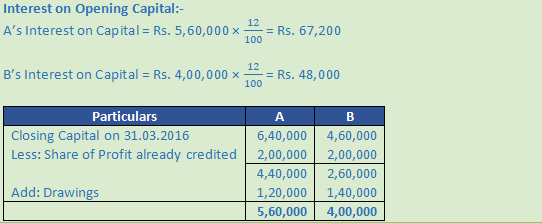

Solution 63 (new). Calculation of Partner’s Capital:-

A’s Interest on Capital = 3,70,000 × 8/100 = Rs. 29,600

B’s Interest on Capital = 2,45,000 × 8/100 = Rs. 19,600

C’s Interest on Capital = 1,45,000 × 8/100 = Rs. 11,600

Calculation of Opening Capital:-

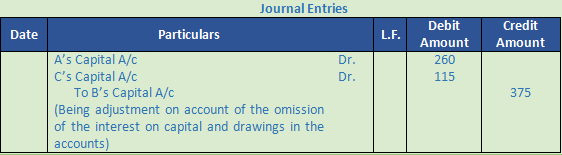

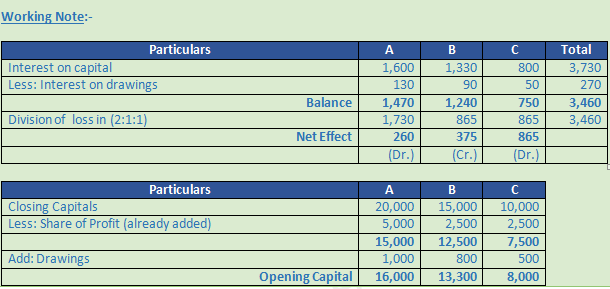

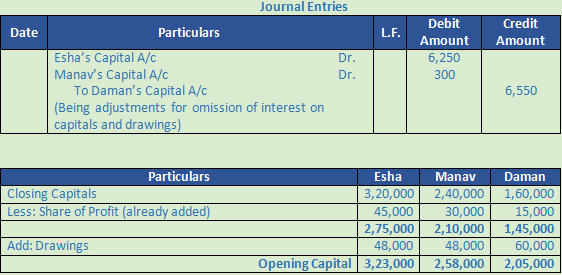

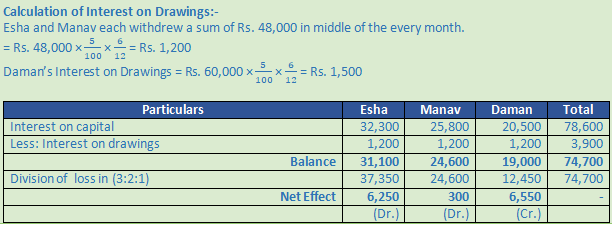

Question 63.

Solution 63.

Working Note:-

Calculation of Interest on Capital:-

Esha’s Interest on Capital = Rs. 3,23,000 × 10% = 32,300

Manav’s Interest on Capital = Rs. 2,58,000 × 10% = 25,800

Daman’s Interest on Capital = Rs. 2,05,000 × 10% = 20,500

Total Interest on Capital = Rs. 32,300 + Rs. 25,800 + Rs. 20,500 = Rs. 78,600

Question 64.

Solution 64.

Question 65.

Solution 65.

Question 66.

Solution 66.

Question 67.

Solution 67.

Calculation Interest on capital:-

A’s Interest on Capital = Rs. 96,000 × 5% = Rs. 4,800

B’s Interest on Capital = Rs. 70,000 × 5% = Rs. 3,500

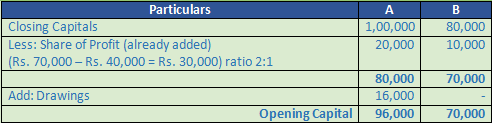

Question 68.

Solution 68.

Calculation of Interest on Capital:-

P’s Interest on Capital = Rs. 1,88,000 × 10% = Rs. 18,800

Q ’s Interest on Capital = Rs. 1,38,000 × 10% = Rs. 13,800

R’s Interest on Capital = Rs. 94,000 × 10% = Rs. 9,400

Question 69. (A)

Solution 69 (A).

Profit & Loss Appropriation Account

For the year ending 31st March, 2020

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Working Note:-

Calculation of Share of Profit in 2020-:-

A’s Share of Profit = Rs. 30,000 × 3/6 = Rs. 15,000

B’s Share of Profit = Rs. 30,000 × 2/6 = Rs. 10,000

C’s Share of Profit = Rs. 30,000 × 1/6 = Rs. 5,000

Calculation of Share of Profit in 2021:-

A’s Share of Profit = Rs. 90,000 × 3/6 = Rs. 45,000

B’s Share of Profit = Rs. 90,000 × 2/6 = Rs. 30,000

C’s Share of Profit = Rs. 90,000 × 1/6 = Rs. 15,000

Question 69. (B)

Solution 69 (B).

Question 70.

Solution 70.

Working Note:-

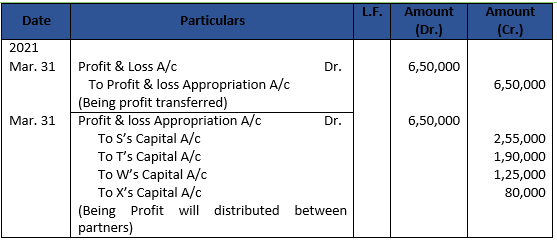

Calculation Profit Distribution:-

S’s Share of Profit = Rs. 6,50,000 × 4/10 = Rs. 2,60,000

T’s Share of Profit = Rs. 6,50,000 × 3/10 = Rs. 1,95,000

W’s Share of Profit = Rs. 6,50,000 × 2/10 = Rs. 1,30,000

X’s Share of Profit = Rs. 6,50,000 × 1/10 = Rs. 65,000

Share of X’s Profit in Total profit is Rs. 65,000 whereas the minimum guarantee amount is Rs. 80,000. Hence, the deficiency of Rs. 15,000 will be cover by S, T, W equally.

S’s Share of Profit = Rs. 2,60,000 – Rs. 5,000 = Rs. 2,55,000

T’s Share of Profit = Rs. 1,95,000 – Rs. 5,000 = Rs. 1,90,000

W’s Share of Profit = Rs. 1,30,000 – Rs. 5,000 = Rs. 1,25,000

X’s Share of Profit = Rs. 65,000 + Rs. 5,000 + Rs. 5,000 + Rs. 5,000 = Rs. 80,000

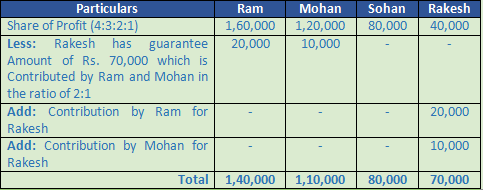

Question 71.

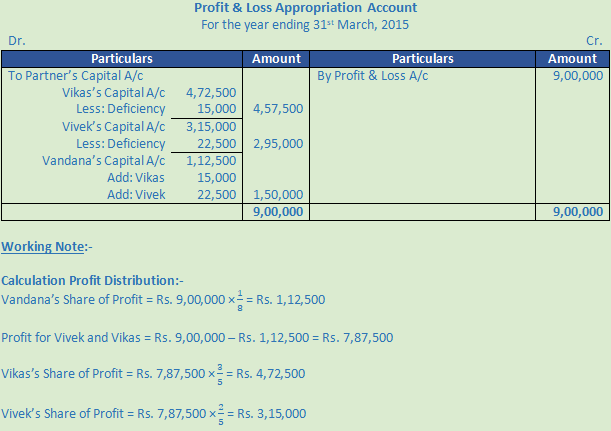

Solution 71.

Vandana’s deficiency = Rs. 1,50,000 – Rs. 1,12,500 = Rs. 37,500. Deficiency will be contributed by Vikas and Vivek in the ratio 2:3.

Vikas’s Contribution = Rs. 4,72,500 – Rs. 15,000 = Rs. 4,57,500

Vivek’s Contribution = Rs. 3,15,000 – Rs. 22,500 = 2,92,500

Question 72.

Solution 72.

Question 73.

Solution 73.

Question 74.

Solution 74.

Question 75.

Solution 75.

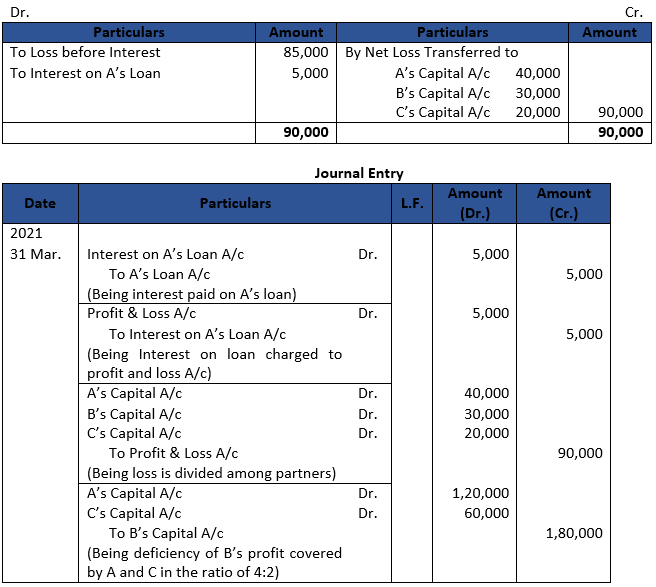

Working Note:-

Z’s Share of Loss = Rs. 1,20,000 × 1/4 = Rs. 30,000

Remaining Profit = Rs. 1,20,000 – Rs. 30,000 = Rs. 90,000

X’s Share of Loss = Rs. 90,000 × 2/5 = Rs. 60,000

Y’s Share of Loss = Rs. 90,000 × 3/5 = Rs. 30,000

Z’s guaranteed minimum profit of Rs. 1,00,000. Total loss of Z = Rs. 1,00,000 + Rs. 30,000 = Rs. 1,30,000. Which is distributed by X and Y in the ratio of 3:2.

Question 76.

Solution 76.

Profit & Loss Account

For the year ending 31st March, 2021

Working Note:-

A’s Share of Loss = Rs. 90,000 × 4/9 = Rs. 40,000

B’s Share of Loss = Rs. 90,000 × 3/9 = Rs. 30,000

C’s Share of Loss = Rs. 90,000 × 2/9 = Rs. 20,000

B’s guaranteed minimum profit of Rs. 1,50,000. Total loss of Z = Rs. 1,50,000 + Rs. 30,000 = Rs. 1,80,000. Which is paid by A and C in the ratio of 4:2.

A’s Share to B = Rs. 1,80,000 × 4/6 = Rs. 1,20,000

A’s Share to B = Rs. 1,80,000 × 2/6 = Rs. 60,000

Question 77 (new).

Solution 77 (new).

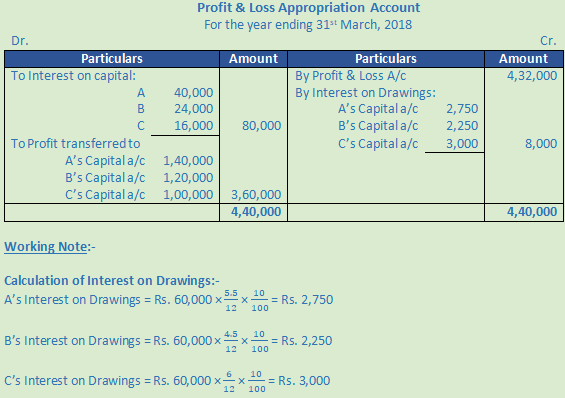

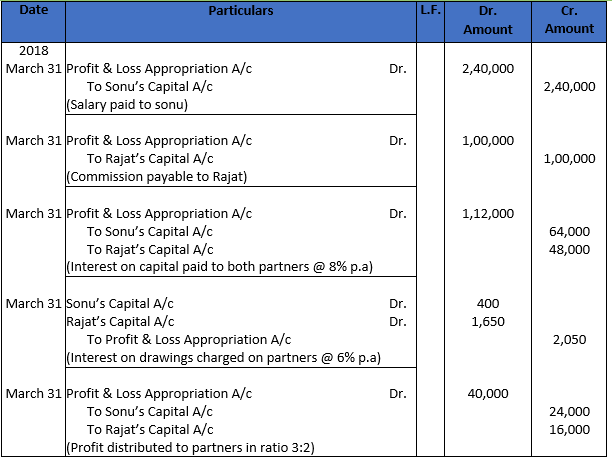

Working Note:

1. Calculation of interest on drawings:-

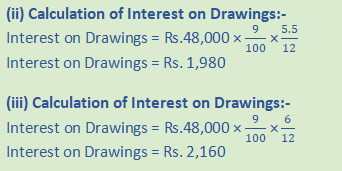

Drawings of Sonu = Rs. 20,000

Interest on Sonu’s drawings = Rs. 20,000 × 6/100 × 4/12

Interest on Sonu’s drawings = Rs. 400

Drawings of Rajat = 12 × Rs. 5,000 = Rs. 60,000

Interest on Rajat’s drawings = Rs. 60,000 × 6/100 × 5.5/12

Interest on Rajat’s drawings = Rs. 1,650

Question 77.

Solution 77.

Question 78.

Solution 78.

Question 79.

Solution 79.

Question 80.

Solution 80.

Question 81.

Solution 81.

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Question 82.

Solution 82.

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Question 83.

Solution 83.

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Question 84.

Solution 84.

Question 85.

Solution 85.

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Question 86.

Solution 86.

Question 87.

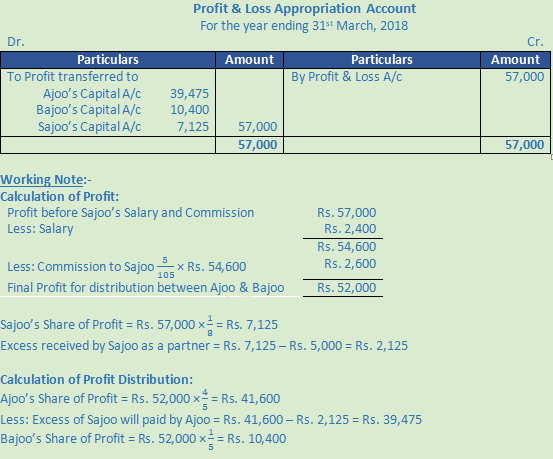

Solution 87 Calculation of Commission:-

Before charging such commission

A’s Commission = Rs. 55,000 × 10/100 = Rs. 5,500

After charging A’s commission and his commission

Rs. 55,000 – Rs. 5,500 = Rs. 49,500

B’s Commission = Rs. 49,500 × 10/100 = Rs. 4,500

Question 88.

Solution 88.

Question 89.

Solution 89.

Question 90.

Solution 90.

Question 91.

Solution 91 Total Drawings = Drawing Amount × Number of quarter in a year

Total Drawings = Rs. 10,000 × 4

Total Drawings = Rs. 40,000

Question 92.

Solution 92. Total Drawings = Drawing Amount × Number of quarter in a year

Total Drawings = Rs. 10,000 × 4

Total Drawings = Rs. 40,000

Question 93.

Solution 93 Total Drawings = Drawing Amount × Number of quarter in a year

Total Drawings = Rs. 10,000 × 4

Total Drawings = Rs. 40,000

Question 94.

Solution 94 Total Drawings = Drawing Amount × Number of month

Total Drawings = Rs. 4,000 × 6

Total Drawings = Rs. 24,000

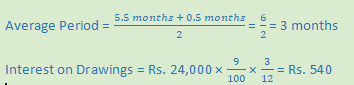

Question 95.

Solution 95 Total Drawings = Drawing Amount × Number of months

Total Drawings = Rs. 4,000 × 6

Total Drawings = Rs. 24,000

Question 96.

Solution 96 Total Drawings = Drawing Amount × Number of months

Total Drawings = Rs. 4,000 × 6

Total Drawings = Rs. 24,000

Question 97.

Solution 97.

Question 98.

Solution 98. Case (i)

If Partnership deed is silent as to the treatment of interest as a charge or appropriation

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Working Note:-

Calculation of Interest on Capital:-

X’s Interest on Capital = Rs. 60,000 × 3/6 = Rs. 30,000

Y’s Interest on Capital = Rs. 60,000 × 2/6 = Rs. 20,000

Z’s Interest on Capital = Rs. 60,000 × 1/6 = Rs. 10,000

Case (ii)

Partnership deed provides for interest even if it involves the firm in loss.

Profit & Loss Appropriation Account

For the year ending 31st March, 2021

Question 99.

Solution 99.

Profit & Loss Account

For the year ending 31st March, 2021

Question 100.

Solution 100.

Question 101.

Solution 101.

Question 102 (new).

Question 102.

Solution 102.

Question 103.

Solution 103.

Question 104.

Solution 104.

Question 105.

Solution 105.