Read DK Goel Class 12 Accountancy Solutions for Chapter 1 Financial Statements of Not for Profit Organisations below. These DK Goel Accountancy Class 12 solutions have been prepared based on the latest book for DK Goel Class 12 for the current academic year by expert accounts teachers at studiestoday.com. These DK Goel Class 12 Solutions help commerce students in class 12 understand accountancy and build a strong base in accounts. Students in Class 12 who study accountancy and use the DK Goel Accountancy book to understand concepts of Chapter 1 Financial Statements of Not for Profit Organisations should understand the concepts and solve practice questions and exercises given at the end of the chapter. We have provided solutions for all questions and have also provided short notes for each problem. This will help Class 12 DK Goel Accountancy students to understand the questions properly. Refer to the solutions provided below prepared by CBSE NCERT teachers

Chapter 1 Financial Statements of Not for Profit Organisations DK Goel Class 12 Solutions

Class 12 Accountancy students should read the following DK Goel Solutions for Class 12 Chapter 1 Financial Statements of Not for Profit Organisations in Standard 12. All solutions provided below can be downloaded in Pdf and are available for free. This DK Goel Book for Grade 12 Accountancy will be very useful for exams and help you to score good marks in Class 12 accountancy examinations. On our website www.studiestoday.com, we have provided solutions for all chapters given in the DK Goel Accountancy Book for Class 12.

DK Goel Solutions Chapter 1 Financial Statements of Not for Profit Organisations Class 12 Accountancy

Short Answer Questions

Question 1.

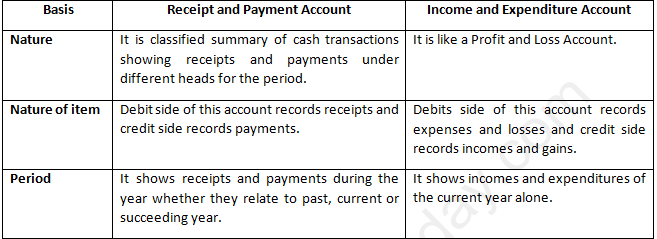

Solution 1. Features of Receipts and Payments Account:

1.) Capital and Revenue: It records all receipts and payments whether they are of revenue nature or capital nature.

2.) Period: It records cash and bank transactions without distinguishing among current, previous or succeeding (next) accounting periods.

3.) Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 2.

Solution 2. Features of Income and Expenditure Account:-

1.) Nature: It is a Nominal Account. Hence, it is debited with expenses and losses and it is credited with income and gains.

2.) Opening and Closing Balance: It does not have an opening Balance. Its Balance at the end is either surplus or deficit. It is transferred to Capital Fund in the Balance Sheet.

3.) Adjustment: This account is prepared on accrual basis of accounting and thus all adjustments relating to prepaid or outstanding expenses and income, provision for depreciation or doubtful debts are made.

Question 3.

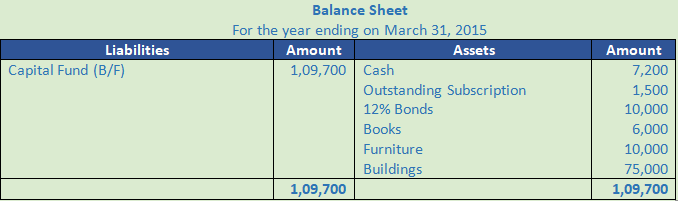

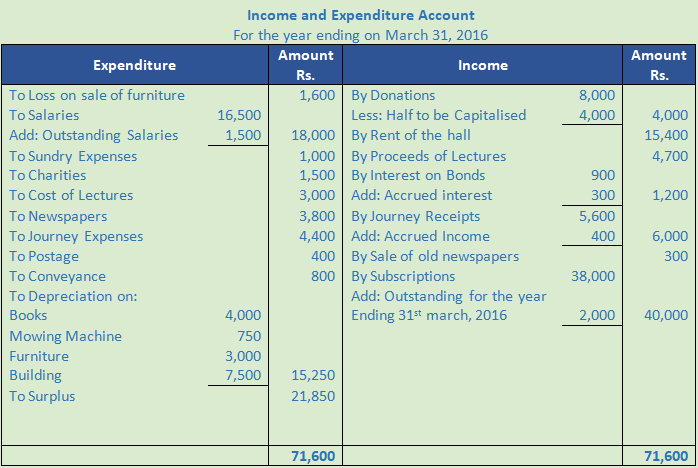

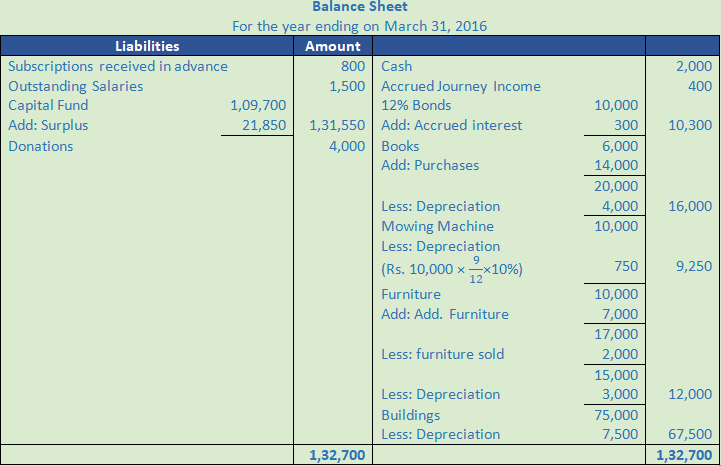

Solution 3.

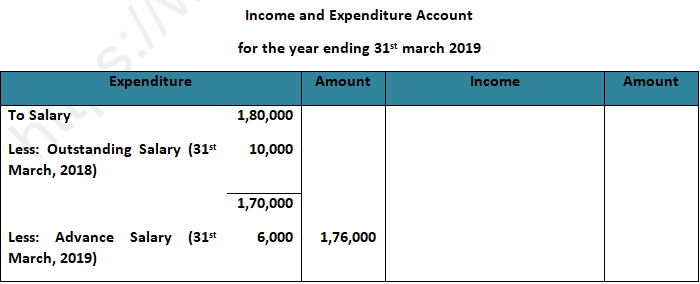

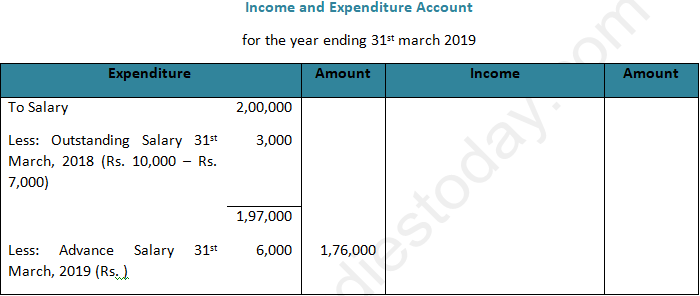

Question 4.

Solution 4.

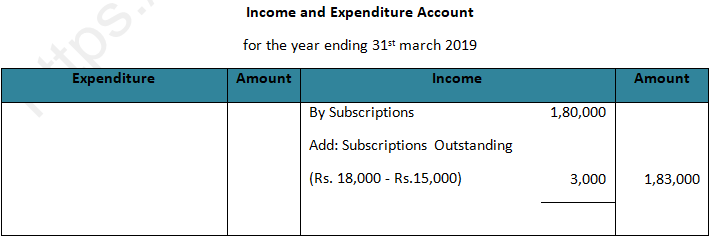

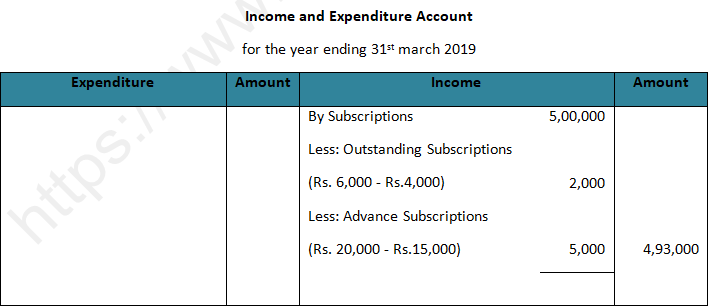

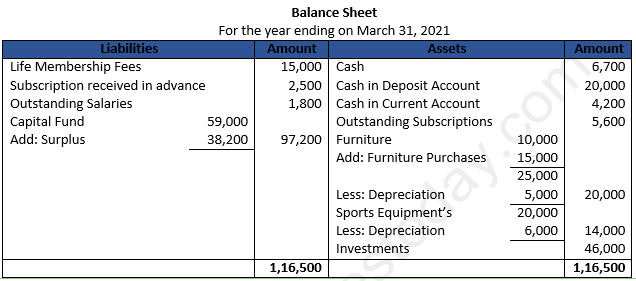

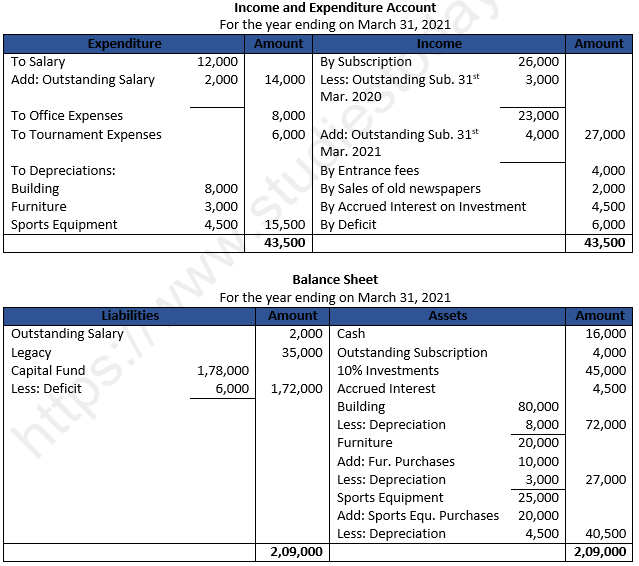

(i) Outstanding Subscription:- Outstanding Subscription Of that year is recorded on debit side of Income and Expenditure A/c and also shown in the Balance Sheet of Current year in the Assets Side.

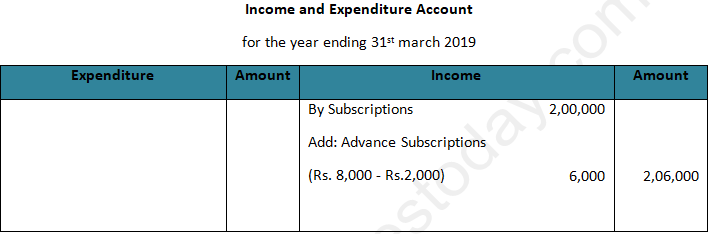

(ii) Subscriptions Received in advance:- Subscriptions Received in advance for the following year are shown on the liabilities side of the Balance Sheet.

(iii) Tournament Fund:- Tournament Fund will be treated in the liability side of Balance Sheet according to its Adjustments.

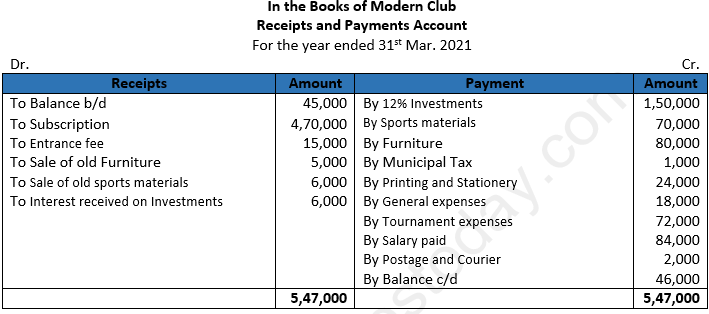

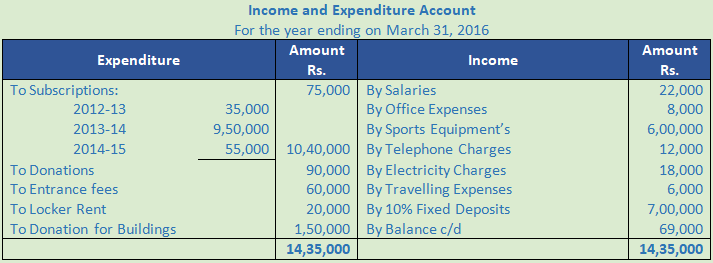

Question 5.

Solution 5.

1. Opening and closing cash/bank balances have been excluded.

2. Payment for purchase of Government securities being capital expenditure has been excluded.

3. Amount of subscriptions received for the year 2013-14 and 2014-15 have been excluded.

4. Life membership fee is an item of capital receipt and so excluded.

5. Donation for building is a receipt for a specific purpose and so excluded.

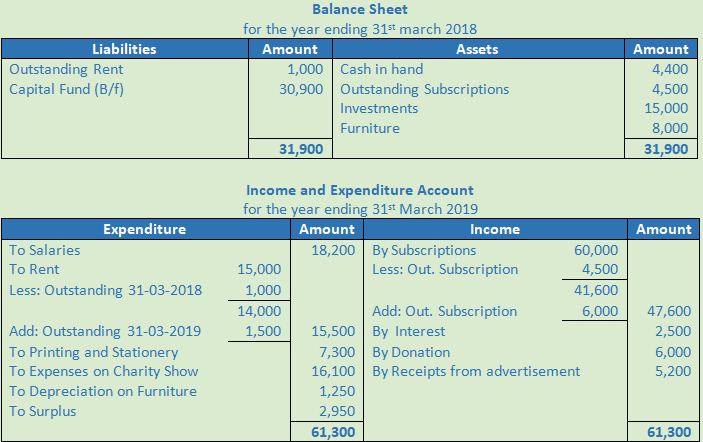

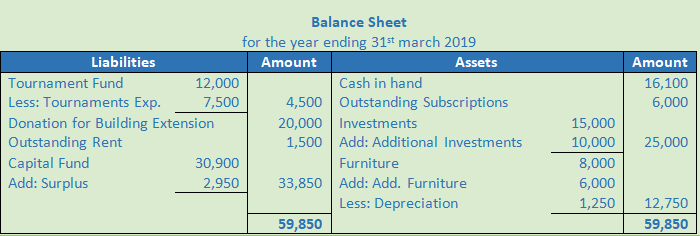

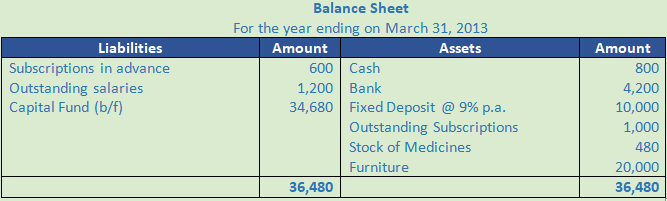

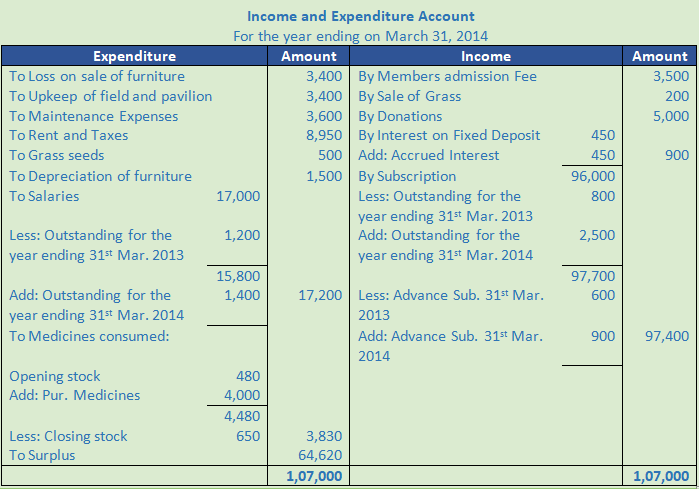

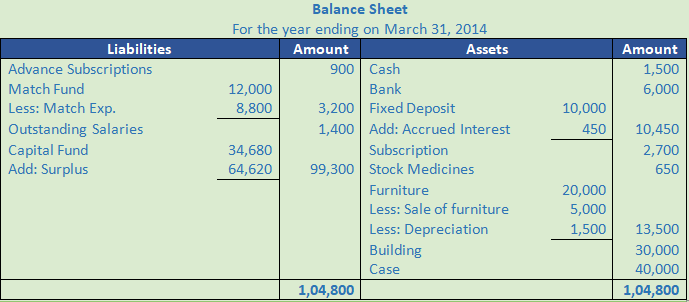

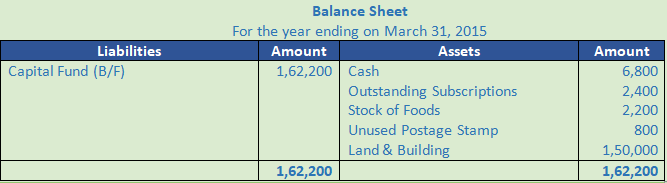

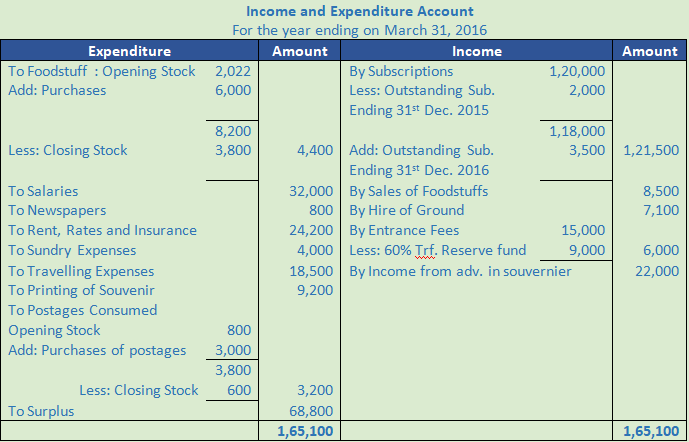

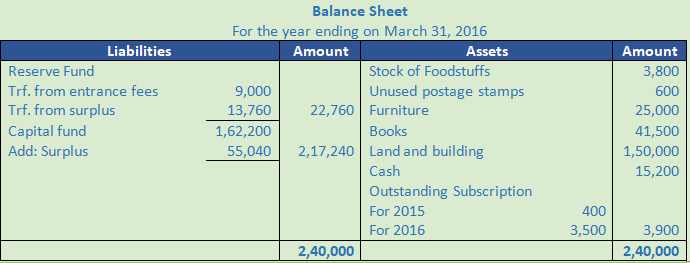

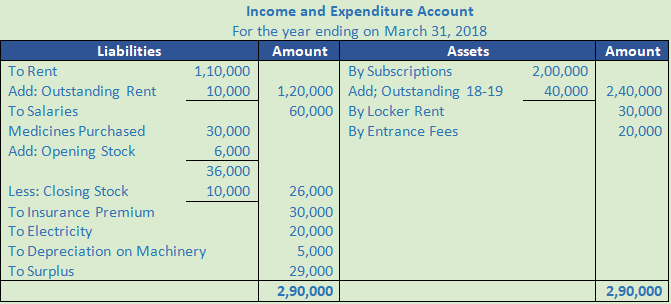

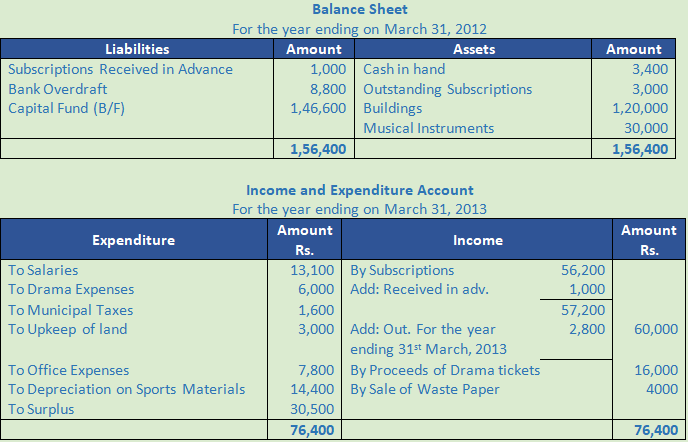

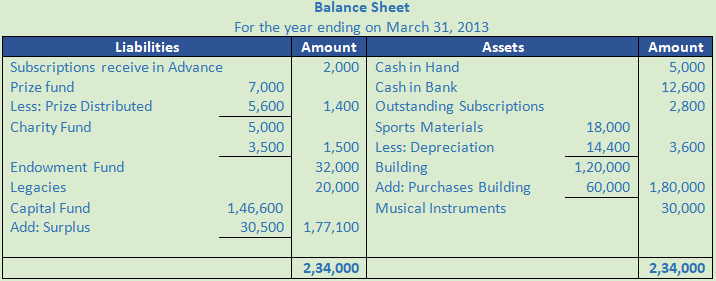

Question 6.

Solution 6.

(i) Capital Fund:- Capital Fund does not carry any restriction with respect to its use. In other words, managements can use the amounts in the fund as it deems appropriate, but to carry out the purpose for which the organisation exists.

(ii) Legacy:- Legacy is the amount received as donation by a Not-for-Profit Organisation under Will of deceased person. The donor may or may not specify conditions for its use. In case, no condition is specified, it is accounted as ‘General Donation’. And if a condition is specified, it is accounted as ‘Specific Donation’.

(iii) Specific Donation:- In case the donor specifies the purpose for which the donation can be used, it is a Specific Donation. For example, a donor donates Rs. 5,00,000 for a library. It means the donation received can be used only for library, i.e. it is a specific donation. Specific donation is capitalised and is shown on the liabilities side of the Balance Sheet.

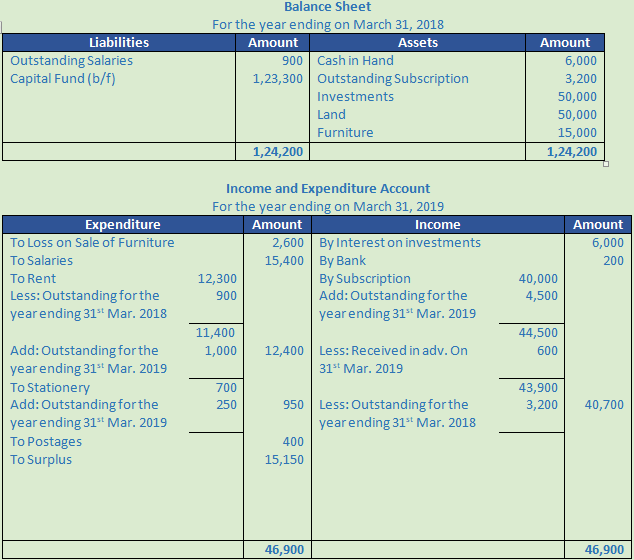

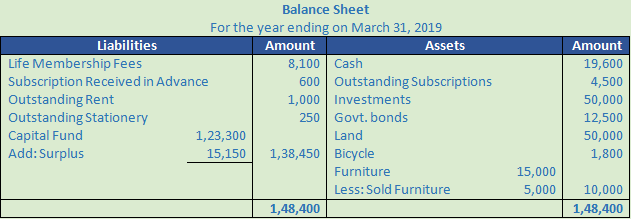

Question 7.

Solution 7. Sale of an asset may result in gain, if sale value is more than the book value; or loss, if sale value is less than the book value; or neither profit nor loss, if sale value is equal to the book value. Book Value of an asset as on the date of sale is determined after charging depreciation up to the date of sale. Sale Value is credited to the Asset Account while gain, if any, is credited or loss, if any is debited to the Income and Expenditure Account.

Question 8.

Solution 8.

(i) Entrance Fees:- Entrance Fee or Admission fee is the amount paid by a person at the time of becoming a member of a Not-for-Profit Organisation. Entrance Fee or Admission Fee is a revenue receipt and therefore, is accounted as an income and credited to Income and Expenditure Account.

(ii) Life Membership Fees:- Life Membership Fees is accounted as a Capital Receipt and added to Capital Fund on the liabilities side of the Balance Sheet. It is not accounted as income because a life member makes one time payment and avails services all through his life.

(iii) Legacy:- Legacy is the amount received as donation by a Not-for-Profit Organisation under Will of deceased person. The donor may or may not specify conditions for its use. In case, no condition is specified, it is accounted as ‘General Donation’. And if a condition is specified, it is accounted as ‘Specific Donation’.

(iv) General Donation:- General Donation is the donation in which the donor does not specify any condition for its use. The amount of general donation is accounted as an income and credited to income and expenditure account.

Question 9.

Solution 9.

(i) Donation for Building:- Donation for Building means the donation received can be used only for building it is a specific donation. Specific donation is capitalised and is shown on the liabilities side of the Balance Sheet.

(ii) Sale of Newspapers:- Amount paid for newspapers, magazines, periodicals, etc. is debited to income and Expenditure Account, it being a revenue expense. Thus, amount realised from sale of old newspapers, magazines, periodicals, etc. is credited to Income and Expenditure Account.

(iii) Investment Purchased:- Purchases of Investments are treated as capital expenditures and shown on the assets side of the Balance Sheet.

Question 10.

Solution 10.

Question 11.

Solution 11.

Question 12.

Solution 12.

Question 13.

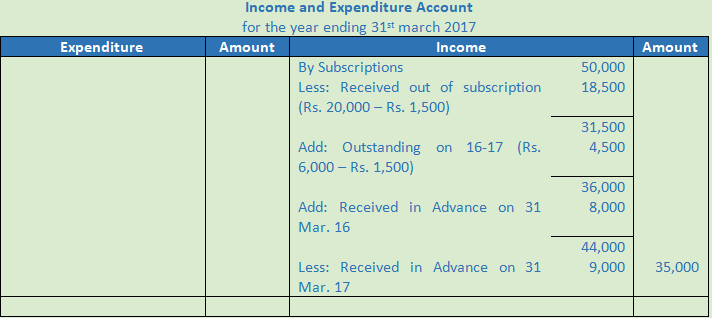

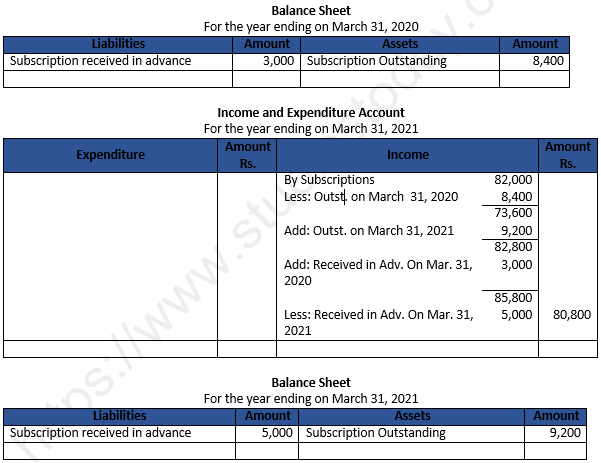

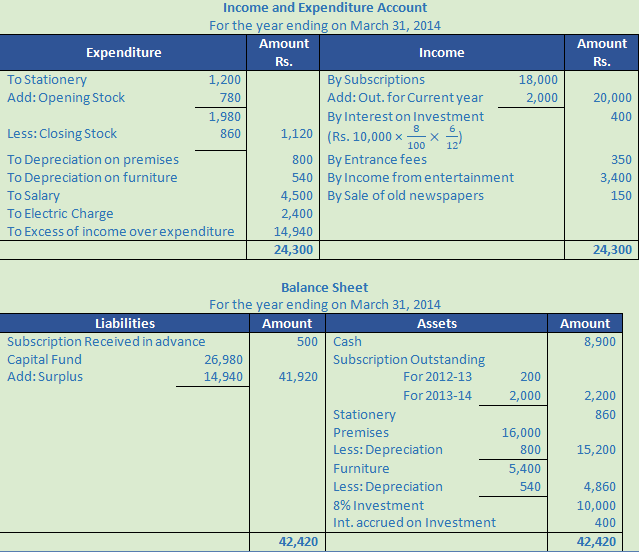

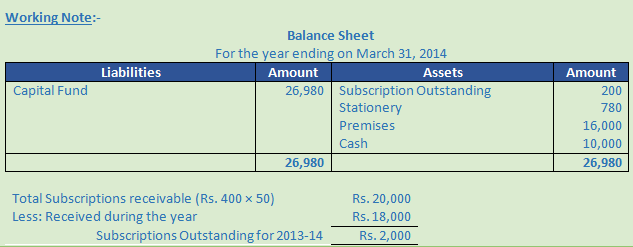

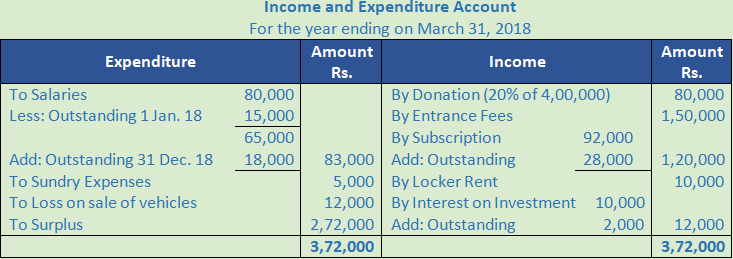

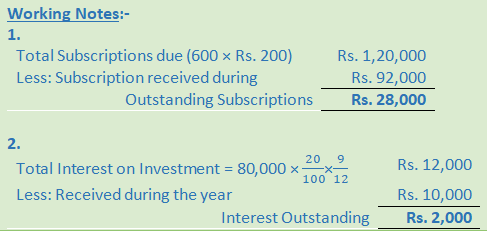

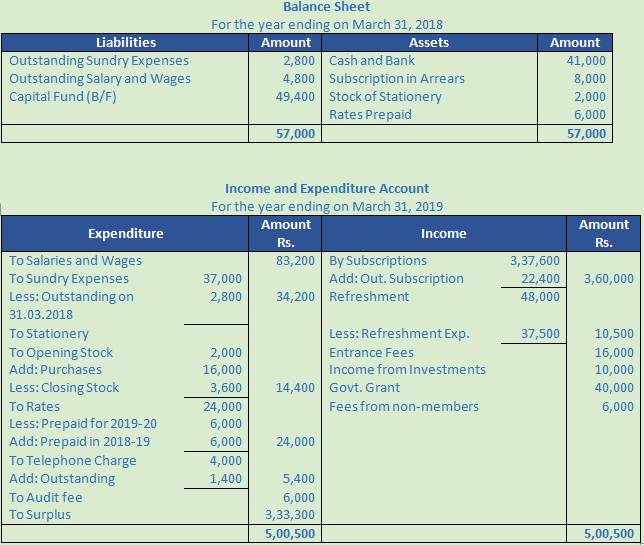

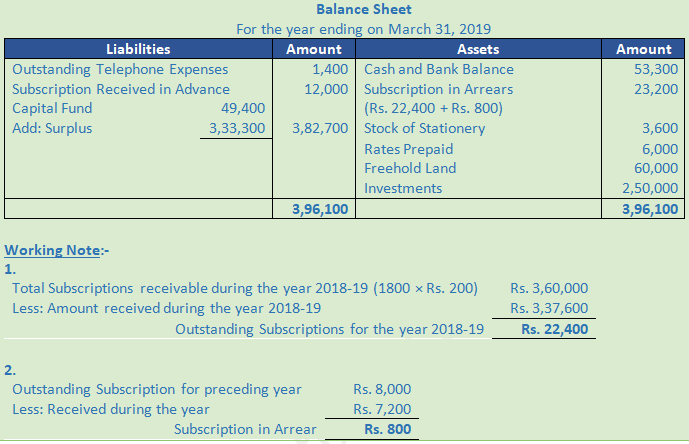

Solution 13. What amount should be credited to Income and Expenditure Account as subscriptions?

Question 14.

Solution 14.

Question 15.

Solution 15.

Question 16.

Solution 16.

Question 17.

Solution 17.

Question 18.

Solution 18.

Question 19.

Solution 19.

Question 20.

Solution 20.

Question 21.

Solution 21.

Question 22.

Solution 22.

Question 23.

Solution 23.

Question 24.

Solution 24.

Question 25.

Solution 25.

Question 26.

Solution 26.

Question 27.

Solution 27.

Question 28.

Solution 28.

Question 29.

Solution 29.

Numerical Questions:-

Question 1.

Solution 1.

Point of Knowledge:-

Sale of an asset may result in gain, if sale value is more than the book value; or loss, if sale value is less than the book value; or neither profit nor loss, if sale value is equal to the book value. Book Value of an asset as on the date of sale is determined after charging depreciation up to the date of sale. Sale Value is credited to the Asset Account while gain, if any, is credited or loss, if any is debited to the Income and Expenditure Account.

Question 2.

Solution 2.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 3.

Solution 3.

Point of Knowledge:-

Receipts and Payments Account is a summary of cash (including bank) receipts and Payments during and accounting period, receipts and payments being shown under appropriate heads of accounts.

Question 4.

Solution 4 .

Point of Knowledge:-

- Receipts and Payments Account is a summary of cash (including bank) receipts and Payments during and accounting period, receipts and payments being shown under appropriate heads of accounts.

Question 5.

Solution 5.

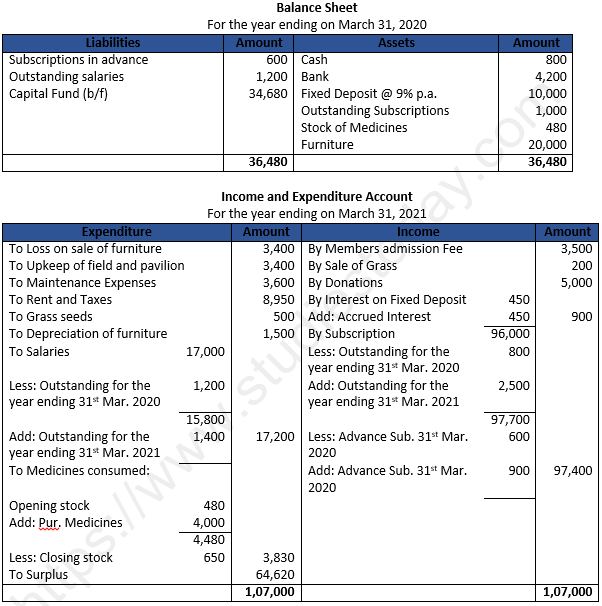

Question 6 (new).

Solution 6 (new).

Question 6.

Solution 6.

Point of Knowledge:-

- Receipts and Payments Account is a summary of cash (including bank) receipts and Payments during and accounting period, receipts and payments being shown under appropriate heads of accounts.

Question 7 (new).

Solution 7 (new).

Question 7.

Solution.

Question 8.

Solution 8.

Question 9.

Solution 9.

Question 10.

Solution 10.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 11.

Solution 11.

Question 12. (A)

Solution 12 (A).

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 12. (B)

Solution 12 (B)

Question 13.

Solution 13 .

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

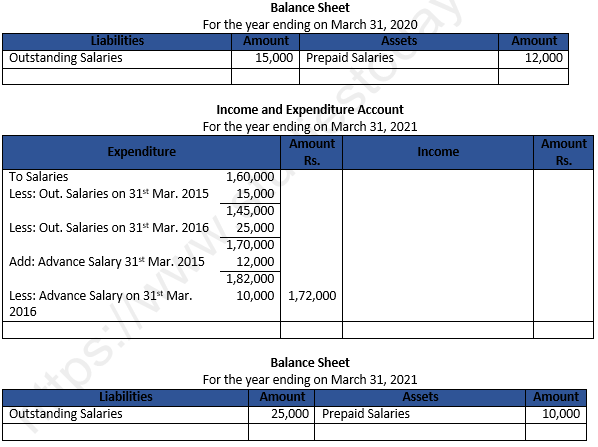

Question 14.

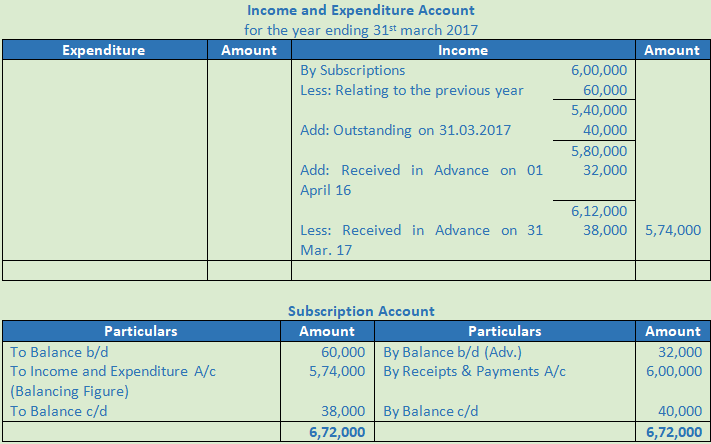

Solution 14.

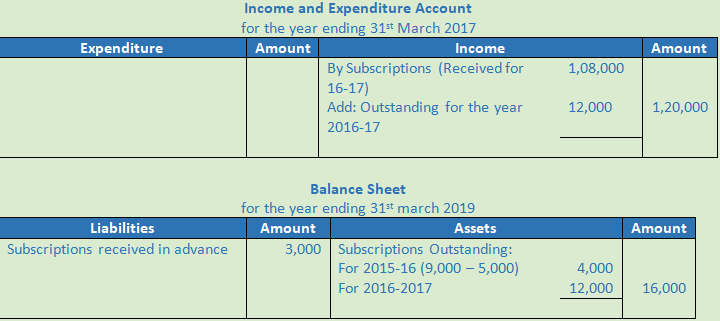

Working Note:-

Total subscription received during the year 2016-17 Rs. 1,20,000

Less: Amount received during the year 2016-17 Rs. 1,08,000

Outstanding subscriptions for the year 2016-17 Rs. 12,000

Question 15.

Solution 15.

Question 16 (new).

Solution 16.

Question 16.

Solution 16.

Question 17.

Solution 17.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 18.

Solution 18.

Point of Knowledge:-

Life membership fees and entrance fees to be capitalised.

Question 19.

Solution 19.

Question 20.

Solution 20.

Question 21.

Solution 21.

Question 22 (new) .

Solution (new).

Question 22.

Solution 22

Working Note:-

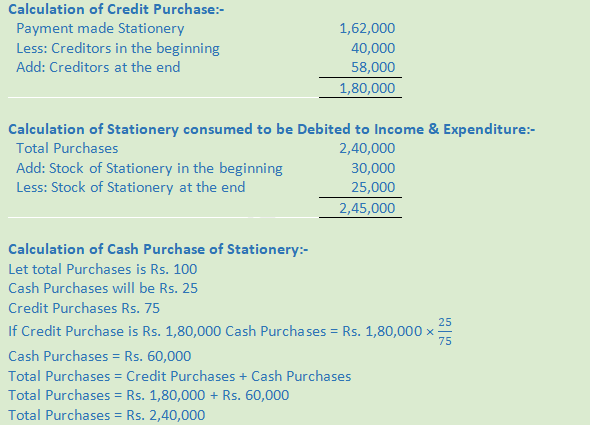

Creditors for Sports Materials will be ignored because purchased of sports materials given in the question.

Question 23 (new).

Solution 23 (new).

Question 23.

Solution 23.

Question 24.

Solution 24.

Question 25.

Solution 25.

Question 26 (new).

Solution 26. (new)

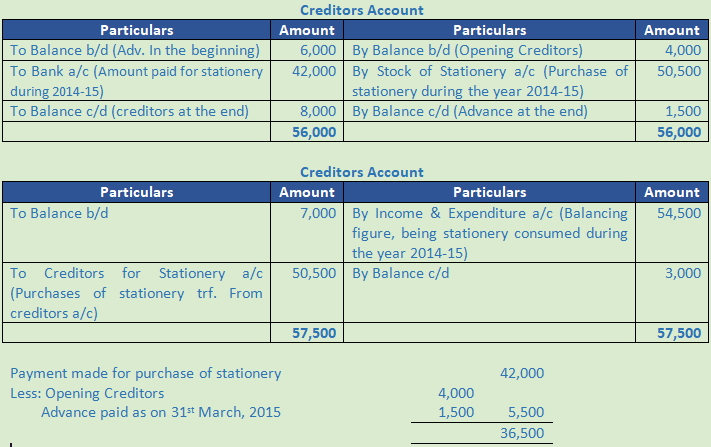

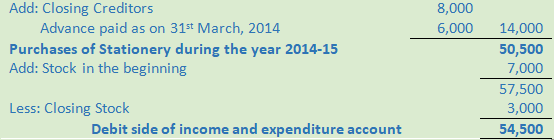

Payment made for purchase of stationery |

| 42,000 |

Less: Opening Creditors | 4,000 |

|

Advance paid as on 31st March, 2021 | 1,500 | 5,500 |

|

| 36,500 |

Add: Closing Creditors | 8,000 |

|

Advance paid as on 31st March, 2020 | 6,000 | 14,000 |

Purchases of Stationery during the year 2020-21 |

| 50,500 |

Add: Stock in the beginning |

| 7,000 |

|

| 57,500 |

Less: Closing Stock |

| 3,000 |

Debit side of income and expenditure account |

| 54,500 |

Question 26.

Solution 26.

Question 27.

Solution 27.

Question 28.

Solution 28.

Question 29 (A) (new).

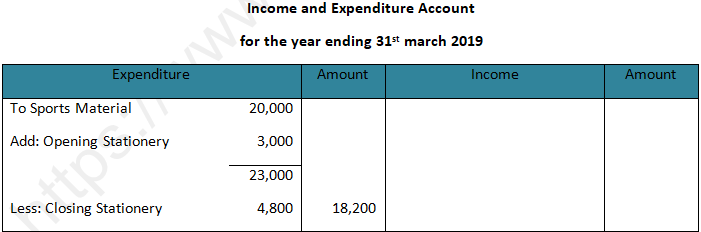

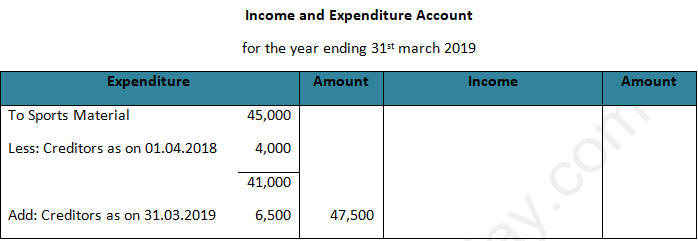

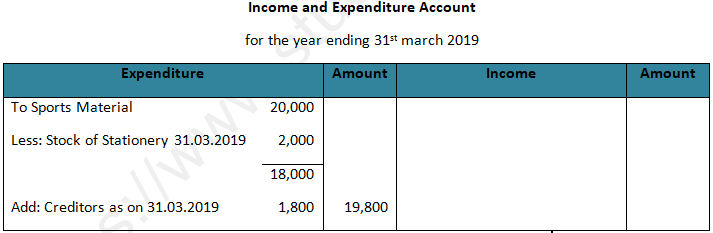

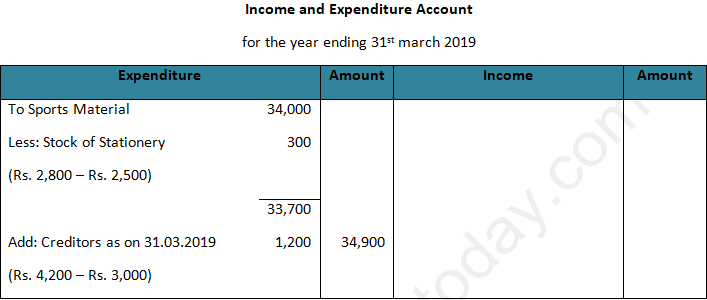

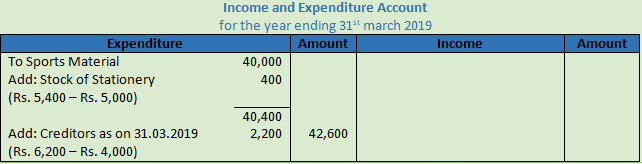

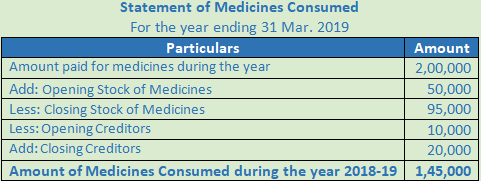

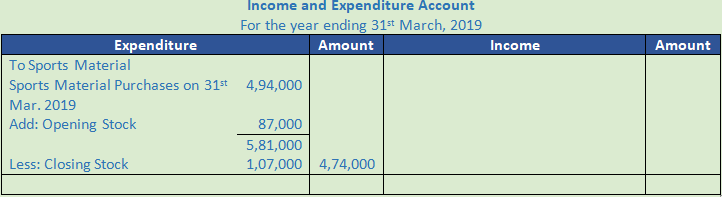

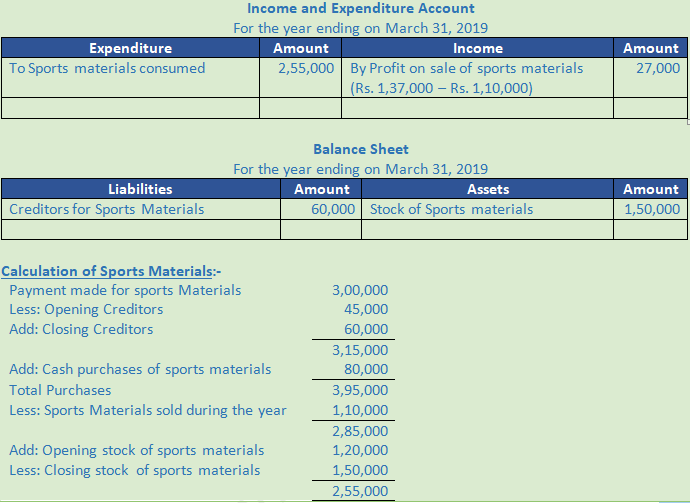

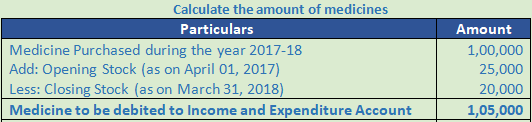

Solution 29. (A) (new). Calculation of Sports Material Consumed to be Debited to Income and Expenditure A/c:-

Points of Knowledge:-

Calculation of the Cost of Consumable Goods:-

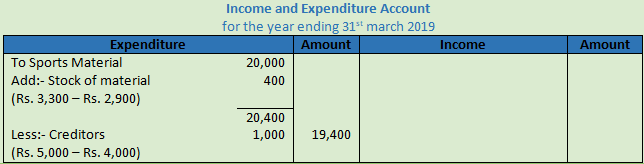

Question 29 (B)

Solution 29 (B). Calculation of Sports Material Consumed to be Debited to Income and Expenditure A/c:-

Assets side of the balance sheet stock of sports materials = Rs. 1,50,000

Liabilities side of the balance sheet creditors of sports materials = Rs. 60,000

Question 29 (new).

Solution 29.

Working Note:-

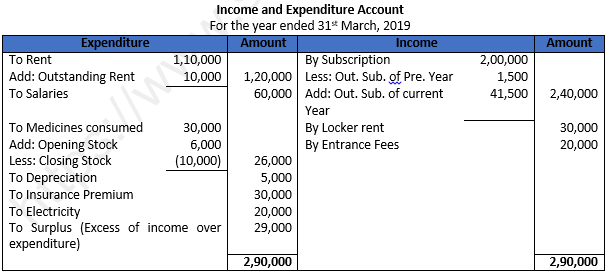

Outstanding Subscription = Rs. 41,500 – Rs. 1,500 = Rs. 40,000

Question 30 (new).

Solution 30 (new).

Question 30.

Solution 30.

Question 31 (new).

Solution 31 (new).

Question 31.

Solution 31.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 32.

Solution 32.

Question 33.

Solution 33.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 34 (new).

Solution 34 (new).

Working Note:-

Calculation of depreciation on furniture:-

Question 34.

Solution 34.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 35 (new).

Solution 35 (new).

Working Note:-

Calculation of depreciation:-

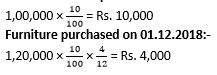

Machinery purchased on 01.oct.2018:-![]()

Question 35.

Solution 35.

Working Note:-

Total subscriptions receivable during the year 16-17 (500 × 50) 25,000

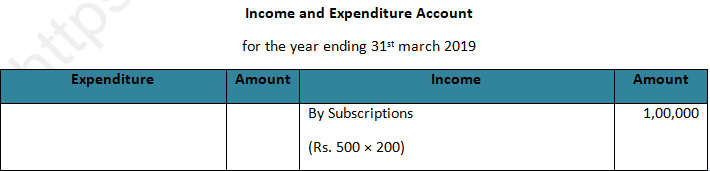

Less: Amount received during the year 2016-17 20,500

Outstanding subscriptions for the year 2016-17 4,500

Question 36.

Solution 36.

Working Note:-

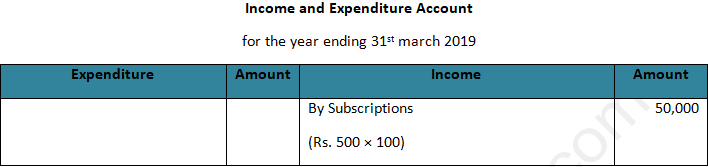

Total subscriptions receivable during the year 16-17 (500 × 50) 25,000

Less: Amount received during the year 2016-17 20,500

Outstanding subscriptions for the year 2016-17 4,500

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 37.

Solution 37.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 38.

Solution 38 (new).

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 38.

Solution 38.

Question 39 (new).

Solution 39 (new).

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 39.

Solution 39.

Question 40.

Solution 40.

Working Note:-

Interest Accrued shown on the assets side Rs. 10,000.

Question 41.

Solution 41.

Question 42.

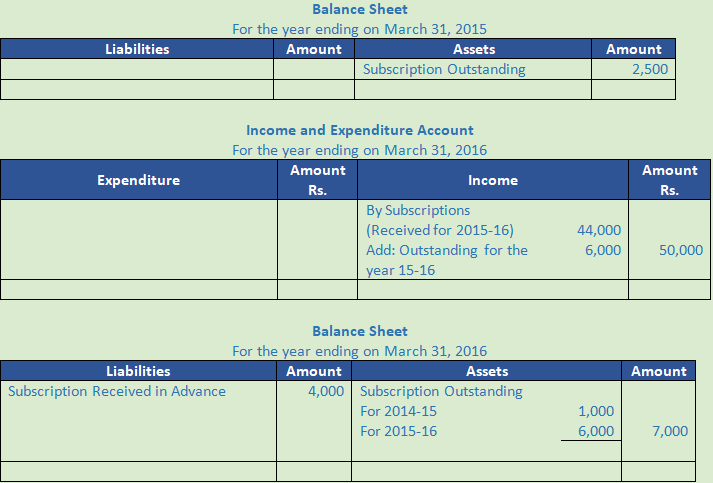

Solution 42.

Working Note:-

Total Subscriptions receivable during the year 2015-16 (100 × Rs. 500) Rs. 50,000

Less: Amount received during the year 2015-16 Rs. 44,000

_________________

Outstanding Subscriptions for the year 2015-16 Rs. 6,000

________________

Question 43.

Solution 43.

Point of Knowledge:-

Receipts and Payments Accounts is Prepared on cash basis, i.e. transactions and events which have been related to cash are shown in the account. This is the summary of the cash transaction as in the cash book.

Question 44.

Solution 44.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 45. .

Solution 45.

Question 46 (new).

Solution 46 (new).

Question 46.

Solution 46.

Question 47 (new).

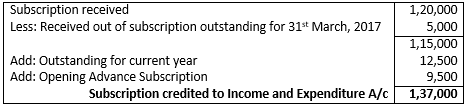

Solution 46 (new). Calculation of Subscription credited to Income and Expenditure A/c:-

Question 47.

Solution 47.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 48.

Solution 48.

Question 49.

Solution 49.

Point of Knowledge:-

Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Question 50.

Solution 50.

Point of Knowledge:-

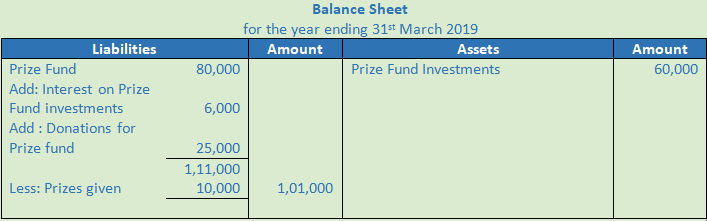

Donations received or funds set aside for specific purposes are credited to a separate Fund Account and are shown on the liabilities side of the Balance Sheet. The incomes from or donations for these funds are credited to respective Fund Account. On the other hand, expenses or Payments out of these funds are debited. Accounting when done on this basis is known as Fund Based Accounting.

Question 51.

Solution 51.

Question 52 (new).

Solution 52 (new).

Question 52.

Solution 52.

Question 53.

Solution 53.

Question 54.

Solution 54.

Question 55.

Solution 55.

Working Note:-

Calculation of Subscription:-

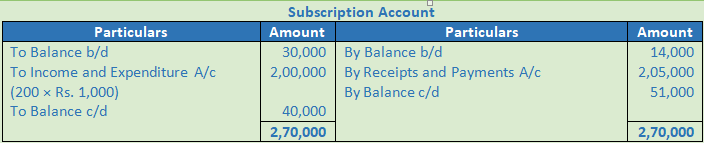

Subscriptions (200 × 1,000) 2,00,000

Add: Subscriptions for 2016-17 (60,000 – 40,000) 20,000

Less: Received Subscriptions during present year 94,000

Less: Received Subscriptions during the last year 25,000

______________

1,01,000

_____________

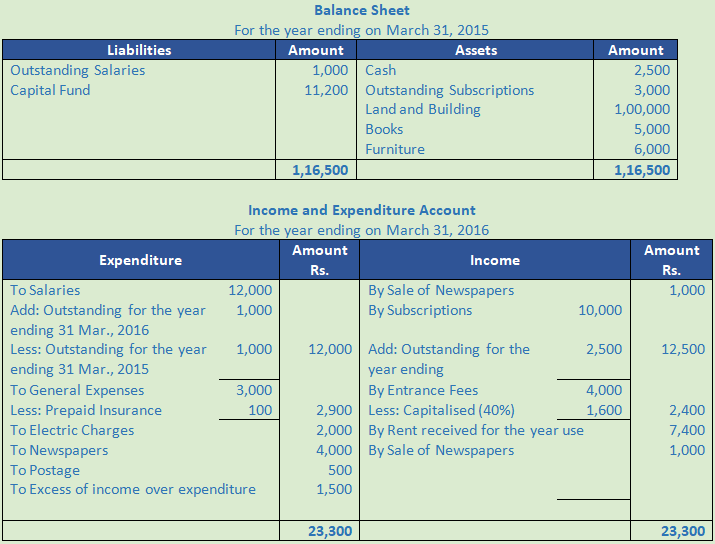

Point of Knowledge:-

Income and Expenditure Account is like profit and loss Account of an enterprise. Since, Not for Profit Organisation are not established for the purpose or earning profit, they do not prepare Profit and loss Account.