Read and download free pdf of CBSE Class 12 Accountancy Admission Of Partner Worksheet Set A. Students and teachers of Class 12 Accountancy can get free printable Worksheets for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner in PDF format prepared as per the latest syllabus and examination pattern in your schools. Class 12 students should practice questions and answers given here for Accountancy in Class 12 which will help them to improve your knowledge of all important chapters and its topics. Students should also download free pdf of Class 12 Accountancy Worksheets prepared by school teachers as per the latest NCERT, CBSE, KVS books and syllabus issued this academic year and solve important problems with solutions on daily basis to get more score in school exams and tests

Worksheet for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner

Class 12 Accountancy students should refer to the following printable worksheet in Pdf for Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner in Class 12. This test paper with questions and answers for Class 12 will be very useful for exams and help you to score good marks

Class 12 Accountancy Worksheet for Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner

MCQ Questions for NCERT Class 12 Accountancy Admission Of Partner

Question. A, B, C, and D are partners. A and B share 2/3rd of profits equally and C and D share remaining profits in the ratio of 3:2. Find the profit sharing ratio of A/ B, C and D.

(a) 5:5:3:2

(b) 7:7:6:4

(c) 2.5:2.5:8:6

(d) 3:9:8:3

Answer: A

Question. X and Y are partners in a firm with capital of Rs.180000 and Rs.200000. Z was admitted for 1/3rd share in profits and brings Rs.340000 as capital. Calculate the amount of goodwill

(a) 240000

(b) 100000

(c) 150000

(d) 300000

Answer: D

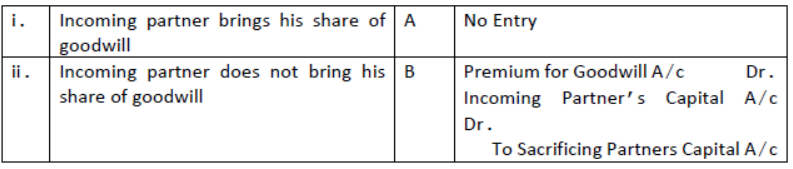

Question. Match the following with respect to journal entries for treatment of goodwill.

(a) i- B, ii-C, iii-A, iv-D

(b) i- C, ii-D, iii-A, iv-B

(c) i- D, ii-C, iii-A, iv-B

(d) i- D, ii-C, iii-B, iv-A

Answer: B

Question. General reserve at the time of admission of a partner is transferred to:

(a) Revaluation a/c

(b) Partners’ capital a/c

(c) Neither of two

(d) Profit and loss a/c

Answer: B

Question. A and B are partners sharing profits and losses in the ratio of 5:3. On admission, C brings Rs.70000 as capital and Rs.43000 against goodwill. New profit ratio between A, B and C is 7:5:4. The sacrificing ratio of A and B is:

(a) 3:1

(b) 1:3

(c) 4:5

(d) 5:9

Answer: A

Question. At the time of admission of a new partner, the balance of Workmen Compensation Reserve will be transferred to:

(a) Old partners in the old profit sharing ratio

(b) Sacrificing partners in the sacrificing ratio

(c) Revaluation Account

(d) All partners in the new profit sharing ratio

Answer: A

Question. On the admission of a new partner:

(a) Old partnership is dissolved

(b) Both old partnership and firm are dissolved

(c) Old firm is dissolved

(d) None of the above

Answer: A

Question. If at the of admission, some balance of profit and loss account appears in the books, it will be transferred to :

(a) Profit and loss adjustment account

(b) All partners’ capital account

(c) Old partners’ capital account

(d) Revaluation account

Answer: C

Question. Premium brought by newly admitted partner should be:

(a) Credited to sacrificing partners

(b) Credited to all partners in the new profit sharing ratio

(c) Credited to old partners in the old profit sharing ratio

(d) Credited to only gaining partners

Answer: A

Question. When a new partner brings his share of goodwill in cash, the amount is debited to:

(a) Cash account

(b) Capital accounts of the new partner

(c) Goodwill account

(d) Capital accounts of the old partner

Answer: A

Question. The balance in the investment fluctuation fund after meeting the fall in book value of investment, at the time of admission of partner will be transferred to:

(a) Revaluation account

(b) Capital accounts of old partners

(c) General reserve

(d) Capital account of all partners

Answer: B

Question. The proportion in which old partners make a sacrifice:

(a) Ratio of capital

(b) Ratio of sacrifice

(c) Gaining ratio

(d) Profit sharing ratio

Answer: B

Question. If the new partner brings his share of goodwill in cash, it will be shared by old partners in:

(a) Sacrificing ratio

(b) Old profit sharing ratio

(c) New ratio

(d) Capital ratio

Answer: A

Question. Which of the following is not the reconstitution of partnership?

(a) Admission of a partner

(b) Dissolution of Partnership

(c) Change in Profit Sharing Ratio

(d) Retirement of a partner

Answer: B

Question. New partner may be admitted to partnership:

(a) With the consent of all the old partners

(b) With the consent of any one partner

(c) With the consent of 2/3rd of the old partners

(d) With the consent of 3/4th of the old partners

Answer: A

Question. A, and B are partners sharing profits in the ratio of 2:3. Their balance sheet shows machinery at ₹2,00,000; stock ₹80,000, and debtors at ₹1,60,000. C is admitted and the new profit sharing ratio is 6:9:5. Machinery is revalued at ₹1,40,000 and a provision is made for doubtful debts @5%. A’s share in loss on revaluation amount to ₹20,000. Revalued value of stock will be:

(a) ₹62,000

(b) ₹1,00,000

(c) ₹60,000

(d) ₹98,000

Answer: C

Question. Yash and Manan are partners sharing profits in the ratio of2:1. They admit Kushagra into partnership for 25% share of profit. Kushagra acquired the share from old partners in the ratio of 3:2. The new profit sharing ratio will be:

(a) 14:31:15

(b) 3:2:1

(c) 31:14:15

(d) 2:3:1

Answer: C

Question. When goodwill is not recorded in the books at all on admission of a partner:

(a) If paid privately

(b) If brought in cash

(c) If not brought in cash

(d) If brought in kind

Answer: A

Question. At the time of admission of a new partner, the entry for unrecorded investment will be:

(a) Dr. Investment A/c and Cr. Revaluation A/c

(b) Dr. Partners’ Capital A/c and Cr. Investment A/c

(c) Dr. Revaluation A/c and Cr. Investment A/c

(d) None of the above

Answer: A

Question. Heena and Sudha share Profit & Loss equally. Their capitals were Rs.1,20,000 and Rs. 80,000 respectively. There was also a balance of Rs. 60,000 in General reserve and revaluation gain amounted to Rs. 15,000. They admit friend Teena with 1/5 share. Teena brings Rs.90,000 as capital. Calculate the amount of goodwill of the firm.

(a) Rs.85,000

(b) Rs.1,00,000

(c) Rs.20,000

(d) None of the above

Answer: A

True Or False:

Question. “Unless agreed otherwise, Sacrificing Ratio of the old partners will be the same as their Old Profit Sharing Ratio”.

Answer: True

Question. Hidden goodwill arises when total capital is computed based on the new partner’s capital is less than total capitals of remaining partners after all adjustments.

Answer: False

Question. New partner may or may not contribute capital at the time of admission.

Answer: True

Question. New partner may bring his share of goodwill premium in kind.

Answer: True

Question. Employee Provident Fund is a part of Accumulated profits and reserves.

Answer: False

Question. The need for valuation of goodwill also arises when the firm is dissolved involving sale of business as a going concern.

Answer: True

Question. New partner brings goodwill in the firm to get share in the past profits.

Answer: False

Question. At the time of admission, reserves may be carried forwarded by the partners.

Answer:True

Question. “As per Section 26 of the Indian Partnership Act, 1932, a person can be admitted as a new partner if it is agreed in the Partnership Deed”.

Answer: False

Question. Claim of workmen compensation if more than workmen compensation reserve, is debited to revaluation account.

Answer: True

Fill in the blanks :

Question. In case of upward revaluation of a liability, revaluation account is …………….

Answer: Debited

Question. A and B are partners sharing profits equally. They admit C for 1/3 share in profits. A debtor whose dues of Rs.5000 were written off as bad debts, paid Rs.4000 in full settlement. Bad debts recovered Rs.4000 will be debited to …………and credited to ……………

Answer: Cash account, revaluation account

Question. On the admission of a new partner, after revaluation has been done, the value of assets and liabilities appear in the books of the firm at………….

Answer: their current value

Question. At the time of admission of a partner, new profit sharing is used for sharing future………

Answer: Profit

Question. when the value of goodwill of the firm is not given but has to be inferred on the basis of net worth of the firm, it is called……………

Answer: Hidden goodwill

Question. At the time of admission, it the book value and the market value of investment is same then investment fluctuation reserved is transferred to …………….account of the old partners in their ………..ratio.

Answer: Capital accounts of old partners, old profit sharing ratio

Question. At the time of admission, the assets are revalued and liabilities are reassessed. The increase or decrease in the values is debited or credited in ……………..

Answer: Revaluation account

Question. Revaluation account is a …………………

Answer: Nominal account

Question. The newly admitted partner brings his/ her share of capital for which he/she will get ……….in firm.

Answer: Profit share

Question. Goodwill appearing in the books oat the time of admission of a new partner is written off by debiting …………..and crediting …………

Answer: Old partners'capital accounts, goodwill account

ONE MARK QUESTIONS.

Question. Why is it necessary to revalue assets and reassess liabilities of a firm in case of admission of a new partner?

Answer: The assets are revalued and liabilities of a firm are reassess, at the time of admission of a partner because the new partner should; neither benefit nor suffer because change in the value of assets and liabilities as on the date of admission.

Question. What are the accumulated profit and accumulated losses?

Answer: The profit accumulated over the years and have not been credited to partners’ capital A/c are known as accumulated Profit or undistributed profit, e.g. the General Reserve, Profit and Loss A/c (credit balance). The losses which have not yet been written off to the debit of Partners’ Capital A/c are known as accumulated Losses, e.g. the Profit and Loss A/c appearing on the assets side of Balance Sheet, etc.

Question. Explain the treatment of goodwill in the books of a firm on the admission of a new Partner when goodwill already appears in the Balance sheet at its full value and the new partner brings his share of good will in cash.

Answer: By following accounting standard - 10, the existing goodwill (i.e. goodwill appearing in the Balance Sheet) is written off to the old partners’ Capital a/c in their old profit sharing ratio.

Old partners’ capital A/c Dr.

To Goodwill A/c

[Being the existing g/w written off in the old ratio.]

Question. Under what circumstances the premium for goodwill paid by the incoming Partner will not recorded in the books of Accounts?

Answer: When the premium for goodwill is paid by the incoming partner privately, it is not recorded in the books of A/c as it is as a matter outside the business.

Question. When a new partner is admitted into the firm the old partner stands to :

(a) Gain in profit sharing ratio

(b) Lose in profit sharing ratio

(c) Not affected at all

(d) Only one partner gain other loose

Answer: B

Question. If at the time of admission if there is some unrecorded liability, it will be -------------to -- ------------ Account.

(a) Debited, Revaluation

(b) Credited, Revaluation

(c) Debited, Goodwill

(d) Credited, Partners’ Capital

Answer: A

Question. When new partner brings cash for goodwill, the amount is credited to:

(a) Realization account

(b) Cash account

(c) Premium for goodwill account

(d) Revaluation account

Answer: C

Question. Match the following:

(a) i- B, ii-C, iii-A, iv-D

(b) i- D, ii-B, iii-A, iv-C

(c) i- D, ii-C, iii-A, iv-B

(d) i- D, ii-C, iii-B, iv-A

Answer: C

Question. All accumulated losses are transferred to the capital a/c of the partners in:

(a) New profit sharing ratio

(b) Old profit sharing ratio

(c) Capital ratio

(d) None of the above

Answer: B

Question. On admission of a new partner, the method of valuation of goodwill is decided by:

(a) the new partner only

(b) the old partners only

(c) the old partners and the new partner

(d) the accountant of the firm

Answer: C

Question. When is Revaluation A/c prepared?

(a) At the time of admission

(b) At the time of retirement

(c) At the time of death

(d) All of the above

Answer: D

Question. Revaluation account is a :

(a) Real account

(b) Nominal account

(c) Personal account

(d) None of the above

Answer: B

Question. At the time of admission of a partner, Employees Provident Fund is:

(a) Distributed to partners in the old profit sharing ratio

(b) Distributed to partners in the new profit sharing ratio

(c) Adjusted through gaining ratio

(d) None of the above

Answer: D

Question. A and B are partners sharing profits in the ratio of 3:2. They admit C for ¼ Rs.30000 for his share of goodwill. The total value of the goodwill of the firm will be:

(a) 150000

(b) 120000

(c) 100000

(d) 160000

Answer: B

Question. The credit balance of profits abnd loss account appears in the books at the time of admission of partner will be transferred to:

(a) Profit and loss appropriation account

(b) All partners capital account

(c) Old partners capital account

(d) Revaluation account

Answer: C

Question. Goodwill of the firm is valued at Rs.100000. Goodwill also appears in the books at RS.50000. C is admitted for ¼ share. The amount of goodwill to be brought in by C will be:

(a) 20000

(b) 25000

(c) 30000

(d) 40000

Answer: B

Question. If the new partner brings any additional cash other than his capital contributions then it is termed as:

(a) Capital

(b) Reserves

(c) Profits

(d) Premium for goodwill

Answer: D

Question. A and B are partners sharing profits and losses in the ratio of 3:2. C is admitted for 1/5 share in profits which he gets from A. New profit sharing ratio will be:

(a) 12:8:5

(b) 8:12:5

(c) 2:2:1

(d) 2:2:2

Answer: C

Question. Anil and Aman are partners sharing profits and losses in the ratio of 3:2. Akhil is admitted as a new partner for 1/3rd share in the profits. Goodwill of the firm is valued at Rs.60000 and goodwill already appears in the books at Rs.18000. It is decided that the existing goodwill should continue to appear in the books at its old value. Akhil’s share of goodwill is:

(a) 26000

(b) 14000

(c) 20000

(d) 6000

Answer: B

Question. Ajay and Vijay are partners sharing profits in the ratio of 2:1. Ajay’s son Anil was admitted for ¼ share of which 1/8 was gifted by Ajay to his son. The remaining was contributed by Vijay. Goodwill of the firm is valued at Rs.40000. How much of the goodwill will be credited to each of old partners’ capital account:

(a) 2500

(b) 5000

(c) 20000

(d) None of the above

Answer: B

Question. Aryaman and Bholu are partners sharing profit and losses in ratio of 5:3. Chirag is admitted for 1/4th share. On the date of reconstitution, the debtors stood at Rs 40,000, bill receivable stood at Rs. 10,000 and the provision for doubtful debts appeared at Rs. 4000. A bill receivable, of Rs 10,000 which was discounted from the bank, earlier has been reported to be dishonored. The firm has sold, the debtor so arising to a debt collection agency at a loss of 40%. If bad debts now have arisen for Rs 6,000 and firm decides to maintain provisions at same rate as before then amount of Provision to be debited to Revaluation Account would be:

(a) Rs 4,400

(b) Rs 4,000

(c) Rs.3,400

(d) None of the above

Answer: C

Question. A and B are partners sharing profits and losses in the ratio of 3:2. A’s capital is Rs.120000 and B’s capital is Rs.60000. they admit C for 1/5th share of profits. C should bring as his capital:

(a) 36000

(b) 48000

(c) 58000

(d) 45000

Answer: D

Question. Profit or loss on revaluation of assets is transferred to Partners’ Capital account in which ratio?

(a) Equally

(b) Profit sharing ratio

(c) Fixed capital ratio

(d) Current capital ratio

Answer: B

Question. Share of goodwill brought by the new partner in cash is shared by old partners in:

(a) ratio of sacrifice

(b) old profit sharing ratio

(c) new profit sharing ratio

(d) none of the above

Answer: A

True Or False:

Question. In the case of admission of a partner, all existing partners sacrifice.

Answer: False

Question. Admission of a partner changes the relationship between / among existing partners.

Answer: True

Question. At the time of admission of partner, the partnership firm is dissolved.

Answer: False

Question. Admission of a new partner does not amount to reconstitution of the partnership firm.

Answer: False

Question. The goodwill brought at the time of admission of partner will be distributed among all the partners in new profit sharing ratio.

Answer: False

Question. Reserve and accumulated profits are distributed in old profit sharing ratio at the time of admission of a partner.

Answer: True

Question. “At the time of admission, old partnership comes to an end”.

Answer: True

Question. Increase in provision for doubtful debts will credited to revaluation account.

Answer: False

Question. Goodwill exists only when firm earns super profits.

Answer: True

Question. “A newly admitted partner cannot pay his share of the goodwill to the sacrificing partners privately”.

Answer: False

Fill in the blanks :

Question. General reserve account indicates ………..and shows ………..balance.(

Answer: Accumulated profits, credit

Question. Revaluation account shows ………….in the values of assets and liabilities.

Answer: Increase or decrease

Question. Gain or loss arising from revaluation is shared by ………..partners in …………ratio.

Answer: Old partners, old profit sharing ratio

Question. A, B and C are partners sharing profits and losses in the ratio of 3:2:1. On admission of D, they agree to share profits and losses in the ratio of 5:4:2:1. Sacrificing ratio of A, B and C will be………..

Answer: Only A sacrifice- 1/12

Question. R and S are partners sharing profits equally. They admitted T for 1/3 share in the firm. New profit sharing ratio will be………..

Answer: Equal

Question. If, at the time of admission of a new partner, provision for doubtful debts is to be reduced, it shall be …………to profit and loss adjustment account.

Answer: Credited

Question. Vinay and Naman are partners sharing profit in the ratio of 4:1. Their capitals were Rs.90000 and Rs.70000 respectively. They admitted Pratik for 1/3 share in the profits. Pratik brings Rs.100000 as his capital. The value of firm’s goodwill be…………..

Answer: 40000

Question. In the case of downward revaluation of an asset, revaluation account is ………………

Answer: Debited

Question. Debit balance in the profit and loss account indicates…………….

Answer: Accumulated loss

Question. If the revaluation account finally shows a debit balance then it indicates ………….., which will be transferred to …………

Answer: Net loss, debit side of old partners’ capital accounts

SHORT ANSWER TYPE-QUESTIONS

Question. Himanshu and Naman share profits & losses equally. Their capitals were Rs.1,20,000 and Rs. 80,000 respectively. There was also a balance of Rs. 60,000 in General reserve and revaluation gain amounted to Rs. 15,000. They admit friend Ashish with 1/5 share. Ashish brings Rs.90,000 as capital. Calculate the amount of goodwill of the firm.

Answer : Rs. 85,000

Question. Why is it necessary to revalue assets and reassess liabilities at the time of admission of new partner?

Answer : It is necessary to revalue assets and reassess liabilities at the time of admission of new partners as if assets and liabilities are overstated or understated in the books then its benefits or loss should not affect the near partner.

Question. A and B were partners sharing profits in the ratio of 3:2. A surrenders 1/6th of his share and B surren-ders 1/4th of his share in favour of C, a new partner. What is the new ratio and the sacrificing ratio. 74

Answer : Old ratio = A: B = 3:2

A surrender = 3/5 X 1/6 = 3/30 =1/10

B surrender = 2/5 X 1/4 = 1/10

A’s new share = 3/5 – 1/10 = 5/10

B’s new share = 2/5 – 1/10 = 3/10

C’s new share = 1/10 +1/10 = 2/10

New ratio = 5/10, 3/10, 2/10 OR 5:3:2

Sacrificing Ration = Old ratio – New ratio

A = 3/5 – 5/10 = 1/10

B = 2/5 – 3/10 = 1/10

Sacrificing ratio = 1:1

Question. Yash and Manan are partners sharing profits in the ratio of2:1. They admit Kushagra into partnership for 25% share of profit. Kushagra acquired the share from old partners in the ratio of 3:2. Calculate the new profit sharing ratio.

Answer : 31:14:15

Question. Aarti and Bharti are partners sharing profits in the ratio of 5:3. They admit Shital for 1/4th share and agree to share between them in the ratio of 2:1 in future. Calculate new and sacrificing ratio.

Answer : Old ratio = 5:3

Shital = 1/4th Share

Let the profit be Rs. 1

Remaining profit = 1-1/4 =3/4

Arti : Babita = 2:1

Arti’s share = 3/4 X 2/3 = 1/2

Babita’s Share = 3/4 X 1/3 = 1/4

New Ratio = 1/2, 1/4, 1/4 Or 2:1:1

Sacrificing ratio = Old ratio – New ratio

Arti’s sacrifies = 5/8 – 2/4 = 1/8

Babita’s Sacrifies = 3/8 – 1/4 = 1/8

Sacrificing Ratio = 1:1

Question. The capital of a firm of Arpit and Prajwal is Rs. 10,00,000. The market rate of return is 15% and the goodwill of the firm has been

valued Rs. 1,80,000 at two years purchase of super profits. Find the average profits of the firm. (i) Super profit = Value of goodwill /Number of

Answer : years purchase

= 180000/2

= 90000

(ii) Normal Profit = Capital employed X Normal rate of return /100

= 1000000 X 15/ 100

= 150000

(iii) Average Profit = Normal Profit + Super profit

= 150000 + 90000

= 240000

Question. On what occasions does the need for valuation of goodwill arise?

Need of valuation of goodwill arises on the following occasions:-

Answer : (i) Change in profit sharing ratio of existing partners.

(ii) Admission of a partner.

(iii) Retirement of a partner.

(iv) Death of a partner

Question. A new partner should contribute towards goodwill on his admission because

(a) Goodwill is an important asset.

(b) The new partner should compensate the old partners for their sacrifice.

(c) That goodwill to be shared by all partners in new profit sharing ratio.

(d) None of the above

Answer : B

Question. The value of furniture given in the old Balance Sheet was ₹66,000 which was overvalued by 10%. The effect of the above transaction in the Revaluation A/c will be:

(a) ₹6,000 will be debited to Revaluation A/c

(b) ₹6,600 will be debited to Revaluation A/c

(c) ₹ 6,000 will be credited to Revaluation A/c

(d) ₹ 6,600 will be credited to Revaluation A/c

Answer : A

Question. A and B share profits in the ratio of 4:1. C is admitted for 1/6th share for which pays ₹ 20,000 for goodwill. New profit sharing ratio is 3:2:1. Journal entry for treatment of goodwill will be:

(a) Premium A/c Dr. 20,000

To A’s Capital A/c 16,000

To B’s Capital A/c 4,000

(b) Premium A/c Dr. 20,000

A’s Capital A/c 16,000

To B’s Capital A/c 36,000

(c) Premium A/c Dr. 20,000

B’s Capital A/c 16,000

To A’s Capital A/c 36,000

(d) Premium A/c Dr. 20,000

To A’s Capital A/c 14,000

To B’s Capital A/c 6,000

Answer : C

Question. The opening balances of X and Y are ₹30,000 each closing balance of capital are ₹50,000 each. They admit Z as a partner for 1/4th share in the profits of the firm. Z brings ₹ 80,000 as his share of capital. The P&L A/c showed a credit balance of ₹ 40,000 on Z’s admission. What will be the amount of goodwill brought by Z?

(a) ₹ 1,50,000

(b) ₹1,00,000

(c) ₹ 50,000

(d) ₹2,00,000

Answer : B

Question. What will be the journal entry to distribute General Reserve and P&L A/c (Dr.) balance given in Balance sheet to the old partners at the time of admission of a new partner?

(a) P&L A/c Dr.

Gaining Partner’s Capital A/c Dr.

To Sacrificing Partner’s Capital A/c

To General Reserve A/c

(b) P&L A/c Dr.

General Reserve A/c Dr.

To Old Partner’s Capital A/c

(c) General Reserve A/c Dr.

Old Partner’s Capital A/c Dr.

To Old Partner’s Capital A/c

To P&L A/c

(d) Old Partner’s Capital A/c Dr.

To P&L A/c

To General Reserve A/c

Answer : C

Q 1 List the two rights of a new partner.

Q 2 What share of future profits does an incoming partner get?

Q 3 Define sacrificing ratio.

Q 4 Why is incoming partner required to bring goodwill at the time of admission?

Q 5 Who gets the goodwill brought by the incoming partner?

Q 6 Why are the assets & liabilities revalued at the time of admission of a partner/

Q 7 A & B are partners in a firm. C is admitted with 1/4th share which he takes equally from A & B. The Balance sheet of A & B showed the following items. Pass the necessary journal entries for the same on C’s admission.

General Reserve Rs 40000 : Profit & Loss a/c (Dr) Rs 30000 : Goodwill (Dr) Rs 10000 Deferred Revenue Expenditure Rs 15000.

Q 8 A ,B & Care partners sharing profits & losses in the ratio of 3:2:1. D is admitted with 1/6th share. C wants to retain his original profit sharing ratio. Calculate the new profit sharing ratio & sacrificing ratio.

Q 9 X & Y are partners sharing in the ratio of 3:2. Z is admitted with 1/6th share. X & Y decide to share future profits in the ratio of 2:3. Z brings in Rs 30000 as his share of goodwill. Calculate the new profit sharing Ratio & sacrificing ratio. Pass the necessary journal entries.

Q 10 A ,B & C are partners sharing P&L in the ratio of 2:3:5. D is admitted with 1/6th share.

Capitals of A , B & C after all necessary adjustments were Rs 250000, 125000 & 75000 resp. Calculate the amount of capital brought in by new partner.

Q 11 P & Q are partners in a firm . R is admitted in the firm with i/3rd share. P & Q decide to share future profits in the ratio of 1;2. Goodwill appears in the books at Rs 10000. R brings in 200000 as capital & his share of goodwill in cash. On R’s admission goodwill is valued at Rs 120000. Partners withdraw ½ the goodwill in cash. Pass the necessary journal entries,

Q 12 A , B & C are partners sharing profits in the ratio of 2:3:5. They admit D into partnership & he brings 32000 as capital for 1/6th share. The capital of A , B & C after all necessary adjustments were 33780, 40670 & 46450 resp. Capitals of the partners shall be proportionate to their profit sharing ratio. Calculate the capitals of the partners & the amount of cash deficiency / surplus.

Q 13 A & B are partners sharing in the ratio of 3:2. Their capitals after all necessary adjustment are Rs 30000 & Rs 20000 resp. C is admitted for 1/5th share& he brings Rs 20000 as his capital but is not able to bring his share of goodwill in cash. Firm’s goodwill is valued at Rs 20000. Capital of the partners is to be readjusted on the basis of profit sharing ratio. Calculate the capitals of the partners & the amount of cash deficiency / surplus.

ADMISSION OF A PARTNER Calculation of New Profit Sharing Ratio

Calculation of New Profit Sharing Ratio

1. A and B are Partners sharing Profits and Losses in the ratio 3:1. C was admitted as a new Partner for 1/4th share. Calculate the new Profit sharing ratio.

2. A and B are Partners sharing Profits and Losses in the ratio 2:3. C was admitted as a new Partner for 1/5th share. Calculate the new Profit sharing ratio.

3. A, B and C are Partners sharing profits and losses in the ratio3:1:1. D is admitted as a new partner for 1/5th share and C retains his original share. Calculate the NPSR.

4. P, Q and R are Partners sharing profits and losses in the ratio 3:2:1. S is admitted as a new partner for 1/6th share and Q retains his original share. Calculate the NPSR.

5. A and B are Partners sharing Profits and Losses in the ratio 3:2. C was admitted as a new Partner for 1/4th share. A and B will share future profits in the ratio 2:1. Calculate the new Profit sharing ratio.

6. A and B are Partners sharing Profits and Losses in the ratio 5:3. C was admitted as a new Partner for 1/5th share. A and B will share future profits in the ratio 1:1. Calculate the new Profit sharing ratio.

7. A and B are Partners sharing Profits and Losses in the ratio 3:2. C was admitted for 3/7th share. which he acquires 2/7th from A and 1/7th from B. Calculate the new Profit sharing ratio.

8. M and N are Partners sharing Profits and Losses in the ratio 5:3. O was admitted for 1/5th share which he acquires 1/10th from M and 1/10th from N.. Calculate the new Profit sharing ratio.

9. X and Y are Partners sharing Profits and Losses in the ratio 3:2. Z was admitted as a new partner. X surrendered 1/5th of his share and Y surrendered 2/5th of his share in flavor of Z Calculate the new Profit sharing ratio.

10. X and Y are Partners sharing Profits and Losses in the ratio 4:3. Z was admitted as a new partner. X surrendered 1/4th of his share and Y surrendered 1/3rd of his share in flavor of Z Calculate the new Profit sharing ratio.

11. X and Y are Partners sharing Profits and Losses in the ratio 9:6. Z was admitted as a new partner. X surrendered 3/15th of his share and Y surrendered 6/15th of his share in flavor of Z Calculate the new Profit sharing ratio.

12. X and Y are Partners sharing Profits and Losses in the ratio 3:2. Z was admitted as a new partner. X gives 1/3rd of his share and Y gives 1/10th from his share Calculate the new Profit sharing ratio.

13. A, B ,C and D are Partners sharing profits and losses in the ratio 9:6:5:5 respectively. E joined the firm as a new partner for 20% share. A,B C and D would in future share profits among themselves as 3:4:2:1.Calculate the NPSR.

14. A and B are Partners sharing Profits and Losses in the ratio 3:1. C was admitted as a new Partner for 1/4th share. C acquired his share in the proportion 2:1. Calculate the new Profit sharing ratio.

15. A and B are Partners sharing Profits and Losses in the ratio 4.1 C was admitted as a new Partner for 1/5th share. C acquired his share in the proportion 3:2. Calculate the new Profit sharing ratio.

16. P, Q and R are Partners sharing profits and losses in the ratio 3:2:1. S is admitted as a new partner for 1/6th share and the new profit sharing ratio will be 4:3:3:2. Calculate the Sacrificing share

17. A and B are Partners sharing Profits and Losses in the ratio 4.3 C was admitted as a new Partner for 1/5th share. C acquired his share in the proportion 3:2. Calculate the new Profit sharing ratio.

18. Ajit, Baljit and Charanjit are partners sharing profits in 5 : 3 : 2 ratio . They admitted Ajit’s son Daljit for 1/8th of the share which he acquired entirely from his father Ajit. Calculate new profit sharing ratio.

19. Mohan and Sohan are partners sharing profits in the ration of 3 : 2. They admit Karan and give him 1/5th share. He gets it equally from Mohan and Sohan. Find out the new ratio.

20. Amar, Bharat and Charat are partners sharing profits in the ratio of 5 : 3 : 2. They admit Sheetal and give him 20 % share. He gets his share from the old partners in their old ratio of 5 : 3 : 2. Calculate the new ratio.

21. Anu , Beena and Leena are sharing profits in the ratio of 5 : 3 : 2 . They admit Disha and give her 1/8th share, which she gets from Anu, Beena and Lena in the ratio of 3: 2: 1. Calculate the new ratio.

22. X and Y share profits in the ratio of 3: 2. They admit Z with 3/7 share in profits. He gets this share as 1/7 from X and 2/7 from Y. Calculate the new ratio.

23. Lalit, Mohan and Narinder share profits in the ratio of 3: 2: 1. They admit Upendra with 1/8th share in future profits. Calculate the new ratio.

24. Ajit and Baljit are partners sharing profits in the ratio of 3: 2. They admit Surjit as a new partner.Ajit surrenders 1/4th of his share and Baljit sacrifices 1/5th of his share. Calculate the new ratio.

25. A, B and C are partners sharing profits as 5 : 3 : 2 . They admit D and give him 1/5th of the share. It is decided that C’s share will not change. Calculate new ratio.

26. Amar and Akbar share profits in the ratio of 3 ; 2. They admit Babar with 1/6th of the share. Calculate the new ratio and sacrificing ratio.

27. X & Y share profits in the ratio of 4: 1. They admit Z with 1/5th share, which he gets only from X. Calculate new ratio and sacrificing ratio.

28.Laxman and Mohan share profits in the ratio of 5: 2. They admit Sunder with 1/8TH share. Sunder gets it: a) equally from Laxman and Mohan b) In the ratio of 3: 1 from Laxman and Mohan respectively. Calculate the sacrificing ratio in both the above cases.

29. Preeti and Ritu share in the ratio of 7: 3. The admit Anshu. Preeti gives 1/3rd of her share and Ritu give 1/4th of her share to Anshu. Calculate Sacrificing ratio.

30. Seeta and Geeta shared profits in the ratio of 3: 2. Rita was admitted with 1/5th share. It was agreed that Seeta and Geeta will share future profits in the ratio of 2: 1. Calculate the new ratio and the sacrificing ratio.

31.Mala and Shalu shared pforits in the ratio of 3: 2. They admitted Kamala and agreed that their ratio will be 5: 3: 2. Calculate the sacrificing ratio.

32.Akash and Prakash shared profits as 2 : 3 . They admit Sudesh as a new partner. Akash, Prakash and Sudesh decide to share their profits in the ratio of 3: 2: 2 respectively. Calculate the gain or sacrifice made by each of the old partners on the admission of Sudesh.

Treatment of Goodwil

1) M and J are partners sharing profits in the ratio of 3:2. They admitted R as a new partner. The new profit sharing ratio between M, J and R will be 5:3:2. R brought ₹25,000 for his share of Goodwill. Pass the necessary journal entries for goodwill.

2) Piyush and Deepika are partners sharing profits in the ratio of 7:3. They admit Seema as a new partner paying ₹4,000 as premium for 1/5th share. The new profit being 5:3:2. Pass journal entries.

3) A and B are partner sharing profits in the ratio of 3:2. Goodwill appears in their books at ₹3,000. They admit C into partnership, C paying a premium of ₹1,000 for one-fourth share in profits. A and B as between themselves sharing profits as before.

4) A and B are partners sharing profits in the ratio of 3:2. They admit C as new partner. C pays a premium of ₹3,000 for 3/10 share of profits which he acquires from A and B in the ratio of 2:1. Goodwill account appears in the books at ₹2,000. Pass journal entries.

5) A , B and C are partners sharing profits in the ratio of 5:3:2. Goodwill is appearing in the books at ₹50,000. D is admitted to the partnership, the new profit sharing ratio between A, B,C and D being 3:3:2:2. Pass the journal entries for Goodwill if the new partner D brings ₹1,00,000 for capital and cash for his share of goodwill. The goodwill of the firm is valued at ₹1,20,000 and it is not to appear in the books after D’s admission.

6) A and B are partners sharing profits in the ratio of 2:1. They admit C for 1/4th share in profits. C brings ₹30,000 for his capital and ₹8,000 out of his share of ₹10,000 for goodwill. Before admission goodwill appeared in books at ₹18,000. Pass journal entries.

7) E and F were partners in a firm sharing in the ratio of 3:1. They admitted G as a new partner on 1.3.2005 for 1/3rd share. It was decided that E, F and G will share future profits equally. G brought ₹50,000 in cash and machinery worth ₹70,000 for his share of profit as premium for goodwill. Pass necessary journal entries.

8) A and B are partners in a firm sharing profits in the ratio of 3:2. They admit C into partnership for 1/5th share. C brings ₹30,000 as capital and ₹10,000 as premium for goodwill. New profit sharing ratio of partners shall be 5:3:2. Pass necessary journal entries.

9) A and B are partners in a firm sharing profits in the ratio of 3:2. They admit C into partnership. C is paying a premium of ₹1,000 for 1/4th share of the profits. A, B and C decided to share the future in the ratio of 3:3:2. Pass journal entries.

10) A and B are partners in a firm sharing profits equally. They admit C into partnership. C pays only ₹1,000 for premium, out of his share of premium of ₹1,800 for 1/4th share of profit. Give necessary journal entries if the new profit sharing ratio is 7:5:4.

11) A and B are partners in a firm sharing profits in the ratio of 3:2. They admit C into partnership for 1/5th share in profits. C brought in ₹80,000 as his share of capital and ₹24,000 as premium. The new profit sharing ratio of A, B and C will be 5:3:2. Pass journal entries.

12) A and B are partners in a firm sharing profits in the ratio of 5:3. They admit C into partnership for 3/10th share in profits which he takes 2/10 from A and 1/10th from B, C brings in ₹3,000 as premium in cash out of his share of ₹7,800. Goodwill does not appear in the books of A and B. Pass journal entries.

13) A and B are partners in a firm with capitals of ₹26,000 and ₹22,000. They admit C as a partner for 1/4th share in profits of the firm. C brings ₹26,000 as his share of goodwill. Pass journal entries.

14) A and B are partners with capitals of ₹13,000 and ₹9,000 respectively. They admit C as partners with 1/5th share in the profit of the firm. C brings ₹8,000 as his capital. Pass journal entries.

15) A and B were partners with ₹ 1,00,000 capital each in affirm sharing profits equally. On1st January they admitted C as a new partner with 1 /4 share in profits and he brings ₹ 1,00,000 as his share of capital but unable to bring premium in cash. On the date of C’s admission the balance sheet of A and B showed a general reserve of ₹50,000 and a debit balance of ₹20,000 in the Profit and loss account. Pass necessary journal entries.

16) Vijay and Sanjay are partners in a firm sharing profits and losses in the ratio of 3:2. They decide to admit Ajay into partnership with 1/4 share in profits. Ajay brings in ₹ 30,000 for capital and the requisite amount of premium in cash. The goodwill of the firm is valued at ₹ 20,000. The new profit sharing ratio is 2:1:1. Vijay and Sanjay withdraw their share of goodwill. Give necessary journal entries.

17),Srikant and Raman are partners in a firm sharing profits and losses in the ratio of 3:2. They decide to admit Venkat into partnership with 1/3 share in the profits. Venkat brings in ₹ 30,000 as his capital. He also promises to bring in the necessary amount for his share of goodwill. On the date of admission, the goodwill has been valued at ₹24,000 and the goodwill account already appears in the books at ₹ 12,000. Venkat brings in the necessary amount for his share of goodwill and agrees that the existing goodwill account be written off. Record the necessary journal entries in the books of the firm

18) Ahuja and Barua are partners in a firm sharing profits and losses in the ratio of3:2. They decide to admit Chaudhary into partnership for 1/5 share of profits, which he acquires equally from Ahuja and Barua. Goodwill is valued at ₹ 30,000. Chaudhary brings in ₹ 16,000 as his capital but is not in a position to bring any amount for goodwill. No goodwill account exists in books of the firm. Goodwill account is to be raised at full value. Record the necessary journal entries.

19) Ram and Rahim are partners in a firm sharing profits and losses in the ratio of 3:2. Rahul is admitted into partnership for 1/3 share in profits. He brings in ₹ 10,000 as capital, but is not in a position to bring any amount for his share of goodwill which has been valued at ₹ 30,000. Give necessary journal entries under each of the following situations: (a) When there is no goodwill appearing in the books of the firm; (b) When the goodwill appears at ₹15,000 in the books of the firm; and (c) When the goodwill appears at ₹ 36,000 in the books of the firm.

20) A and B are partners sharing profits and losses equally. They admit C into partnership and the new ratio is fixed as 4:3:2. C is unable to bring anything for goodwill but brings ₹ 25,000 as capital. Goodwill of the firm is valued at ₹18,000. Give the necessary journal entries assuming that the partners do not want goodwill to appear in the Balance Sheet.

21) Hem and Nem are partners in a firm sharing profits in the ratio of 3:2. Their capitals were ₹ 80,000 and ₹ 50,000 respectively. They admitted Sam on Jan. 1, 2015 as a new partner for 1/5 share in the future profits. Sam brought ₹ 60,000 as his capital. Calculate the value of goodwill of the firm and record necessary journal entries on Sam’s admission.

22) X and Y are partners in a firm sharing profits and losses in 4:3 ratio. They admitted Z for 1/8 share. Z brought ₹ 20,000 for his capital and ₹ 7,000 for his 1/8 share of goodwill. Subsequently X, Y and Z decided to show goodwill in their books at ₹ 40,000. Show necessary journal entries in the books of X, Y and Z?

23) Aditya and Balan are partners sharing profits and losses in 3:2 ratio. They admitted Christopher for 1/4 share in the profits. The new profit sharing ratio agreed was 2:1:1. Christopher brought ₹ 50,000 for his capital. His share of goodwill was agreed to at ₹ 15,000. Christopher could bring only ₹ 10,000 out of his share of goodwill. Record necessary journal entries in the books of the firm?

24) Amar and Samar were partners in a firm sharing profits and losses in 3:1 ratio. They admitted Kanwar for 1/4 share of profits. Kanwar could not bring his share of goodwill premium in cash. The Goodwill of the firm was valued at ₹ 80,000 on Kanwar’s admission. Record necessary journal entry for goodwill on Kanwar’s admission.

25) Mohan Lal and Sohan Lal were partners in a firm sharing profits and losses in 3:2 ratio. They admitted Ram Lal for 1/4 share on 1.1.2010. It was agreed that goodwill of the firm will be valued at 3 years purchase of the average profits of last 4 years which were ₹ 50,000 for 2010, ₹ 60,000 for 2011, ₹ 90,000 for 2012 and ₹ 70,000 for 2013. Ram Lal did not bring his share of goodwill premium in cash. Record the necessary journal entries in the books of the firm on Ram Lal’s admission when: a) Goodwill already appears in the books at ₹ 2,02,500. b) Goodwill appears in the books at ₹ 2,500. c) Goodwill appears in the books at ₹ 2,05,000.

| CBSE Class 12 Accountancy Accounting for Not-for-Profit Organisation Worksheet |

| CBSE Class 12 Accountancy Accounting For Partnership Firms Worksheet Set A |

| CBSE Class 12 Accountancy Accounting For Partnership Firms Worksheet Set B |

| CBSE Class 12 Accountancy Admission Of Partner Worksheet Set A |

| CBSE Class 12 Accountancy Admission Of Partner Worksheet Set B |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set A |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set B |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set C |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set D |

| CBSE Class 12 Accountancy Dissolution Of Partnership Firm Worksheet Set A |

| CBSE Class 12 Accountancy Dissolution Of Partnership Firm Worksheet Set B |

| CBSE Class 12 Accountancy Share Capital Worksheet Set A |

| CBSE Class 12 Accountancy Share Capital Worksheet Set B |

| CBSE Class 12 Accountancy Debentures Worksheet |

| CBSE Class 12 Accountancy Financial Statements Of Company Worksheet |

| CBSE Class 12 Accountancy Financial Analysis And Tools For Financial Analysis Worksheet |

| CBSE Class 12 Accountancy Ratio Analysis Worksheet |

| CBSE Class 12 Accountancy Cash Flow Statement Worksheet Set A |

| CBSE Class 12 Accountancy Cash Flow Statement Worksheet Set B |

More Study Material

CBSE Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner Worksheet

We hope students liked the above worksheet for Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner designed as per the latest syllabus for Class 12 Accountancy released by CBSE. Students of Class 12 should download in Pdf format and practice the questions and solutions given in the above worksheet for Class 12 Accountancy on a daily basis. All the latest worksheets with answers have been developed for Accountancy by referring to the most important and regularly asked topics that the students should learn and practice to get better scores in their class tests and examinations. Studiestoday is the best portal for Class 12 students to get all the latest study material free of cost.

Worksheet for Accountancy CBSE Class 12 Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner

Expert teachers of studiestoday have referred to the NCERT book for Class 12 Accountancy to develop the Accountancy Class 12 worksheet. If you download the practice worksheet for one chapter daily, you will get higher and better marks in Class 12 exams this year as you will have stronger concepts. Daily questions practice of Accountancy worksheet and its study material will help students to have a stronger understanding of all concepts and also make them experts on all scoring topics. You can easily download and save all revision worksheet for Class 12 Accountancy also from www.studiestoday.com without paying anything in Pdf format. After solving the questions given in the worksheet which have been developed as per the latest course books also refer to the NCERT solutions for Class 12 Accountancy designed by our teachers

Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner worksheet Accountancy CBSE Class 12

All worksheets given above for Class 12 Accountancy have been made as per the latest syllabus and books issued for the current academic year. The students of Class 12 can be rest assured that the answers have been also provided by our teachers for all worksheet of Accountancy so that you are able to solve the questions and then compare your answers with the solutions provided by us. We have also provided a lot of MCQ questions for Class 12 Accountancy in the worksheet so that you can solve questions relating to all topics given in each chapter. All study material for Class 12 Accountancy students have been given on studiestoday.

Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner CBSE Class 12 Accountancy Worksheet

Regular worksheet practice helps to gain more practice in solving questions to obtain a more comprehensive understanding of Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner concepts. Worksheets play an important role in developing an understanding of Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner in CBSE Class 12. Students can download and save or print all the worksheets, printable assignments, and practice sheets of the above chapter in Class 12 Accountancy in Pdf format from studiestoday. You can print or read them online on your computer or mobile or any other device. After solving these you should also refer to Class 12 Accountancy MCQ Test for the same chapter.

Worksheet for CBSE Accountancy Class 12 Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner

CBSE Class 12 Accountancy best textbooks have been used for writing the problems given in the above worksheet. If you have tests coming up then you should revise all concepts relating to Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner and then take out a print of the above worksheet and attempt all problems. We have also provided a lot of other Worksheets for Class 12 Accountancy which you can use to further make yourself better in Accountancy

You can download the CBSE Printable worksheets for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner for latest session from StudiesToday.com

Yes, you can click on the links above and download Printable worksheets in PDFs for Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner Class 12 for Accountancy

Yes, the Printable worksheets issued for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner have been made available here for latest academic session

You can easily access the links above and download the Class 12 Printable worksheets Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner for each chapter

There is no charge for the Printable worksheets for Class 12 CBSE Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner you can download everything free

Regular revision of practice worksheets given on studiestoday for Class 12 subject Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner can help you to score better marks in exams

Yes, studiestoday.com provides all latest NCERT Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner Class 12 Accountancy test sheets with answers based on the latest books for the current academic session

Yes, studiestoday provides worksheets in Pdf for Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner Class 12 Accountancy in mobile-friendly format and can be accessed on smartphones and tablets.

Yes, worksheets for Part 1 Chapter 3 Reconstitution of a Partnership Firm Admission of a Partner Class 12 Accountancy are available in multiple languages, including English, Hindi