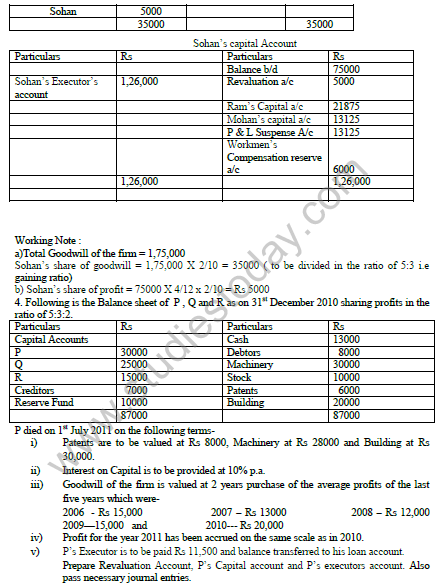

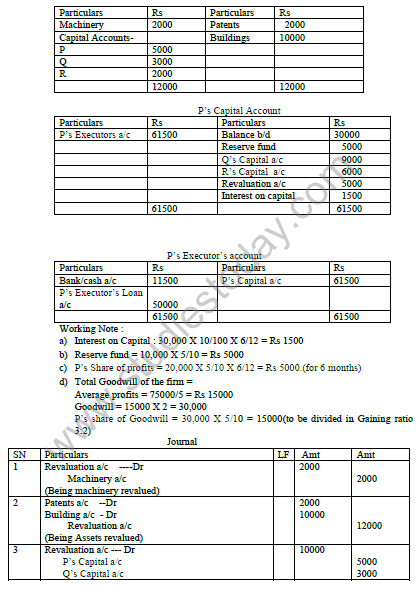

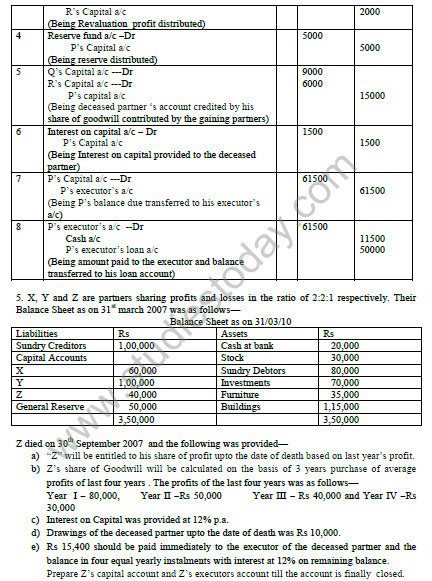

Please refer to CBSE Class 12 Accountancy HOTs Death Retirement Of A Partner. Download HOTS questions and answers for Class 12 Accountancy. Read CBSE Class 12 Accountancy HOTs for Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner below and download in pdf. High Order Thinking Skills questions come in exams for Accountancy in Class 12 and if prepared properly can help you to score more marks. You can refer to more chapter wise Class 12 Accountancy HOTS Questions with solutions and also get latest topic wise important study material as per NCERT book for Class 12 Accountancy and all other subjects for free on Studiestoday designed as per latest CBSE, NCERT and KVS syllabus and pattern for Class 12

Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner Class 12 Accountancy HOTS

Class 12 Accountancy students should refer to the following high order thinking skills questions with answers for Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner in Class 12. These HOTS questions with answers for Class 12 Accountancy will come in exams and help you to score good marks

HOTS Questions Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner Class 12 Accountancy with Answers

Retirement Of A partner

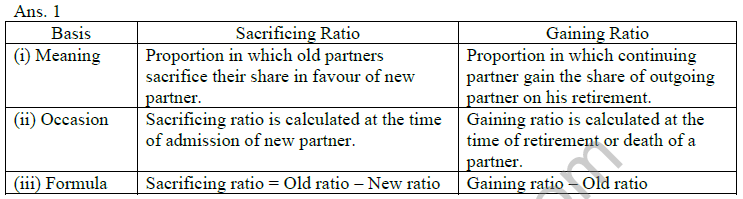

Q.1 Distinguish between Sacrificing Ratio and Gaining Ratio.

Q.2 Kamal, Kishore and Kunal are partners in a firm sharing profits equally. Kishore retires from the firm. Kamal and Kunal decide to share the profits in future in the ratio 4:3. Calculate the Gaining Ratio.

Ans. 2 Gaining Ratio = New ratio – Old ratio

Kamal‘s Gain = 4/7 – 1/3 = 5/21

Kunal‘s Gain = 3/7 – 1/3 = 2/21

Gaining Ratio = 5:2

Q.3 P, Q and R are partners sharing profits in the ratio of 7:2:1. P retires and the new profit sharing ratio between Q and R is 2:1. State the Gaining Ratio.

Ans. 3 Old ratio = P Q R

7 : 2 : 1

New ratio = Q R

2 : 1

Gaining Ratio = New ratio – Old ratio

Q‘s gain = 2/3 – 2/10 = 14/30

R‘s gain = 1/3 – 1/10 = 7/30

Gaining Ratio = 14:7 or 2:1

Q.4 A, B and C are partners in a firm sharing profits in the ration of 2:2:1. B retires and his share is acquired by A and C equally. Calculate new profit sharing ratio of A and C.

Ans. 4 A‘s gaining share = 2/5 X ½ = 1/5

A‘s new share = 2/5 + 1/5 = 3/5

C‘s gaining share = 2/5 X ½ = 1/5

C‘s New share = 1/5 + 1/5 = 2/5

New ratio of A and C = 3:2

Q.5 X, Y and Z are partners sharing profits in the ratio of 4/9, 1/3 and 2/9. X retires and surrenders 2/3rd of his share in favour of Y and remaining in favour of Z. Calculate new profit sharing ratio and gaining ratio.

Ans. 5

Y‘s gaining share = 4/9 X 2/3 = 8/27

Z‘s gaining share = 4/9 – 8/27 = 4/27

Y‘s new share = Old share + gain

= 1/3 + 8/27 = 17/27

Z‘s new share = 2/9 + 4/27 = 10/27

[

New Ratio = 17:10

Gaining ratio = 8/27 : 4/27 or 2:1

Q.6 X, Y and Z have been sharing profits and losses in the ratio of 3:2:1. Z retires. His share is taken over by X and Y in the ratio of 2:1. Calculate the new profit sharing ratio.

Ans. 6

Old Ratio = 3:2:1

Z Retire

X‘s Gaining = 1/6 X 2/3 = 2/18

X‘s New share = 3/6 + 2/18 = 11/18

Y‘s Gaining = 1/6 X 1/3 = 1/18

Y‘s new share = 2/6 + 1/18 = 7/18

New Ratio = 11/18, 7/18 Or 11:7

Q.7 P, Q and R were partners in a firm sharing profits in 4:5:6 ratio. On 28-02-2008 Q retired and his share of profits was taken over by P and R in 1:2 ratio. Calculate the new profit sharing ratio of P and R.

Ans. 7 Old ratio = P Q R

= 4 :5 :6

Q retired

P‘s gaining = 1/3 X 5/15 = 1/9

P‘s new share = 4/15 + 1/9 = 17/45

R‘s Gaining share = 2/3 X 5/15 = 2/9

R‘s new share = 6/15 + 2/9 = 28/45

New Ratio = 17:28

Q.8 Mayank, Harshit and Rohit were partners in a firm sharing profits in the ratio of 5:3:2. Harshit retired and goodwill is valued at Rs 60000. Mayank and Rohit decided to share future profits in the ratio 2:3. Pass necessary journal entry for treatment of goodwill.

Ans. 8 Rohit‘s capital A/C Dr. 24000

To Mayank‘s capital A/C 6000

To harshit‘s Capital A/C 18000

(Adjustment Entry for treatment of goodwill in gaining ratio.)

Q.9 Ramesh, Naresh and Suresh were partners in a firm sharing profits in the ratio of 5:3:2. Naresh retired and the new profit sharing ratio between Ramesh and Suresh was 2:3. On Naresh retirement the goodwill of the firm was valued at Rs. 120000. Pass necessary journal entry for the treat.

Ans. 9 Suresh capital A/C Dr. 48000

To Ramesh‘s capital A/C 12000

To Naresh capital A/C 36000

(Goodwill adjusted among the gaining partner in gaining ratio.)

Q.10 L, M and O were partners in a firm sharing profits in the ratio of 1:3:2. L retired and the new profit sharing ratio between M and O was 1:2. On L‘s retirement the goodwill of the firm was valued Rs. 120000. Pass necessary journal entry for the treatment of goodwill.

Ans. 10 O‘s capital A/C Dr. 40000

To C‘s capital A/C 20000

To M‘s capital A/C 20000

(Adjustment of goodwill in gaining partners in their gaining ratio.)

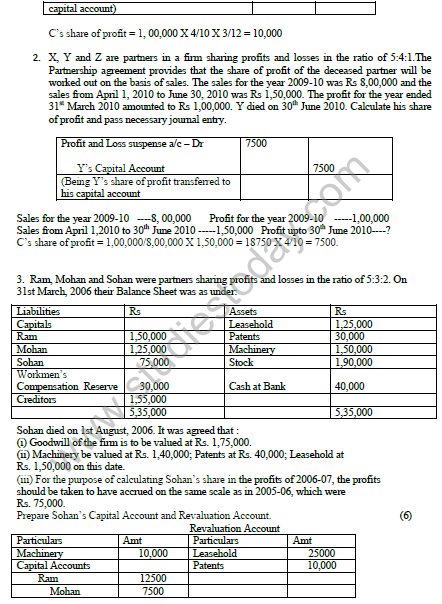

Q.11 State the journal entry for treatment of deceased partners share of profit for his life period in the year of death.

Ans. 11 Profit and loss suspense A/C Dr

To deceased partner‘s capital A/C

Q.12 X, Y and Z were partners in a firm sharing profits and losses in the ratio of 3:2:1. The profit of the firm for the year ended 31st March, 2007 was Rs. 3,00000. Y dies on 1st July 2007. Calculate Y‘s share of profit up to date of death assuming that profits in the year 2007- 2008 have been accured on the same scale as in the year 2006-07 and pass necessary journal entry.

Ans. 12 Total profit for the year ended 31st March 2007 = Rs 300000

Y‘s share of profit up to date of death = 300000 X 2/6 X 3/12

= 25000

Profit and Loss suspense A/C Dr. 25000

To Y‘s capital A/C 25000

( Y‘s share of profit transferred to Y‘s capital A/C)

Q.13 A, B and C were partners in a firm sharing profits in 3:2:1 ratio. The firm closes its books on 31st March every year. B died on 12-06-2007. On B‘s death the goodwill of the firm was valued at Rs. 60000. On B‘s death his share in the profit of the firm till the time of his death was to be calculated on the basis of previous years which was Rs.150000. Calculate B‘s share in the profit of the firm. Pass necessary journal entries for the treatment of goodwill and B‘s share of profit at the time of his death.

Ans. 13 Profit and Loss suspense A/C Dr. 10000

To B‘s capital A/C 10000

(B‘s share of profit transferred to B‘s capital A/C)

A‘s capital A/C Dr. 15000

C‘s capital A/C Dr. 5000

To B‘s capital A/C 20000

(B‘s share of goodwill transferred to B‘s capital A/C and debited to remaining partners capital A/C in their gaining ratio.)

B‘s share of profit = Number of days from 1 April to 12th June 2007

= 73 Days

B‘s share of profit = 150000 X 1/3 X 73/365

= 10000

Q.14 A, B and C were partners in a firm sharing profits in the ratio of 2:2:1. C dies on 31st July, 2007. Sales during the previous year upto 31st march, 2007 were Rs. 6,00,000 and profits were Rs. 150000. Sales for the current year upto 31st July were Rs. 250000. Calculate C‘s share of profits upto the date of his death and pass necessary journal entry.

LEARNING OBJECTIVES:

After studying this lesson, we are confident; you should be competent enough to:

• Identify adjustments arising due to retirement of a partner.

•Calculate new and gaining ratio.

• Make accounting treatment of goodwill in different cases.

• Make accounting treatment of the revaluation of assets and liabilities and distribution of profit or loss on revaluation among partners.

•Make accounting treatment of undistributed profit or loss.

• Determine the amount payable to retiring partner and make payment as per agreement and provisions of law.

• Make adjustment of partners‘ capital account

Salient Points:-

1. An existing partner may wish to withdraw from a firm for various reasons.

2. The amount due to a retiring partner will be the total of :-

a. his capital in the firm

b. His share in firm‘s accumulated profits and losses.

c. His share of profit or loss on revaluation of assets and liabilities

d. ;his share of profits till the date of retirement

e. His remuneration and interest on capital.

f. His share in firm‘s goodwill.

3. The ratio in which the continuing (remaining) partners have acquired the share from the outgoing partner is called gaining ratio.

4. Share of goodwill of outgoing partner will be debited to gaining partners in their gaining ratio.

5. At the retirement of a partner Profit & Loss on Revaluation of Assets and liabilities and balances of accumulated Profits and losses will be distributed among all partners (including outgoing partner) in their old ratio.

6. The outstanding balance of outgoing partner‘s capital A/C may be settled by fully or partly payment and (or) transferring into his loan account.

Q.1 What is meant by retirement of a partner?

Ans. Retirement of a partner is one of the modes of reconstituting the firm in which old partnership comes to an end and a new partner among the continuing (remaining) partners (i.e., partners other than the outgoing partner) comes into existence.

Q.2 ‗How can a partner retire from the firm?

Ans. A partner may retire from the firm;

i) In accordance with the terms of agreement; or

ii) With the consent of all other partners; or

iii) Where the partnership is at will, by giving a notice in writing to all the partners of his intention to retire.

Q.3 What do you understand by ‗Gaining Ratio?

Ans. Gaining Ratio means the ratio by which the share in profit stands increased. It is computed by deducting old ratio from the new ratio.

Q.4 What do you understand by ‗Gaining Partner‘?

Ans Gaining Partner is a partner whose share in profit stands increased as a result of change in partnership.

Q.5 Give two circumstances in which gaining ratio is computed.

Ans. Gaining Ratio is computed in the following circumstances: (i) When a partner retires or dies. (ii) When there is a change in profit-sharing ratio.

Q.6 Why is it necessary to revalue assets and reassess liabilities at the time of retirement of a partner?

Ans. At the time of retirement or death of a partner, assets are revalued and liabilities are reassessed so that the profit or loss arising on account of such revaluation up to the date of retirement or death of a partner may be ascertained and adjusted in all partners‘ capital accounts in their old profit-sharing ratio.

Q.7 Why is it necessary to distribute Reserves Accumulated, Profits and Losses at the time of retirement or death of a partner?

Ans. Reserves, accumulated profits and losses existing in the books of account as on the date of retirement or death are transferred to the Capital Accounts (or Current Accounts) of all the partners (including outgoing or deceased partner) in their old profit-sharing ratio so that the due share of an outgoing partner in reserves, accumulated profits/losses gets adjusted in his Capital or Current Account.

Q.8 What are the adjustments required on the retirement or death of a partner?

Ans. At the time of the retirement or death of a partner, adjustments are made for the following:

(i) Adjustment in regard to goodwill.

(ii) Adjustment in regard to revaluation of assets and reassessment of liabilities.

(iii) Adjustment in regard to undistributed profits.

(iv) Adjustment in regard to the Joint Life Policy and individual policies.

Q.9 X wants to retire from the firm. The profit on revaluation of assets on the date of retirement is Rs. 10,000. X is of the view that it be distributed among all the partners in their profit-sharing ratio whereas Y and Z are of the view that this profit be divided between Y and Z in new profit-sharing ratio. Who is correct in this case?

Ans. X is correct because according to the Partnership Act a retiring partner is entitled to share the profit up to the date of his retirement. Since the profit on revaluation arises before a partner retires, he is entitled to the profit.

Q.10 How is goodwill adjusted in the books of a firm -when a partner retires from partnership?

Ans. When a partner retires (or dies), his share of profit is taken over by the remaining partners. The remaining partners then compensate the retiring or deceased partner in the form of goodwill in their gaining ratio. The following entry is recorded for this purpose:

Remaining Partners‘ Capital A/cs ...Dr.

[Gaining Ratio]

To Retiring/Deceased Partner‘s Capital A/c [With his share of goodwill]

If goodwill (or Premium) account already appears in the old Balance Sheet, it should be written off by recording the following entry:

All Partners‘ Capital/Current A/cs ...Dr. [Old Ratio]

To Goodwill (or Premium) A/c

Q.13 State the ratio in which profit or loss on revaluation will be shared by the partners when a partner retires. ;

Ans. Profit or loss on revaluation of assets/liabilities will be shared by the partners (including the retiring partner) hi their old profit-sharing ratio.

Q.14 How is the account of retiring partner settled?

Ans. The retiring partner account is settled either by making payment in cash or by promising the retiring partner to pay in installments along with interest or by making payment partly in call and partly transferring to his loan account. The -following Journal entry is passed:

Retiring Partner‘s Capital A/c ...Dr.

To Cash* [If paid in cash] Or

To Retiring Partner‘s Loan [If transferred to loan]

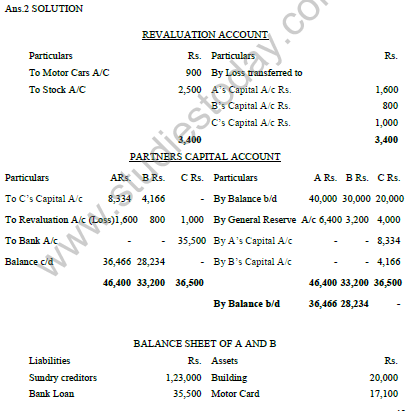

The partners share profits in the ratio of 8 : 4 : 5. C retires from the firm on the same date subject to the following term S and conditions:

i) 20% of the General Reserve is to remain‘ as a reserve for bad and doubtful debts.

ii) Motor)r Car is to be decreased by 5%.

iii) Stock is to be revalued at Rs.17, 500.

iv) Goodwill is valued at‘ 2 ½ years purchase of the average profits of last 3 years.

Profits were; 2001: Rs.11,000; 200l: Rs. 16,000 and 2003: Rs.24,000.

C. was paid in July A and B borrowed the necessary amount from the Bank on the security of Motor Car and stock to payoff C.

Prepare Revaluation Account, Capital Accounts and Balance Sheet of A and B.

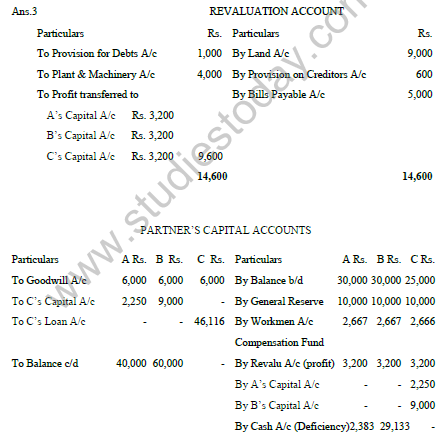

it was mutuallyagreed that C will retire from partnership and for this purpose following terms were agreed upon.

i) Goodwill to be valued on 3 years‘ purchase of average profit of last 4 years which were 2004 : Rs.50,000 (loss); 2005 : Rs. 21,000; 2006: Rs.52,000; 2007 : Rs.22,000.

ii) The Provision for Doubtful Debt was raised to Rs. 4,000.

iii) To appreciate Land by 15%.

iv) To decrease Plant and Machinery by 10%.

v) Create provision of Rs;600 on Creditors.

vi) A sum of Rs.5,000 of Bills Payable was not likely to be claimed.

vii) The continuing partners decided to show the firm‘s capital at 1,00,000 which would be in their new profit sharing ratio which is 2:3. Adjustments to be made in cash

Make necessary accounts and prepare the Balance Sheet of the new partners.

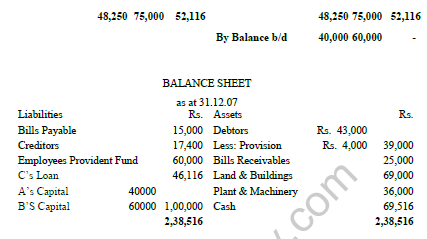

1. Thomas, Biju and Sunil were partners sharing profits in the ratio of 3:2:1 with a capital balance of Rs. 1,00,000, Rs. 75,000 and Rs. 50,000. They had a joint life policy for Rs. 3,00,000. On 15.10.06 Sunil died. The company admitted for a claim of Rs. 3,60,000 on his death. The firms profit and loss had a debit balance of Rs. 60,000.

Ascertain: (a) The amount due to Sunil

(b) Pass journal entries regarding the distribution of joint life policy.

(c) Prepare capital accounts.

Soln: (a) Amount due to Sunil = Rs. 1,00,000 (See

point C)

(b) Journal entry

Joint Life Policy a/c Dr. 3,60,000

To Thomas capital a/c 1,80,000

To Biju capital a/c 1,20,000

To Sunil capital a/c 60,000

2. Aby, Suby and Minu are partners sharing profits

in the ratio of 5:3:2. Minu retired on 31.09.06. The

capital account balance and share of reserve due

to Minu together amounted to Rs. 1,80,000. But

Aby and Suby agreed to pay him Rs. 2,40,000. The

new profit sharing ratio of Aby and Suby have been

fixed at 3:2.

(i) Why has Minu been paid over and above the

actual amount due to him?

(ii) Give a journal entry to record this through capi-

tal a/c adjustments.

Soln: (i) Extra amount paid to Minu = 240000 180000 = 60,000

That amount is treated as the share of goodwill to Min

(ii) Journal entry

Abys capital a/c Dr. 30,000

Subys capital a/c Dr. 30,000

To Minus capital a/c 60,000

(Share of goodwill transferred in gaining ratio)

(ii) Calculation of Gaining ratio

Gaining ratio = New ratio Old ratio

New ratio of Aby & Suby = 3 : 2 ie 3 / 5 & 2 / 5

Old ratio of Aby, Suby & Minu = 5 : 3 : 2

ie 5 / 10 , 3 / 10 & 2 / 10

Gaining ratio of Aby = 3 / 5 - 5 / 10 = 6 - 5 / 10 = 1 / 10

Gaining ratio of Suby = 2 / 5 - 3 / 10 = 4-3 / 10 = 1 / 10

Gaining ratio = 1 : 1 ie 1 / 2: 1 / 2

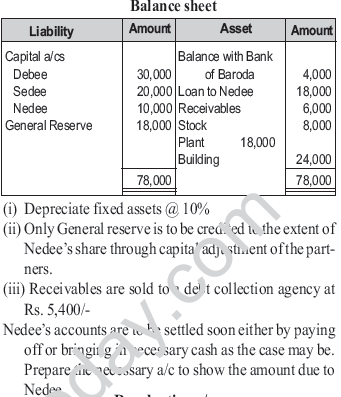

3. Debee, Sedee and Nedee are in partnership, who were sharing profits in the ratio of 3 : 2:1. On 31.03.05, Nedee left the firm as per agreement. The following details are available.

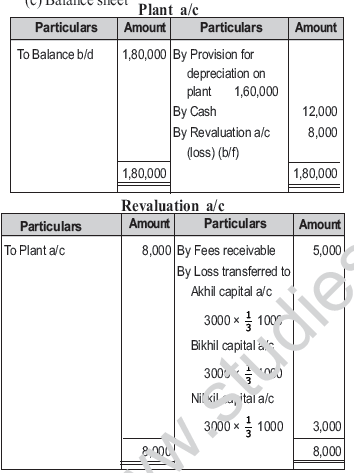

On the above date Nikkil retired.

(a) The entire plant was sold for Rs. 12,000

(b) Nikkils share of goodwill was valued at Rs. 3,000

(c) General reserve to be adjusted to the extend of Nikkils share through a capital adjustment entry.

(d) Fee receivable has to be taken into a/c Rs. 5,000 which has not been brought into the books so far

Prepare: (a) Revaluation account (b) Capital accounts (c) Balance sheet

1) Adjusting entry for goodwill

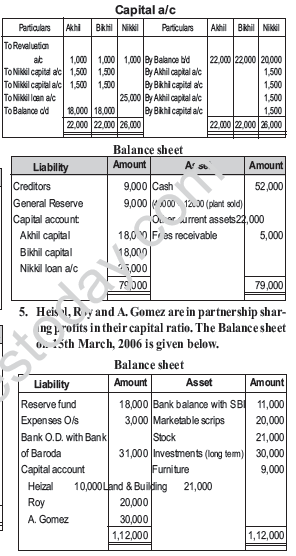

Akhil capital a/c 3000 × 1 / 2 1,500

Bikhil capital a/c 3000 × 1 / 2 1,500

To Nikkil capital a/c 3,000

(ii) Adjusting entry for General Reserve

Akhils capital a/c 3000 × 1 / 2 1,500

Bikhils capital a/c 3000 × 1 / 2 1,500

Nikkils capital a/c 9000 x 1 / 3 3,000

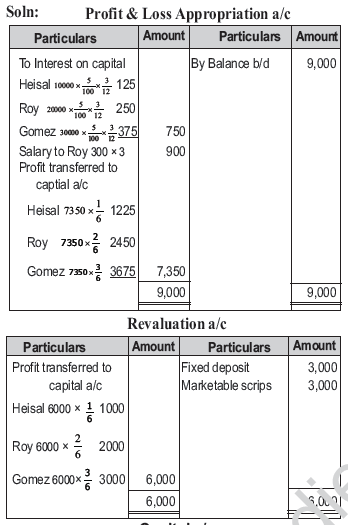

Further information on retirement of Roy on 15th June,

2006

Profit for 3 months - Rs. 9,000

Drawings: Heisal - Rs. 1,000

Roy - Rs. 2,000

A. Gomez - Rs. 3,000

Interest on capital @ 5% p.a

Salary to Roy Rs. 300 p.m.

The firm had a fixed deposit worth Rs. 3,000 which

has not accounted so far, has to be brought into the

books. Marketable scrips were valued at Rs. 23,000.

Prepare: (a) Profit and loss appropriation a/c

(b) Capital a/c (c) Balance sheet

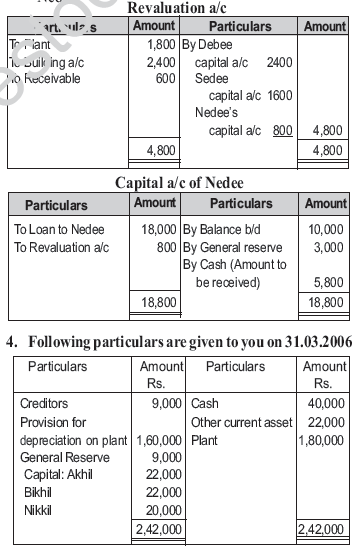

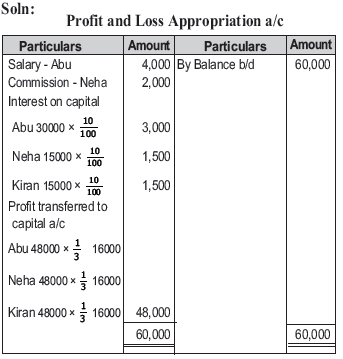

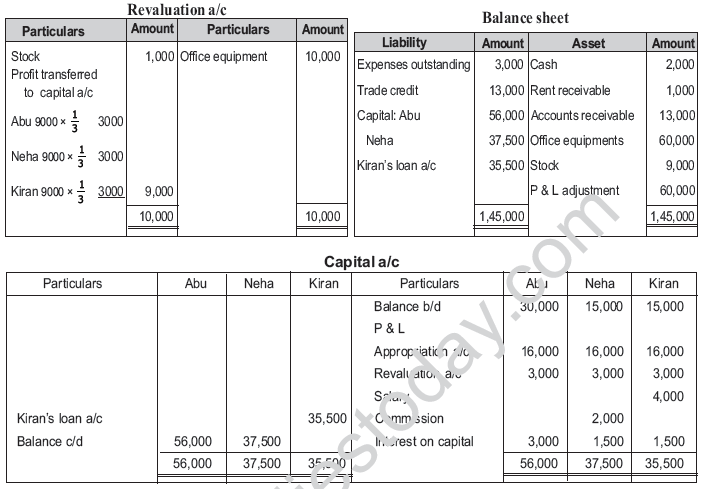

6. Abu, Neha and Kiran are equal partners. The led-

ger accounts as on 31.03.2006 shows the follow-

ing balances.

Expenses outstanding Rs. 3,000

Trade credit Rs. 13,000

Cash Rs. 2,000

Rent receivable Rs. 1,000

Accounts receivable Rs. 13,000

Capital

Abu - Rs. 30,000

Neha - Rs. 15,000

Kiran - Rs. 15,000

Office equipments Rs. 50,000

Stock Rs. 10,000

During the year the firm made a net profit of

Rs. 60,000 out of which the following distributions

are to be made.

Salary to Abu Rs. 4,000

Commission to Neha Rs. 2,000

Interest on capital @10% each

Kiran retired from the firm on 31.03.2006. Office

equipments are revalued at Rs. 60,000 and stock

Rs. 9,000.

Prepare:

(a) Profit and Loss appropriation a/c

(b) Revaluation a/c (c) Capital accounts

(d) Balance sheet

| CBSE Class 12 Accountancy HOTs Accounting for Debentures |

| CBSE Class 12 Accountancy HOTs Partnership Basic Concepts |

| CBSE Class 12 Accountancy HOTs Admission Of A Partner |

| CBSE Class 12 Accountancy HOTs Death Retirement Of A Partner |

| CBSE Class 12 Accountancy HOTs Dissolution of A partnership firm |

| CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation |

| CBSE Class 12 Accountancy HOTs Accounting For Share Capital |

| CBSE Class 12 Accountancy HOTs Issue And Redemption of Debentures |

| CBSE Class 12 Accountancy HOTs Financial Statements of a Company |

| CBSE Class 12 Accountancy HOTs Analysis of Financial Statement |

| CBSE Class 12 Accountancy HOTs Accounting Ratios |

| CBSE Class 12 Accountancy HOTs Cash Flow Statement |

More Study Material

CBSE Class 12 Accountancy Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner HOTS

We hope students liked the above HOTS for Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner designed as per the latest syllabus for Class 12 Accountancy released by CBSE. Students of Class 12 should download the High Order Thinking Skills Questions and Answers in Pdf format and practice the questions and solutions given in above Class 12 Accountancy HOTS Questions on daily basis. All latest HOTS with answers have been developed for Accountancy by referring to the most important and regularly asked topics that the students should learn and practice to get better score in school tests and examinations. Studiestoday is the best portal for Class 12 students to get all latest study material free of cost.

HOTS for Accountancy CBSE Class 12 Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner

Expert teachers of studiestoday have referred to NCERT book for Class 12 Accountancy to develop the Accountancy Class 12 HOTS. If you download HOTS with answers for the above chapter daily, you will get higher and better marks in Class 12 test and exams in the current year as you will be able to have stronger understanding of all concepts. Daily High Order Thinking Skills questions practice of Accountancy and its study material will help students to have stronger understanding of all concepts and also make them expert on all critical topics. You can easily download and save all HOTS for Class 12 Accountancy also from www.studiestoday.com without paying anything in Pdf format. After solving the questions given in the HOTS which have been developed as per latest course books also refer to the NCERT solutions for Class 12 Accountancy designed by our teachers

Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner HOTS Accountancy CBSE Class 12

All HOTS given above for Class 12 Accountancy have been made as per the latest syllabus and books issued for the current academic year. The students of Class 12 can refer to the answers which have been also provided by our teachers for all HOTS of Accountancy so that you are able to solve the questions and then compare your answers with the solutions provided by us. We have also provided lot of MCQ questions for Class 12 Accountancy in the HOTS so that you can solve questions relating to all topics given in each chapter. All study material for Class 12 Accountancy students have been given on studiestoday.

Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner CBSE Class 12 HOTS Accountancy

Regular HOTS practice helps to gain more practice in solving questions to obtain a more comprehensive understanding of Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner concepts. HOTS play an important role in developing an understanding of Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner in CBSE Class 12. Students can download and save or print all the HOTS, printable assignments, and practice sheets of the above chapter in Class 12 Accountancy in Pdf format from studiestoday. You can print or read them online on your computer or mobile or any other device. After solving these you should also refer to Class 12 Accountancy MCQ Test for the same chapter

CBSE HOTS Accountancy Class 12 Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner

CBSE Class 12 Accountancy best textbooks have been used for writing the problems given in the above HOTS. If you have tests coming up then you should revise all concepts relating to Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner and then take out print of the above HOTS and attempt all problems. We have also provided a lot of other HOTS for Class 12 Accountancy which you can use to further make yourself better in Accountancy.

You can download the CBSE HOTS for Class 12 Accountancy Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner for latest session from StudiesToday.com

Yes, you can click on the link above and download topic wise HOTS Questions Pdfs for Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner Class 12 for Accountancy

Yes, the HOTS issued by CBSE for Class 12 Accountancy Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner have been made available here for latest academic session

You can easily access the link above and download the Class 12 HOTS Accountancy Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner for each topic

There is no charge for the HOTS and their answers for Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner Class 12 CBSE Accountancy you can download everything free

HOTS stands for "Higher Order Thinking Skills" in Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner Class 12 Accountancy. It refers to questions that require critical thinking, analysis, and application of knowledge

Regular revision of HOTS given on studiestoday for Class 12 subject Accountancy Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner can help you to score better marks in exams

Yes, HOTS questions are important for Part 1 Chapter 4 Reconstitution of a Partnership Firm Retirement/Death of a Partner Class 12 Accountancy exams as it helps to assess your ability to think critically, apply concepts, and display understanding of the subject.