Read TS Grewal Accountancy Class 11 Solution Chapter 14 Depreciation 2023 2024. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers of Grade 11. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in standard 11 Accounts class tests and examinations.

Class 11 Accounts Chapter 14 Depreciation TS Grewal Solutions

TS Grewal Solutions for Chapter 14 Depreciation Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2023 2024 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11. Class 11 Grewal solutions should be revised regularly as more practice will help you get a better rank and easily solve more questions.

Chapter 14 Depreciation TS Grewal Class 11 Solutions

Question.1. What is Depreciation? What is the need for need for providing Depreciation? Describe the two methods of providing Depreciation.

Answer 1.

Meaning of Depreciation: Depreciation is the fall in the value of tangible fixed asset because of its usage or with efflux of time or due to obsolescence or accident.

Need or Objectives for providing Depreciation:-

The following are the need or objectives for providing depreciation:

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

(iii) Provision for funds out of profits for replacement: Funds should be retained, out of Profits, for replacement of assets at the end of life of the asset. The amount of depreciation is debited to Profit and Loss Account, on account of depreciation are retained in the business as no payment is made like other expenses.

(iv) To ascertain the correct cost of production: Depreciation should be taken into consideration for calculating the cost of production.

Two Methods of Depreciation:-

The amount of depreciation to be charged for the year is calculated by using various methods. But the two main methods for calculating depreciation are:

1. Fixed Percentage on Original Cost or Fixed Installment or Straight Line Method.

2. Fixed Percentage on Diminishing Balance or Reducing Installment Method or Written Down Value Method.

Question.2. What are the two methods for providing Depreciation? Give the merits and demerits of each method.

Answer 2.

Two Methods of Depreciation:-

The amount of depreciation to be charged for the year is calculated by using various methods. But the two main methods for calculating depreciation are:

1. Fixed Percentage on Original Cost or Fixed Installment or Straight Line Method.

2. Fixed Percentage on Diminishing Balance or Reducing Installment Method or Written Down Value Method.

Advantages of the Straight Line Method are:-

1. It is a simple method of calculating the depreciation.

2. In this method, assets can be depreciated up to the estimated scrap value or zero value.

3. It is easy to calculate the amount of depreciation under this method.

4. The Profit and Loss Account is debited or charged with same amount of depreciation every year and uniformity is maintained on the expenditure.

Disadvantages of the Straight Line Method are:

1. There is no arrangement of interest on capital invested in assets in this method.

2. With the passage of time, work efficiency of assets decreases and repair expenses increases. As a result, in later years, there is more load on the Profit and Loss Account due to increased repair expenses.

3. Sometimes in this method, the book value of assets becomes nil, still the assets are used in the business.

Advantages of the Written Down Value Method:

The following are the advantages of the Written Down Value Method:

1. There is same weightage on Profit and Loss Account of depreciation and repair expenses.

2. This method is easier than Straight Line Method.

3. In case of expansion and increase in assets, the depreciation can be computed easily by this method.

4. This method is acceptable by the Government under the Income Tax Act.

Disadvantages of the Written Down Value Method:

The following are the disadvantages of the Written Down Value Method:

1. In this method the value of the asset can never be zero.

2. It is a difficult task to ascertain the proper rate of depreciation.

3. There is no provision of interest on capital invested in use of assets.

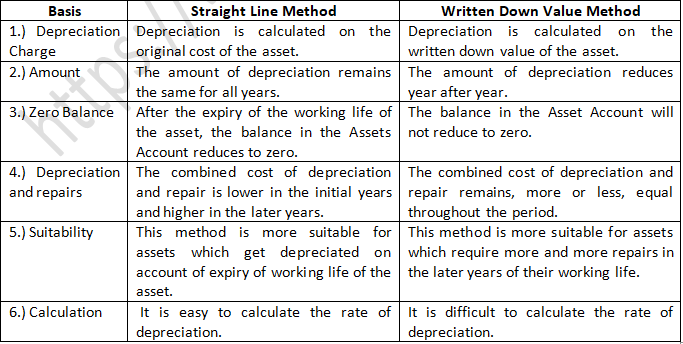

Question.3. Distinguish between the Straight Line Method and Written Down Value Method of Providing Depreciation.

Answer 3.

Distinction between Straight Line Method and Written Down Value Method of providing Depreciation:-

Question.4. State briefly the necessity of providing Depreciation.

Answer 4.

The necessity of providing Depreciation:

The following are the necessity of providing depreciation:

(i) To find out the correct profit or loss: the profit for any year can be determined only when all cost of earning revenues have been accounted for. Decrease in the value of fixed assets or depreciation shows the cost of earning revenue by use of fixed assets in the accounting year. Depreciation is not optional but compulsory to determine correct profit or loss.

(ii) To show true and fair view of the financial position: Depreciation, if not charged, would result in assets being stated at a higher value. As a result of this, the Position Statement or Balance Sheet would not present a true and fair view of the financial position.

(iii) Provision for funds out of profits for replacement: Funds should be retained, out of Profits, for replacement of assets at the end of life of the asset. The amount of depreciation is debited to Profit and Loss Account, on account of depreciation are retained in the business as no payment is made like other expenses.

(iv) To ascertain the correct cost of production: Depreciation should be taken into consideration for calculating the cost of production. If it is not considered the cost of production will not be correct.

(v) To meet the legal requirements: It is mandatory to charge Depreciation to comply with the provisions of the Companies Act and the Income Tax Act.

Question.5. Explain the following briefly:

(i) Assets Disposal Account

(ii) Written Down Value Method of Providing Depreciation

Answer 5.

(i) Asset Disposal Account: In case of asset being sold. a new account named ‘Asset Disposal Account’ is opened in the ledger for the purpose of calculating profit or loss on the sale of an asset. Journal entries for sale or disposal of asset will depend upon the method of recording depreciation.

(ii) Written Down Value/Diminishing Balance/Reducing Balance Method of Charging Depreciation: Under this method, depreciation is charged at a fixed rate on the reducing balance or cost less depreciation every year. A fixed rate on the written down value of the asset is charged as depreciation every year the expected useful life of the asset. A fixed depreciation percentage is applied to the book value and not to the cost of the asset.

For example the cost of the asset is 1,00,000 and the percentage of depreciation to be written off each year is 10%. In the first year, the amount of depreciation will be 10.000; this will reduce the book value to 90.000, Second year, the depreciation amount will be 9,000, that is of 90,000. Thus, every year the depreciation amount will go on reducing.

Question.6. Ram & Co. purchased machinery for Rs. 21,000 on 1st April, 2021. The estimated life of the machinery is 10 years, after which its residual value will be Rs. 1,000 only. Find the amount of Annual Depreciation according to the Fixed Installment Method. Ignore GST.

Answer 6.

Amount on Annual Depreciation under Fixed Installment Method:-

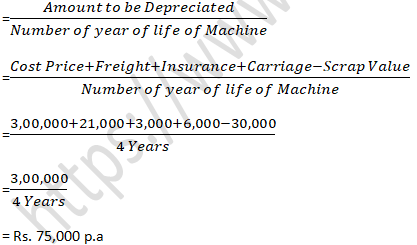

Question.7. On 1st April, 2017, Grand Ltd. Purchased a machinery for Rs. 3,00,000 and incurred Rs. 21,000 towards freight and insurance, Rs. 3,000 towards carriage inward and Rs. 6,000 towards installation charges. It has estimated that the machinery will have a scrap value of Rs. 30,000 at the end of the useful life which is four years. What will be the annual depreciation and the value of machinery after four years according to the Straight Line Method? Ignore GST.

Answer 7.

Amount on Annual Depreciation under Straight Line Method:-

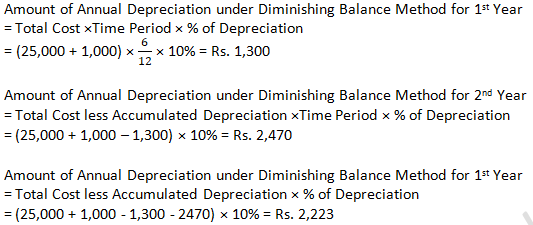

Question.8. Good Manufactures Ltd. Purchase on 1st October, 2018 a machinery costing Rs. 25,000. A sum of Rs. 1,000 was spent upon its installation. Depreciation is charged @ 10% p.a. on the Diminishing Balance Method. The company closes its books every year on 31st March (ignore GST).

What will be the amount of Depreciation for the year ended 31st March 2019, 31st March 2020 and 31st March, 2021?

Answer 8.

Class 11 Accounts Ch 14 Practical Problems TS Grewal

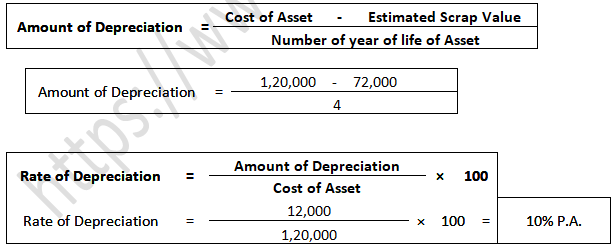

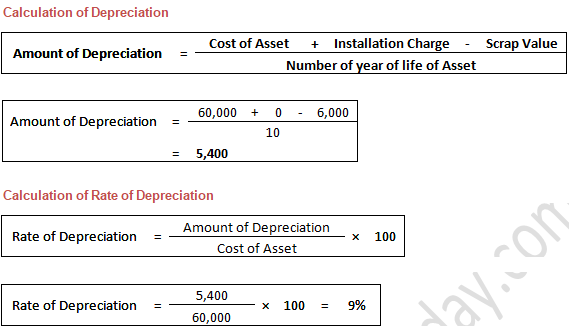

Question 1: Calculate the Amount of annual Depreciation and Rate of Depreciation under Straight Line Method (SLM) from the following:

Purchased a second-hand machine for Rs 96,000, spent Rs 24,000 on its cartage, repairs and installation, estimated useful life of machine 4 years. Estimated residual value Rs 72,000.

Answer 1:

Calculation of Rate of Depreciation by Straight line Method

Point of Knowledge:-

Cost of Assets = Purchases Price of Machine + Repairs and installation Charge.

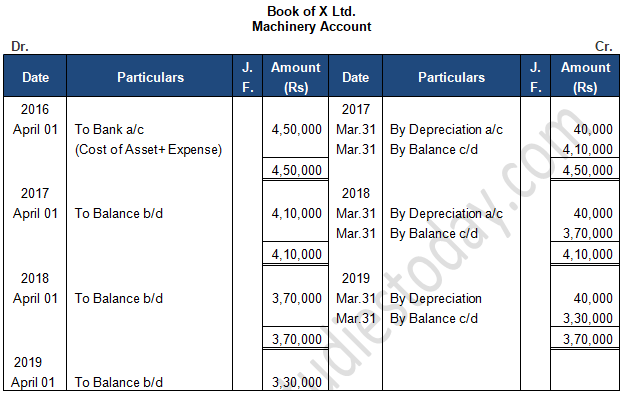

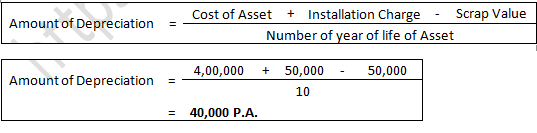

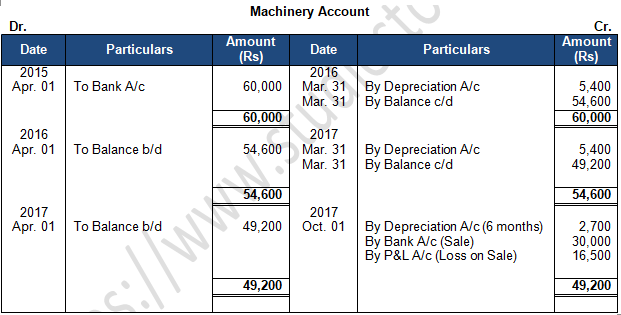

Question 2: On 1st April, 2016, X Ltd. purchased a machine costing Rs 4, 00,000 and spent Rs 50,000 on its installation. The estimated life of the machinery is 10 years, after which its residual value will be Rs 50,000 only. Find the amount of annual depreciation according to the Fixed Installment Method and prepare Machinery Account for the first three years. The books are closed on 31st March every year.

Answer 2:

Point of Knowledge:-

Cost of Assets = Purchases Price of Machine + Repairs and installation Charge

= 4, 00,000+50,000

= 4, 50,000

Working Note:-

Calculation of Depreciation:-

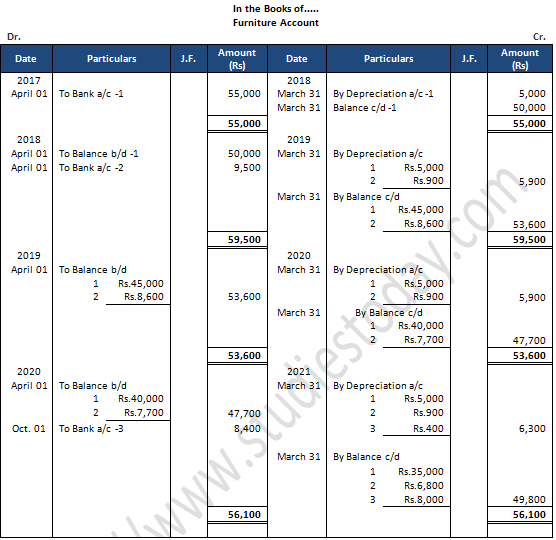

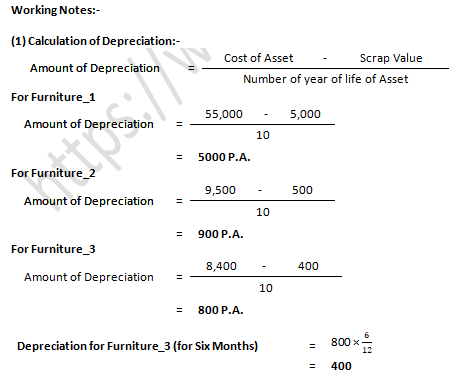

Question 3: On 1st April, 2017, Furniture costing Rs. 55,000 was purchased. It is estimated that its life is 10 years at the end of which it will be sold for Rs. 5,000. Additions are made on 1st April 2018 and 1st October, 2020 to the value of Rs. 9,500 and Rs. 8,400 (Residual values Rs. 500 and Rs. 400 respectively). Show the Furniture Account for the first four years, if Depreciation is written off according to the Straight Line Method.

Answer 3:

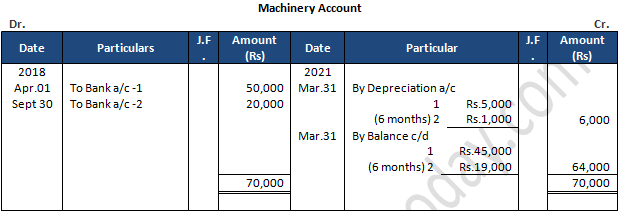

Question 4: From the following transactions of a concern, prepare the Machinery Account for the year ended 31st March, 2021:

1st April, 2020 : Purchased a second-hand machinery for Rs. 40,000

1st April, 2020 : Spent Rs. 10,000 on repairs for making it serviceable.

30th September, 2020 : Purchased additional new machinery for Rs. 20,000.

31st December, 2020 : Repairs and renewals of machinery Rs. 3,000.

31st March, 2021 : Depreciate the machinery at 10% p.a.

Answer 4:

Point of Knowledge:-

- If the Repair & Renewal Charge made on same day, when the machinery was purchases then it should be added in the cost of machinery. But after purchasing date, expenses on machinery should not be recorded in the Machinery Account.

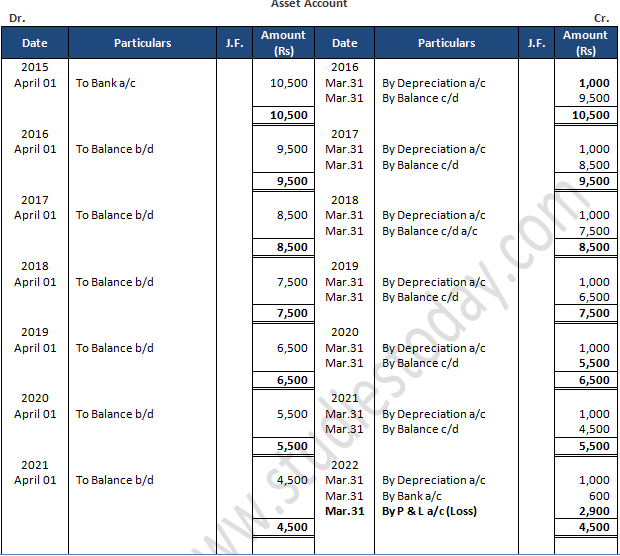

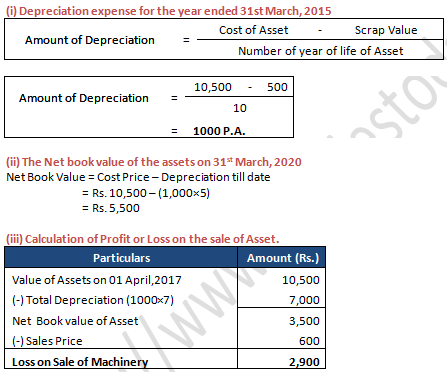

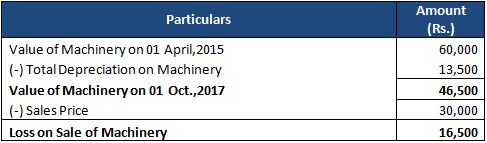

Question 5: An asset was purchased for Rs 10,500 on 1st April, 2014. The scrap value was estimated to be Rs. 500 at the end of asset's 10 years' life. Straight Line Method of depreciation was used. The accounting year ends on 31st March every year. The asset was sold for Rs. 600 on 31st March, 2021. Calculate the following.

(i) The Depreciation expense for the year ended 31st March, 2015.

(ii) The net book value of the asset on 31st March, 2019.

(iii) The grain or loss on sale of the asset on 31st March, 2021.

Answer 5:

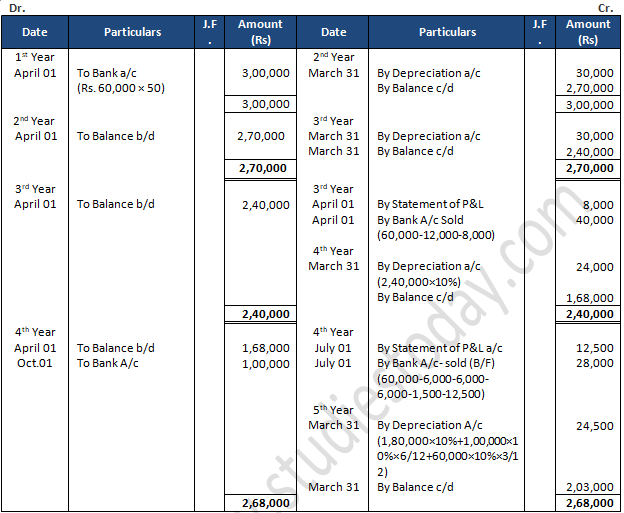

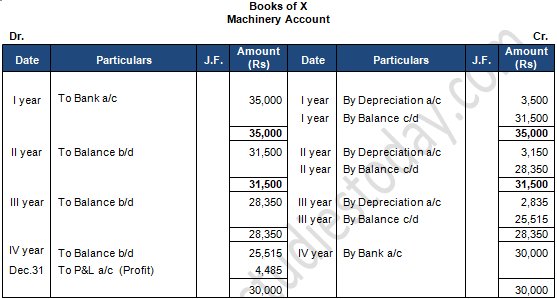

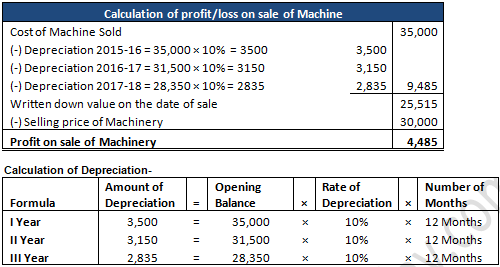

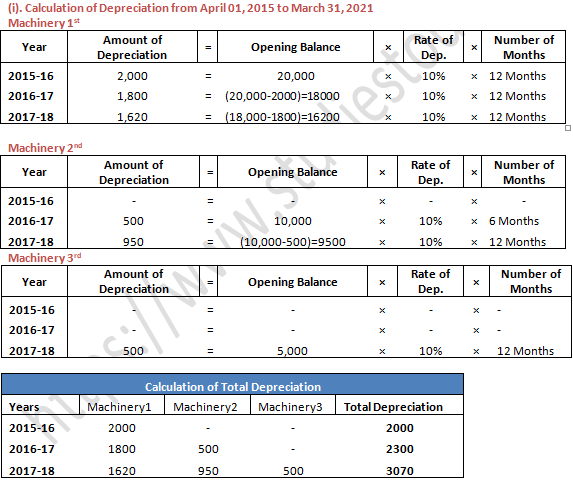

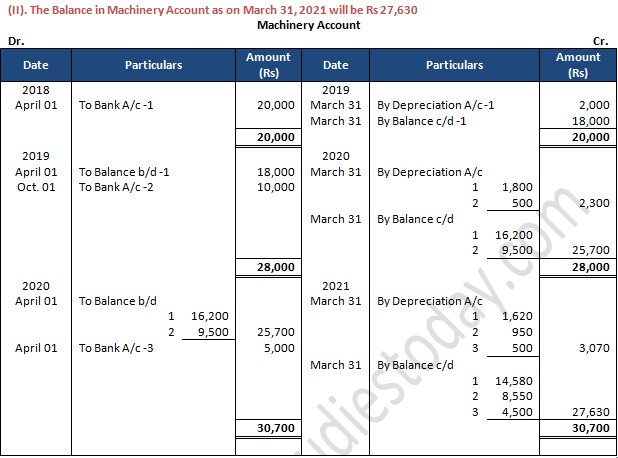

Question 6: On 1st April, 2015, Star Ltd. Purchased 5 machines for Rs. 60,000 each. On 1st April, 2017, one of the machines was sold at a loss of Rs. 8,000. On 1st July, 2018, second machine was sold at a loss of Rs. 12,500. A new machine was purchased for Rs. 1,00,000 on 1st October, 2018.

Prepare Machinery Account for 4 years, assuming accounts are closed on 31st March each year and depreciation is charged @ 10% per annum as per Straight Line Method.

Answer 6:

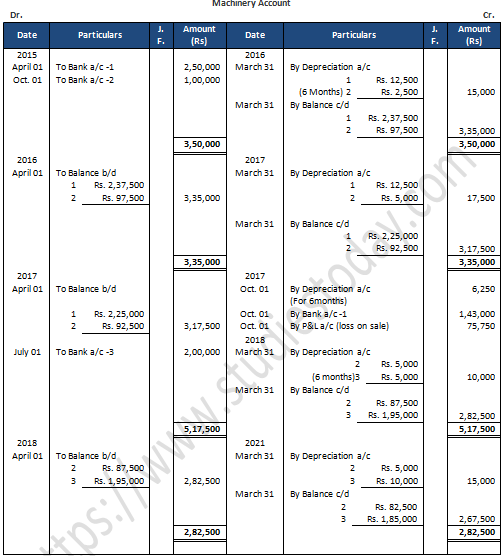

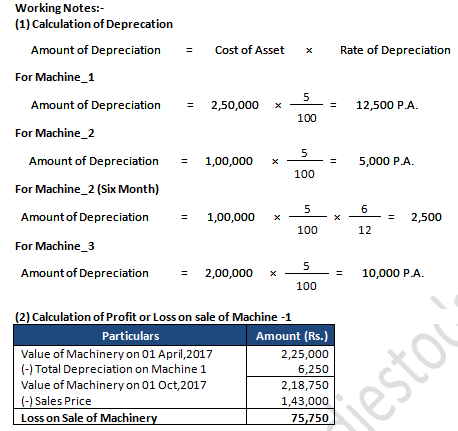

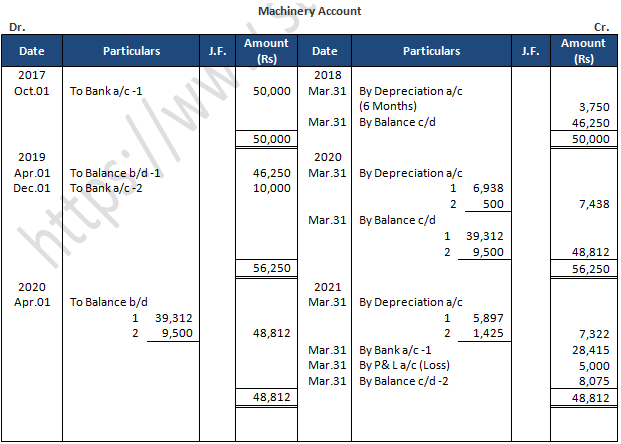

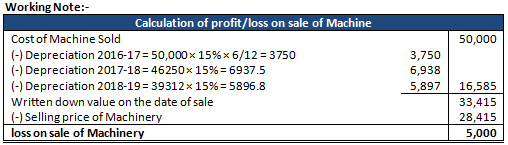

Question 7: On 1st April, 2017, A Ltd. purchased a machine for Rs. 2,40,000 and spent Rs. 10,000 on its erection. On 1st October, 2015 an additional machinery costing Rs. 1,00,000 was purchased. On 1st October, 2017, the machine purchased on 1st April, 2015 was sold for Rs. 1,43,000 and on the same date, a new machine was purchased at cost of Rs. 2,00,000.

Show the Machinery Account for the first four financial years after charging Depreciation at 5% p.a. by the Straight Line Method.

Answer 7:

Point of Knowledge:-

Cost of Assets = Purchases Price of Machine + Repairs and installation Charge

Cost of Assets = 2, 40,000 + 10,000

Cost of Assets = 2, 50,000

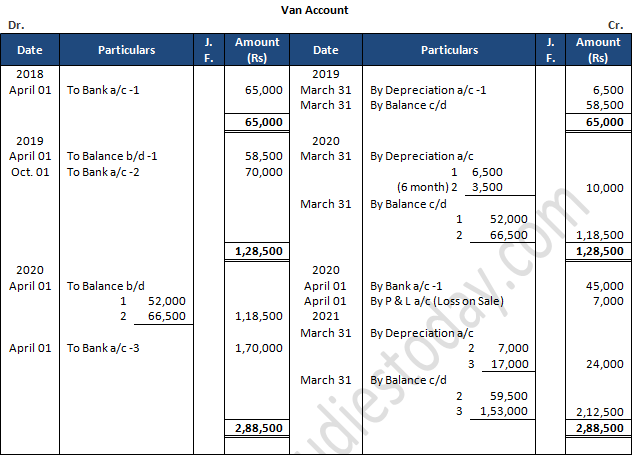

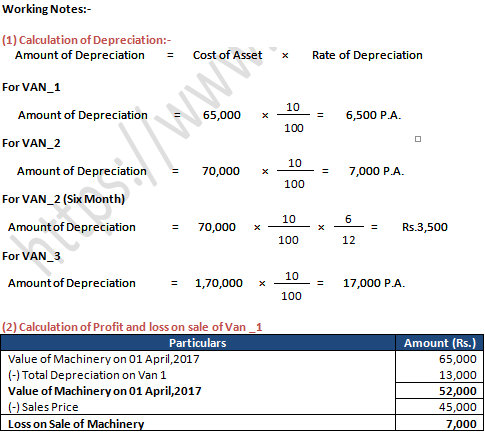

Question 8: A Van was purchased on 1st April, 2018 for Rs. 60,000 and Rs. 5,000 was spent on its repair and Registration. On 1st October, 2019 another van was purchased for Rs 70,000. On 1st April, 2020, the first van purchased on 1st April, 2020 was sold for Rs. 45,000 and a new van costing Rs. 1,70,000 was purchased on the same date. Show the Van Account from 2018-19 to 2020-21 on the basis of Straight Line Method, if the rate of Depreciation charged is 10% p.a. Assume that books are closed on 31st March every year.

Answer 8:

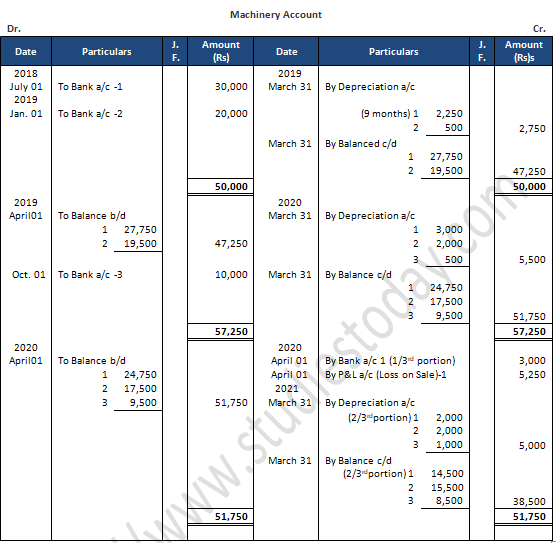

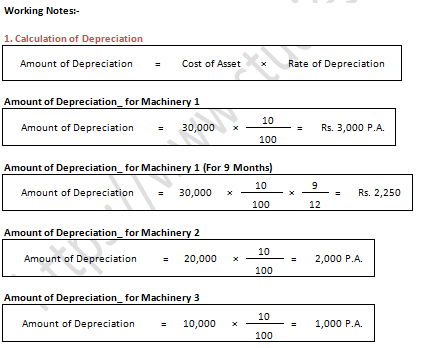

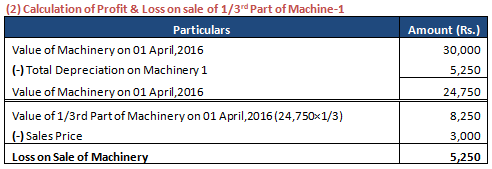

Question 9: A company whose accounting year is a financial year, purchased on 1st July, 2018 machinery costing Rs 30,000. It purchased further machinery on 1st January, 2019 costing Rs 20,000 and on 1st October, 2019 costing Rs 10,000. On 1st April, 2020, one-third of the machinery installed on 1st July, 2018 became obsolete and was sold for Rs 3,000. Show how Machinery Account would appear in the books of the company. It being given that machinery was depreciated by Fixed Installment Method at 10% p.a. What would be the value of Machinery Account on 1st April, 2021?

Answer 9:

Question 10: On 1st April, 2010, Plant and Machinery was purchased for Rs. 1,20,000. New machinery was purchased on 1st October, 2010 for Rs. 50,000 and on 1st July, 2011, for Rs. 25,000. On 1st January, 2013, a machinery of the original value of Rs. 20,000 which was included in the machinery purchased on 1st April, 2010, was sold for Rs. 6,000. Prepare Plant and Machinery a/c for three years after providing depreciation at 10% p.a. on Straight Line Method. Accounts are closed on 31st March every year.

Answer 10:

1. Calculation of depreciation for the year 2010 - 11

Depreciation on 1st machine Rs 1,20,000 × 10% = Rs. 12,000

Depreciation on 2nd machine Rs 50,000 × 10% × = Rs. 2,500

2. Calculation of depreciation for the year 2011 -12

Depreciation on 1st machine Rs 1,20,000 × 10% = Rs. 12,000

Depreciation on 2nd machine Rs 50,000 × 10% = Rs. 5,000

Depreciation on 3rd machine Rs 25,000 × 10% × = Rs. 1,875

3. Calculation of depreciation for the year 2011 -12

Depreciation on 1st machine Rs. 1,00,000 × 10% = Rs. 10,000

Depreciation on 2nd machine Rs. 50,000 × 10% = Rs. 5,000

Depreciation on 3rd machine Rs. 25,000 × 10% = Rs. 2,500

Depreciation on 4th machine Rs. 20,000 × 10% × = Rs. 500

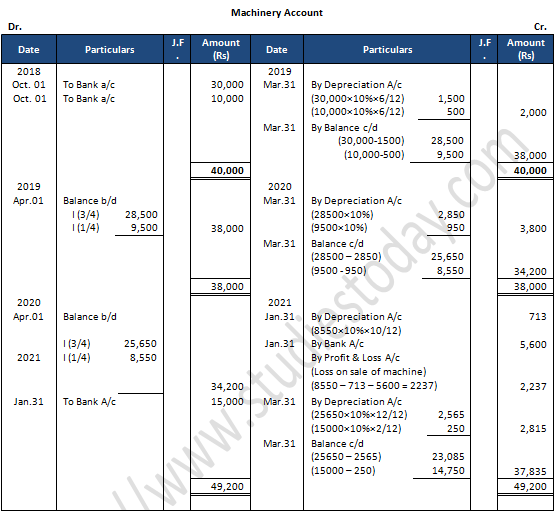

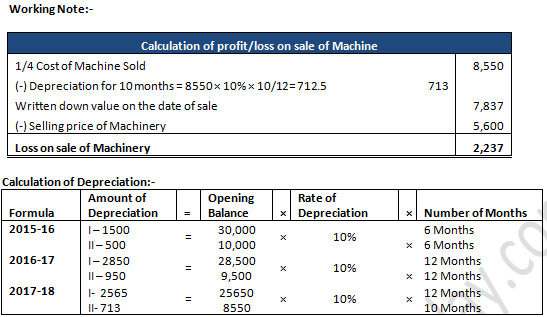

Question 11: On 1st July, 2017, A Co. Ltd. purchases second-hand machinery for Rs 20,000 and spends Rs 3,000 on reconditioning and installing it. On 1st January, 2016, the firm purchases new machinery worth Rs 12,000. On 30th June, 2017, the machinery purchased on 1st January, 2016, was sold for Rs 8,000 and on 1st July, 2017, a fresh plant was installed. Payment for this plant was to be made as follows:

1st July, 2017 Rs 5,000

30th June, 2018 Rs 6,000

30th June, 2021 Rs 5,500

Answer 11:

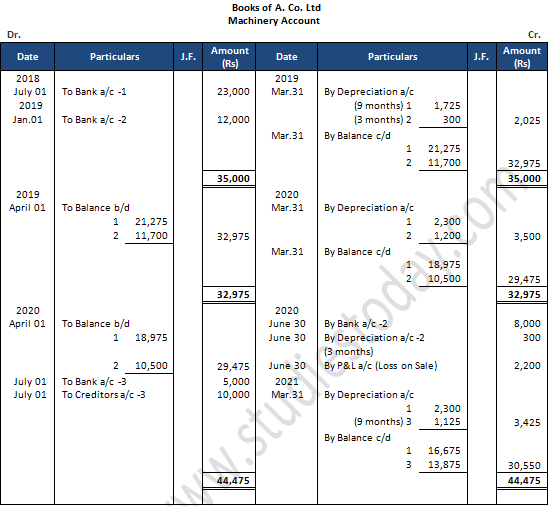

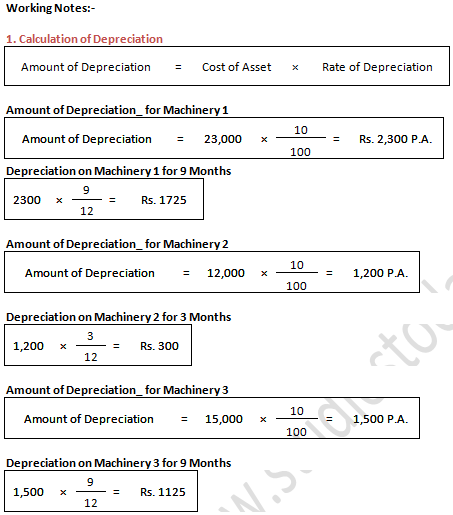

Question 11: On 1st April, 2015, Shivam Enterprise purchased second-hand machinery for Rs 52,000 and spent Rs 2,000 on cartage, Rs 3,000 on unloading, Rs 2,000 on installation and Rs 1,000 as brokerage of the middle man. It was estimated that the machinery will have a scrap value of Rs 6,000 at the end of its useful life, which is 10 years. On 31st December 2015, repairs and renewals amounted to Rs 2,500 were paid. On 1st October, 2017, this machine was sold for Rs 30,600 and an amount of Rs 600 was paid as commission to an agent. Calculate the amount of annual depreciation and rate of depreciation. Also prepare the Machinery Account for first 3 years, assuming that firm follows financial year for accounting. (Old Question)

Answer 11:

Working Notes:-

(1) Cost of Machinery: -

52,000+2,000+3,000+2,000+1,000 = Rs. 60,000/-

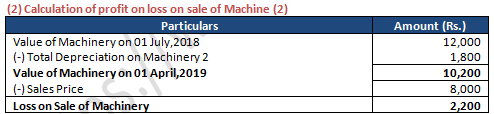

(2) Calculation of Profit or Loss on Sale

Point of Knowledge:-

1. If the nature of Expense is recurring it will not be added to Machinery A/c.

2. All the expenses which incurred on the date of purchases will be added to cost of machine.

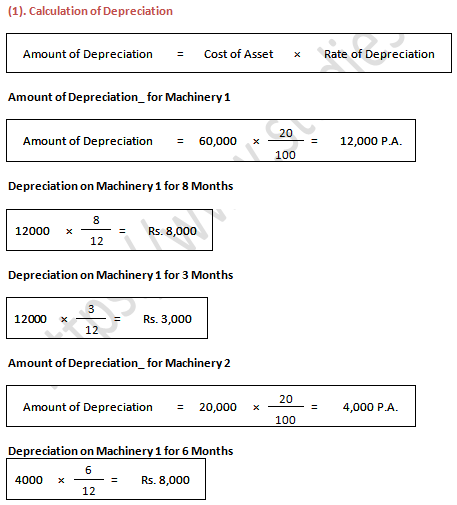

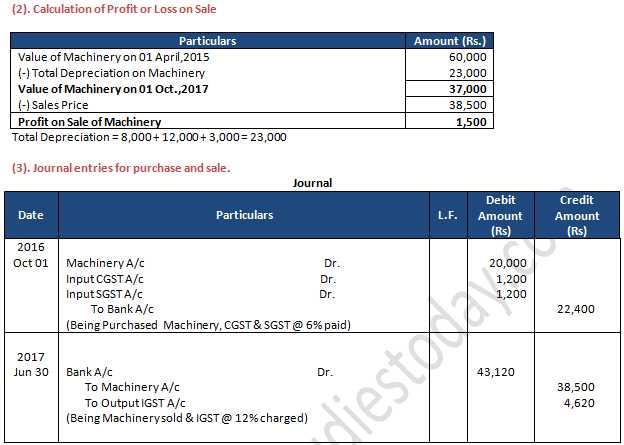

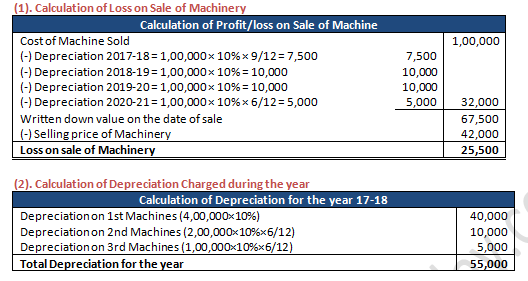

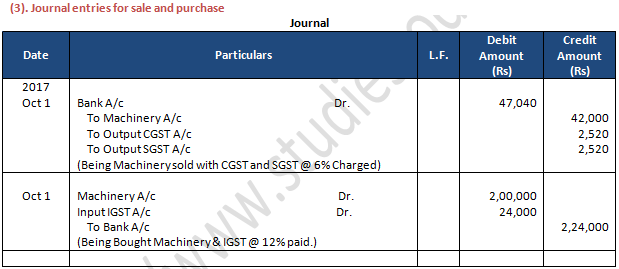

Question 12: Modern Ltd. purchased machinery on 1st August, 2018 for Rs. 60,000. On 1st October, 2019, it purchased another machine for Rs. 20,000 plus CGST and SGST @ 6% each. On 30th June, 2020, it sold the first machine purchased in 2018 for Rs. 38,500 charging IGST @ 12%. Depreciation is provided @ 20% p.a. on the original cost each year. Accounts are closed on 31st March every year. Prepare the Machinery A/c for three years.

Answer 12:

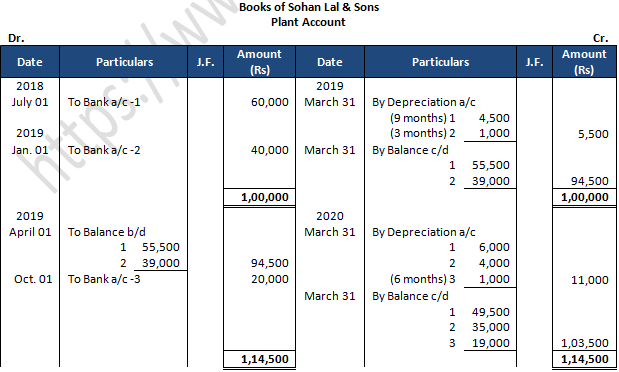

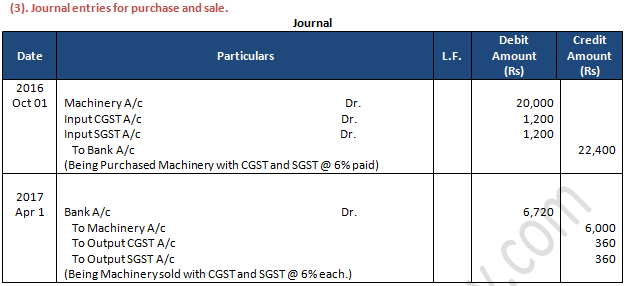

Question 13: On 1st July, 2018, Sohan Lal & Sons purchased a plant costing Rs 60,000. Additional plant was purchased on 1st January, 2019 for Rs 40,000 and on 1st October, 2019, for Rs 20,000, paying CGST and SGST @ 6% each. On 1st April, 2020, one-third of the plant purchased on 1st July, 2018, was found to have become obsolete and was sold for Rs 6,000, charging CGST and SGST @ 6% each.

Prepare the Plant Account for the first three years in the books of Sohan Lal & Sons. Depreciation is charged @ 10% p.a. on Straight Line Method. Accounts are closed on 31st March each year.

Answer 13:

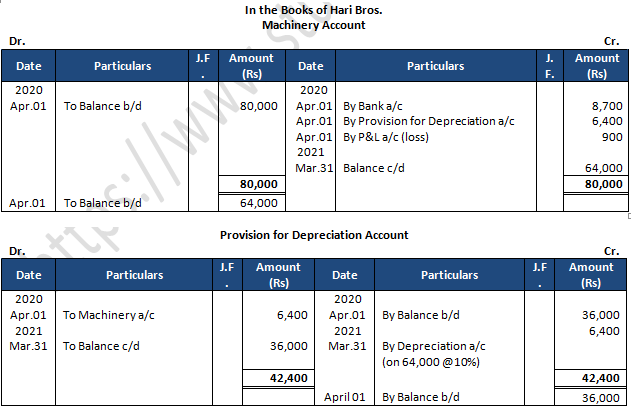

Question 14: Following balances appear in the books of Hari Bros:

On 1st April, 2020, they decided to sell a machine for Rs. 8,700. This machine was purchased for Rs. 16,000 in April, 2016. Prepare the Provision for Depreciation Account and Machinery Account on 31st March, 2021, assuming the firm has been charging Depreciation at 10% p.a. on Straight Line Method.

Answer 14:

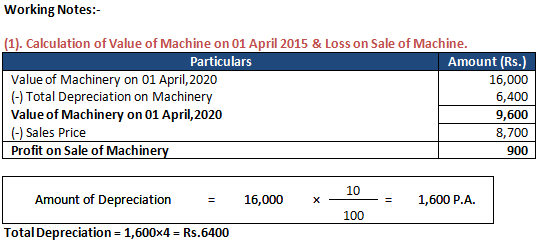

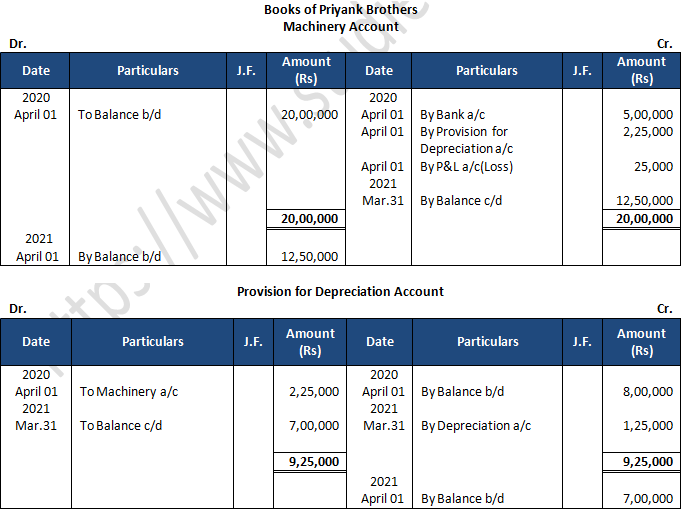

Question 15: Following balances appear in the books of Priyank Brothers:

On 1st April, 2020, they decide to sell a machine for Rs 5,00,000. This machine was purchased for Rs. 7,50,000 on 1st April, 2021. Prepare the Machinery Account and Provision for Depreciation Account for the year ended 31st March, 2021 assuming that the firm has been charging Depreciation @ 10% p.a. on the Straight Line Method.

Answer 15:

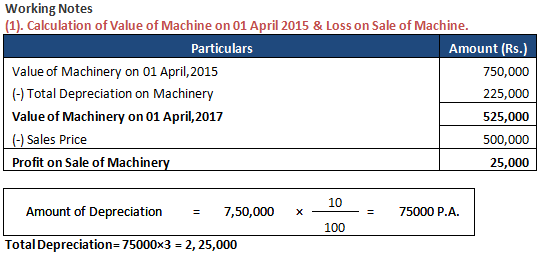

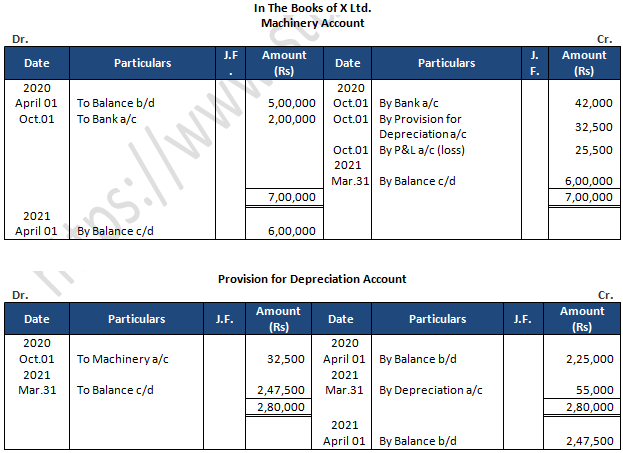

Question 16: Following balances appear in the books of X Ltd. as on 1st April, 2019:

The machinery is depreciated @ 10% p.a. on the Fixed Installment Method. The accounting year being April - March. On 1st October, 2019, a machinery which was purchased on 1st July, 2016 for Rs 1,00,000 was sold for Rs. 42,000 plus CGST and SGST @ 6% each and on the same date a new machine was purchased for Rs 2,00,000 paying IGST @ 12%. Prepare Machinery Account and Provision for Depreciation Account for the year ended 31st March, 2020.

Answer 16:

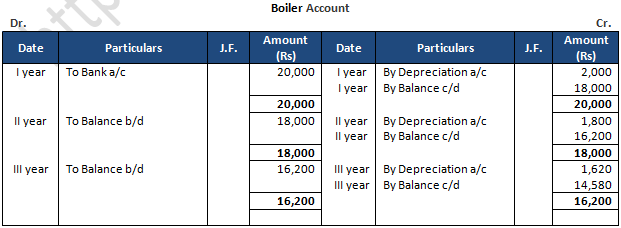

Question 17: A boiler was purchased from abroad for Rs 10,000; shipping and forwarding charges Rs 2,000, Import duty Rs 7,000 and expenses of installation amounted to Rs 1,000. Calculate the depreciation for the first three years (separately for each year) @ 10% on Diminishing Balance Method.

Answer 17:

Point of Knowledge:-

Cost of Boiler = Cost of Boiler + Shipping and forward charges + Import Duty + Installation Charges

= 10,000+2000+7000+1000

= Rs. 20,000

Calculation of Depreciation:-

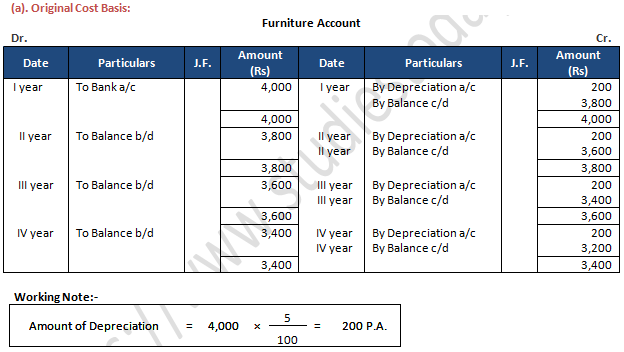

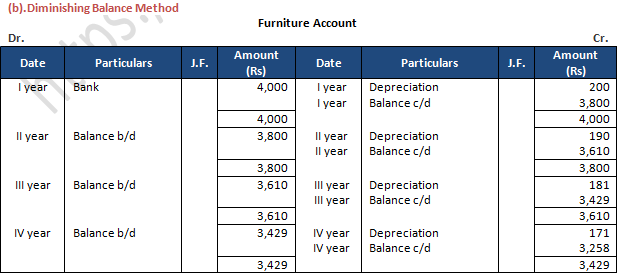

Question 18: The original cost of furniture amounted to Rs 4,000 and it is decided to write off 5% on the original cost as depreciation at the end of each year. Show the Ledger Account as it will appear during the first four years. Show also how the same account will appear if it was decided to write off 5% on the diminishing balance of the asset each year.

Answer 18:

Point of Knowledge:-

(1) Straight line Method is also known as Original Cost Method in this method the amount of depreciation is uniform from year to year. Sometimes in this method, the book value of assets becomes zero; still the assets are used in the business.

(2) Written down value method is also known as Diminishing Balance Method in this method, depreciation is charged at a fixed rate on the reducing balance every year.

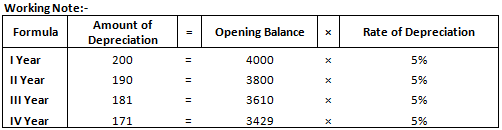

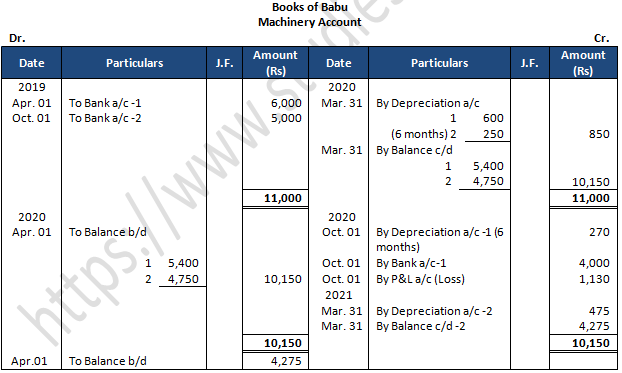

Question 19: Babu purchased on 1st April, 2019, a machine for Rs 6,000. On 1st October, 2019, he also purchased another machine for Rs 5,000. On 1st October, 2020, he sold the machine purchased on 1st April, 2019 for Rs 4,000. It was decided that Depreciation @ 10% p.a. was to be written off every year under Diminishing Balance Method. Assuming the accounts were closed on 31st March every year, show the Machinery Account for the years ended 31st March, 2020 and 2021.

Answer 19:

Question 20: X bought a machine for Rs 25,000 on which he spent Rs 5,000 for carriage and freight. Rs 1,000 for brokerage of the middleman, Rs 3,500 for installation and Rs 500 for an iron pad. The machine is depreciated @ 10% every year on Written Down Value basis. After three years, the machine was sold to Y for Rs 30,500 and Rs 500 was paid as commission to the broker through whom the sale was effected. Find out the profit and loss on sale of machine.

Answer 20:

Point of Knowledge:-

(a). Book Value of Machinery = Cost of Machine + Freight + Brokerage + Installation

= 25,000 + 5,000 + 1,000 + 3,500 + 500

= Rs.35,000

(b). Selling price of Machinery = 30500 - 500

= Rs. 30,000

(Only price of machinery includes in the books any of expenses are done on selling will not be added)

Working Note:-

Question 21: A company purchased machinery for Rs 50,000 on 1st October, 2018. Another machinery costing Rs 10,000 was purchased on 1st December, 2019. On 31st March, 2021, the machinery purchased in 2018 was sold at a loss of Rs 5,000. The company charges depreciation @ 15% p.a. on Diminishing Balance Method. Accounts are closed on 31st March every year. Prepare the Machinery Account for 3 years.

Answer 21:

Question 22: On 1st April, 2018, machinery was purchased for Rs. 20,000. On 1st October, 2019 another machine was purchased for Rs. 10,000 and on 1st April, 2020, one more machine was purchased for Rs. 5,000. The firm depreciates its machinery @ 10% p.a. on the Diminishing Balance Method.

What is the amount of Depreciation for the years ended 31st March, 2019; 2020 and 2021? What will be the balance in Machinery Account as on 31st March, 2021?

Answer 22:

Question 23: M/s. P & Q purchased machinery for Rs 40,000 on 1st October, 2018. Depreciation is provided @ 10% p.a. on the Diminishing Balance. On 31st January, 2021, one-fourth of the machinery was found unsuitable and disposed off for Rs 5,600. On the same date new machinery at a cost of Rs 15,000 was purchased. Write up the Machinery account for the years ended 31st March, 2019, 2020 and 2021. Accounts are closed on 31st March each year.

Answer 23:

Point of Knowledge:-

Always highlight your final answer at the end of the question.

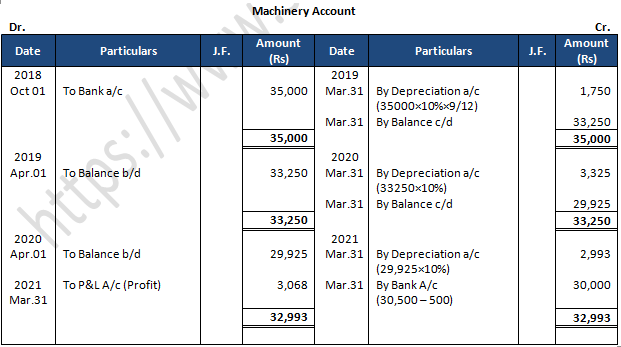

Question 24: On 1st October, 2018, Meenal Sharma bought a machine for Rs 25,000 on which he spent Rs 5,000 for carriage and freight; Rs 1,000 for brokerage of the middle-man, Rs 4,000 for installation. The machine is depreciated @ 10% p.a. on written down value basis. On 31st March, 2021 the machine was sold to Deepa for Rs 30,500 and Rs 500 was paid as commission to broker through whom the sales was effected. Find out the profit or loss on sale of machine if accounts are closed on 31st March, every year.

Answer 24:

Point of Knowledge:-

(a). Book Value of Machinery = Cost of Machine + Freight + Installation

= 25,000 + 5,000 + 1,000 + 4,000

= Rs.35,000

(b). Selling price of Machinery = 30500 - 500

= Rs. 30,000

(Only price of machinery includes in the books any of expenses are done on selling will not be added)

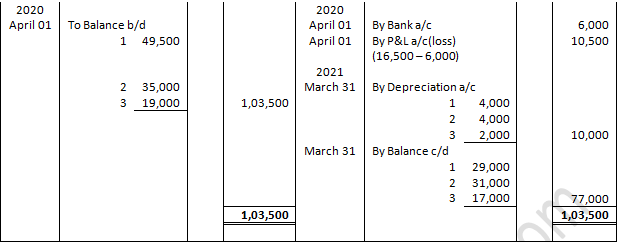

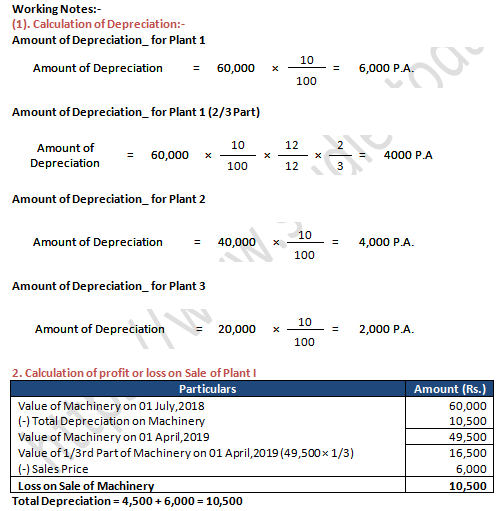

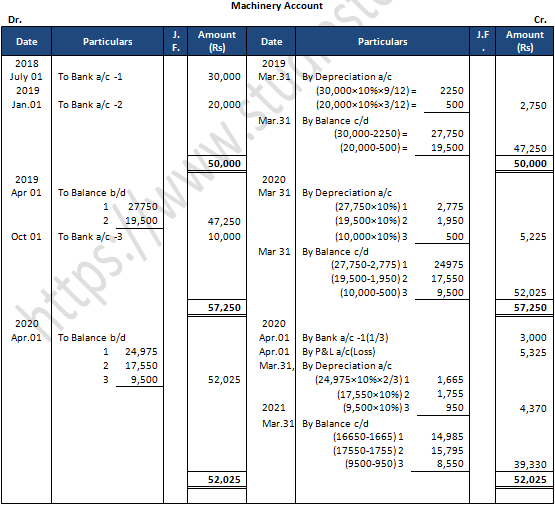

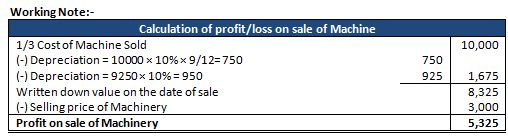

Question 25: A company purchased on 1st July, 2018 machinery costing Rs 30,000. It further purchased machinery on 1st January, 2019 costing Rs 20,000 and on 1st October, 2020 costing Rs 10,000. On 1st April, 2020, one-third of the machinery installed on 1st July, 2018 became obsolete and was sold for Rs 3,000. The company follows financial year as accounting year.

Show how the machinery Account would appear in the books of company if depreciation is charged @ 10% p.a. on Written Down Value Method.

Answer 25:

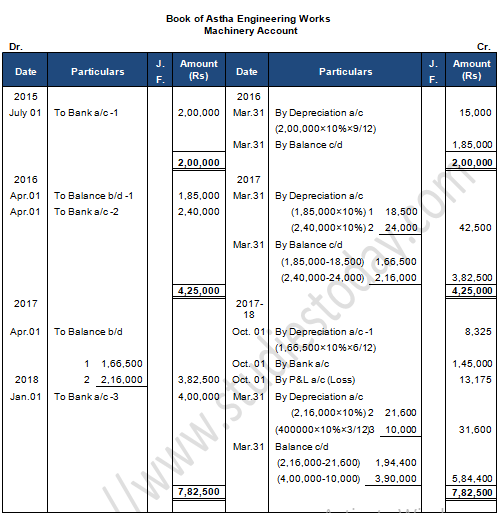

Question 26: Astha Engineering Works purchased a machine on 1st July, 2015 for Rs 1,80,000 and spent Rs 20,000 on its installation.

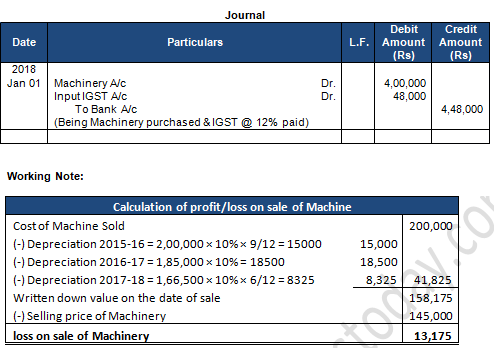

On 1st April, 2016, if purchased another machine for Rs 2,40,000. On 1st October, 2017, the machine purchased on 1st July, 2015 was sold for Rs 1,45,000. On 1st January, 2018, another machine was purchased for Rs 4,00,000 plus IGST @ 12%.

Prepare the Machinery Account for the years ended 31st March, 2016 to 2018 after charging Depreciation @ 10% p.a. by Diminishing Balance Method.

Accounts are closed on 31st March every year.

Answer 26:

Point of Knowledge:-

Total Cost of Machinery = Cost of Machinery + Installation charge

= Rs. 1, 80,000 + Rs. 20,000

= Rs. 2, 00,000

Journal entry for purchase

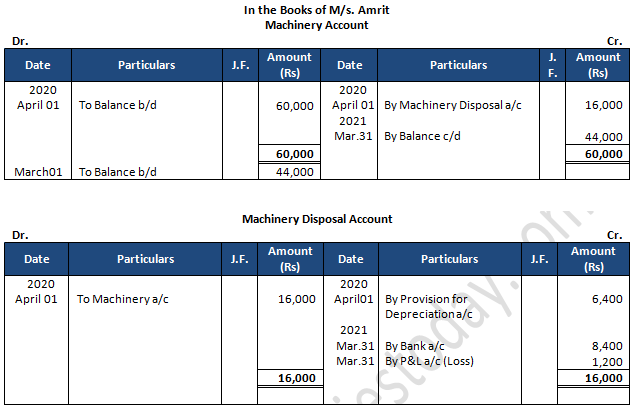

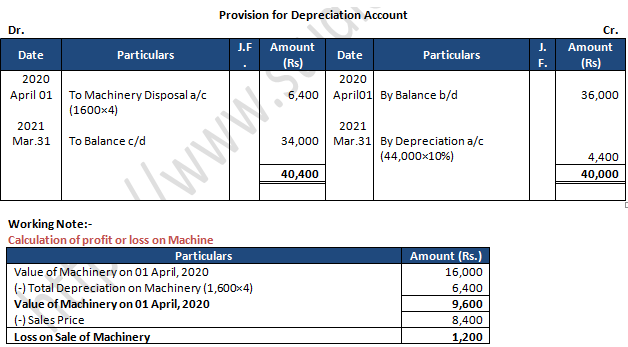

Question 27: Following balances appear in the books of M/s. Amrit as on 1st April, 2018:

On 1st April, 2020, they decided to dispose off machinery for Rs 8,400 which was purchased on 1st April, 2016 for Rs 16,000. You are required to prepare the Machinery A/c, Provision for Depreciation A/c and Machinery Disposal A/c for the year ended 31st March, 2021. Depreciation was charged at 10% on Cost following SLM.

Answer 27:

Point of Knowledge:-

(a). The Amount of depreciation is same every year.

(b). If the rate of depreciation is given, depreciation is computed on the original cost.

Question 28: Ashoka & Co. whose books are closed on 31st March, purchased a machinery for Rs 1,50,000 on 1st April, 2018, Additional machinery was acquired for Rs 50,000 on 1st October, 2018. Certain machinery which was purchased for Rs 50,000 on 1st October, 2018 was sold for Rs 40,000 on 30th September, 2020.

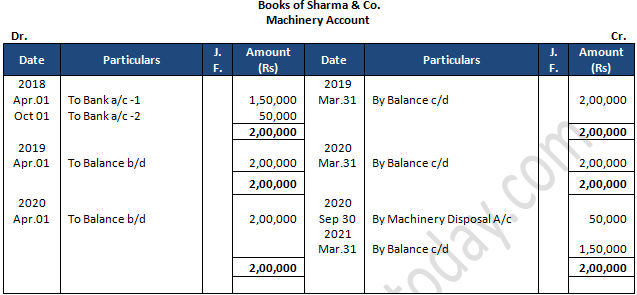

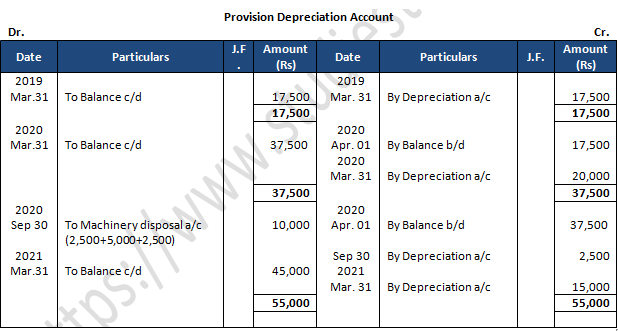

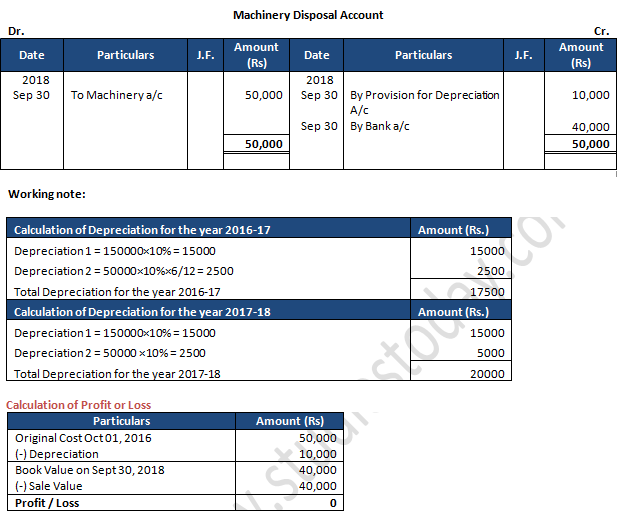

Prepare the Machinery Account and Accumulated Depreciation Account for all the years up to the year ended 31st March, 2021. Depreciation is charged @ 10% p.a. on Straight Line Method. Also, show the Machinery Disposal Account.

Answer 28:

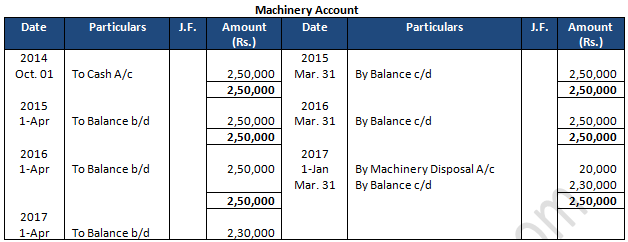

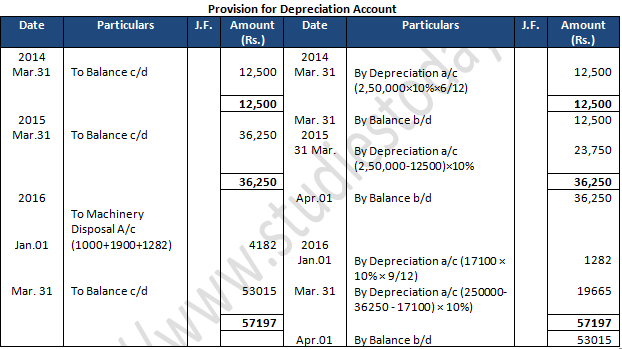

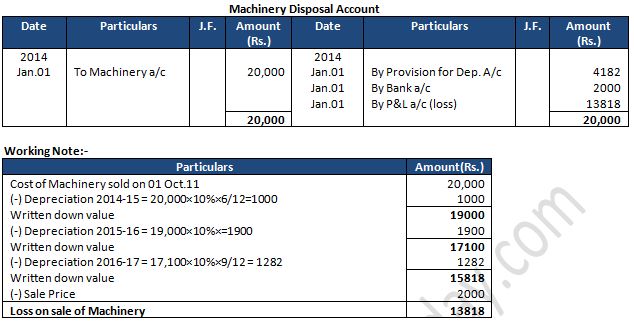

Question 29: On 1st October, 2014, X Ltd. purchased a machinery for Rs 2,50,000. A part of machinery which was purchased for Rs 20,000 on 1st October, 2011 became obsolete and was disposed off on 1st January, 2014 (having a book value Rs 17,100 on 1st April, 2013) for Rs 2,000. Depreciation is charged @ 10% annually on written down value. Prepare machinery disposal account and also show your workings. The books being closed on 31st March of every year.

Answer 29:

Point of Knowledge:-

Asset Disposal Account = When an asset being sold, a new account titled ‘Asset Disposal Account’ is opened in the ledger for the calculating profit & loss on the sale of an asset.