Please refer to CBSE Class 12 Accountancy HOTs Partnership Basic Concepts. Download HOTS questions and answers for Class 12 Accountancy. Read CBSE Class 12 Accountancy HOTs for Part 1 Chapter 2 Accounting for Partnership Basic Concepts below and download in pdf. High Order Thinking Skills questions come in exams for Accountancy in Class 12 and if prepared properly can help you to score more marks. You can refer to more chapter wise Class 12 Accountancy HOTS Questions with solutions and also get latest topic wise important study material as per NCERT book for Class 12 Accountancy and all other subjects for free on Studiestoday designed as per latest CBSE, NCERT and KVS syllabus and pattern for Class 12

Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 Accountancy HOTS

Class 12 Accountancy students should refer to the following high order thinking skills questions with answers for Part 1 Chapter 2 Accounting for Partnership Basic Concepts in Class 12. These HOTS questions with answers for Class 12 Accountancy will come in exams and help you to score good marks

HOTS Questions Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 Accountancy with Answers

MCQ Questions for NCERT Class 12 Accountancy Fundamentals Of Partnership

Question: Ajay is a partner in a firm. He withdrew Rs.2,000 per month on the last day of every month during the year ended 31st March, 2019. If interest on drawings is charged @ 9% p.a. the interest charged will be :

(A) Rs.990

(B) Rs.1,080

(C) Rs.1,170

(D) Rs.2,160

Answer: A

Question: If a fixed amount is withdrawn by a partner on the last day of each quarter, interest on the total amount is charged for ……………… months

(A) 6

(B) 4.5

(C) 7.5

(D) 3

Answer: B

Question: If a fixed amount is withdrawn by a partner in each quarter, interest on the total amount is charged for ……………….. months

(A) 3

(B) 6

(C) 4.5

(D) 7.5

Answer: B

Question: If fixed amount is withdrawn by a partner on the first day of each quarter, interest on the total amount is charged for …………….. months

(A) 4.5

(B) 6

(C) 7.5

(D) 3

Answer: C

Question: Bipasa is a partner in a firm. She withdrew Rs.6,000 at the end of each quarter during the year ended 31st March, 2019. Interest on her drawings @ 10% p.a. will be :

(A) Rs.900

(B) Rs.600

(C) Rs.1,500

(D) Rs.1,200

Answer: A

Question: Charulata is a partner in a firm. She withdrew Rs.10,000 in each quarter during the year ended 31st March, 2019. Interest on her drawings @ 9% p.a. will be:

(A) Rs.1,350

(B) Rs.2,250

(C) Rs.900

(D) Rs.1,800

Answer: D

Question: If equal amount is withdrawn by a partner in the beginning of each month during a period of 6 months, interest on the total amount will be charged for ……………… months

(A) 2.5

(B) 3

(C) 3.5

(D) 6

Answer: C

Question: Anuradha is a partner in a firm. She withdrew Rs.6,000 in the beginning of each quarter during the year ended 31st March, 2019. Interest on her drawings @ 10% p.a. will be :

(A) Rs.900

(B) Rs.1,200

(C) Rs.1,500

(D) Rs.600

Answer: C

Question: If equal amount is withdrawn by a partner in each month during a period of 6 months, interest on the total amount will be charged for …………… months

(A) 6

(B) 3

(C) 2.5

(D) 3.5

Answer: B

Question: Y is a partner in a firm. He withdrew regularly Rs.3,000 at the end of every month for the six months ending 31st March, 2019. If interest on drawings is charged @ 10% p.a. the interest charged will be :

(A) Rs.375

(B) Rs.450

(C) Rs.525

(D) Rs.900

Answer: A

Question: If equal amount is withdrawn by a partner in the end of each month during a period of 6 months, interest on the total amount will be charged for ………………… months

(A) 2.5

(B) 3

(C) 3.5

(D) 6

Answer: A

Question: P, Q and R are equal partners with fixed capitals of Rs.5,00,000, Rs.4,00,000 and Rs.3,00,000 respectively. After closing the accounts for the year ending 31st March 2019 it was discovered that interest on capitals was provided @ 7% instead of 9% p.a. In the adjusting entry :

(A) P will be credited by Rs.2,000 and Q will be debited by Rs.2,000.

(B) P will be debited by Rs.2,000 and Q will be credited by Rs.2,000.

(C) P will be debited by Rs.2,000 and R will be credited by Rs.2,000.

(D) P will be credited by Rs.2,000 and R will be debited by Rs.2,000.

Answer: D

Question: Z is a partner in a firm. He withdrew regularly Rs.2,000 every month for the six months ending 31st March, 2019. If interest on drawings is charged @ 8% p.a. the interest charged will be :

(A) Rs.480

(B) Rs.280

(C) Rs.200

(D) Rs.240

Answer: D

Question: X is a partner in a firm. He withdrew regularly Rs.1,000 at the beginning of every month for the six months ending 31st March, 2019. If interest on drawings is charged @ 8% p.a. the interest charged will be :

(A) Rs.240

(B) Rs.140

(C) Rs.100

(D) Rs.120

Answer: B

Question: A partner draws Rs.2,000 each on 1st April 2018, 1st July 2018, 1st October, 2018 and 1st January 2019. For the year ended 31st March, 2019 interest on drawings @ 8% per annum will be :

(A) Rs.540

(B) Rs.320

(C) Rs.960

(D) Rs.400

Answer: D

Question: A partner withdraws Rs.8,000 each on 1st April and 1st Oct. Interest on his drawings @ 6% p.a. on 31st March will be :

(A) Rs.480

(B) Rs.720

(C) Rs.240

(D) Rs.960

Answer: B

Question: A partner withdraws from firm Rs.7,000 at the end of each month. At the rate of 6% per annum total interest will be :

(A) Rs.5,040

(B) Rs.2,310

(C) Rs.3,570

(D) Rs.1,370

Answer: B

Question: Sony and Romy are equal partners with fixed capitals of Rs.4,00,000 and Rs.3,00,000 respectively. After closing the accounts for the year ending 31st March, 2019 it was discovered that interest on capitals was provided @ 8% instead of 10% p.a. In the adjusting entry :

(A) Sony will be credited by Rs.8,000 and Romy will be credited by Rs.6,000.

(B) Sony will be debited by Rs.8,000 and Romy will be debited by Rs.6,000.

(C) Sony will be debited by Rs.1,000 and Romy will be credited by Rs.1,000.

(D) Sony will be credited by Rs.1,000 and Romy will be debited by Rs.1,000.

Answer: D

Question: Anu and Tanu are equal partners with fixed capitals of Rs.2,00,000 and Rs.1,00,000 respectively. After closing the accounts for the year ending 31st – March, 2019 it was discovered that interest on capitals @ 8% p.a. was omitted to be provided. In the adjusting entry :

(A) Anu will be credited by Rs.16,000 and Tanu will be credited by Rs.8,000

(B) Anu will be debited by Rs.16,000 and Tanu will be debited by Rs.8,000

(C) Anu will be credited by Rs.4,000 and Tanu will be debited by Rs.4,000

(D) Anu will be debited by Rs.4,000 and Tanu will be credited by Rs.4,000

Answer: C

Question: P and Q sharing profits in the ratio of 2 : 1 have fixed capitals of Rs.90,000 and f60,000 respectively. After closing the accounts for the year ending 31st March 2019 it was discovered that interest on capitals was provided @ 6% instead of 8% p.a. In the adjusting entry :

(A) P will be credited by Rs.1,800 and Q will be credited by Rs.1,200;

(B) P will be debited by Rs.200 and Q will be credited by Rs.200;

(C) P will be credited by Rs.200 and Q will be debited by Rs.200;

(D) P will be debited by Rs.1,800 and Q will be debited by Rs.1,200;

Answer: B

Question: A and B sharing profits in the ratio of 7 : 3 have fixed capitals of Rs.2,00,000 and Rs.1,00,000 respectively. After closing the accounts for the year ending 31st March 2019 it was discovered that interest on capitals was provided @ 12% instead of 10% p.a. In the adjusting entry :

(A) A will be debited by Rs.4,000 and B will be debited by Rs.2,000;

(B) A will be credited by Rs.4,000 and B will be credited by Rs.2,000;

(C) A will be debited by Rs.200 and B will be credited by Rs.200;

(D) A will be credited by Rs.200 and B will be debited by Rs.200;

Answer: D

Question: Xand 7are partners in the ratio of 3 : 2. Their fixed capitals are Rs.2,00,000 and Rs.1,00,000 respectively. After clsoing the accounts for the year ending 31st March 2019, it was discovered that interest on capital was allowed @ 12% instead of 10% per annum. By how much amount A will be debited/credited in the adjustment entry :

(A) Rs.600 (Debit)

(B) Rs.400 (Credit)

(C) Rs.400 (Debit)

(D) Rs.600 (Credit)

Answer: C

Question: Asha and Vipasha are equal partners with fixed capitals of Rs.5,00,000 and Rs.2,00,000 respectively. After closing the accounts for the year ending 31st March 2019 it was discovered that interest on capitals was provided @ 6% instead of 5% p.a. In the adjusting entry :

(A) Asha will be debited by Rs.1,500 and Vipasha will be credited by Rs.1,500;

(B) Asha will be credited by Rs.1,500 and Vipasha will be debited by Rs.1,500;

(C) Asha will be debited by Rs.5,000 and Vipasha will be debited by Rs.2,000;

(D) Asha will be credited by Rs.5,000 and Vipasha will be credited by Rs.2,000;

Answer: A

Question: X, Y and Z are equal partners with fixed capitals of Rs.2,00,000, Rs.3,00,000 and Rs.4,00,000 respectively. After closing the accounts for the year ending 31st March 2019 it was discovered that interest on capitals @ 8% p.a. was omitted to be provided. In the adjusting entry :

(A) Dr. X and Cr. Y by Rs.8,000

(B) Cr. X and Dr. Z by Rs.8,000

(C) Dr. X and Cr. Z by Rs.8.000

(D) Cr. X and Dr. Y by Rs.8,000

Answer: C

CASE STUDEY BASED QUESTIONS

Read the hypothetical text and answer the following questions.

: X and Y are partners in a firm sharing profits equally. On 1st April, 2020, the capitals of the partners were Rs. 2,00,000 and Rs. 1,50,000 respectively. The Profit and Loss Appropriation Account of the firm showed a net profit of Rs. 3,75,000 for the year ended 31st March, 2021. The Partnership Deed provided the following:

i) Transfer 10% of distributable profit to Reserve Fund.

ii) Interest on capital @ 6% p.a.

iii) Interest on drawings @ 6% p.a. Drawings for X and Y were Rs. 40,000 and Rs. 30,000 respectively.

Question: Total interest on capital provided is ………………………..

a) Rs. 9,000

b) Rs. 12,000

c) Rs. 21,000

d) Rs. 18,000

Answer: C

Question: What is the average period for which interest on drawings will be calculated?

a) 3 months

b) 6 months

c) 9 months

d) 12 months

Answer: B

Question: The amount is to be transferred to Reserve Fund is ………………

a) Rs. 37,500

b) Rs. 35,610

c) Rs. 37,710

d) Rs. 36,400

Answer: B

Question: The lesser interest on drawings charged is ………………….

a) Rs. 900

b) Rs. 1,200

c) Rs. 2,100

d) Rs. 1,500

Answer: A

Read the hypothetical text and answer the following questions.

:M, N and O entered into partnership firm on 1st July, 2018 and decided to share profits and losses in the ratio of 3:2:1. M guaranteed that O’s share of profit after charging interest on capitals @ 6% p.a. would not be less than Rs. 36,000 p.a. The capital contributed by M: Rs. 2,00,000, N: Rs. 1,00,000 and O: Rs. 1,00,000 respectively. Profit for the year ended 31st March, 2019 was Rs. 1,38,000.

Question: What is the distributable amount of profit?

a) Rs. 1,00,000

b) Rs. 1,20,000

c) Rs. 1,10,000

d) Rs. 90,000

Answer: B

Question: What is the total amount of interest on capital?

a) Rs. 9,000

b) Rs. 12,000

c) Rs. 18,000

d) Rs. 24,000

Answer: C

Question: What is deficiency amount to be borne by M?

a) Rs. 16,000

b) Rs. 7,000

c) 12,000

d) Rs. 15,000

Answer: B

Question: What is the share of profit of O?

a) Rs. 27,000

b) Rs. 36,000

c) Rs. 18,000

d) Rs. 9,000

Answer: A

Read the hypothetical text and answer the following questions.

Luv and Kush formed a partnership to sell low sodium, plant based vegan snacks. Since both of them had a family, they decided to withdrew a salary of Rs. 12,000 per quarter. Luv also withdrew Rs. 1,00,000 on 31st December,2020 to get his wife treated for Covid 19.

The partnership deed provided for 10% interest on drawings.

Kush introduced Rs. 50,000 as additional capital on 31st January,2021. The net distributable profit was Rs. 2,00,000 which was divided by the partners after providing 25% to General Reserve.

Question: Interest on Luv’s drawings will be ……………………………

a) Rs. 2,500

b) Rs. 5,000

c) Rs. 7,500

d) Rs. 10,000

Answer: A

Question: Interest on Kush’s capital will be………………………….

a) Rs. 5,000

b) Rs. 10,000

c) Rs. 20,000

d) None of these

Answer: D

Question: Total amount of salary credited to partners’ account is……………………….

a) Rs. 12,000

b) Rs. 48,000

c) Rs. 96,000

d) Rs. 24,000

Answer: C

Question: What was the amount to be transferred to General Reserve?

a) Rs. 25,000

b) Rs. 50,000

c) Rs. 75,000

d) Rs. 1,00,000

Answer: B

Read the hypothetical text and answer the following questions.

S and P are two partners in a firm sharing profit and losses in the ratio of 3:2. At the time of distributing the net profit between the partners, interest on capital was credited @ 18% instead of 8% wrongly. Partners’ capitals are given on 1st April, 2018 as Rs. 5,00,000 and Rs. 3,00,000 respectively. Profit on 31st March, 2019 is Rs. 2,00,000.

Question: The excess interest on capital provided to P which is to be debited now is ………………

a) Rs. 24,000

b) Rs. 30,000

c) Rs. 54,000

d) Rs. 50,000

Answer: B

Question: The excess interest on capital provided to S which is to be debited now is ………………

a) Rs. 40,000

b) Rs. 50,000

c) Rs. 90,000

d) Rs. 30,000

Answer: B

Question: Whose account will be benefitted by this past adjustment?

a) P

b) S

c) Both of these

d)None of the above

Answer: A

Read the hypothetical text and answer the following questions.

P, Q and R are partners in a firm. Their capitals are Rs. 30,000, Rs. 20,000 and Rs. 10,000 respectively. As per partnership deed,

i) R is to be allowed remuneration of Rs. 3,000 p.a.

ii) Interest on capital @ 5% p.a.

iii) Profits should be distributed in the ratio of 2:2:1.

Ignoring the above terms, net profit of Rs. 18,000 was distributed among the partners equally.

Question: How much profit is to be credited to the Partner Q after all adjustments?

a) Rs. 2,400

b) Rs. 4,800

c) Rs. 1,000

d) Rs. 1,200

Answer:B

Question: How much interest on capital is to be credited to the partner P?

a) Rs. 1,500

b) Rs. 1,000

c) Rs. 900

d) Rs. 800

Answer: A

Question: What is the amount of the past adjustment entry?

a) Rs. 350

b) Rs. 450

c) Rs. 250

d) Rs. 550

Answer: B

Question: What is the total profit to be credited to P, Q and R after all adjustments?

a) Rs. 12,000

b) Rs. 8,000

c) Rs. 9,000

d) Rs. 10,000

Answer: A

Read the hypothetical text and answer the following questions .

A,B and C are partners in a firm sharing profits and losses in the ratio of 2:2:1. Their capitals(Fixed) are Rs. 1,00,000, Rs. 80,000 and Rs. 70,000 respectively. For the year 2018-19, interest on capital was to be credited to them @ 9% p.a. instead of 12%

Question: What was the net amount should be credited to partner C?

a) Rs. 1,800

b) Rs. 2,000

d) Rs. 2,100

d) Rs. 1,700

Answer: C

Question: What was the net amount should be credited to partner B?

a) Rs. 1,500

b) Rs. 2,400

c) Rs. 1,800

d) Rs.1,200

Answer: B

Question: What was the amount of past adjustment entry?

a) Rs. 400

b) Rs. 300

c) Rs. 600

d) Rs. 500

Answer: C

Question: What was the amount that debited to partner B?

a) Rs. 1,500

b) Rs. 2,000

c) Rs. 3,000

d) Rs. 4,000

Answer: C

MCQ Questions for NCERT Class 12 Accountancy Fundamentals Of Partnership

Question: Which of the following statement is true?

(A) Fixed capital account will always have a credit balance

(B) Current account can have a positive or a negative balance

(C) Fluctuating capital account can have a positive or a negative balance

(D) All of the above

Answer: D

Question: Seeta and Geeta are partners sharing profits and losses in the ratio 4 : 1. Meeta was manager who received the salary of Rs.4,000 p.m. in addition to a commission of 5% on net profits after charging such commission. Profit for the year is Rs.6,78,000 before charging salary. Find the total remuneration of Meeta. (A) Rs.78,000

(B) Rs.88,000

(C) Rs.87,000

(D) Rs.76,000

Answer: A

Question: Which accounts are opened when the capitals are fluctuating?

(A) Only Capital Accounts

(B) Only Current Accounts

(C) Capital Accounts as well as Current Accounts

(D) Either Capital Accounts or Current Accounts

Answer: A

Question: Balance of partner’s current accounts are :

(A) Debit balance

(B) Credit balances

(C) Debit or Credit balances

(D) Neither Debit nor credit balances

Answer: C

Question: If the Partners’ Capital Accounts are fixed ‘salary payable to partner’ will be recorded :

(A) On the debit side of Partners’ Current Account

(B) On the debit side of Partners’ Capital Account

(C) On the credit side of Partners’ Current Account

(D) None of the above

Answer: C

Question: Which accounts are opened when the capitals are fixed?

(A) Only Capital Accounts

(B) Only Current Accounts

(C) Capital Accounts as well as Current Accounts

(D) Either Capital Accounts or Current Accounts

Answer: C

Question: Which item is recorded on the credit side of partner’s current accounts :

(A) Interest on Fanner’s Capitals

(B) Salaries of Partners

(C) Share of profits of Partners

(D) All of the Above

Answer: D

Question: If the Partner’s Capital Accounts are fluctuating, in that case following item/items will be recorded in the credit side of capital accounts :

(A) Interest on capital

(B) Salary of partners

(C) Commission of partners

(D) All of the above

Answer: D

Question: Interest on partner’s capitals will be credited to :

(A) Profit and Loss Account

(B) Profit and Loss Appropriation Account

(C) Interest Account

(D) Partner’s Capital Accounts

Answer: D

Question: It the Partner’s Capital Accounts are fixed, interest on capital will be recorded:

(A) On the credit side of Current Account

(B) On the credit side of Capital Account

(C) On the debit side of Current Account

(D) On the debit side of Capital Account

Answer: A

Question: For the firm, interest on drawings is

(A) Capital Payment

(B) Expenses

(C) Capital Receipt

(D) Income

Answer: D

Question: Interest on partner’s capitals will be debited to :

(A) Profit and Loss Account

(B) Profit and Loss Appropriation Account

(C) Partner’s Capital Accounts

(D) None of the Above

Answer: B

Question: When partners’ capital accounts are floating, which one of the following items will be written on the credit side of the partners’ capital accounts? :

(A) Interest on drawings

(B) Loan advanced by partner to the firm

(C) Partner’s share in the firm’s loss

(D) Salary to the active partners

Answer: D

Question: Interest on Partner’s drawings will be debited to :

(A) Profit and Loss Account

(B) Profit and Loss Appropriation Account]

(C) Partner’s Current Account

(D) Interest Account

Answer: C

Question: Interest on partner’s drawings will be credited to

(A) Profit and Loss Account

(B) Profit and Loss Appropriation Account

(C) Partner’s Capital Accounts

(D) None of the Above

Answer: B

Question: When partners’ capital accounts are fixed, which one of the following items will be written in the partner’s capital account? :

(A) Partner’s Drawings

(B) Additional capital introduced by the partner in the firm

(C) Loan taken by partner from the firm

(D) Loan Advanced by partner to the firm

Answer: B

Question: On 1st April 2018, a partner, A’s Capital was Rs.2,00,000. On 1st October 2018, he introduces additional capital of Rs.1,00,000.His interest on capital @ 6% p.a. on 31st March, 2019 will be :

(A) Rs.9,000

(B) Rs.18,000

(C) Rs.10,500

(D) Rs.15,000

Answer: D

Accounting for partnership firms - Fundamentals

Question: What is the status of partnership from an accounting viewpoint ?

Answer: From an accounting viewpoint, partnership is a separate business entity. From a legal viewpoints, however, a Partnership, like a sole proprietorship, is not separate from the owners.

Question: List the items that may appear on the debit side and credit side of a partner's fluctuating capital account.

Answer: On debit side : Drawing, interest on drawing, share of loss, closing credit balance of the capital. On credit side : Opening credit balance of capital, additional capital introduced, share of profit, interest on capital, salary to a Partner, commission to a Partner.

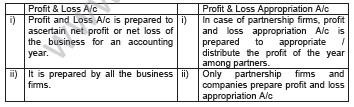

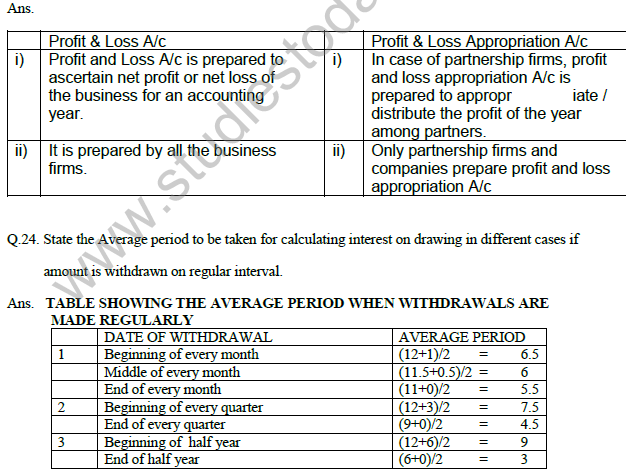

Question: 3 Give two points of difference between Profit and Loss and profit and loss appropriation A/c.

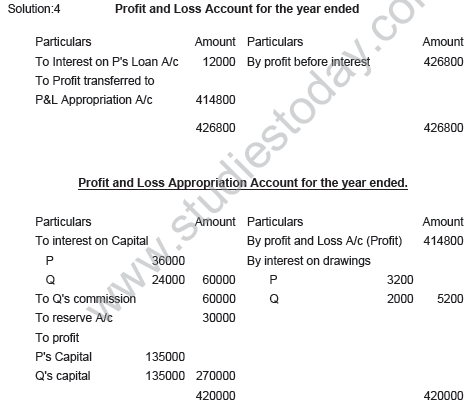

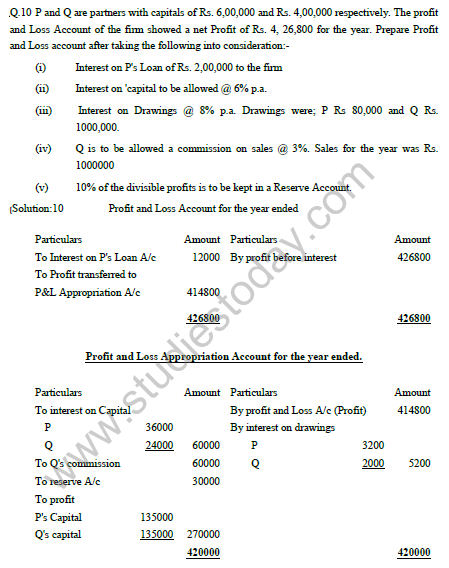

Question: P and Q are partners with capitals of Rs. 6,00,000 and Rs. 4,00,000 respectively.

The profit and Loss Account of the firm showed a net Profit of Rs. 4, 26,800 for the year. Prepare Profit and Loss account after taking the following into consideration:-

(i) Interest on P's Loan of Rs. 2,00,000 to the firm.

(ii) Interest on 'capital to be allowed @ 6% p.a.

(iii) Interest on Drawings @ 8% p.a. Drawings were ; P Rs 80,000 and Q Rs.1000,000.

(iv) Q is to be allowed a commission on sales @ 3%. Sales for the year was Rs. 1000000

(v) 10% of the divisible profits is to be kept in a Reserve Account.

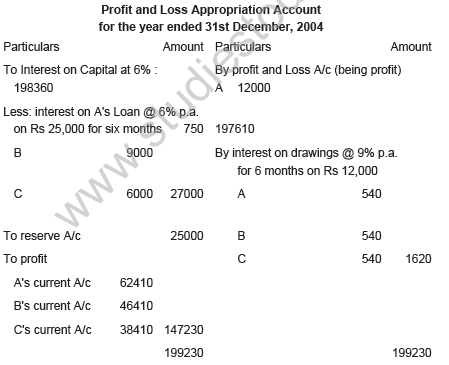

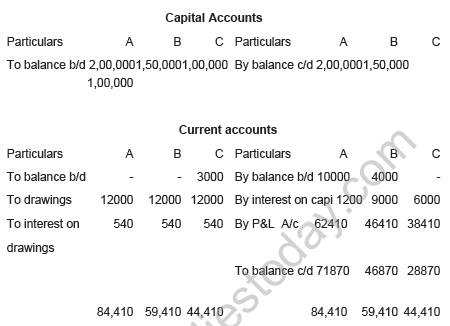

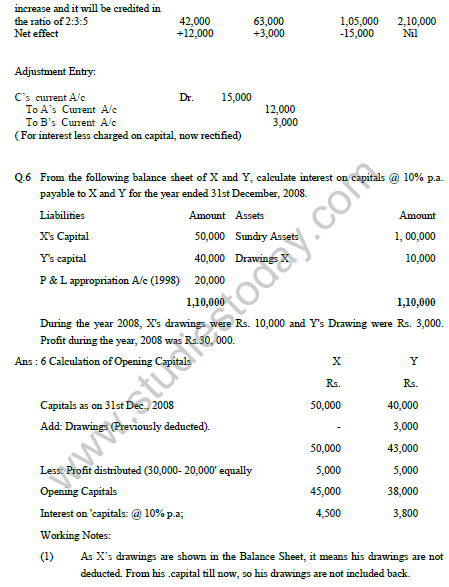

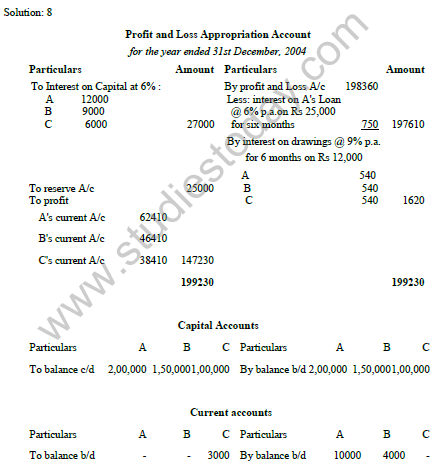

A Rs. 10,000 (Cr.); B Rs. 4,000 (Cr.) and C Rs. 3,000 (Dr.). A gave a loan to the firm of Rs. 25,000 on 1st July, 2004. The Partnership deed provided for the following:-

(i) Interest on Capital at 6%.

(ii) Interest on drawings at 9%. Each partner drew Rs. 12,000 on 1st July, 2004.

(iii) Rs. 25,000 is to be transferred in a Reserve Account.

(iv) Profit sharing ratio is 5:3: 2 upto Rs. 80,000 and above Rs. 80,000 equally.

Net Profit of the firm before above adjustments was Rs. 1,98,360. From the above information prepare Profit and Loss Appropriation Account, Capital and Current Accounts of the partners.

Solution: 5

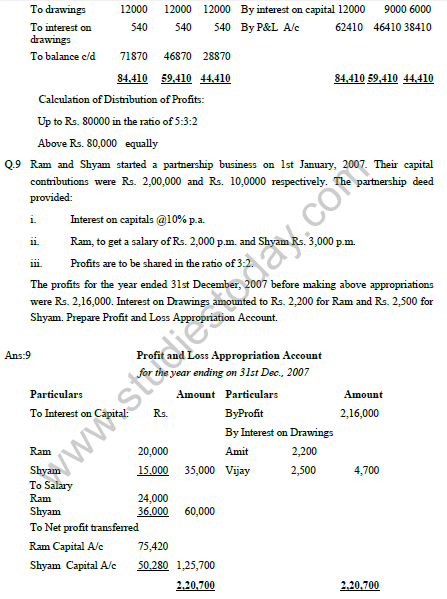

Question: Yogesh, Ajay and Atul are partners sharing profits in the ratio 4:3:2. Yogesh withdraws Rs.3,000 in the beginning of every month. Ajay withdraws Rs. 2,000 in the middle of every month whereas Atul withdraws Rs. 1,500 at the end of every month. Interest on capitals and drawings is to be calculated @ 12% p.a. Ajay is also to be allowed a salary of Rs. 1,000 per month. After deducting salary but before charging any type of interest, the profit for the year ending 31stpecember, 1997 was Rs.,1,14,780. Prepare Profit & Loss Appropriation Account, Partners' Capital Accounts and Current Accounts from the additional information given below:

SOLUTION

When there is no agreement between the partners, whether written or verbal, expressed or implied accounts of partners are determined by the following rules given in the Indian Partnership Act, 1932 sections 12 to 17.

(i) No interest is to be given on the partners' capital.

(ii) No interest is to be charged on the personal drawings of the partners.

(iii) No Salary Remuneration or Commission is to be given to any partner for his active participation.

(iv) If any partner has given loan to the firm interest at the rate of 6% p.a. can be given.

(v) Profits and losses will be shared among all the partners equally irrespectiveof their capitals.

Question: Ram and Shyam were Partners. in a firm sharing profits in the ratio of 3 : 5. Their Fixed Capitals were ': Ram Rs. 5,00,000 and Shyam Rs. 9,00,000. After the accounts of the year had been closed, it was found that interest on capital at 10% per annum as provided in the partnership agreement has not been credited to the Capital Accounts of the partners. pass necessary entry to rectify the error.

Solution: Rs.

Interest on Ram's Capital of Rs. 5,00,000 @ 10% = 50,000

Interest on Shyam 's Capital of Rs. 9,00,000 @ 10% = 90,000

Total interest to be a1lowed = 1,40,000

Profit already distributed 140000 in the ratio 3:5 ie 52500 and 87500 the difference is 2500 . The entry is

Ram A/C Dr 2500

To Shyam A/C 2500

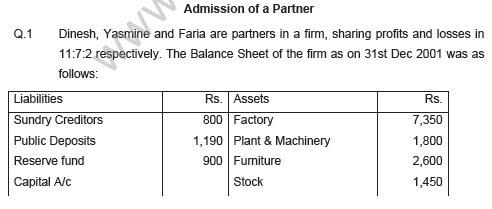

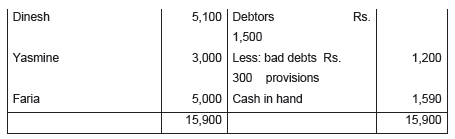

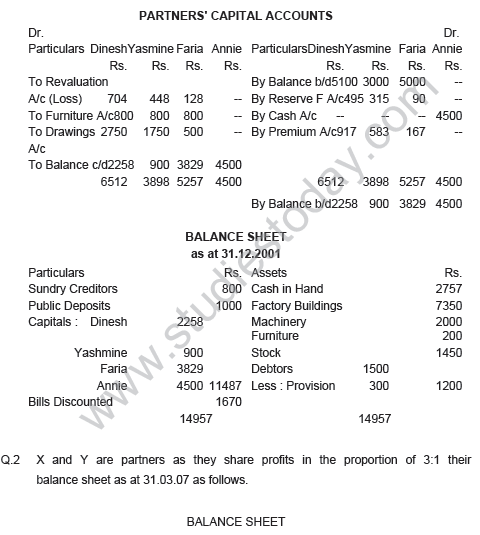

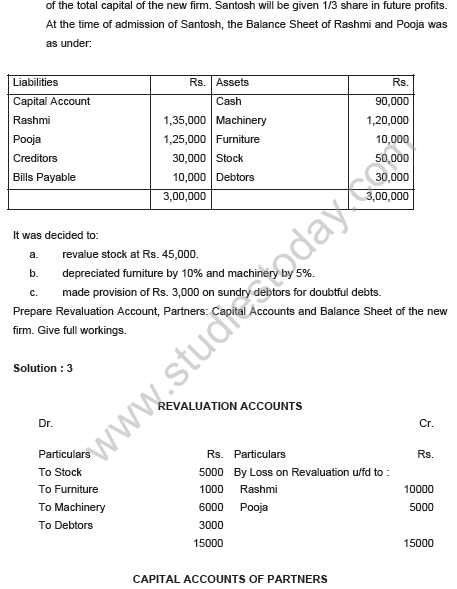

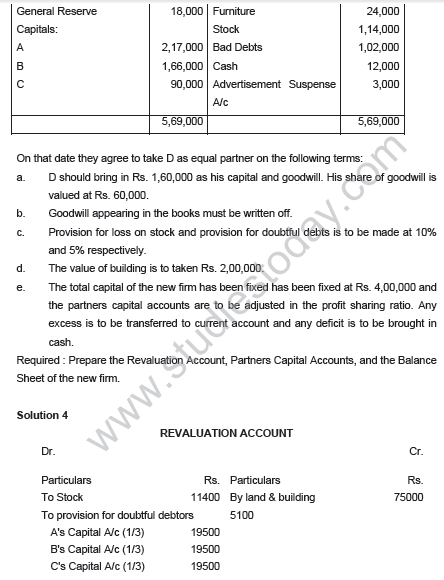

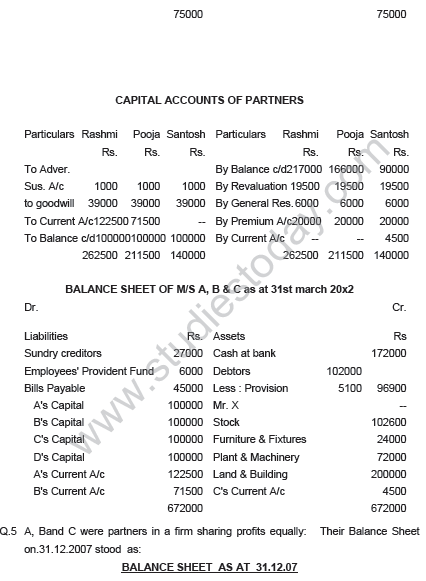

On the same date, Annie is admitted as a partner for on-sixth share in the profits with Capital of Rs. 4,500 and necessary amount for his share of goodwill on the following terms:-

a. Furniture of Rs. 2,400 were to be taken over by Dinesh, Yasmine and Faria equally.

b. A Liability of Rs. 1,670 be created against Bills discounted.

c. Goodwill of the firm is to be valued at 2.5 years' purchase of average profits of 2 years. The profits are as under: 2000:- Rs. 2,000 and 2001 - Rs. 6,000.

d. Drawings of Dinesh, Yasmine, and Faria were Rs. 2,750; Rs. 1,750; and Rs. 500 Respectively.

e. Machinery and Public Deposits are revalued to Rs. 2,000 and Rs. 1,000 respectively.

Prepare Revaluation Account, Partners' Capital Accounts and Balance Sheet of the new firm.

Solution 1

Books of Dinesh, Yamine, Farte and Anie

REVALUATION ACCOUNT

Particulars Rs. Assets Rs.

To Bills Discounted A/c 1670 By Public deposits A/c 190

By Machinery A/c 200

By Loss transferred to

Dinesh's capital A/c 704

Yasmine's Capital A/c 448

Faria's Capitla A/c 128 1280

1670 1670

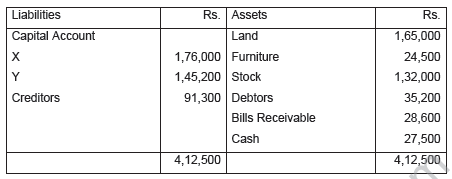

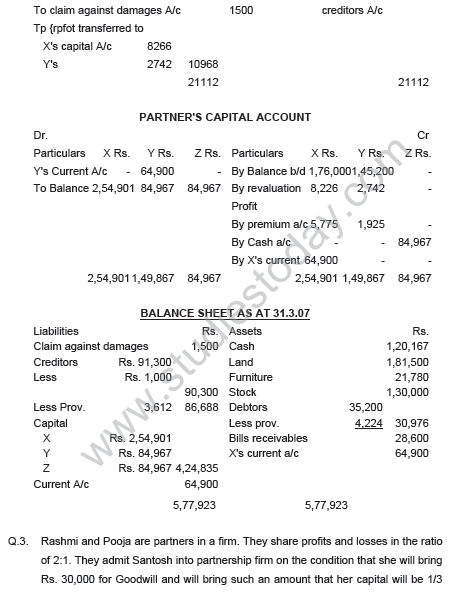

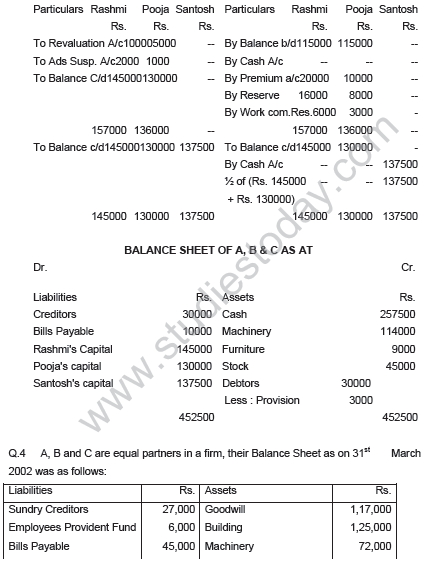

On the same date, Z is admitted into partnership for 1/5th share on the following terms

a. Goodwill is to be valued at 3½ years purchase of average profits of last for year which were Rs. 20,000 Rs. 17,000 Rs. 9,000 (Loss) respectively.

• Stock is fund to be overvalue by Rs. 2,000 Furniture is reduced and Land to be appreciated by 10% each, a provision for Bad Debts @ 12% is to be created on Debtors and a Provision of Discount of Creditors @ 4% is to be created.

• A liability to the extent of Rs. 1,500 should be created for a claim against the firm for damages.

• An item of Rs. 1,000 included in Creditors is not likely to be claimed, and hence it should be written off.

Prepare Revaluation Account, Partners: Capital Accounts and Balance Sheet of the new firm if Z is to contribute proportionate capital and goodwill. The capital of partners are to be in profit sharing ratio by opening current Accounts.

Solution 2

BOOK OF X, Y AND Z

REVALUATION ACCOUNT

Dr. Cr.

Particulars Amount Particulars Amount

To Stock A/c 2000 By land A/c 16500

To furniture A/c 2420 By creditors A/c 1000

To Provision for bad debts A/c 4224 By provision of discount on 3612

CASE STUDEY BASED QUESTIONS

Read the hypothetical text and answer the following questions.

X and Y started business on 1St April, 2020 with capitals of Rs. 5,00,000 each. As per the partnership Deed, both X and Y are to get monthly salary of Rs. 10,000 each and interest on capital is Rs. 50,000 each. Interest on drawings are as follows X : Rs. 3,000 and Y: Rs. 5,000.

During the year, the firm incurred a loss of Rs. 2,00,000.

Question: What is the total amount of salary to be credited to Partners’ capital account?

a) Rs. 1,20,000

b) Rs. 2,40,000

c) Rs. 1,80,000

d) No salary will be given

Answer: D

Question: What is the amount to be transferred to Profit and Loss Appropriation Account?

a) Rs. 5,00,000

b) Rs. 2,00,000

c) Rs. 3,00,000

d) Rs. 1,50,000

Answer: B

Question: What is the share of loss of X?

a) Rs. 1,00,000

b) Rs. 96,000

c) Rs. 98,000

d) Rs. 90,000

Answer: B

Question: What amount of loss is to be transferred to the capital account of the both partners?

a) Rs. 1,92,000

b) Rs. 2,00,000

c) Rs. 1,96,000

d) Rs. 1,80,000

Answer: A

Read the hypothetical text and answer the following questions.

Ajay and Vijay are partners sharing profits in the ratio of 3:2. Ajay is a non-working partner and contributes Rs. 20,00,000 as his capital. Vijay is a working partner of the firm. The Partnership Deed provides for interest on capital @ 8% p.a. and salary to every working partner @ Rs. 8,000 p.m. Profit before providing for interest on capital and partner’s salary for the year ended 31st March, 2021, was Rs. 80,000.

Question: What is the amount of salary payable to Vijay?

a) Rs. 96,000

b) Rs. 30,000

c) Rs. 60,000

d) Rs. 80,000

Answer: B

Question: How much interest on capital is payable to Ajay?

a) Rs. 50,000

b) Rs. 1,60,000

c) Rs.80,000

d) Rs. 1,00,000

Answer: A

Question: What is the amount of profit to credited to Ajay’s capital account?

a) Rs. 40,000

b) Rs. 60,000

c) Rs. 80,000

d) None of these

Answer: D

Question: What is the amount of net profit to be transferred to Profit and Loss Appropriation account?

a) Rs. 50,000

b) Rs. 30,000

c) Rs. 80,000

d) Rs. 60,000

Answer: C

Read the hypothetical text and answer the following questions.

X and Y are partners sharing profits and losses in the ratio of 7:3. Their capital accounts as at 1st April, 2018 stood at X: Rs. 5,00,000 and Y: Rs. 4,00,000. Partners are allowed interest on capital @ 5% p.a. Drawings of the partners during the year ended 31st March, 2019 were Rs. 72,000 and Rs. 50,000 respectively. Profit for the year before allowing interest on capital and salary to Y @ Rs. 5,000 p.m. was Rs. 8,00,000. 10% of the net profit is to be transferred to General Reserve.

Question: How much amount of interest on capital payable to both the partners?

a) Rs. 45,000

b) Rs. 60,000

c) Rs. 75,000

d) Rs.1,00,000

Answer: A

Question: What is the amount to be transferred to General reserve?

a) Rs. 1,60,000

b) Rs. 80,000

c) Rs. 40,000

d) Rs. 2,00,000

Answer: B

Question: What is the share of X in distributable profit?

a) Rs. 4,20,500

b) Rs. 4,30,500

c) Rs. 4,25,500

d) Rs. 4,10,500

Answer: B

Question: What is the amount of salary payable to Y?

a) Rs. 90,000

b) Rs. 1,20,000

c) Rs. 60,000

d) 75,000

Answer: C

Read the hypothetical text and answer the following questions.

A, B and C started a firm on 1st October, 2020 sharing profits equally. A drew regularly Rs. 4,000 in the beginning of every month for the six months ended 31st March, 2021. B drew regularly Rs. 4,000 at the end of every month for the six months ended 31st March, 2021. C drew regularly Rs. 4,000 in the middle of every month for the six months ended 31st March, 2021. IOD is charged at 5% p.a

Question: What is the interest on drawings of B?

Page 13 of 152

a) Rs. 350

b) Rs. 300

c) Rs. 200

d) Rs. 250

Answer: D

Question: What the total amount of drawings of the partners?

a) Rs. 1,44,000

b) Rs. 72,000

c) Rs. 24,000

d) 96,000

Answer: B

Question: What is the total amount of interest on drawings of the partners?

a) Rs. 1,200

b) Rs.1,500

c) Rs. 600

d) Rs. 900.

Answer: D

Question: What is the interest on drawings of A?

a) Rs. 300

b) Rs. 250

c) Rs. 350

d) Rs. 400

Answer: C

MCQ Questions for NCERT Class 12 Accountancy Fundamentals Of Partnership

Question: For the firm, interest on capital is :

(A) Capital Payment

(B) Capital Receipt

(C) Loss

(D) Income

Answer: C

Question: X and Y are partners in the ratio of 3 : 2. Their capitals are Rs.2,00,000 and Rs.1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of Rs.15,000 for the year ended 31st March 2019. Interest on Capital will be :

(A) X Rs.16,000; Y Rs.8,000

(B) X Rs.9,000; Y Rs.6,000

(C) X Rs.10,000; Y Rs.5,000

(D) No Interest will be allowed

Answer: C

Question: X and Y are partners in the ratio of 3 : 2. Their capitals areRs. 2,00,000 and Rs.1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm incurred a loss of Rs.60,000 for the year ended 31st March 2019. Interest on Capital will be :

(A) X Rs.16,000; Y Rs.8,000

(B) A Rs.8,000; Y Rs.4,000

(C) X Rs.14,400; Y Rs.9,600

(D) No Interest will be allowed

Answer: D

Question: X and Y are partners in the ratio of 3 : 2. Their capitals are Rs.2,00,000 and Rs.1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of Rs.60,000 for the year ended 31st March 2019. Interest on Capital will be :

(A) X Rs.16,000; Y Rs.8,000

(B) V Rs.8.000; Y Rs.4,000

(C) X Rs.14,400; Y Rs.9,600

(D) No Interest will be allowed

Answer: A

Question: X and Y are partners in the ratio of 3 : 2. Their capitals are Rs.2,00,000 and Rs.1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of Rs.15,000 for the year ended 31st March 2019. As per partnership agreement, interest on capital is treated a charge on profits. Interest on Capital will be :

(A) X Rs.16,000; Y Rs.8,000

(B) X Rs.9,000; Y Rs.6,000

(C) X Rs.10,000; Y Rs.5,000

(D) No Interest will be allowed

Answer: A

Question: Partners are suppose to pay interest on drawing only when_____ by the________.

(A) Provided, Agreement

(B) Permitted, Investors

(C) Agreed, Partners

(D) ‘A’ & ‘C’ above

Answer: D

Question: Where will you record interest on drawings :

(A) Debit Side of Profit & Loss Appropriation Accoun

(B) Credit Side of Profit & Loss Appropriation Account

(C) Credit Side of Profit & Loss Account

(D) Debit Side of Capital/Current Account only.

Answer: B

Question: A and B contribute Rs.1,00,000 and Rs.60,000 respectively in a partnership firm by way of capital on which they agree to allow interest @ 8% p.a. Their profit or loss sharing ratio is 3 : 2. The profit at the end of the year was Rs.2,800 before allowing interest on capital. If there is a clear agreement that interest on capital will be paid even in case of loss, then S’s share will be:

(A) Profit Rs.6,000

(B) Profit Rs.4,000

(C) Loss Rs.6,000

(D) Loss Rs.4,000

Answer: D

Question: If date of drawings of the partner’s is not given in the question, interest is charged for how much time

(A) 1 month

(B) 3 months

(C) 6 months

(D) 12 months

Answer: C

Question: How would you close the Partner’s Drawing Account:

(A) By transfer to Capital or Current Account Debit Side.

(B) By transfer to Capital Account Credit Side.

(C) By transfer to Current Account Credit Side.

(D) Either ‘B‘ or ‘C’.

Answer: A

Question: Vikas is a partner in a firm. His drawings during the year ended 31st March, 2019 were Rs.72,000. If interest on drawings is charged @ 9% p.a. the interest charged will be :

(A) Rs.324

(B) Rs.6,480

(C) Rs.3,240

(D) Rs.648

Answer: C

Question: If a fixed amount is withdrawn by a partner on the last day of every month, interest on the total amount is charged for …………… months :

(A) 12

(B) 6 1/2

(C) 5 1/2

(D) 6

Answer: C

Question: If a fixed amount is withdrawn by a partner on the first day of every month, interest on the total amount is charged for …………… months :

(A) 6

(B) 61/2

(C) 51/2

(D) 12

Answer: B

Question: In a partnership firm, a partner withdrew Rs.5,000 per month on the first day of every month during the year for personal expenses. If interest on drawings is charged @ 6% p.a. the interest charged will be

(A) Rs.3,600

(B) Rs.1,950

(C) Rs.1,800

(D) Rs.1,650

Answer: B

Question: If a fixed amount is withdrawn by a partner in the middle of every month, interest on the total amount is charged for …………… months

(A) 6

(B) 6 1/2

(C) 5 1/2

(D) 12

Answer: A

Question: Sushil is a partner in a firm. He withdrew Rs.4,000 per month in the middle of every month during the year ended 31st March, 2019. If interest on drawings is charged @ 8% p.a. the interest charged will be :

(A) Rs.2,080

(B) Rs.1,760

(C) Rs.3,840

(D) Rs.1,920

Answer: D

Question: Define partnership.

Answer: When two or more persons enter into an agreement to carry on business and share its profit and losses, it is a case of partnership. The Indian partnership Act, 1932, defines Partnership as follows:

"Partnership is the relation between persons and who have agreed to share the profits of a business carried on by all or any of them acting for all.

Question: What do you understand by 'partners', 'firm' and 'firms' name?

Answer: The persons who have entered in to a Partnership with one another are individually called 'Partners' and collectively 'a firm' and the name under which the business is carried is called 'the firm's name'.

Question: Write any four main features of partnership.

Answer: Essential elements or main features of Partnership :

i) Two or more persons: Partnership is an association of two or more persons.

ii) Agreement: The Partnership is established by an agreement either oral or in writing.

iii) Lawful Business: A Partnership formed for the purpose of carrying a business, it must be a legal business.

iv) Profit sharing: Profit of the firm is share by the partners in an agreed ration, if the ratio is not agreed then equally. Profit also includes loss.

Question: What is the minimum and maximum number of partners in all partnership?

Answer: There should be at least two persons to form a Partnership. The maximum number of Partners in a firm carrying an banking business should not exceed ten and in any other business should not exceed ten and in any other business it should not exceed twenty.

Question: What is the status of partnership from an accounting viewpoint?

Answer: From an accounting viewpoint, partnership is a separate business entity. From legal viewpoints, however, a Partnership, like a sole proprietorship, is not separate from the owners.

Question: What is meant by partnership deed?

Answer: Partnership deed is a written agreement containing the terms and conditions agreed by the Partners.

Question: In the absence of a partnership deed, how are mutual relations of partners governed?

Answer: In the absence of Partnership deed, mutual relations are governed by the Partnership Act, 1932.

Question: Give any two reason in favour of having a partnership deed.

Answer: i) In case of any dispute or doubt, Partnership deed is the guiding document.

ii) It can specify the duties and powers of each Partner.

Question: State the provision of 'Indian partnership Act 1932‘ relating to sharing of profits in absence of any provision in the partnership deed.

Answer: In the absence of any provision in the Partnership deed, profit or losses are share by the Partners equally.

Question: Why is it important to have a partnership deed in writing?

Answer: Partnership deed is important since it is a document defining relationship of among Partners thus is assistance in settlement of disputes, if any and also avoids possible disputes: it is good evidence in the court.

Question: What do you understand by fixed capital of partners?

Answer: Partners' capital is said to be fixed when the capital of Partners remain unaltered except in the case where further capital is introduced or capital is withdrawn permanently.

Question: What do you understand by fluctuating capital of partners?

Answer: Partner‘s capital is said to be fluctuating when capital alters with every transaction in the capital account. For example, drawing, credit of interest, etc

Question: Give two circumstances in which the fixed capital of partners may change.

Answer: Two circumstances in which the fixed capital of Partners may change are :

i) When additional capital is introduced by the Partners.

ii) When a part of the capital is permanently withdrawn by the Partners.

Question: List the items that may appear on the debit side and credit side of a partner's fluctuating capital account.

Answer: On debit side: Drawing, interest on drawing, share of loss, closing credit balance of the capital. On credit side : Opening credit balance of capital, additional capital introduced, share of profit, interest on capital, salary to a Partner, commission to a Partner.

Question: How will you show the following in case the capitals are?

i) Fixed and ii) Fluctuating

a) Additional capital introduced

b) Drawings

c) Withdrawal of capital

d) Interest on capital and

e) Interest on loan by partners?

Answer: i) In case, capitals are fixed:

a) On credit side of capital

(b) on debit side of current A/c

(c) on debit side of capital A/c

(d) on credit side of current A/c

(e) on credit side of loan from partner's A/c.

Question: If the partners capital accounts are fixed, where will you record the following items :

i) Salary to partners

ii) Drawing by a partners

iii) Interest on capital and

iv) Share of profit earned by a partner?

Answer: i) Credit side of Partner's current A/c

ii) Debit side of Partner's current A/c

iii) Credit side of Partners current A/c

iv) Credit side of Partners current A/c

Question: How would you calculate interest on drawings of equal amounts drawn on the Last day of every month?

Answer: When a partners draws a fixed amount at the beginning of each month, interest on total drawing would be on the amount withdraw for 6.5 months at the agreed rate of interest per annum. Apply the following formula.

Question: How would you calculate interest on drawing of equal amounts drawn on the last day of every month?

Answer: When drawing of fixed amounts are made at regular monthly intervals on the day of every month, Interest would be charged on the amount withdrawn at the agreed rate of interest for 5.5 months. Apply the following formula. :

Question: How would you calculate interest on drawing of equal amount drawn in the middle of every month?

Question: Ramesh, a partner in the firm has advanced a loan of a Rs. 1,00,000 to the firm and has demanded on interest @ 9% per annum. The partnership deed is silent on the matter. How will you deal with it?

Answer: Since the Partnership deed is silent on payment of interest, the provisions of the Partnership Act, 1932 will apply. Accordingly, Ramesh is entitled to interest @ 6% p.a.

Question: The partnership deed provides that Anjali, the partner will get Rs. 10,000 per month as salary. But, the remaining partners object to it. How will this matter be resolved?

Answer: No, he is not entitled to the salary because it is not so, Provided in the Partnership deed and according to the Partnership act, 1932 if the Partnership deed does not provided for payment of salary to Partners, he will not be entitled to it.

Q.23 Distinction between Profit and loss and profit and loss appropriation account:

PROBLEMS BASED ON FUNDAMENTALS

Question: A, B, and C were partners in a firm having no partnership agreement. A, B and C contributed Rs.2, 00,000, Rs.3, 00,000 and 1, 00,000 respectively. A and B desire that the profits should be divided in the ratio of capital contribution. C does not agree to this. How will the dispute be settled?

Answer: C is correct because in the absence of Partnership deed the profits are to be shared equally.

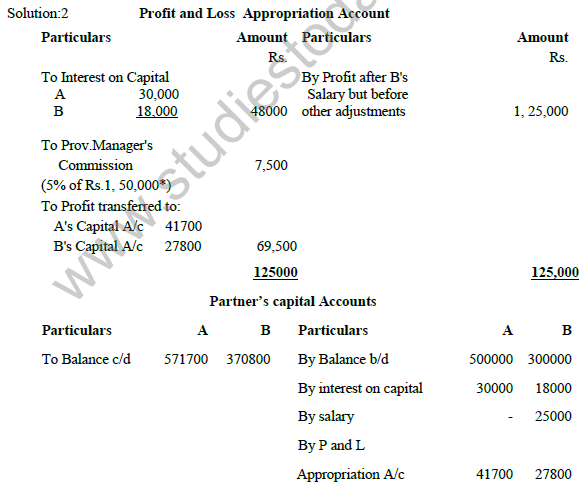

Question: A and B are partners sharing profits in the ratio of 3: 2 with capitals of Rs. 5, 00,000 and Rs. 3, 00,000 respectively. Interest on capital is agreed @ 6% p.a. B is to be allowed an annual salary of Rs. 25000. During 2006, the profits of the year prior to calculation of interest on capital but after charging B's salary amounted to Rs. 1,25,000. A provision of 5% of the profits is to be made in respect of Manager's commission. Prepare an account showing the allocation of profits and partners' capital accounts.

571700 370800 571700 370800

Question: X and Y are partners sharing profits and losses in the ratio of 3: 2 with capitals of Rs. 50,000 and Rs. 30,000 respectively. Each partner is entitled to 6% interest on his capital. X is entitled to a salary of Rs. 800 per month together with a commission of 10% of net 'Profit remaining after deducting interest on capitals and salary but before charging any commission. Y is entitled to a salary of Rs. 600 per month together I. with-a commission of 10% of Net profit remaining after deducting interest on capitals and salary and after charging all commissions. The profits for the year prior to calculation of interest on capital but after charging salary of partners amounted to Rs. 40,000. Prepare partners' Capital

Accounts:-

(i) When capitals are fixed, and

(ii) When capitals are. Fluctuating.

Note: (1) Calculation of interest on Capital: Interest for 3 months i.e. from 1st April to 30th June, 2004

A B

A on Rs. 5,00,000 @ 10% p.a. 12500

B on Rs. 3,00,000 @ 10% p.a. 7500

Interest for 9 months i.e. from 1st July, 2004 to 31st March, 2005:

A on Rs. 3,50,000 @ 10% p.a. 26250

B on Rs. 3,50,000 @ 10% p.a. 26250

Question: Give the answer to the following:

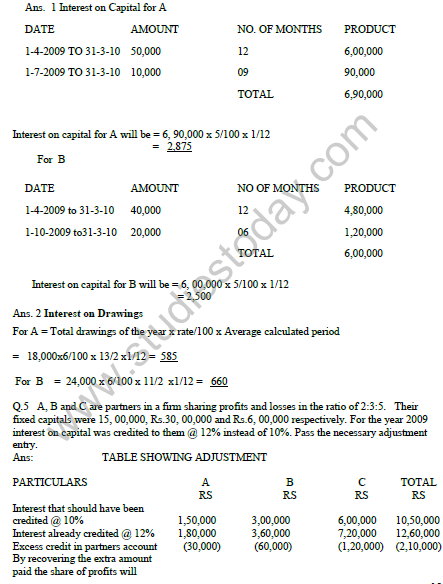

(1) P and Q are partners sharing profits and losses in the ratio of 3:2. On 1st April 2009 their capital balances were Rs.50, 000 and 40,000 respectively. On 1st July 2009 P brought Rs.10, 000 as his additional capital whereas Q brought Rs.20, 000 as additional capital on 1st October 2009. Interest on capital was provided @ 5% p.a. Calculate the interest on capital of P and Q on 31st March 2010.

(2) A and B are partners sharing profits and losses in the ratio of 2:1. A withdraws Rs.1500 at the beginning of each month and B withdrew Rs. 2000 at the end of each month for 12 months. Interest on drawings was charged @ 6% p.a. Calculate the interest on drawings of A and B for the year ended 31st December 2009.

(2) Profits for 2008 were Rs. 30,000 and profits of Rs. 20,000· are, shown in the Balance Sheet, which means only Rs. 10,000 profits were distributed between the partners.

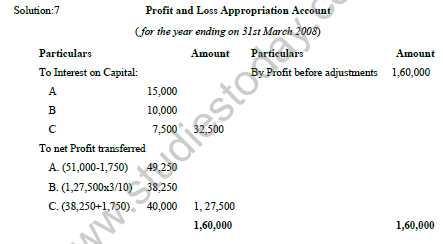

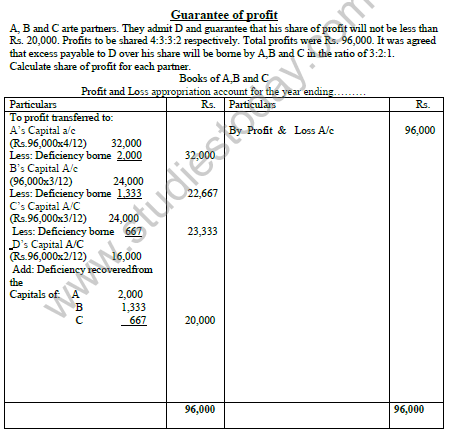

Question: A, B and C entered into partnership on 1st April, 2008 to share profits & losses in the ratio of 4:3:3. A, however, personally guaranteed that C's share of profit after charging interest on Capital @ 5% p.a. would not be less than Rs. 40,000 in any year. The Capital contributions were:

A, Rs. 3, 00,000; B, Rs. 2, 00,000 and C, Rs. 1, 50,000.

The profit for the year ended on 31st March, '2008 amounted to Rs. 1, 60,000. Show the Profit & Loss Appropriation Account.

Question: A, and C are partners with fixed capitals of Rs. 2,00,000, Rs. 1,50,000 and Rs. 1,00,000 respectively. The balance of current accounts on 1st January, 2004 were A Rs. 10,000 (Cr.); B Rs. 4,000 (Cr.) and C Rs. 3,000 (Dr.). A gave a loan to the firm of Rs. 25,000 on 1st July, 2004. The Partnership deed provided for the following:-

(i) Interest on Capital at 6%.

(ii) Interest on drawings at 9%. Each partner drew Rs. 12,000 on 1st July, 2004.

(iii) Rs. 25,000 is to be transferred in a Reserve Account.

(iv) Profit sharing ratio is 5:3: 2 up to Rs. 80,000 and above Rs. 80,000 equally. Net Profit of the firm before above adjustments was Rs. 1,98,360. From the above information prepare Profit and Loss Appropriation Account, Capital and Current Accounts of the partners.

(i) If the rate of interest on Partners' Loan is not given in the question, it is to be wed @ 6% p.a. according to the Partnership Act.

(ii) Interest on Partners' Loan is treated as a charge against Profit, so it is shown in the debit of Profit and Loss A/c.

(iii) If the date of Drawings is not given in the question, interest on drawings will be charged and average period of 6 months.

(iv) Reserve Fund is calculated at 10% on Rs. 3,00,000 (i.e. Rs. 4,26,800 + Rs. 5,200- 12,000 - Rs. 60,000 - Rs. 60,000.

CASE STUDEY BASED QUESTIONS

Read the hypothetical text and answer the following questions .:

P and Q were partners in a firm sharing profits and losses equally. Their fixed capitals were Rs. 1,00,000 and Rs. 50,000 respectively. The partnership deed provided that interest on capital is to be given @ 10% p.a. For the year ended 31.03.2016, the profits of the year were distributed without providing interest on capital.

Question:How much amount should be credited to P’s current account for Interest on capital?

a) Rs. 8,000

b) Rs. 10,000

c) Rs. 9,000

d) Rs. 7,000

Answer: B

Question: How much amount is already debited to P’s current account?

a) 2,500

b) Rs. 3,000

c) Rs. 7,500

d) Rs. 1,500

Answer: C

Question: What was the amount of past adjustment entry?

a) Rs. 2,500

b) Rs. 1,500

c) Rs. 1,200

d) Rs. 1,600

Answer: A

Question: How much amount should be credited to Q’s current account for interest on capital?

a) Rs. 2,000

b) Rs. 3,000

c) Rs. 5,000

d) Rs.4,000

Answer: C

Read the hypothetical text and answer the following questions.

Aman and Boman are partners sharing profits equally. Business is being carried from the property owned by Aman on a yearly rent of Rs. 24,000. Aman is to get salary of Rs. 1,20,000 p.a. and Boman is to get commission @ 5% on net sales, which during the was Rs. 30,00,000.

Profits for the year ended 31st March, 2019 before providing rent was Rs. 5,00,000.

Question: What is the profit after charging rent?

a) Rs. 4,00,000

b) Rs. 3,00,000

c) Rs. 4,76,000

d) Rs.5,00,000

Answer: C

Question:. What is the amount of commission payable to Boman?

a) Rs. 1,50,000

b) Rs. 2,00,000

c) Rs. 1,20,000

d) Rs. 1,00,000

Answer: A

Question: What is the amount of profit to be credited to Aman’s capital account?

a) Rs. 1,00,000

b) Rs. 1,03,000

c) Rs. 1,02,000

d) Rs. 1,05,000

Answer: B

Question: What is the total distributable profit?

a) Rs. 1,06,000

b) Rs. 2,06,000

c) Rs. 1,00,000

d) Rs. 2,00,000

Answer: B

Read the hypothetical text and answer the following questions .:

Amit, Bimal and Chaman are sharing profits and losses equally. Amit and Chaman have given loan to the firm on 1st October, 2018 of Rs. 1,00,000 and Rs. 1,50,000 respectively. It is agreed that interest @ 9% p.a. will be paid on loan. Books of account of the firm are closed on 31st March, every year. Interest on loan is yet to be paid as on 31st March, 2019.

Question: How much interest the partner Chaman will get on his loan amount?

a) Rs. 4,500

b) Rs. 6,750

c) Rs. 6,000

d) Rs. 5,500

Answer: B

Question: How much interest the partner Amit will get on his loan amount?

a) Rs. 4,500

b) Rs.3,000

c) Rs. 2,500

d) Rs. 1,500

Answer: A

Question: What is the total amount of interest on loan of both the partners?

a) Rs. 10,250

b) Rs. 11,250

c) Rs. 12,250

d) Rs.13,750

Answer: B

Question: What is the credit balance of Amit’s loan account after adjustments?

a) Rs. 1,00,000

b) Rs. 1,02,500

c) Rs. 1,04,000

d) Rs. 1,04,500

Answer: D

Unit 1:

ACCOUNTING FOR PARTNERSHIP FIRMS: BASIC CONCEPTS

Question: State the conditions under which capital balances may change under the system of a Fixed Capital Account.

Answer: (i) When additional capital is introduced.

(ii) When capital is withdrawn.

Question: A is partner in a firm. His capital as on Jan 01, 2007 was Rs. 60,000. He introduced additional capital of Rs. 20000 on Oct 01 2007. Calculate interest on A‘s capital @ 9% p.a.

Answer: 2 60000 X 9/100 = 5400

20000 X 9/100 X 3/12 = 450

Total Interest 5850

Question: A, B and C are partners in a firm having no partnership agreement. A, B and C contributed Rs. 20,000, Rs. 30,000 and Rs. 1,00,000 respectively. A and B desire that the profit should be divided in the ratio of capital contribution. C does not agree to this. How will you settle the dispute.

Answer: C is correct as in the absence of partnership agreement, profits and losses are divided equally among partners.

Question: A and B are partners in a firm without a partnership deed. A is an active partner and claims a salary of Rs. 18,000 per month. State with reason whether the claim is valid or not.

Answer: A‘s claim is not valid as in the absence of partnership deed, no salary is allowed to partners.

Question: Chandar and Suman are partners in a firm without a partnership deed. Chandar‘s capital is Rs. 10,000 and Suman‘s capital is Rs. 14,000. Chander has advanced a loan of Rs. 5000 and claim interest @ 12% p.a. State whether his claim is valid or not.

Answer: Chander‘s claim is not valid as in the absence of partnership deed interest on partners loan is provided @ 6% p.a.

Question: R, S, and T entered into a partnership of manufacturing and distributing educational CD‘s on April 01, 2006. R looked after the business development, S content development and T financed the project. At the end of the year (31-03-2007) T wanted an interest of 12% on the capital employed by him. The other partners were not inclined to this. How would you resolve this within the ambit of the Indian Partnership Act, 1932?

Answer: As per provision of Indian Partnership act 1932, when there is no partnership, no partner is entitled for interest on his capital contribution.

Question: A, B and C are partners in a firm. A withdrew Rs. 1000 in the beginning of each month of the year. Calculate interest on A‘s drawing @ 6% p.a.

Answer: Interest on drawing = 12000 X 6/100 X 6.5/12 = 390

Question: A, B and C are partners in a firm, B withdrew Rs. 800 at the end of each month of the year. Calculate interest on B‘s drawings @ 6% p.a.

Answer: Interest on drawing = 9600 X 6/100 X 5.5/12 = 264

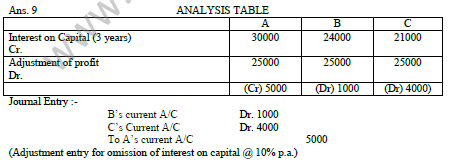

Question: A, B and C are partners in a firm. They have omitted interest on capital @ 10 % p.a. for three years ended 31st march 2007. Their fixed capitals on which interest was to be calculated through –out were

A Rs. 1,00,000

B Rs. 80,000

C Rs. 70,000

Give the necessary Journal entry with working notes.

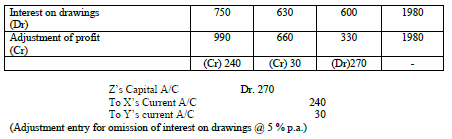

Question: X, Y, and Z are partners sharing profits and losses in the ratio of 3:2:1. After the final accounts have been prepared it was discovered that interest on drawings @ 5 % had not been taken into consideration. The drawings of the partner were X Rs. 15000, Y Rs. 12,600, Z Rs. 12,000. Give the necessary adjusting Journal entry.

![]()

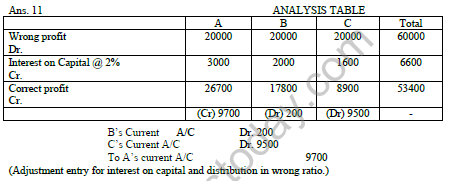

Question: A, B and C are partners sharing profits and losses in the ratio of 3:2:1. Their fixed capitals are Rs. 1,50,000, Rs. 1,00,000 and Rs. 80,000 respectively. Profit for the year after providing interest on capital was Rs. 60,000, which was wrongly transferred to partners equally. After distribution of profit it was found that interest on capital provided to them @ 10% instead of 12% . Pass necessary adjustment entry. Show your working clearly.

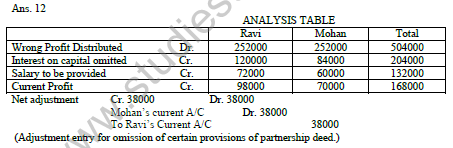

Question: Ravi and Mohan were partner in a firm sharing profits in the ratio of 7:5. Their respective fixed capitals were Ravi Rs. 10,00,000 and Mohan Rs. 7,00,000. The partnership deed provided for the following:-

(i) Interest on capital @ 12% p.a.

(ii) Ravi‘s salary Rs. 6000 per month and Mohan‘s salary Rs. 60000 per year.

The profit for the year ended 31-03-2007 was Rs. 5,04,000 which was distributed equally without providing for the above. Pass an adjustment Entry.

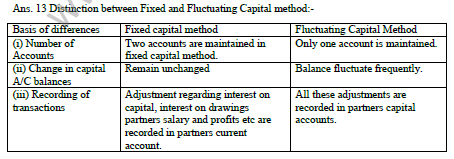

Question: Distinguish between fixed capital method and fluctuating capital method.

Question: A, B and C were partners in a firm having capitals of Rs. 60,000, Rs. 60,000 and Rs. 80,000 respectively. Their current account balances were A- Rs. 10,000, B- Rs. 5000 and C- Rs. 2000 (Dr.). According to the partnership deed the partners were entitled to an interest on capital @ 5% p.a. C being the working partner was also entitled to a salary of

Rs. 6,000 p. a. The profits were to be divided as follows:

(i) The first Rs. 20,000 in proportion to their capitals.

(ii) Next Rs. 30,000 in the ratio of 5:3:2.

(iii) Remaining profits to be shared equally.

During the year the firm made a profit of Rs. 1,56,000 before charging any of the above items. Prepare the profit and loss appropriate on A/C.

Answer: 14 Profit transferred to A‘s current A/C Rs. 51,000

B‘s current A/C Rs. 45,000

C‘s current A/C Rs. 44,000

Question: A and B are partners sharing profits in proportion of 3:2 with capitals of Rs. 40,000 and Rs. 30,000 respectively. Interest on capital is agreed at 5 % p.a. B is to be allowed an annual salary of Rs. 3000 which has not been withdrawn. During 2001 the profits for the year prior to calculation of interest on capital but after charging B‘s salary amounted to Rs. 12,000. A provision of 5% of this amount is to be made in respect of commission to the manager.

Prepare profit and loss appropriation account showing the allocation of profits.

Answer: 15 Net profit transferred to A‘s Capital A/C Rs. 4,650

B‘s Capital A/C Rs. 3,100

CASE STUDEY BASED QUESTIONS

Read the hypothetical text and answer the following questions.

Arun, Varun and Tarun were partners in a firm sharing profits equally. On 1st April, 2020, their capitals stood at Rs. 2, 00,000, Rs. 1, 50,000 and Rs. 1, 00,000 respectively. As per the provisions of Partnership Deed:

1) Arun was entitled to a salary of Rs. 2,500 p.m.

2) Partners were entitled to interest on capital @ 10% p.a.

The net profit for the year ended 31st March, 2021, Rs. 1,50,000 was distributed among the partners without providing for the above items.

Question: What is the amount of distributable profit for the partners after providing salary and interest on capitals to the partners?

a) Rs. 50,000 each

b) Rs. 25,000 each

c) Rs. 10,000 each

d) Rs. 15,000 each

Answer:B

Question: Capital Account/Accounts of …………………… will be debited to give the effect of above adjustments.

a) Varun

b) Tarun and Arun

c) Arun and Varun

d) Varun and Tarun

Answer: D

Question: Arun’s Capital A/c will be credited with Rs…………….for giving the adjustment to above omissions.

a) Rs. 20,000

b) Rs. 15,000

c) Rs. 25,000

d) Rs. 10,000

Answer: C

Question: What is the amount of interest on capital of Varun?

a) Rs. 20,000

b) Rs. 15,000

c) Rs. 10,000

d) Rs. 30,000

Answer: A

Read the hypothetical text and answer the following questions .

Sonu and Monu are partners sharing profits and losses in the ratio of 2:1. Their capital Accounts as at 1st April, 2015 were Rs. 10,00,000 and Rs. 8,00,000 respectively. The partners are allowed interest on capital @ 5% p.a. Drawings of the partners during the year ended 31st March, 2016 were Rs. 1,44,000 and Rs. 1,00,000 respectively. Monu is entitled to get a salary of Rs. 10,000 p.m.

Profit for the year before allowing interest on capital and salary was Rs. 16,00,000. 10% of the net profit is to be transferred to General Reserve.

Question: What is the distributable amount of profit which is to be credited to Partners’ Capital Accounts?

a) Rs. 16,00,000

b) Rs. 14,40,000

c) Rs. 12,30,000

d) Rs. 10,00,000

Answer: C

Question: Find the closing capital of Sonu?

a) Rs. 12,70,000

b) Rs. 17,26,000

c) Rs. 16,00,000

d) Rs. 10,00,000

Answer: C

Question: What is the share of Monu’s profit to be credited to his Capital Account?

a) Rs. 14,40,000

b) Rs. 12,30,000

c) Rs. 4,10,000

d) Rs. 8,20,000

Answer: C

Read the hypothetical text and answer the following questions.

Mahesh, Dinesh and Suresh are equal partners with capitals of Rs. 5,00,000, Rs. 3,00,000 and Rs. 2,00,000 respectively. Mahesh withdrew Rs. 60,000 in the beginning of each quarter for the year ended 31st March, 2020. Dinesh withdrew Rs. 60,000 at the end of each quarter for the year ended 31st March,2020. Suresh withdrew Rs. 90,000 in the middle of each quarter for the year ended 31st March,2020. Interest on drawings is charged @ 10% p.a.

Question: What is the total amount of drawings of all the partners?

a) Rs. 9,00,000

b) Rs. 8,40,000

c) Rs. 8,60,000

d) Rs. 9,20,000

Answer: B

Question: Mahesh’s interest on drawings is………………………….

a) Rs. 12,000

b) Rs. 13,500

c) Rs. 10,000

d) Rs. 15,000

Answer: D

Question: What is the average period of Dinesh’s drawings?

a) 4.5 months

b) 6 months

c) 7.5 months

d) 12 months

Answer: A

Question: What is the total amount of interest on drawings of all the partners?

a) Rs. 42,000

b) Rs. 40,000

c) Rs. 45,000

d) Rs. 48,000

Answer: A

Read the hypothetical text and answer the following questions .

Anil and Sunil started a firm on 1st April, 2020 sharing profits equally. Anil withdrew regularly Rs. 2,000 in the beginning of every month for the year ended 31St March, 2021 and Sunil withdrew the amount as follows.

On 1st July,2020: Rs. 8,000

On 1st October, 2020: Rs. 10,000

On 1St February, 2021: Rs. 6,000

As per Partnership Deed, interest on drawings is to be charged @ 10% p.a.

Question: Anil’s interest on drawings is …………………..

a) Rs. 1,100

b) Rs. 1,200

c) Rs. 1,300

Page 6 of 152

d) Rs. 1,400

Answer: C

Question: What is the total amount of drawings of Anil and Sunil?

a) Rs. 46,000

b) Rs. 48,000

c) Rs. 50,000

d) Rs. 52,000

Answer: B

Question: What is the average time period of Anil’s drawings?

a) 5.5 months

b) 6 months

c) 6.5 months

d) 12 months

Answer: C

Question: Sunil’s interest on drawings is ………………….

a) Rs. 1,000

b) Rs. 1,200

c) Rs. 1,400

d) Rs. 1,600

Answer: B

Read the hypothetical text and answer the following questions.

Amar, Saleem and John are partners without a Partnership Deed. On 1st April, 2020, their capitals were Rs. 3,00,000, Rs. 2,00,000 and Rs. 1,00,000 respectively. During the year, they withdrew Rs. 30,000, Rs. 20,000 and Rs. 10,000 respectively.

On 1st October, 2020, Saleem gave a loan of Rs. 50,000 to the firm and demands interest on loan @ 10% p.a. for the year ended 31st March, 2021.

John wants to admit a new partner, Vinod but Amar and Saleem do not agree for it.

Amar demands a salary of Rs. 1,000 p.m. for the year for taking part in business of the firm.

For the year ended 31st March, 2021, the firm earned a profit of Rs. 60,000.

Question: Find the amount to be given to Amar as salary.

a) Rs. 10,000

b) Rs. 12,000

c) Rs. 9,000

d) No salary will be given

Answer: D

Question: Interest on Saleem’s loan is ………………………

a) Rs. 5,000

b) Rs. 2,500

c) Rs. 3,000

d) Rs. 1,500

Answer:D

Question: Vinod can be admitted as a new partner in the firm when…………………….

a) John agrees to admit him as a new partner.

b) John and Saleem agree to admit him as a new partner.

c) All the existing partners agree to admit him as a new partner.

d) There is no need of other partners’ consent.

Answer: C

Question: What is the distributable profit for each partner?

a) Rs. 20,000 each

b) Rs. 19,500 each

c) Rs. 30,000, Rs. 20,000 and Rs. 10,000

d) Rs. 30,000, Rs. 15,000 and Rs. 15,000

Answer: B

Read the hypothetical text and answer the following questions.

Umesh and Mahesh are partners in a firm. On 1st April, 2020, their capitals were Rs. 4,00,000 and Rs. 6,00,000. The profit for 2020-21 was Rs. 5,24,000. Partnership Deed provided that interest on drawings/capital to be calculated @ 10%, Mahesh had withdrawn Rs. 1,00,000 on 31st December,2020. In addition to it, rent (in case of any partner providing his premises for business) for premises decided to be Rs. 8,000 per month. Due to lockdown during pandemic, the partners decided to shut down the factory and shifted to Umesh’s farmhouse on 1st August, 2020.

Question: What is the interest on drawings of Mahesh?

a) Rs. 10,000

b) Rs. 7,500

c) Rs. 2,500

d) Rs. 3,000

Answer: C

Question: What amount is to be transferred to Profit and Loss Appropriation Account?

a) Rs. 5,24,000

b) Rs. 5,00,000

c) Rs. 4,88,000

d) Rs. 4,60,000

Answer: D

Question: What is net distributable profit?

a) Rs. 5,00,000

b) Rs. 3,62,500

c) Rs. 5,02,500

d) Rs. 4,02,500

Answer: C

Question: What is total interest on capitals of both partners?

a) Rs. 1,00,000

b) Rs. 50,000

c) Rs. 2,00,000

d) Rs. 1,25,000

Answer: A

Read the hypothetical text and answer the following questions.

Mohan and Sohan are equal partner Their capitals as on 1St April,2020 are 1,00,000 and 2,00,000 respectively. Profits for the year 2020-21 were Rs. 90,000. As per the agreement, interest on capitals was Rs. 10,000 and Rs. 20,000 respectively and interest on drawings was Rs. 6,000 and Rs. 10,000 respectively. Mohan’s salary was Rs. 2,000 p.m. and Sohan’s salary was Rs. 5,000 p.a.

Accountant, however, committed the mistake and credited the profit in the capital ratio,Without interest on capitals, drawings and salary.

Question: What was the total salary required to be credited?

a) Rs. 70,000

b) Rs. 84,000

c) Rs. 29,000

d) 48,000

Answer: C

Question: With what amount was Sohan’s account credited with initially?

a) Rs. 30,000

b) Rs. 45,000

c) Rs. 60,000

d) 90,000

Answer: C

Question: What was the rate of interest on capital?

a) 5%

b) 10%

c) 15%

d) 20%

Answer: B

Question: What was the amount of past adjustment entry?

a) Rs. 20,500

b) Rs. 21,500

c) Rs.23,500

d) Rs. 22,500

Answer: B

| CBSE Class 12 Accountancy HOTs Accounting for Debentures |

| CBSE Class 12 Accountancy HOTs Partnership Basic Concepts |

| CBSE Class 12 Accountancy HOTs Admission Of A Partner |

| CBSE Class 12 Accountancy HOTs Death Retirement Of A Partner |

| CBSE Class 12 Accountancy HOTs Dissolution of A partnership firm |

| CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation |

| CBSE Class 12 Accountancy HOTs Accounting For Share Capital |

| CBSE Class 12 Accountancy HOTs Issue And Redemption of Debentures |

| CBSE Class 12 Accountancy HOTs Financial Statements of a Company |

| CBSE Class 12 Accountancy HOTs Analysis of Financial Statement |

| CBSE Class 12 Accountancy HOTs Accounting Ratios |

| CBSE Class 12 Accountancy HOTs Cash Flow Statement |

More Study Material

CBSE Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts HOTS

We hope students liked the above HOTS for Part 1 Chapter 2 Accounting for Partnership Basic Concepts designed as per the latest syllabus for Class 12 Accountancy released by CBSE. Students of Class 12 should download the High Order Thinking Skills Questions and Answers in Pdf format and practice the questions and solutions given in above Class 12 Accountancy HOTS Questions on daily basis. All latest HOTS with answers have been developed for Accountancy by referring to the most important and regularly asked topics that the students should learn and practice to get better score in school tests and examinations. Studiestoday is the best portal for Class 12 students to get all latest study material free of cost.

HOTS for Accountancy CBSE Class 12 Part 1 Chapter 2 Accounting for Partnership Basic Concepts

Expert teachers of studiestoday have referred to NCERT book for Class 12 Accountancy to develop the Accountancy Class 12 HOTS. If you download HOTS with answers for the above chapter daily, you will get higher and better marks in Class 12 test and exams in the current year as you will be able to have stronger understanding of all concepts. Daily High Order Thinking Skills questions practice of Accountancy and its study material will help students to have stronger understanding of all concepts and also make them expert on all critical topics. You can easily download and save all HOTS for Class 12 Accountancy also from www.studiestoday.com without paying anything in Pdf format. After solving the questions given in the HOTS which have been developed as per latest course books also refer to the NCERT solutions for Class 12 Accountancy designed by our teachers

Part 1 Chapter 2 Accounting for Partnership Basic Concepts HOTS Accountancy CBSE Class 12

All HOTS given above for Class 12 Accountancy have been made as per the latest syllabus and books issued for the current academic year. The students of Class 12 can refer to the answers which have been also provided by our teachers for all HOTS of Accountancy so that you are able to solve the questions and then compare your answers with the solutions provided by us. We have also provided lot of MCQ questions for Class 12 Accountancy in the HOTS so that you can solve questions relating to all topics given in each chapter. All study material for Class 12 Accountancy students have been given on studiestoday.

Part 1 Chapter 2 Accounting for Partnership Basic Concepts CBSE Class 12 HOTS Accountancy

Regular HOTS practice helps to gain more practice in solving questions to obtain a more comprehensive understanding of Part 1 Chapter 2 Accounting for Partnership Basic Concepts concepts. HOTS play an important role in developing an understanding of Part 1 Chapter 2 Accounting for Partnership Basic Concepts in CBSE Class 12. Students can download and save or print all the HOTS, printable assignments, and practice sheets of the above chapter in Class 12 Accountancy in Pdf format from studiestoday. You can print or read them online on your computer or mobile or any other device. After solving these you should also refer to Class 12 Accountancy MCQ Test for the same chapter

CBSE HOTS Accountancy Class 12 Part 1 Chapter 2 Accounting for Partnership Basic Concepts

CBSE Class 12 Accountancy best textbooks have been used for writing the problems given in the above HOTS. If you have tests coming up then you should revise all concepts relating to Part 1 Chapter 2 Accounting for Partnership Basic Concepts and then take out print of the above HOTS and attempt all problems. We have also provided a lot of other HOTS for Class 12 Accountancy which you can use to further make yourself better in Accountancy.

You can download the CBSE HOTS for Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts for latest session from StudiesToday.com

Yes, you can click on the link above and download topic wise HOTS Questions Pdfs for Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 for Accountancy

Yes, the HOTS issued by CBSE for Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts have been made available here for latest academic session

You can easily access the link above and download the Class 12 HOTS Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts for each topic

There is no charge for the HOTS and their answers for Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 CBSE Accountancy you can download everything free

HOTS stands for "Higher Order Thinking Skills" in Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 Accountancy. It refers to questions that require critical thinking, analysis, and application of knowledge

Regular revision of HOTS given on studiestoday for Class 12 subject Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts can help you to score better marks in exams

Yes, HOTS questions are important for Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 Accountancy exams as it helps to assess your ability to think critically, apply concepts, and display understanding of the subject.